Yes, the US economy has been greatly overstimulated by the Federal government (fiscal stimulus) and The Federal Reserve (monetary stimulus). This has caused inflation that we haven’t seen in a long time.

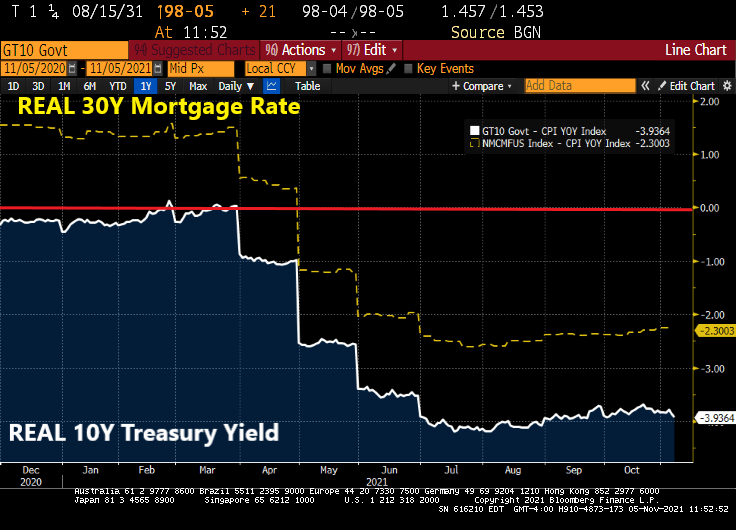

How overstimulated in the economy? The REAL 10-year Treasury yield (nominal less CPI YoY) is now -3.9364% and the 30-year REAL mortgage rate is -2.30%.

If The Federal Reserve is actually looking to achieve full employment in the USA, then it is a fool’s errand.

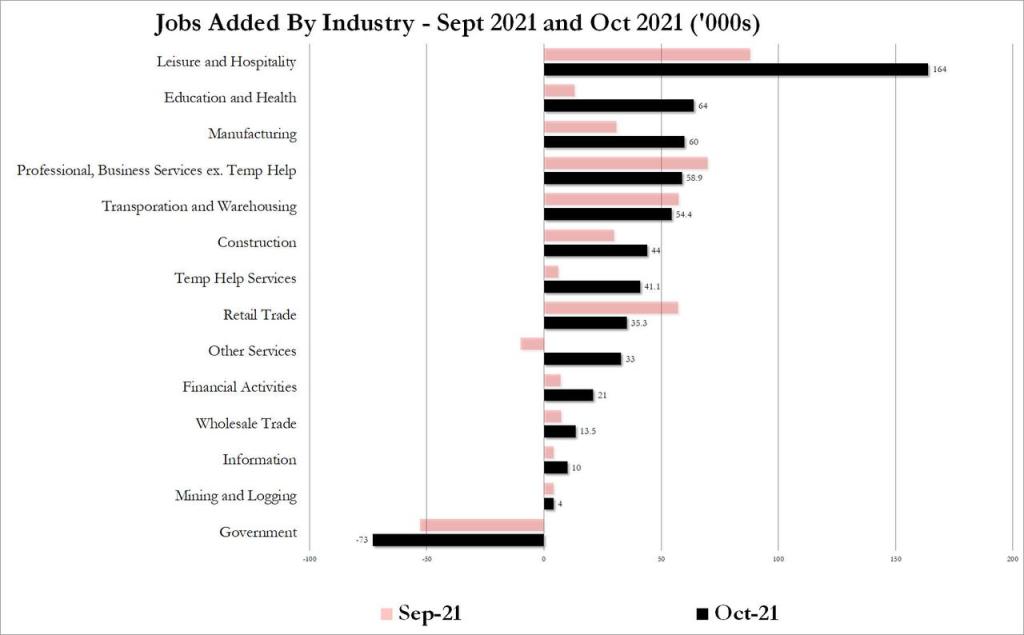

Today’s jobs report is both good and bad. The good news? 531k jobs were added, more than expected. The U-3 unemployment rate fell to 4.6%, also better than expected.

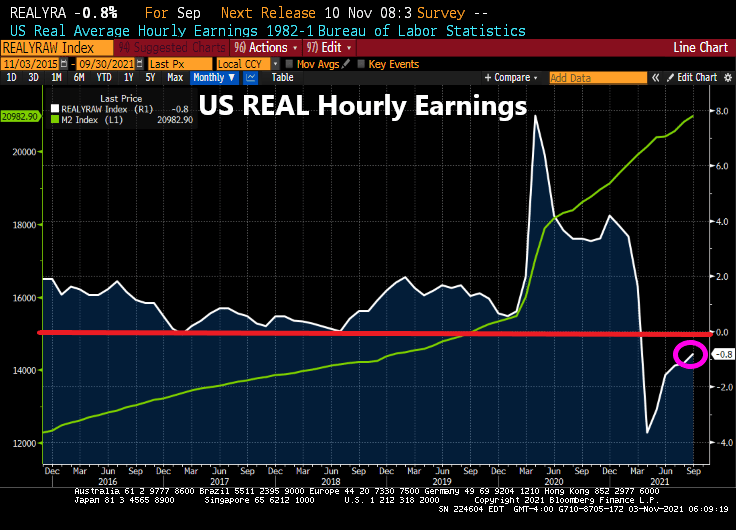

The bad news? REAL average hourly earnings growth “rose” to -0.8141% meaning that inflation is outpacing wage growth (despite what Joe Bidensaid yesterday).

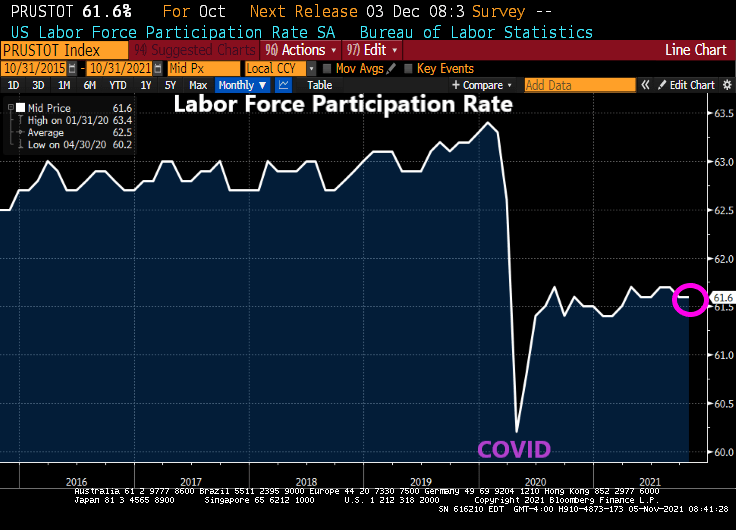

Look at labor force participation both in October and before Covid. After the large decline in LFP, it rose again then leveled-off to near where it is in October 61.6%.

Here is the rest of the story. Zero Hedge had the enticing headline of “October Payrolls Soar To 531K, Smashing Expectations As Prior Months Revised Sharply Higher”. Too bad inflation is eating away at the gains.

Biden: “We have increased labor force participation by inches.”

Employment in leisure and hospitality increased by 164,000 in October and has risen by 2.4 million thus far in 2021. Over the month, employment rose by 119,000 in food services and drinking places and by 23,000 in accommodation. Employment in leisure and hospitality is down by 1.4 million, or 8.2 percent, since February 2020.

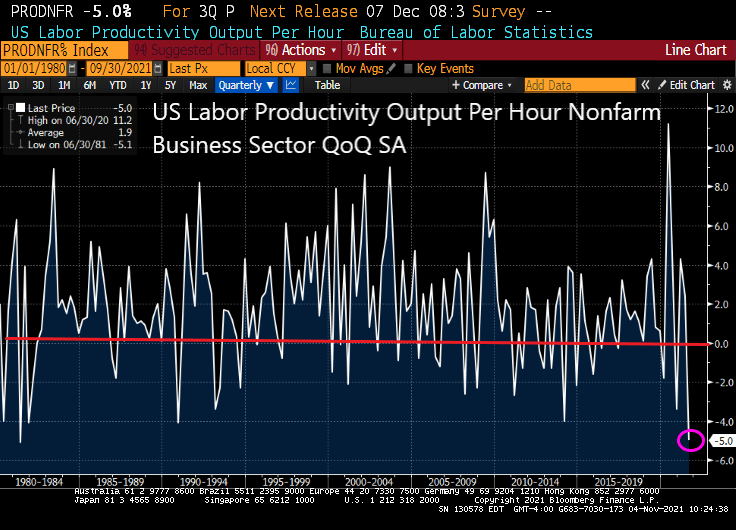

The last time we saw US labor productivity out per hour this low was in 1981 when President Reagan inherited stagflation from President Jimmy Carter.

As unit labor costs soar +8.3%.

Any wonder that the 1% have been doing so well relative to the bottom 50% in terms of wealth since entrance of The Fed in 2008 with zero-interest rate policies (ZIRP) and assets purchases (QE). And also after Covid struck.

“That will be $10,000 for your Big Mac, fries and a soda, please!”

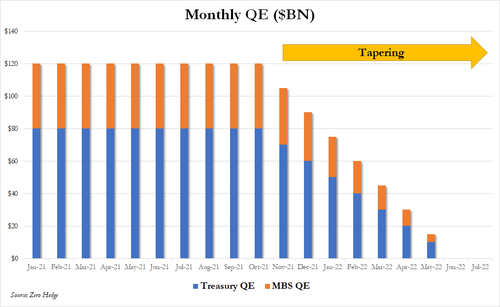

The Federal Reserve Open Market Committee (FOMC) did what was expected today. They left their target rate unchanged at 25 basis points and enacted a slooooowwww tapering of their balance sheet.

Complete the increase in System Open Market Account (SOMA) holdings of Treasury securities by $80 billion and of agency mortgage-backed securities (MBS) by $40 billion, as indicated in the monthly purchase plans released in mid-October.

o Increase the SOMA holdings of Treasury securities by $70 billion and of agency MBS by $35 billion, during the monthly purchase period beginning in mid-November.

o Increase the SOMA holdings of Treasury securities by $60 billion and of agency MBS by $30 billion, during the monthly purchase period beginning in mid-December.

o Conduct overnight repurchase agreement operations with a minimum bid rate of 0.25 percent and with an aggregate operation limit of $500 billion; the aggregate operation limit can be temporarily increased at the discretion of the Chair.

o Conduct overnight reverse repurchase agreement operations at an offering rate of 0.05 percent and with a per-counterparty limit of $160 billion per day; the per-counterparty limit can be temporarilyincreased at the discretion of the Chair.

Yes, a slowdown in the trajectory of Fed asset purchases.

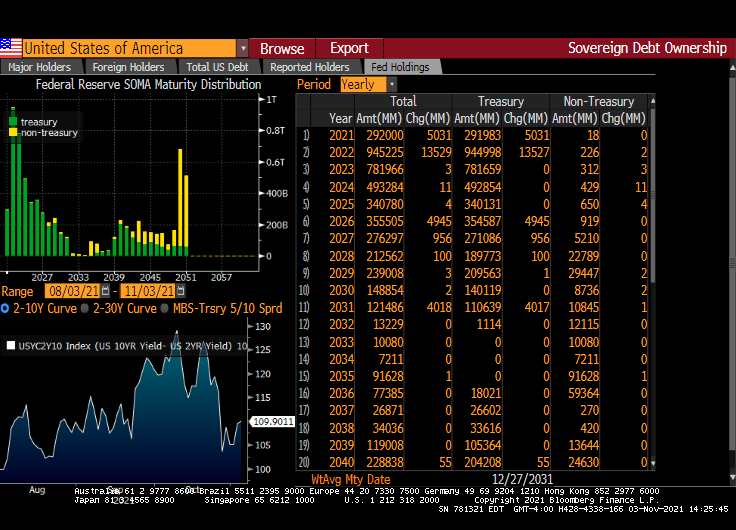

The maturity structure of System Open Market Holdings by The Fed?

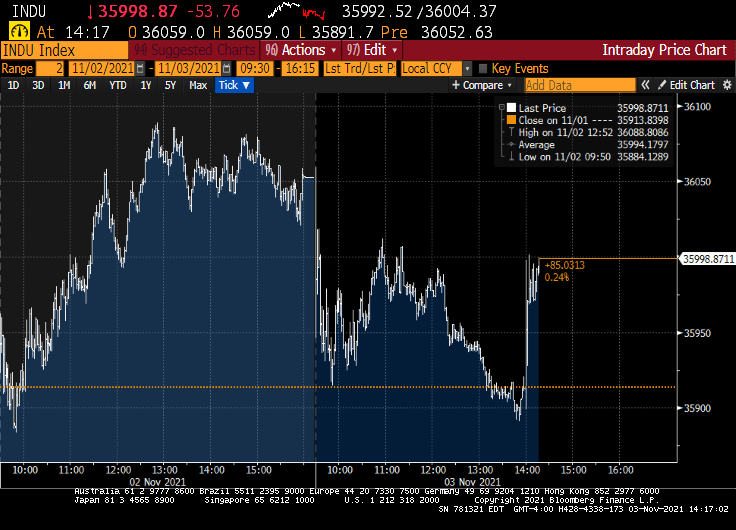

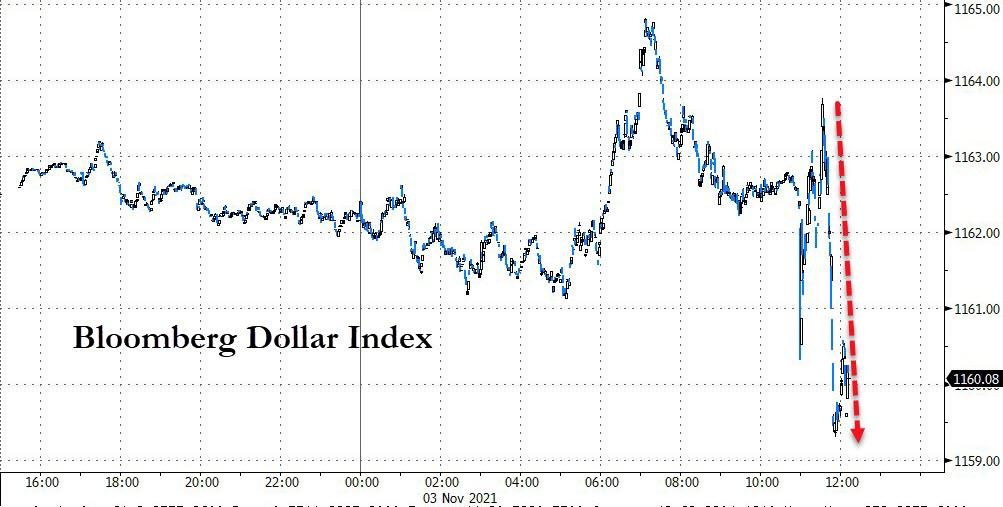

The reaction in the stock market and bond markets? How about the Dow?

Nothing has been the same since Covid struck in early 2020.

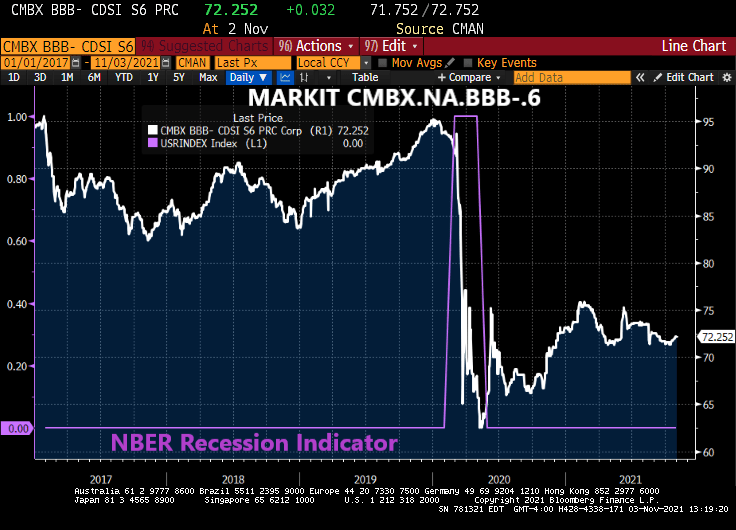

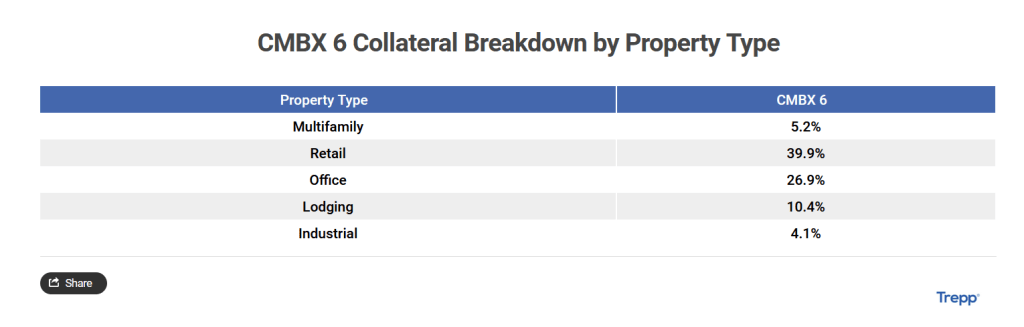

CMBX BBB-, the reference basket for CMBS 6, was climbing to around $95 prior to the Covid outbreak and resulting recession. The CMBX reference basket is now at $72.25.

CMBX 6 is largely composed of retail and office, both hit hard by Covid and the ensuing lockdowns and fearmongering by the Federal government and main street media.

From The Land of 1,000 Excuses, The Federal Reserve Open Market Committee (FOMC) will announce … no rate increases and a slight reduction in their assets purchases (Treasuries and Agency MBS). The announcement will be at 2pm EST (not at The Midnight Hour).

The Federal Open Market Committee is all but certain to hold rates near zero after a two-day policy meeting and announce a $15 billion monthly reduction in bond buying from the current $120 billion pace, judging that the test for tapering has been met as the economy heals from Covid-19.

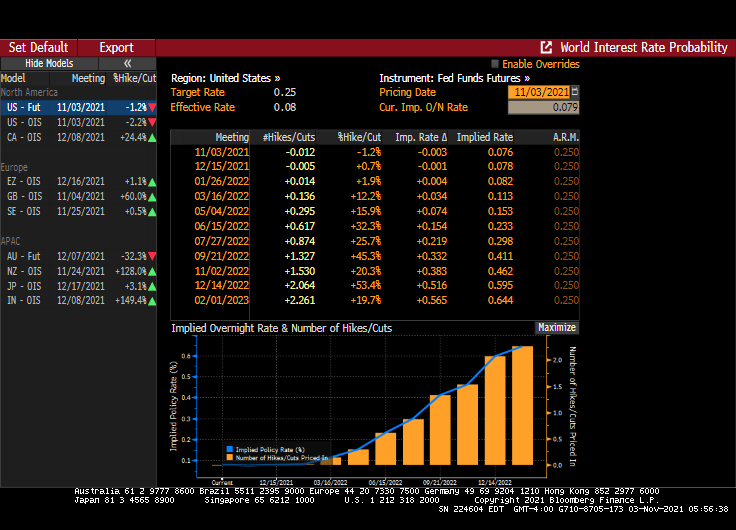

There are two rate increases baked into the Fed Funds futures data as of today.

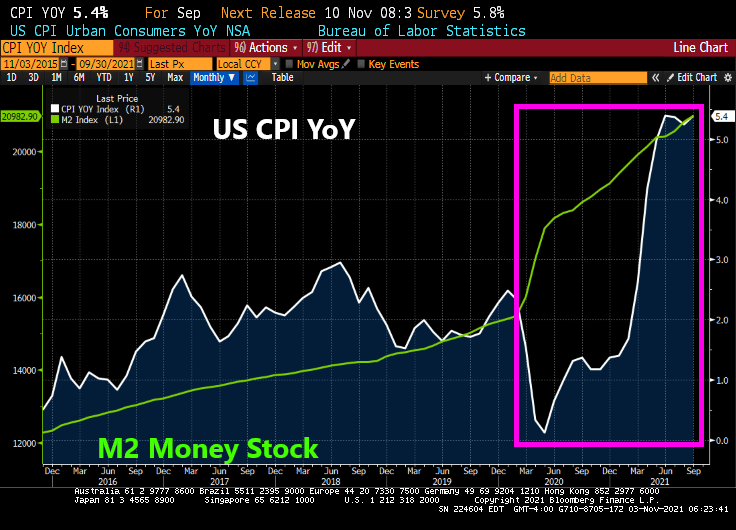

But a troubling aspect of The Fed’s monetary policy is that M2 Money Velocity is near the lowest in history and The Fed has been binge printing. What this means is that money printing has had little impact on GDP growth.

When The Fed mentions the post-COVID recovery, I hope they mention that REAL hourly wage growth is NEGATIVE.

And REAL S&P 500 earnings yield is also negative.

The Fed will likely to blame TRANSITORY effects such as the backed-up port traffic in Long Beach for rising prices rather than their flooding the markets with too much money.

But The Fed will continue to print, even though they will blame bottlenecks for inflation rather than their haphazard drowning of the economy in money.

Given that The Fed is monetizing the reckless spending by The Federal government, particularly Pelosi’s latest budget, we will see coordination between Chairman Powell and Treasury Secretary Janet Yellen (aka, Mustang Sally).

Call Jerome at 634-5789 to tell him to raise rate to normal levels.

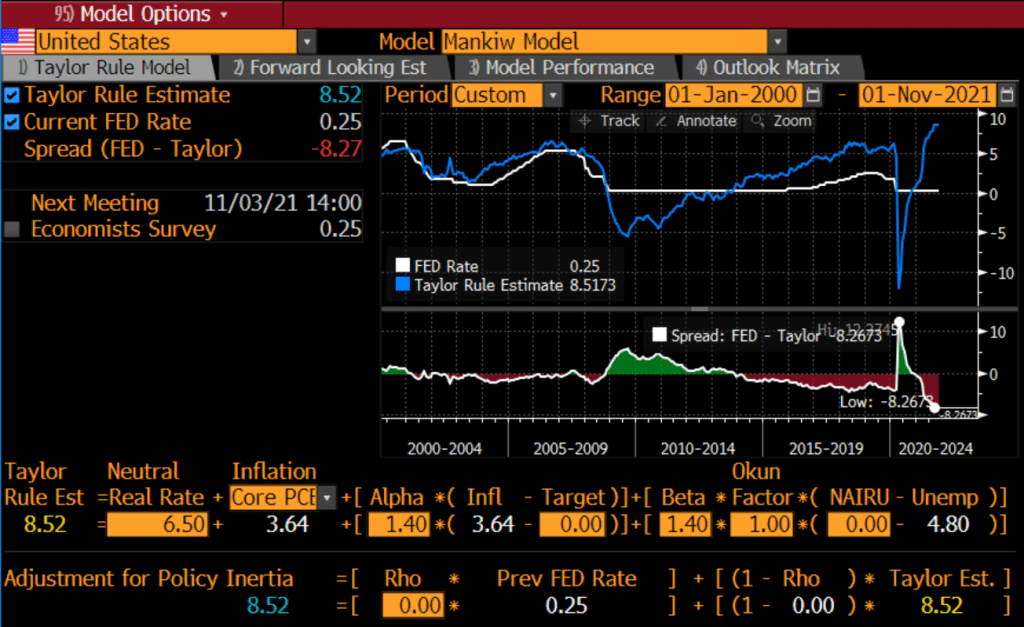

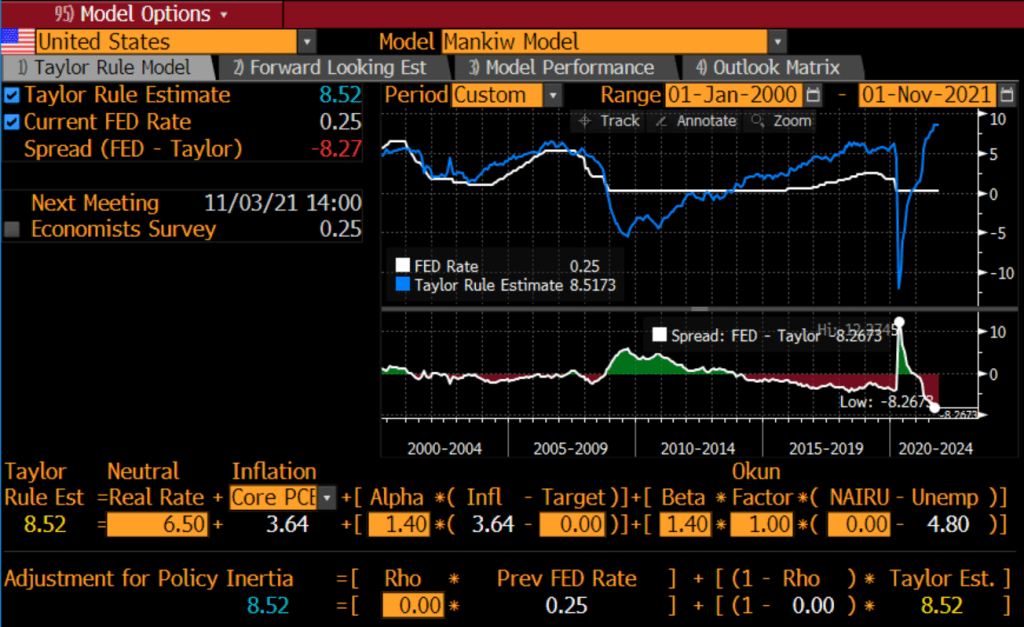

As we approach another Fed Open Market Committee (FOMC) meeting (November 3rd), it is time to look at the Taylor Rule, created by Stanford economist John Taylor to help everyone understand what The Fed is likely to do. Unfortunately, The Fed doesn’t do what expected.

For example, look at the Taylor Rule using Greg Mankiw’s specification. It says The Fed Funds Target Rate should be 8.52%, not the lowly 0.25% it is today.

That is a big gap between where The Taylor Rule says we should be and where Powell and the FOMC is.

Will The Fed raise their target rate on November 3rd? Or at least start slowing the balance sheet?

Somewhere over the Alps, T-Sec Janet Yellen is fearmongering over a possible US debt default if Republicans don’t kowtow to Democrat’s desires to raise the debt ceiling.

(Washington ComPost) — SOMEWHERE OVER THE ALPS — Treasury Secretary Janet Yellen on Sunday said Democrats should be willing to approve a fix to the nation’s debt ceiling without GOP support if necessary, an approach senior Democrats ruled out during arecent standoff over the issue.

In an interview aboard a government airplane between Rome and Dublin, Yellen castigated Republicans for refusing to help raise the debt limit but acknowledged Democrats may be able to address the issue without GOP support through the Senate budget procedure known as reconciliation.

Senior Democratic leaders were adamant that the debt ceiling be resolved on a bipartisan basis last month. Senate Republicans have uniformly insisted that Democrats should alone be responsible for raising the nation’s debt limit. Congress probably will face a deadline of Dec. 3 to act, though the exact date is uncertain.

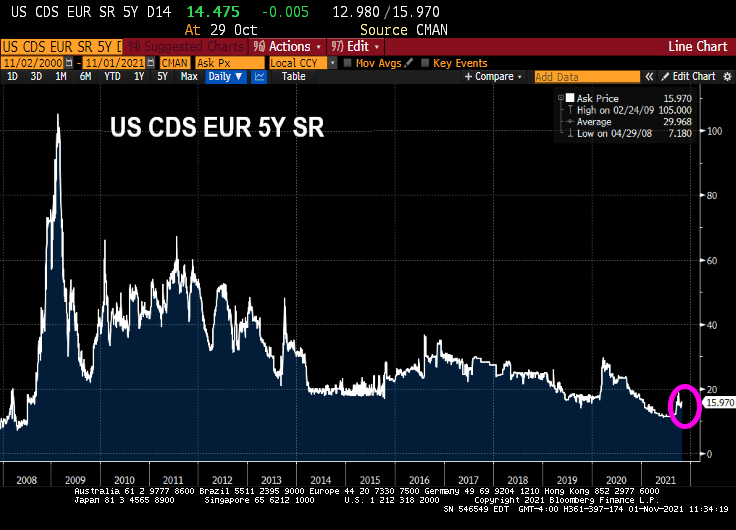

Well, Janet, the market (Credit Default Swaps for US) doesn’t seem to be worried about raising the debt ceiling.

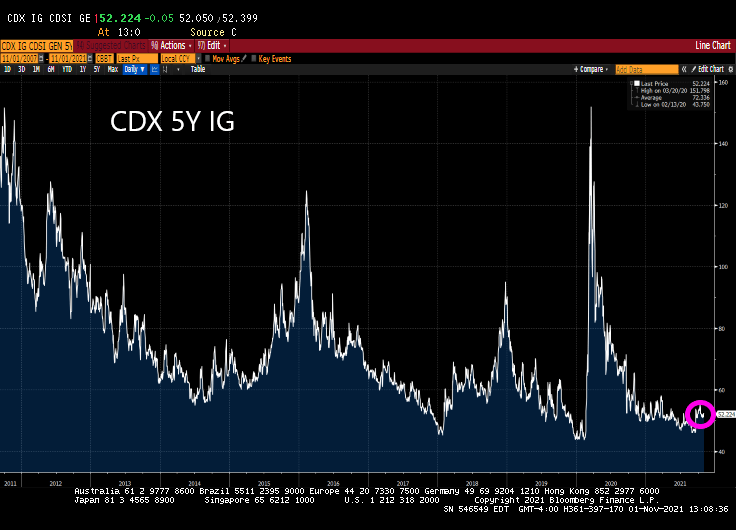

Likewise, the CDX 5Y IG for the US investment grade corporate bonds is near historic lows. Even Yellen can’t make that rise.

Only a career academic and politico Bambina like Janet Yellen would try to drum up agita about a US debt default when Democrats can cram down most anything through “budget reconciliation.”

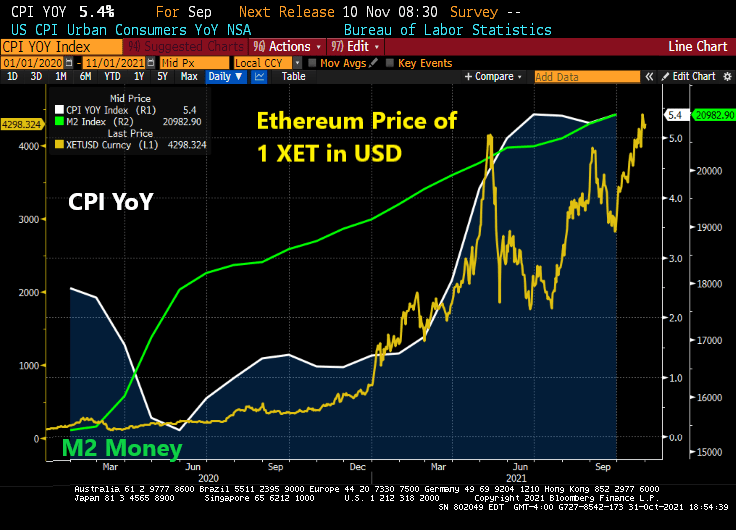

Ethererum, the cryptocurrency, is now at $4,298. It under $200 as the Covid crisis took shape in March 2020. Since Covid, The Federal Reserve went loco and massively increased their money supply and asset purchases. With that response (and economic bottlenecks), inflation has increased to 5.4% YoY.

The Fed’s new moto should be “Policy errors ARE our business!”

No, we don’t look to President Beavis to do much of anything positive about inflation.

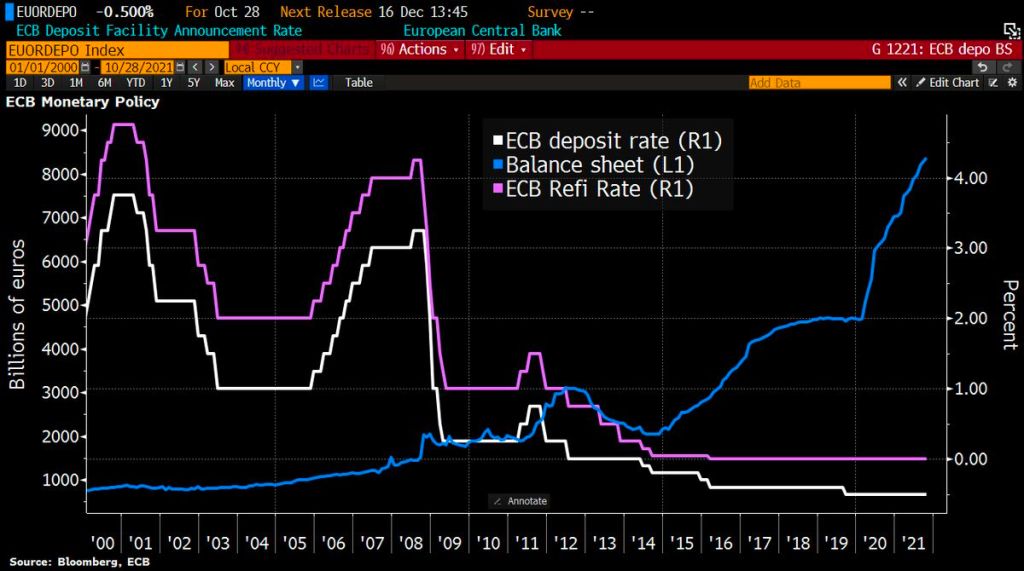

With central banks around the world signalling tighter policy amid rising prices, Lagarde said the ECB had done much “soul-searching” over its stance but concluded that inflation was still temporary, so a policy response would be premature.

Soul-searching? The ECB is just doing what Powell and the Fed (aka, Jerome Jett and the Blackhearts) are doing. Keeping the foot on the monetary gas pedal in the face of inflation.

Let’s start Eurozone inflation. It is now sitting a 4.10% YoY. And core inflation is sitting at 2.10% YoY. Inflation is now the highest since 2009 while core inflation is at the highest since 2001.

Like the Federal Reserve, the ECB still has its foot on the monetary accelerator pedal despite booming inflation.

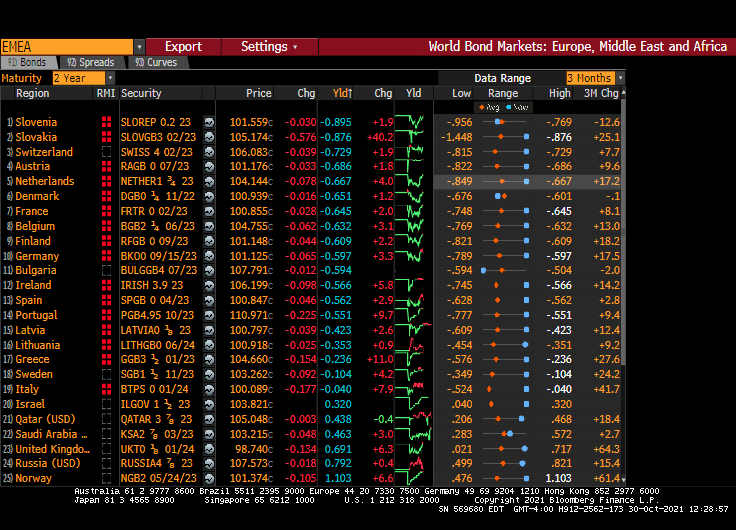

So, Christine, 19 nations in “Europe” having negative 2-year sovereign yields isn’t low enough for you?

The ECB’s platform in Frankfurt reminds me of a bad TV quiz show where participants try to guess prices next year. Call it “The Price Is Wrong.”

Unless, of course, the ECB sees a massive depression ahead.

You must be logged in to post a comment.