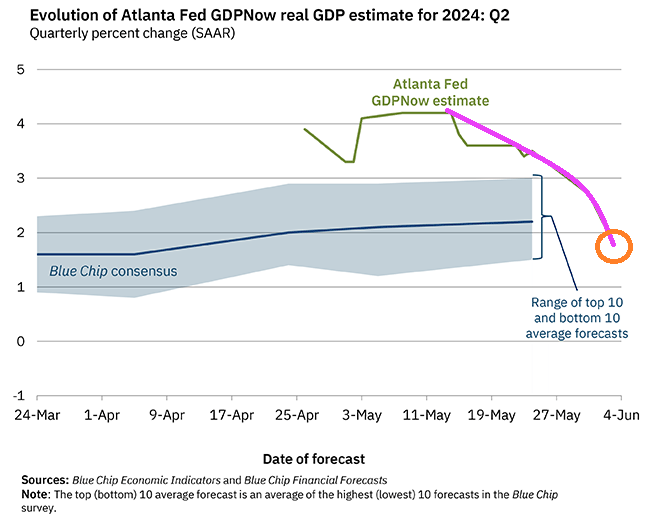

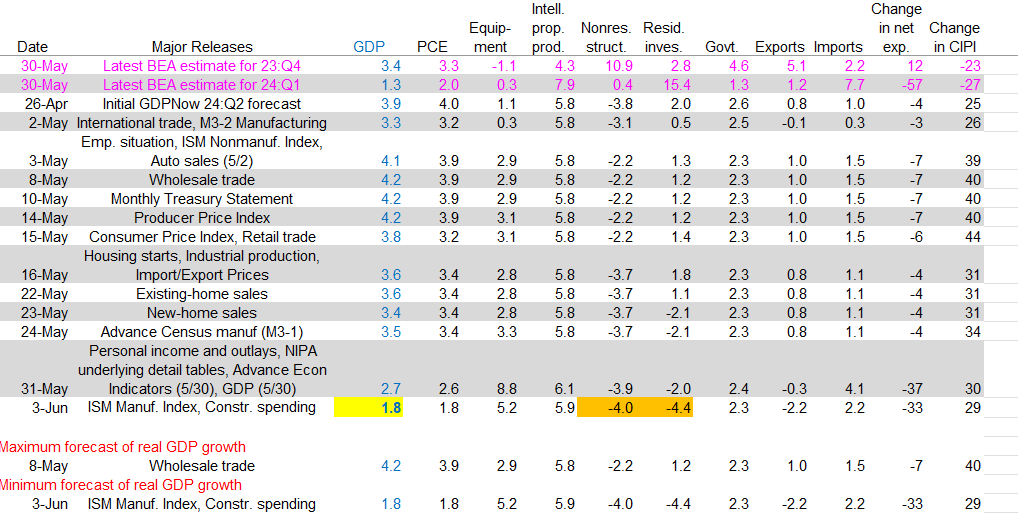

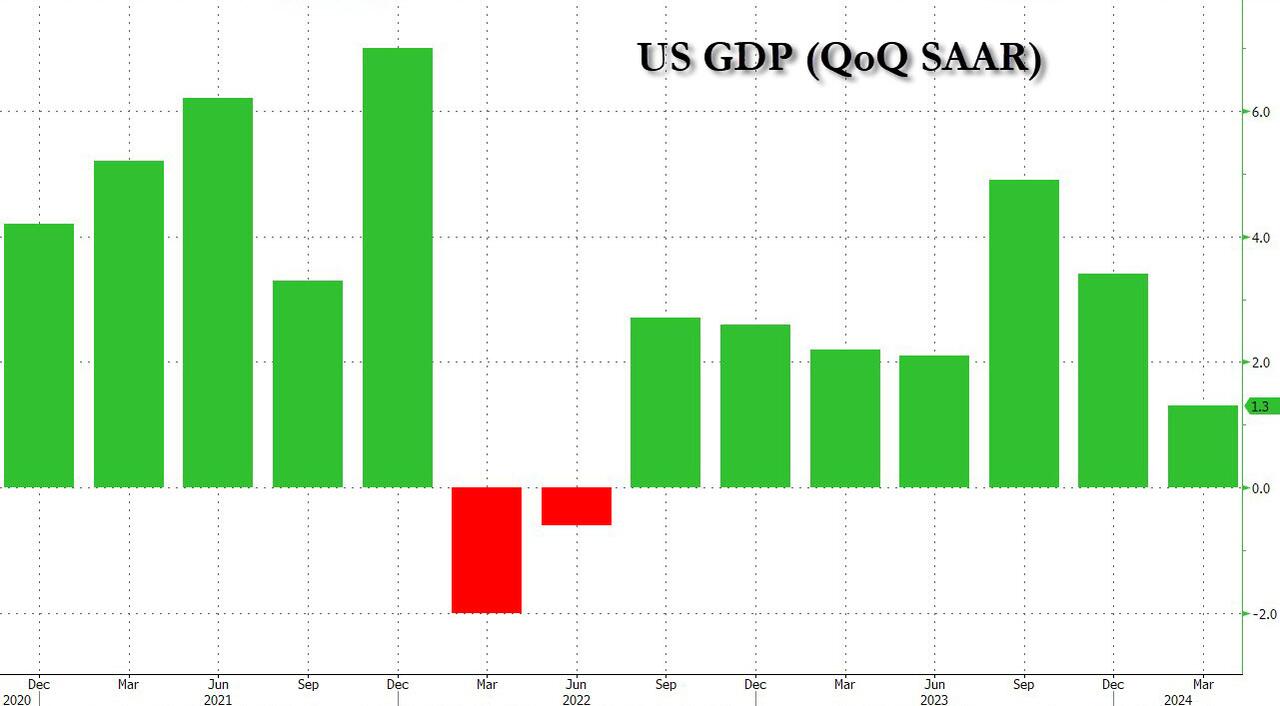

The GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the second quarter of 2024 is 1.8 percent on June 3, down from 2.7 percent on May 31. After recent releases from the US Census Bureau and the Institute for Supply Management, the nowcasts for annualized second-quarter real personal consumption expenditures growth and real private fixed investment growth declined from 2.6 percent and 3.1 percent, respectively, to 1.8 percent and 1.5 percent.

fff

Since I used The Animal’s version of the John Lee Hooker great tune “Boom Boom,” I will use another Animals tune for Joe Biden’s penchant for sniffing little girls. “Baby Let Me Take You Home.”

The Animals band. Not to be confused with the animals in the Biden Administration and Congress.

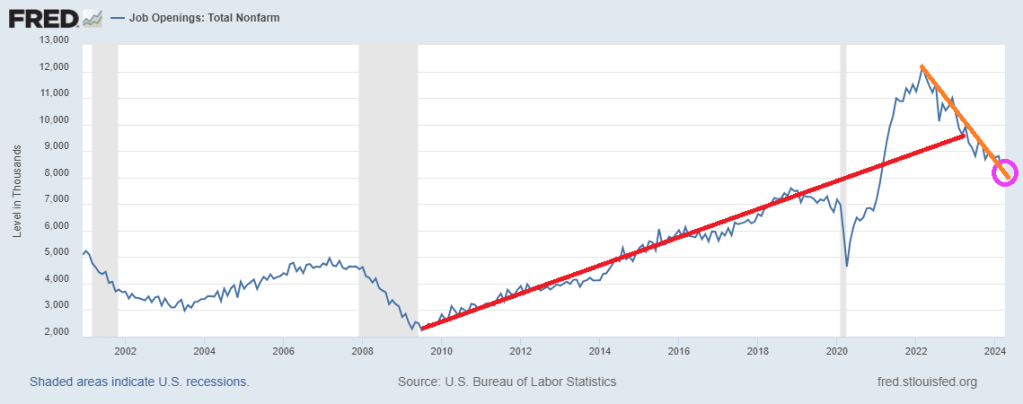

Job openings in April 2024 dipped to 8,059. Notice the trend (orange line) is below the trend set prior to Covid (red line).

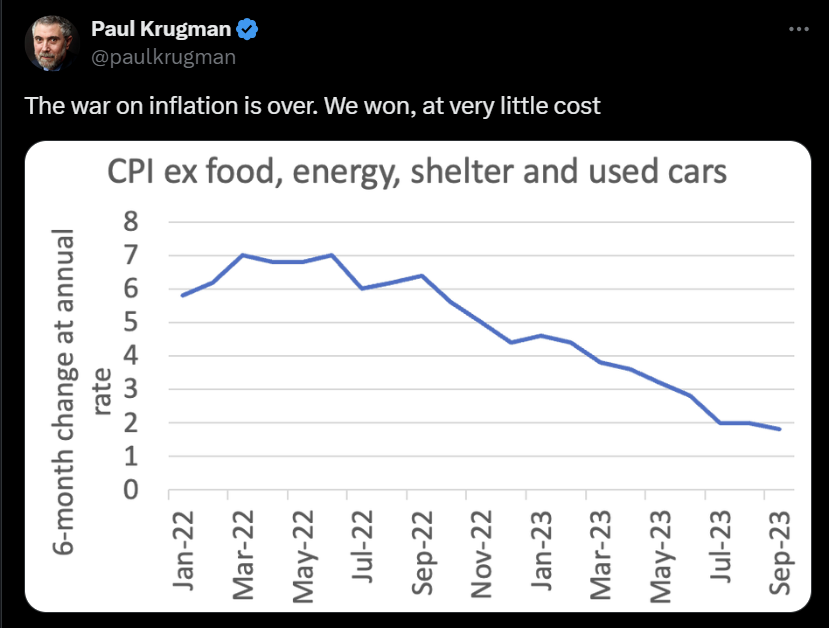

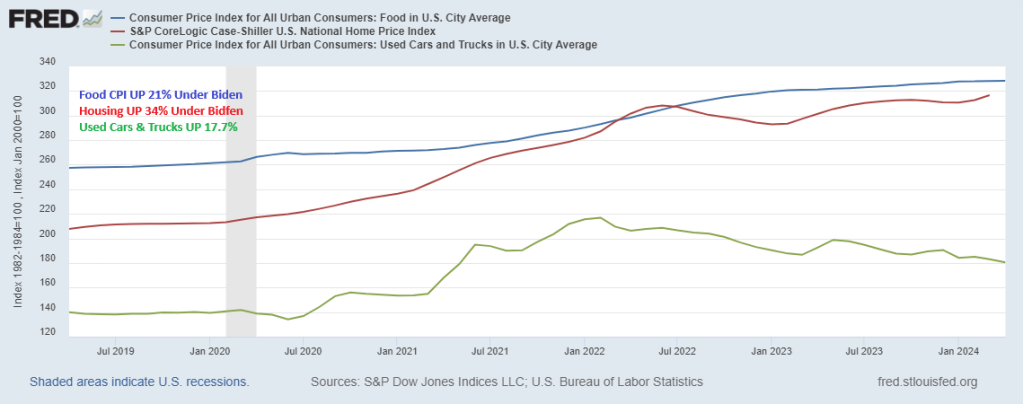

Back in 2023, Socialist Paul Krugman declared that “the war on inflation is over!!! “We” won, at very little cost.” I love when elitists claim “We won!” since clearly 99% of Americans lost since food, housing and car prices up are double digits under Biden.

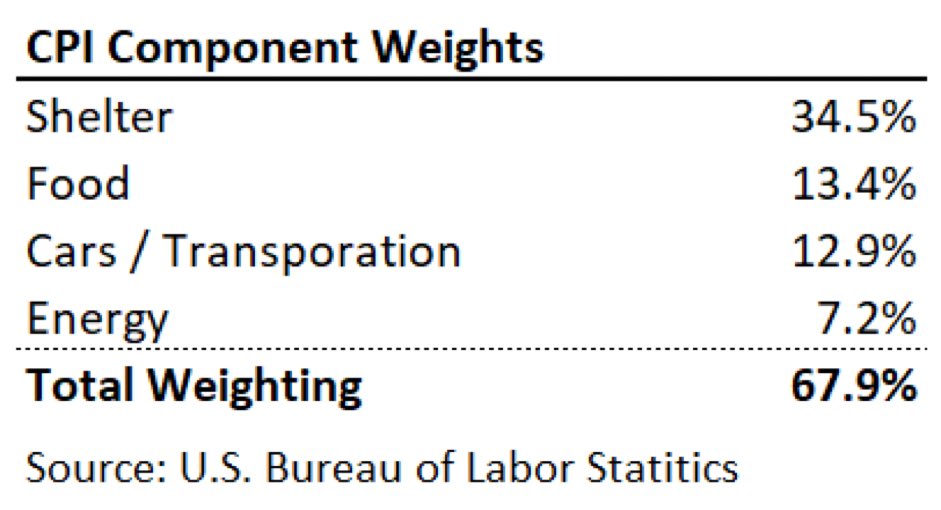

The problem is that food, energy, shelter, and used cars/trucks are a huge part of Americans consumption basket.

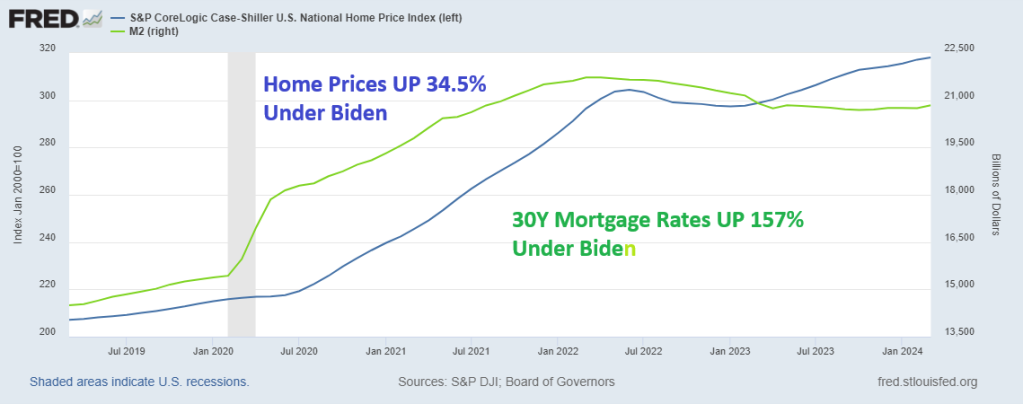

Under Biden, food CPI is up 23%. Home prices are up 34% and used cars/truck prices are up 17.7%.

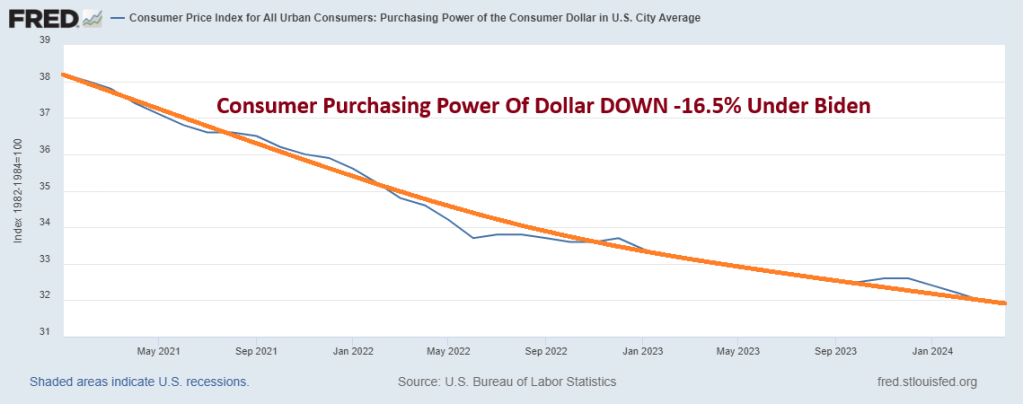

A note to Paul Krugman, YOU may have won, but the rest of Americans lost. Consumer purchasing power of the US Dollar is DOWN 16.5% Under Biden.

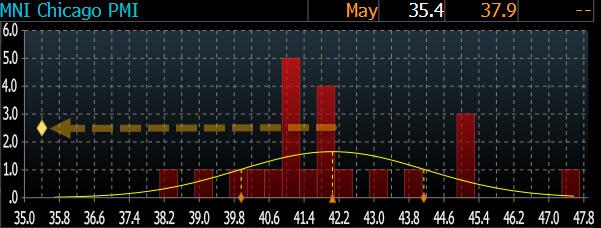

… which seems to suggest that at least according to Chicago-based purchasing managers, the economy is in a depression.

This is how the final number looked relative to expectations.

Looking at the report we find the following:

Business barometer fell at a faster pace; signaling contraction

New orders fell at a faster pace; signaling contraction

Employment fell at a faster pace; signaling contraction

Inventories fell at a faster pace; signaling contraction

Supplier deliveries fell at a slower pace; signaling contraction

Production fell at a slower pace; signaling contraction

Order backlogs fell at a faster pace; signaling contraction

Did nothing rise? One thing did:

Prices paid rose at a slower pace; signaling expansion

So we have not just a depression, but a stagflationary depression in which everything else is going to hell, except prices: they keep on rising.

And while it is unclear what has prompted this unprecedented bearishness (the surely negative contribution from Boeing is likely to blame for a substantial portion of the apocalyptic outlook), one thing is certain: Goldman will have to come up with even more goalseeked surveys that explain away reality and tell us how purchasing managers really should feel…

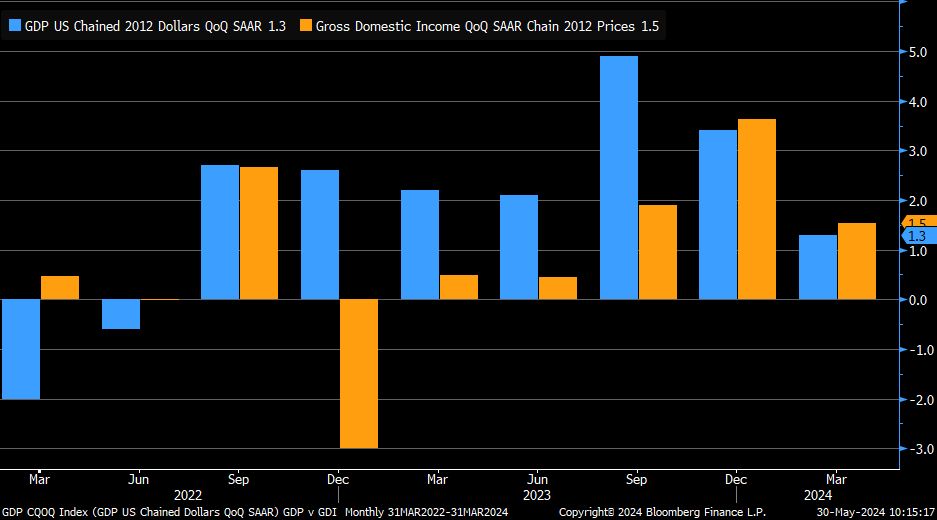

On the good news front, REAL Gross Domester Income rose to 1.5%.

As copper prices keep on rising. Which is bad news for Biden’s shift to EVs! (Once again, Biden is driven around in gas guzzling Chevy Tahoes/Suburbans and owns a Chevy Corvette). There isn’t enough copper production to build the EVs that Biden wants.

I have testified and sat through many trials in New York city and have never seen a court case quite like the one the Trump lost with the Judge effectively telling the jury to find Trump guilty.

After an unexpected jump in March, pending home sales were expected to drop 1.0% MoM in April as mortgage rates pushed back above 7.00% and stayed there.

Well, the analysts had the direction right but magnitude was way off as pending home sales plunged 7.7% MoM – the biggest drop since Feb 2021 (and below the lowest estimate), leaving sales down 0.7% YoY…

Source: Bloomberg

This is the 29th straight month of YoY declines for non-seasonally-adjusted pending home sales.

This MoM decline pushed the Pending Home Sales Index back to record lows…

Source: Bloomberg

The Midwest saw the biggest drop in pending sales, down 9.5% in April, followed by declines of 8.5% and 7.6% in the West and South, respectively. Contract signings in the Northeast fell 3.5%.

“The impact of escalating interest rates throughout April dampened home buying, even with more inventory in the market,” NAR Chief Economist Lawrence Yun said in a statement.

“But the Federal Reserve’s anticipated rate cut later this year should lead to better conditions, with improved affordability and more supply.”

All driven by affordability crisis as mortgage rates surged back above 7.00%…

Source: Bloomberg

“The prospect of measurable home price declines appears minimal,” Yun said.

“The few markets experiencing price declines will be viewed as second-chance opportunities for buyers to enter the market if those regions continue to add jobs.”

As a reminder, the pending-sales report tends to be a leading indicator of sales of previously owned homes, because houses typically go under contract a month or two before they’re sold.

What I like about Biden’s economy … nothing. Most of Biden’s economic growth came from Trump’s spending and Fed monetary policy from the Covid shutdown of 2020.

The sharp downward revision primarily reflected a downward revision to consumer spending, which rose 2.0% annualized, down from 2.5% in the first GDP report and below the 2.2% estimate.

Drilling down into the number, the 1.3% increase reflected increases in consumer spending (below previous forecasts) and housing investment that were partly offset by a decrease in inventory investment. Imports, which are a subtraction in the calculation of GDP, increased.

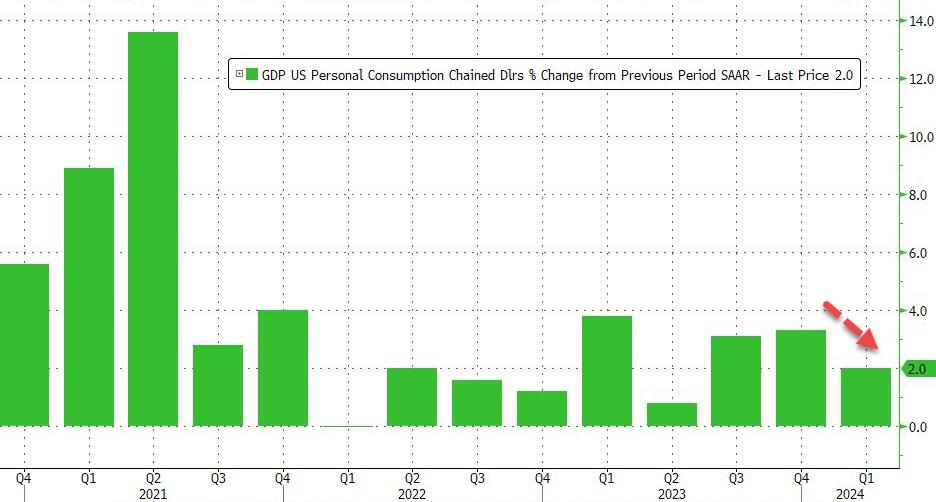

The increase in consumer spending reflected an increase in services that was partly offset by a decrease in goods. Within services, the leading contributors to the increase were health care as well as financial services and insurance. Within goods, the leading contributors to the decrease were motor vehicles and parts as well as gasoline and other energy goods.

The increase in housing investment was led by brokers’ commissions and other ownership transfer costs as well as new single-family housing construction.

The decrease in inventory investment was led by decreases in wholesale trade and manufacturing

In terms of bottom-line contributions, we find the following:

Personal consumption accounted for 1.34% (down from 1.68%), or more than the entire GDP print.

Fixed Investment added 1.02%, up from 0.91% in the first estimate.

The change in private inventories subtracted -0.45%, a deterioration from the -0.35% estimated previously.

Net trade (exports less imports), subtracted -0.89% from the bottom line print, comparable to the -0.86% detraction in the first estimate.

Finally, government added just 0.23%, up from 0.21% initially estimated, yet still the lowest contribution since Q2 2022.

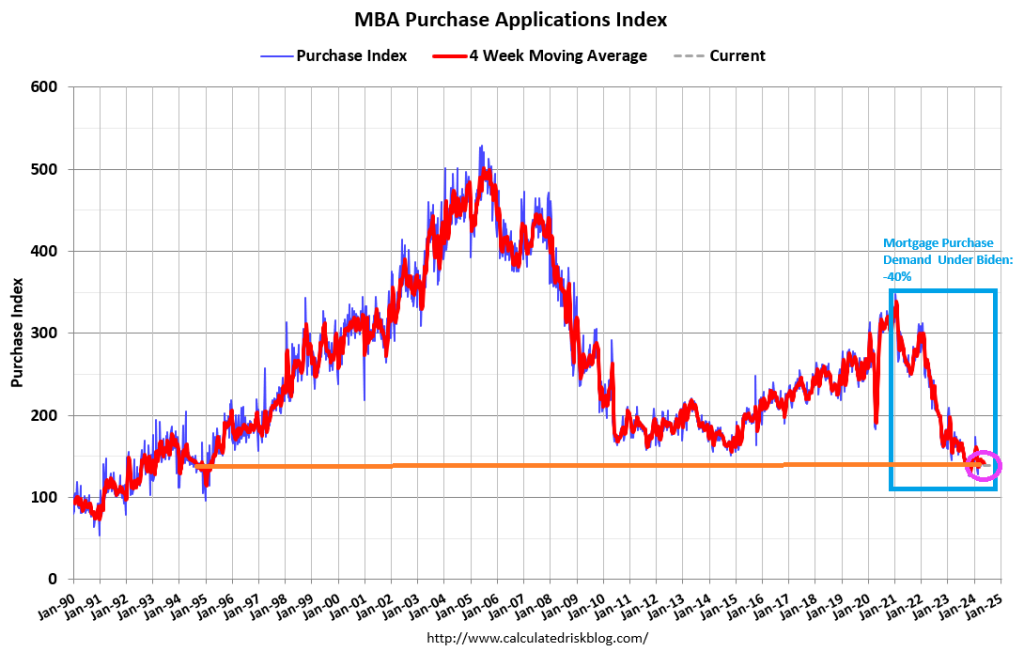

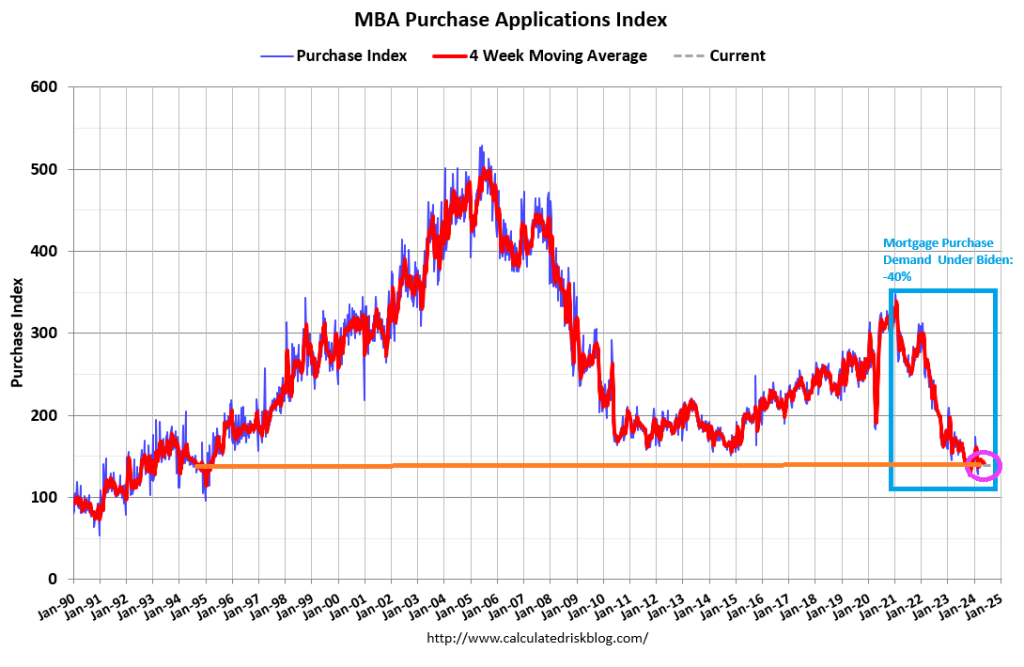

The Market Composite Index, a measure of mortgage loan application volume, decreased 5.7 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 6.3 percent compared with the previous week. The seasonally adjusted Purchase Index decreased 1 percent from one week earlier. The unadjusted Purchase Index decreased 3 percent compared with the previous week and was 10 percent lower than the same week one year ago. And -40% under Biden.

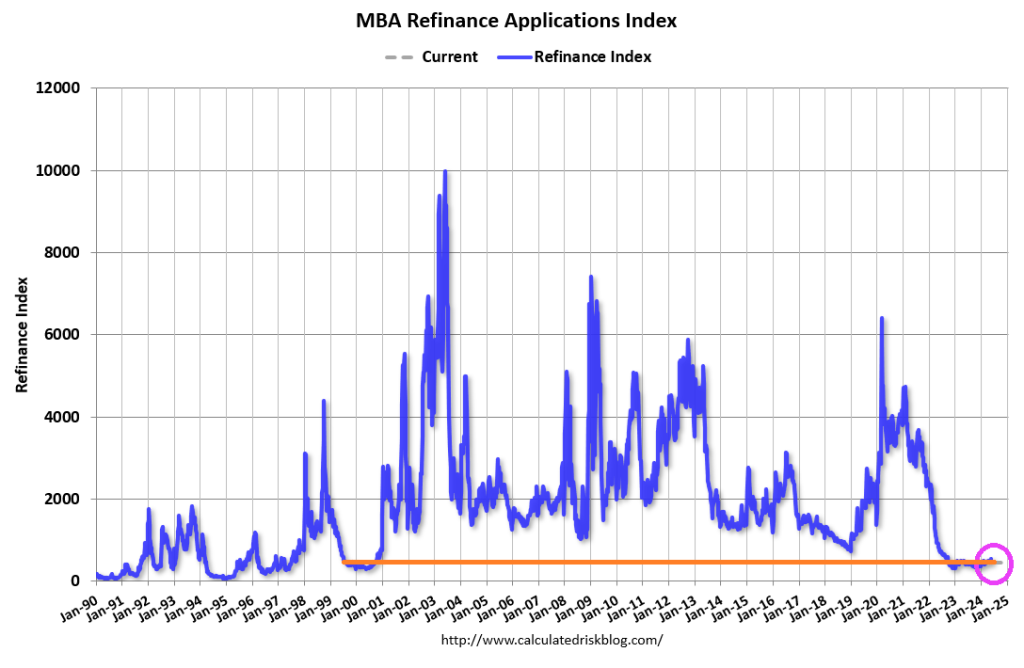

The Refinance Index decreased 14 percent from the previous week and was 12 percent higher than the same week one year ago.

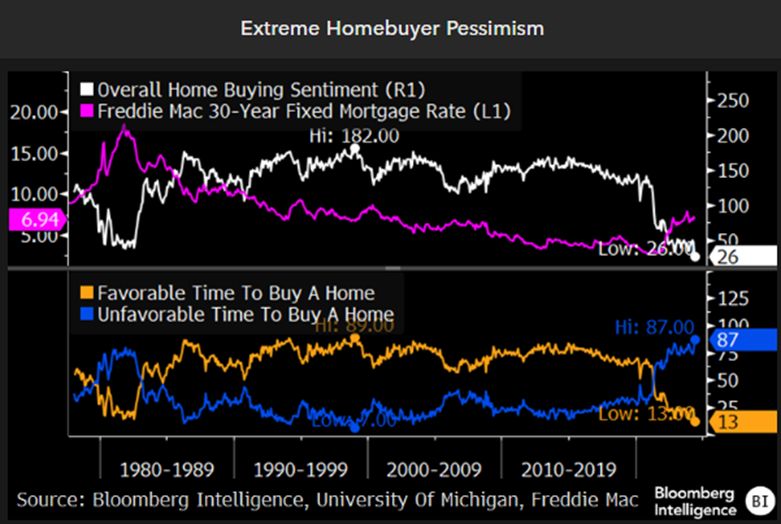

It is still an unfavorable time to buy a home!

From the film “Ronin” that sums up actor Robert DeNiro in one sentence.

Spence (Sean Bean): “You know, you think too hard.” Sam (Robert DeNiro): “Nobody ever told me that before.”

How would DeNiro consider the 40% drop in mortgage purchase demand under Biden?

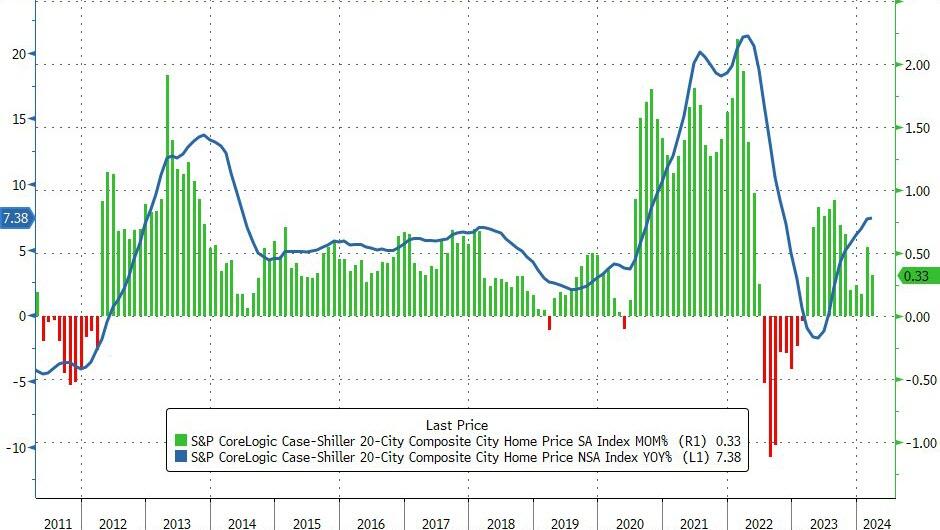

This pushed the price up 7.38% YoY – the fastest rise since October 2022…

“We’ve witnessed records repeatedly break in both stock and housing markets over the past year. Our National Index has reached new highs in six of the last 12 months.” says Brian D. Luke, Head of Commodities, Real & Digital Assets at S&P Dow Jones Indices.

Overall, US home prices reached a new record high in March (as median new home prices began to fall)…

Source: Bloomberg

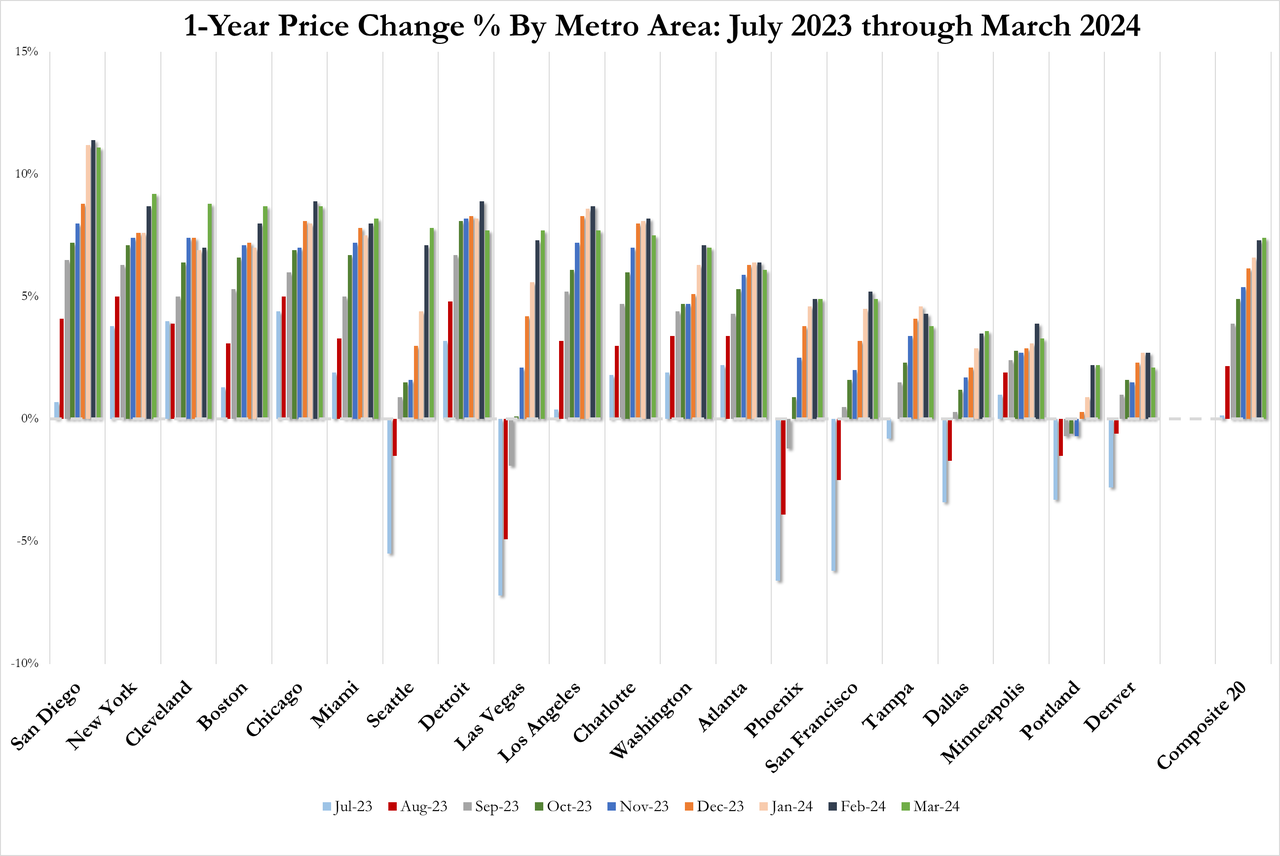

San Diego continued to report the highest year-over-year gain among the 20 cities this month with an 11.1% increase in March, followed by New York and Cleveland, with increases of 9.2% and 8.8%, respectively.

Portland, which still holds the lowest rank after reporting three consecutive months of the smallest year-over-year growth, posted the same 2.2% annual increase in March as the previous month.

Luke suggested this implies “a strong demand for urban markets.”

No city has seen a MoM decline in price in 2024.

Home prices continue to track Fed Reserves closely, but a turning point may come soon…

Source: Bloomberg

Given the smoothing and heavy lag in the Case-Shiller data, it’s hard to find a causal relationship between prices and mortgage rates…

Source: Bloomberg

…but with rates remaining above 7%, it seems hard to believe prices can continue their advance.

Who the heck is HUD Secretary? It was Cleveland’s Marcia Fudge (a typical Biden political appointment). Now it is Adrianne Todman, from the US Virgin Islands and former executive director of the District of Columbia Housing Authority. Not exactly a high-powered resume for a cabinet post, Joe!

I saw former President Obama criticizing former President Trump for not passing “transformative” changes. That is, Trump didn’t sign any Obama-like transformative changes (like Obamacare). Truimp did try to slow down the damage done by Obama and his transformative agenda (e.g., open borders, wealth redistritution, green energy) that Biden has attempted to continue.

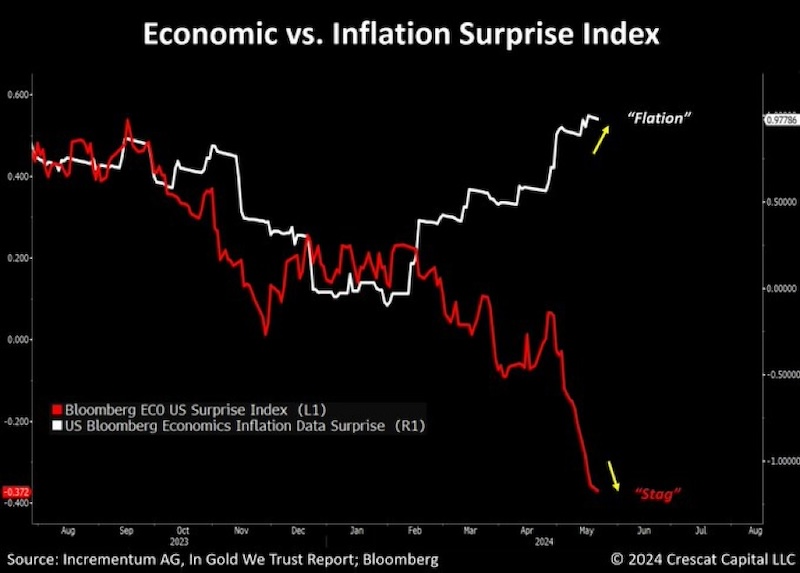

As we approach the party conventions and Presidential election of 2024, we saw the Economic Surprise Index (ESI) in May decline to -0.126.

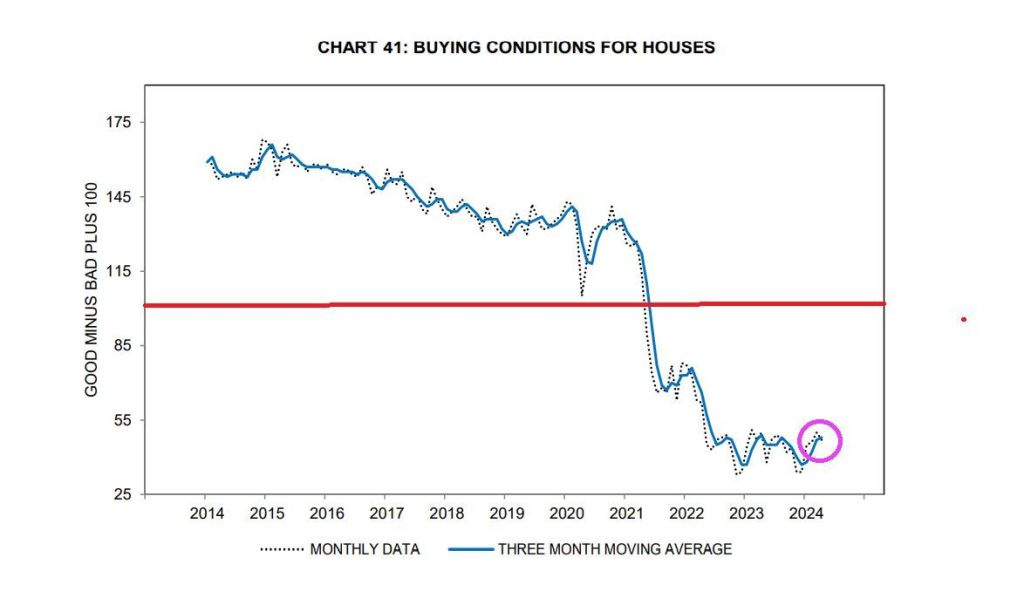

Coupled with Biden’s negative buying conditions for housing (higher mortgage rates and soaring house prices), Obama’s Jacobian transformative economic fantasty is on thin ice.

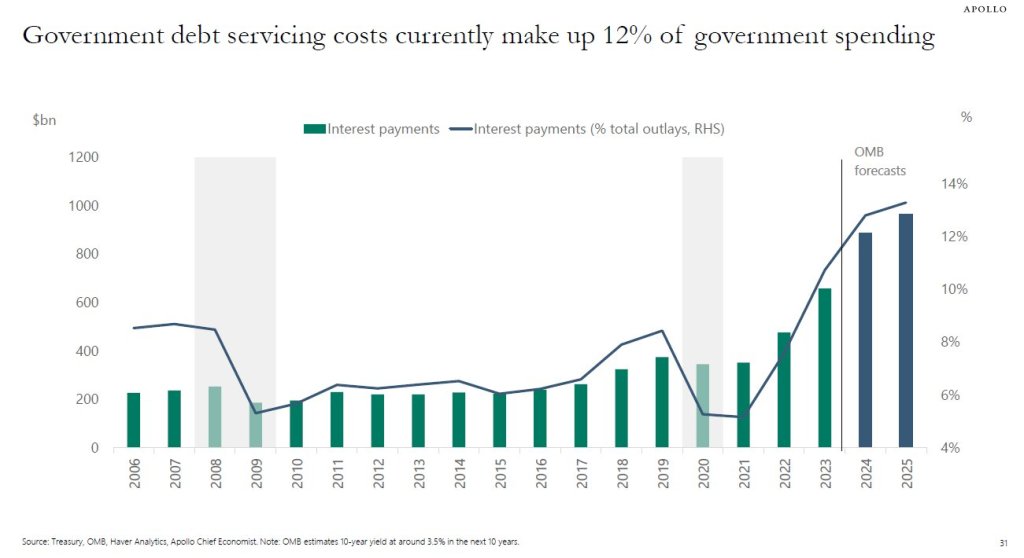

Speaking of higher interest rates, US debt servicing costs currently make up 12% of government spending. Jacobin revolution = Cloward-Piven.

Let’s hope the Obama/Biden Jacobin revolution doesn’t get to this point!

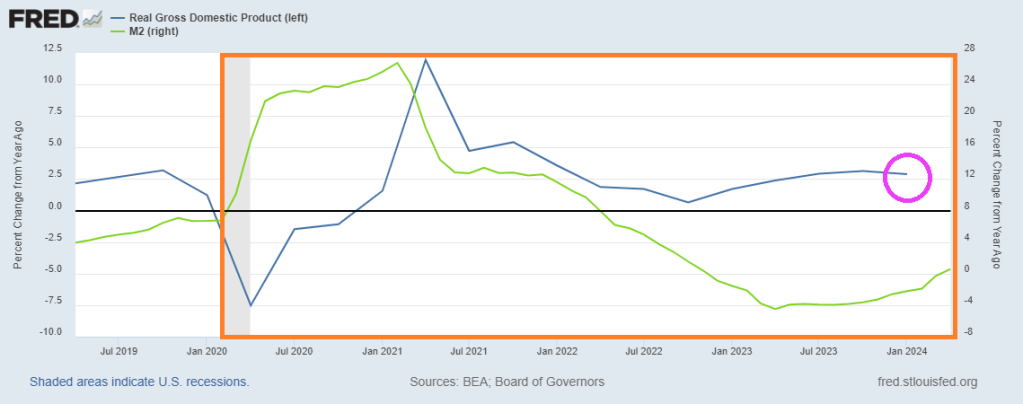

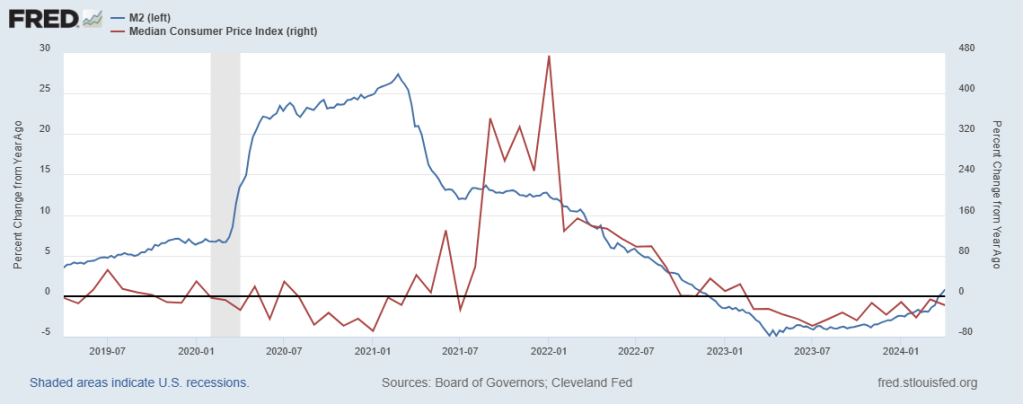

The various talking heads from The Federal Reserve keep jawboning about whether to raise rates or not. One of the major drivers of inflation is … money. M2 Money growth YoY is growing again (blue line)! And with it, inflation has been rekindled.

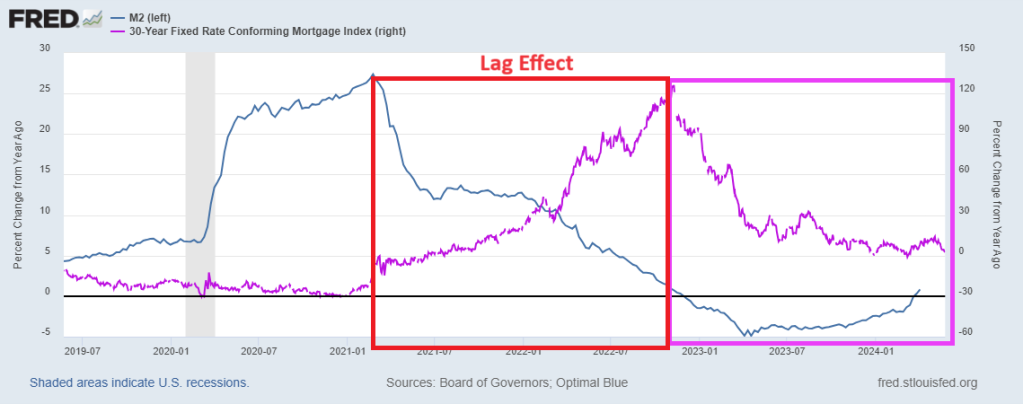

Mortgage rates? There is a lag between M2 Money printing and conforming mortgage rate growth.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.