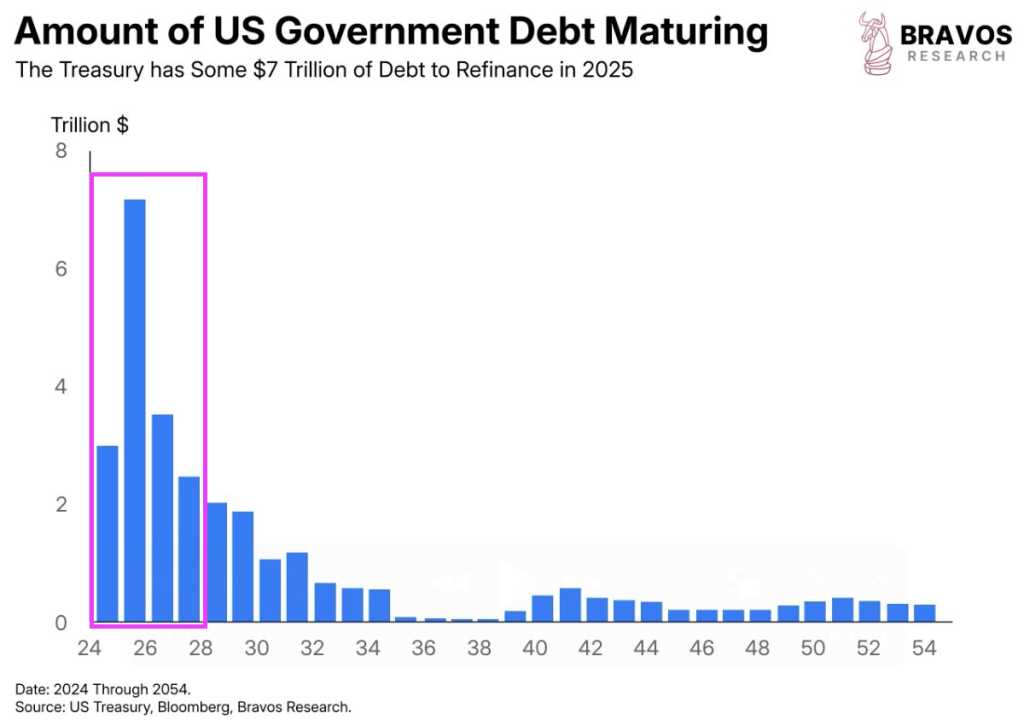

Doge is necessary to get close to closing the budget gap (tax receipts – spending). Biden left Trump and the US with an untenable fiscal situation (think Cloward/Piven). Extremely large debt load with debt maturing over the next couple of years. Thanks to former Treasury Secretary Janet “The Snake” Yellen government funding formula using ST government debt. And its time to pay the piper to pay for Biden’s overspending and Yellen’s Treasury mismanagement.

Most of the Treasury debt that Treasury Secretary Bessent must refinance is short-term.

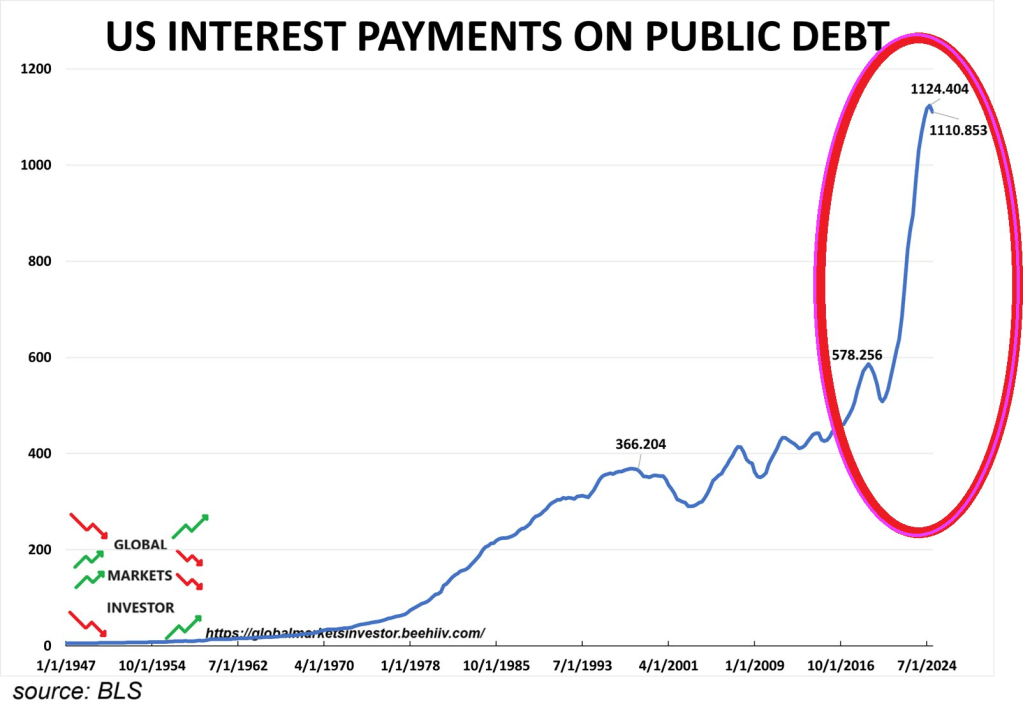

And with interest rates higher under Trump/Bessent than Biden/Yellen, US Interest Payments on Public Debt is expected to keep rising.

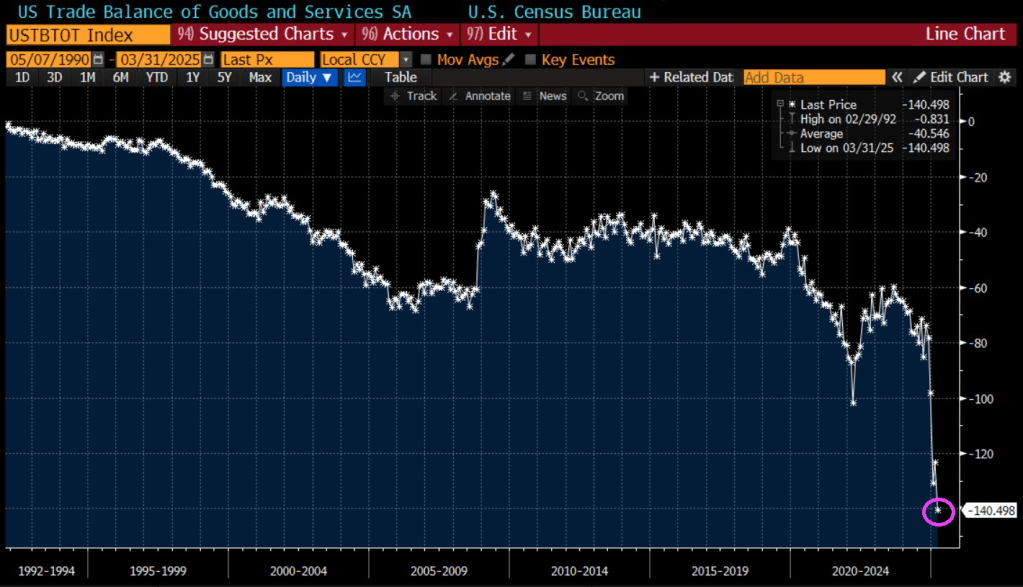

And US trade balance fell to -140.5.

So, were Biden’s economic policies (and Yellen’s Treasury mismanagement) an intentional Cloward-Piven strategy?

Here are Columbia sociologists Cloward and Piven attending a bill signing by President Bill Clinton.

Republicans are trying to lock in Trump’s tax cuts and Democrats are resisting. We now know that DOGE is trying to end the wasteful spending in DC. But I would really like to see tax rates on the middle class fall.

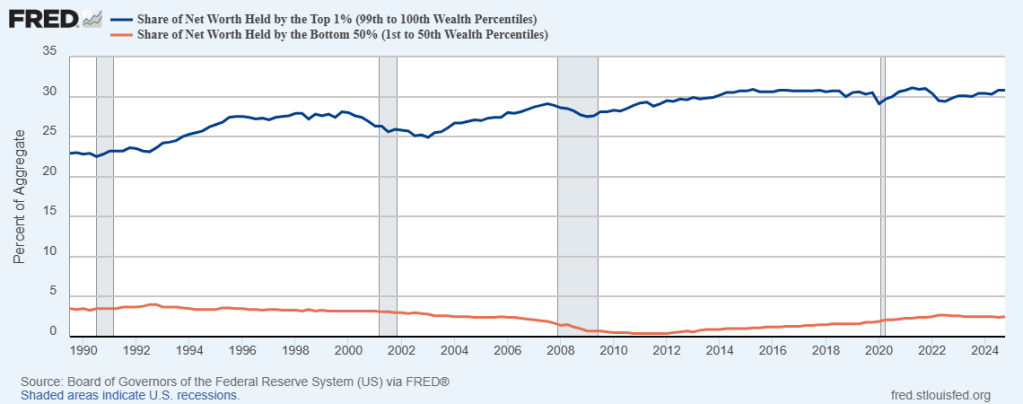

The wealth gap between the top 1% of taxpayers and the bottom 50% of taxpayers is enormous. And has gotten worse since 1990.

Meanwhile. to fight off the temporary effects of the tariff war, Trump is urging Fed Chair Powell to cut rates.

Powell will likely NOT cut rates. But what does “Lunatic Liz” Warren say about rate cuts??

DOGE is working: in Q1, US debt funding needs were $2BN less than the Treasury forecast in February, and in Q2 the Treasury is expected to need $53 billion less than it forecast 3 months ago.

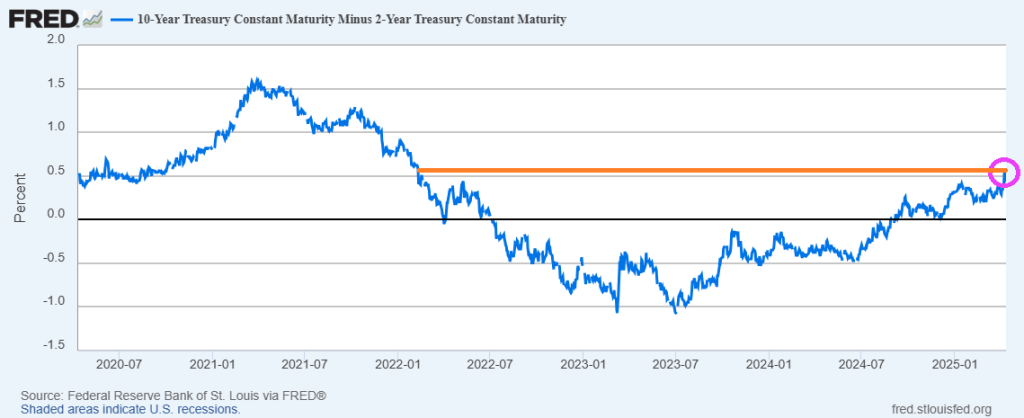

The good news? The US Treasury 10Y-2Y yield curve is normalizing to January 2022 levels.

One the mortgage side, adjustable rate mortgage (ARM) share is the highest since the financial crisis (2008).

As Trump continues to stand up for Americans and China (and Democrats) continues to fight, the S&P 500 index lags MSCI World index by most since 1993 (The Clintons).

Despite the slump in ‘soft’ survey data, analysts expected Empire Fed Manufacturing to bounce back from March’s tumble to one year lows and they were right with the headline index rising from -20.0 to -8.1 (considerably better than the -13.5), but still negative. However, while current conditions jumped, expectations plunged to the lowest since 9/11/.

Obama/Biden/Harris/Schumer/Pelosi have let the US be the punks for China. Trump is simply trying to level the playing field and China’s Xie doesn’t like the new equilibrium.

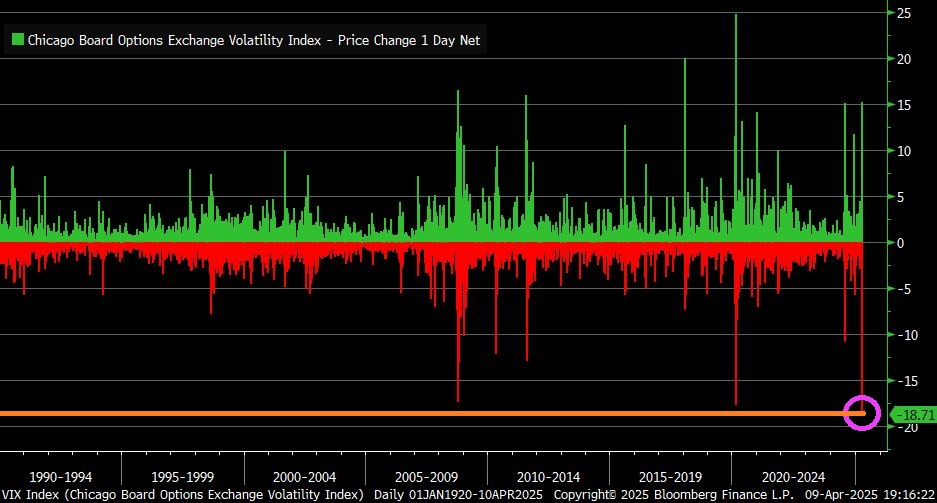

VIX Index fell by 18.7 points yesterday … largest one-day decline in history.

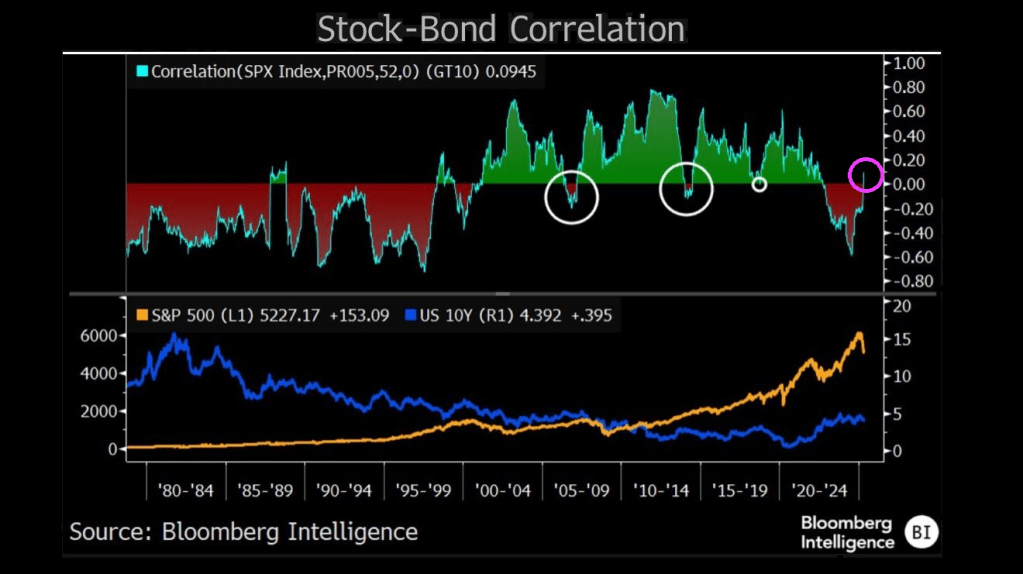

The correlation between stock prices and bond yields has returned to positive territory — hinting at a period of distress in equities and a regime shift in equity and bond markets where recession fears, rather than inflation, may be starting to drive direction of both. The correlation between the two asset classes was positive for the better part of 20 years prior to the pandemic, suggesting equities trended in the direction of yields as inflation mostly coincided with growth. Stocks held a negative correlation to yields throughout most of the 1980s and 1990s, when inflation hurt stocks — and that phenomenon returned for the 2022-24 bear market and recovery period.

Notably, major stock corrections occurred each time the correlation jumped out of its primary regime.

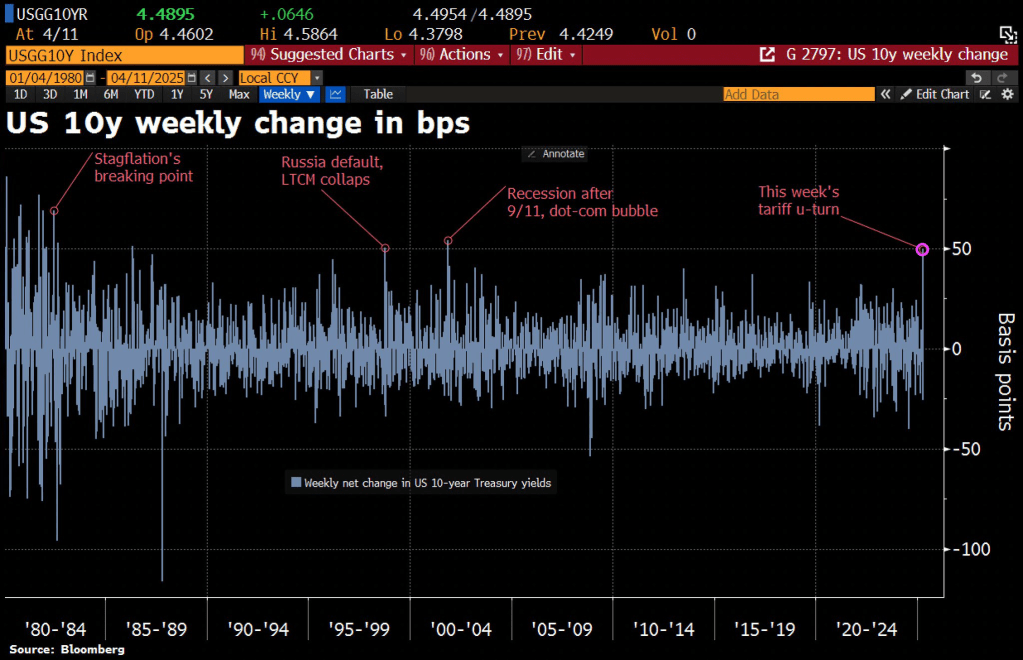

Thunderstruck! The tariff kerfuffle between the Trump Administration and China is causing turbulence in the Treasury market. The 10-year Treasury rate is soaring with China’s counterpunching.

MBS spreads are widening.

Along with volatility.

But corporate spreads are widening more than MBS spreads.

The 10Y-2Y yield curve has risen to the highest level since the early days of “China Joe” Biden.

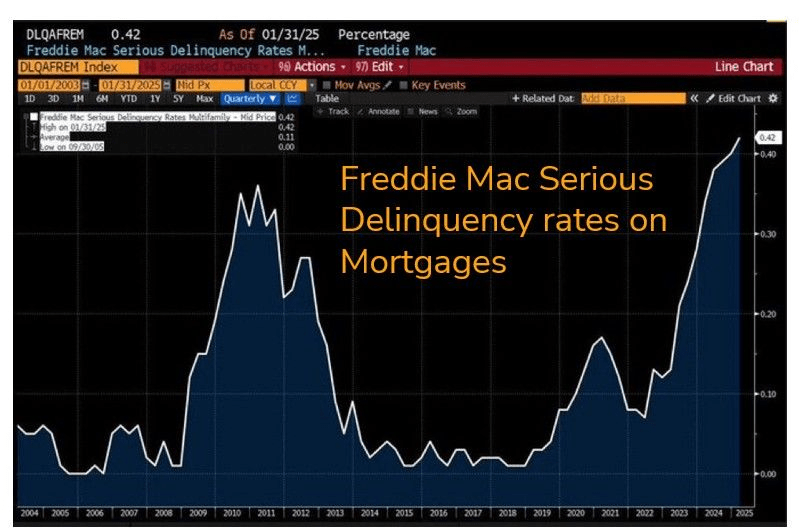

On a related note, Freddie Mac serious delinquency rates on mortgages is now the highest since the financial crisis.

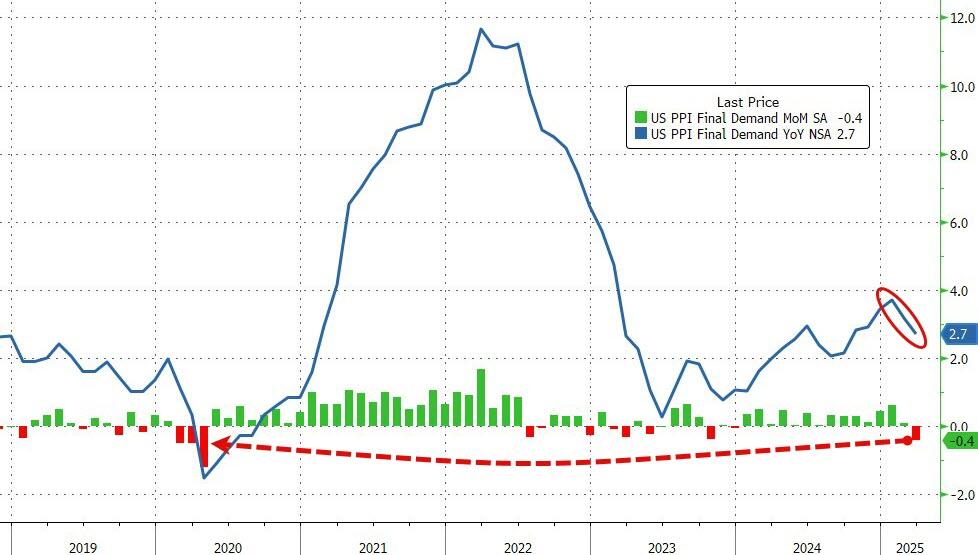

Headline PPI fell (yes fell) 0.4% MoM (dramatically cooler than the 0.2% MoM rise expected), dragging the headline index down to +2.7% YoY.

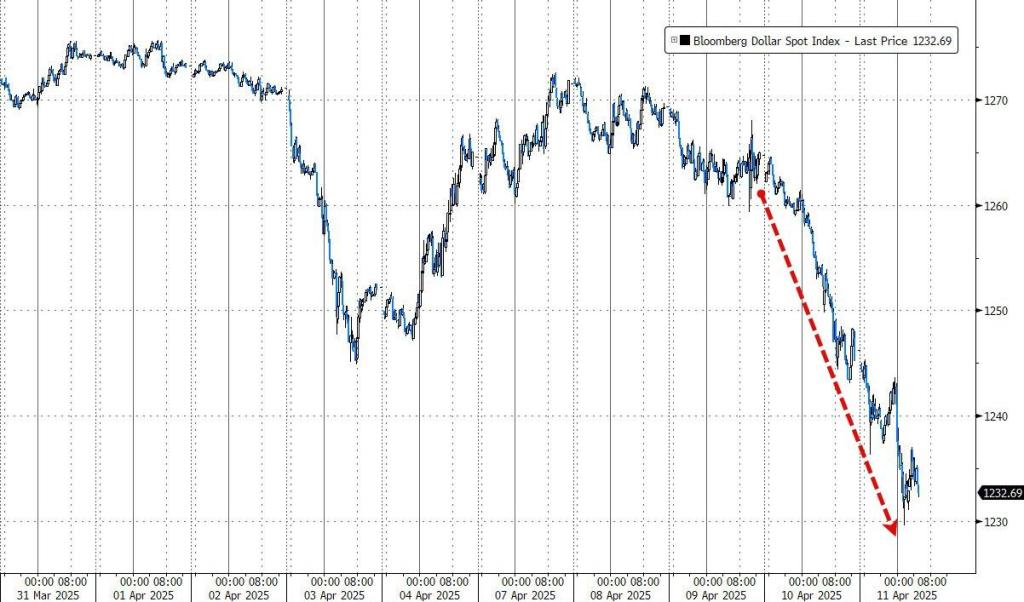

The market is re-assessing the structural attractiveness of the dollar as the world’s global reserve currency and is undergoing a process of rapid de-dollarization.

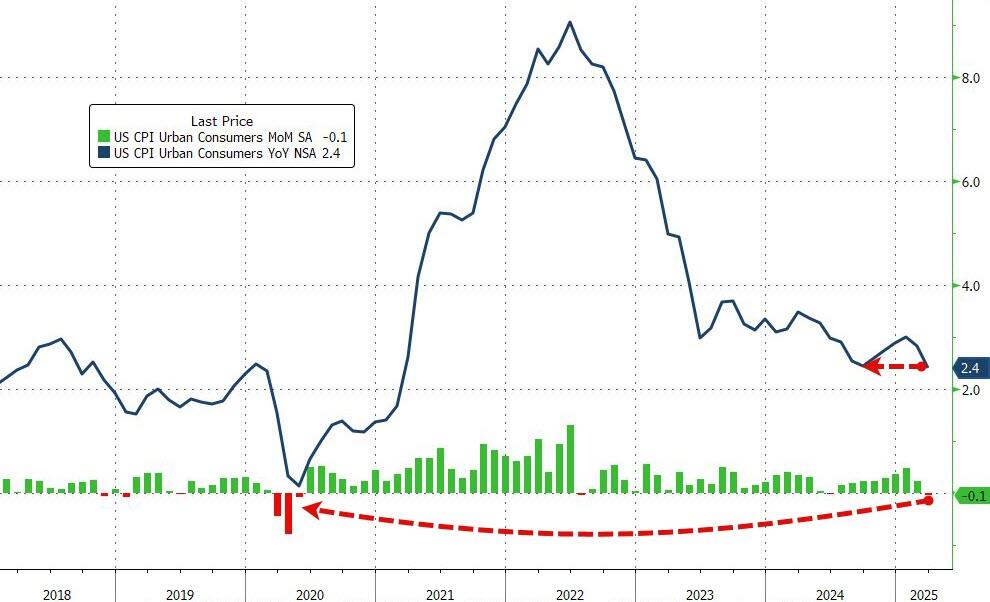

Having dipped lower in the previous month (following a few straight months of re-acceleration), expectations were for both headline and core measures to continue trending lower on a YoY basis… and they were.

Headline CPI FELL 0.1% MoM (vs +0.1% exp), which dragged the YoY CPI to +2.4%, matching the September lows…

Source: Bloomberg

That is the weakest MoM print since May 2020.

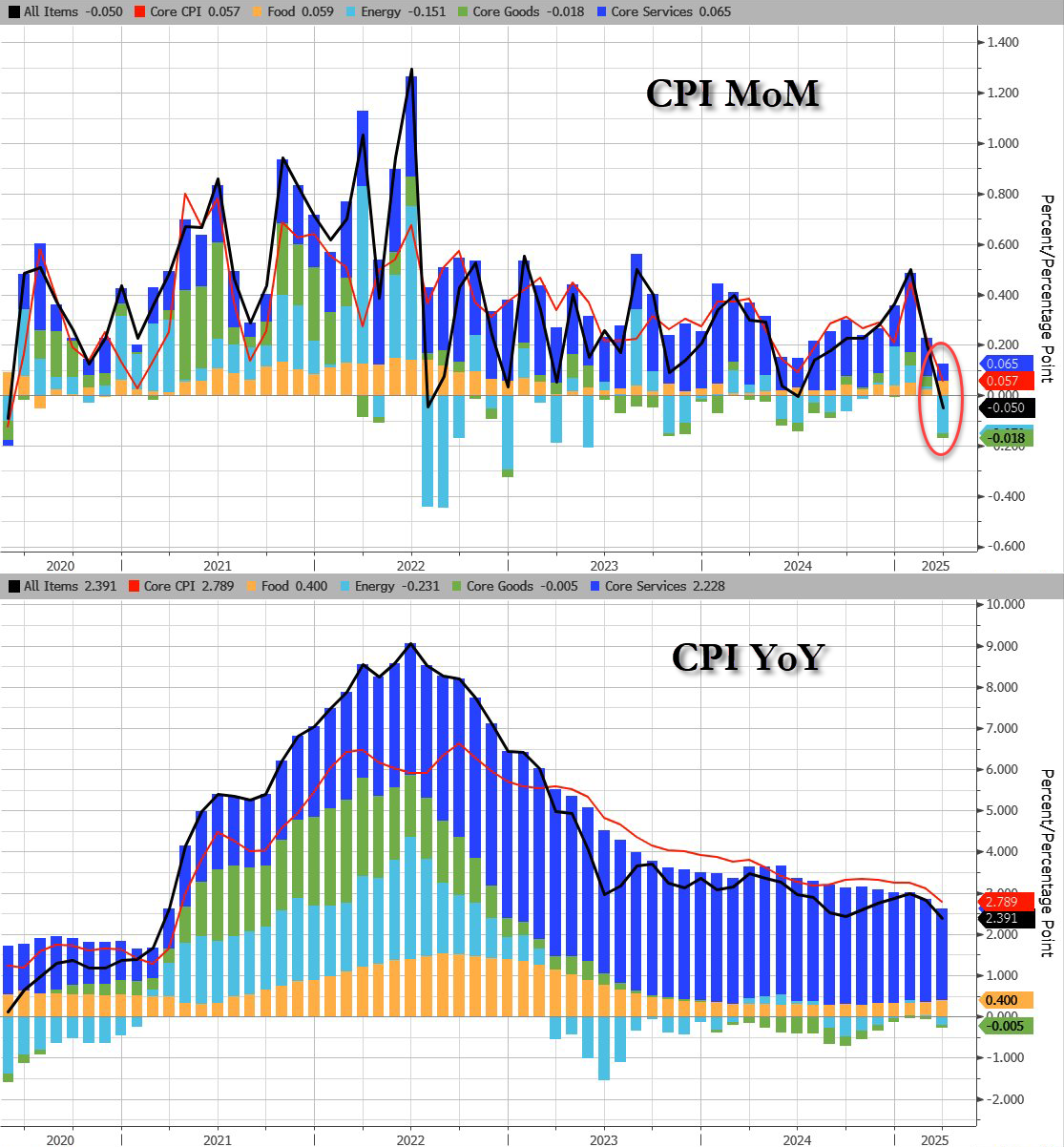

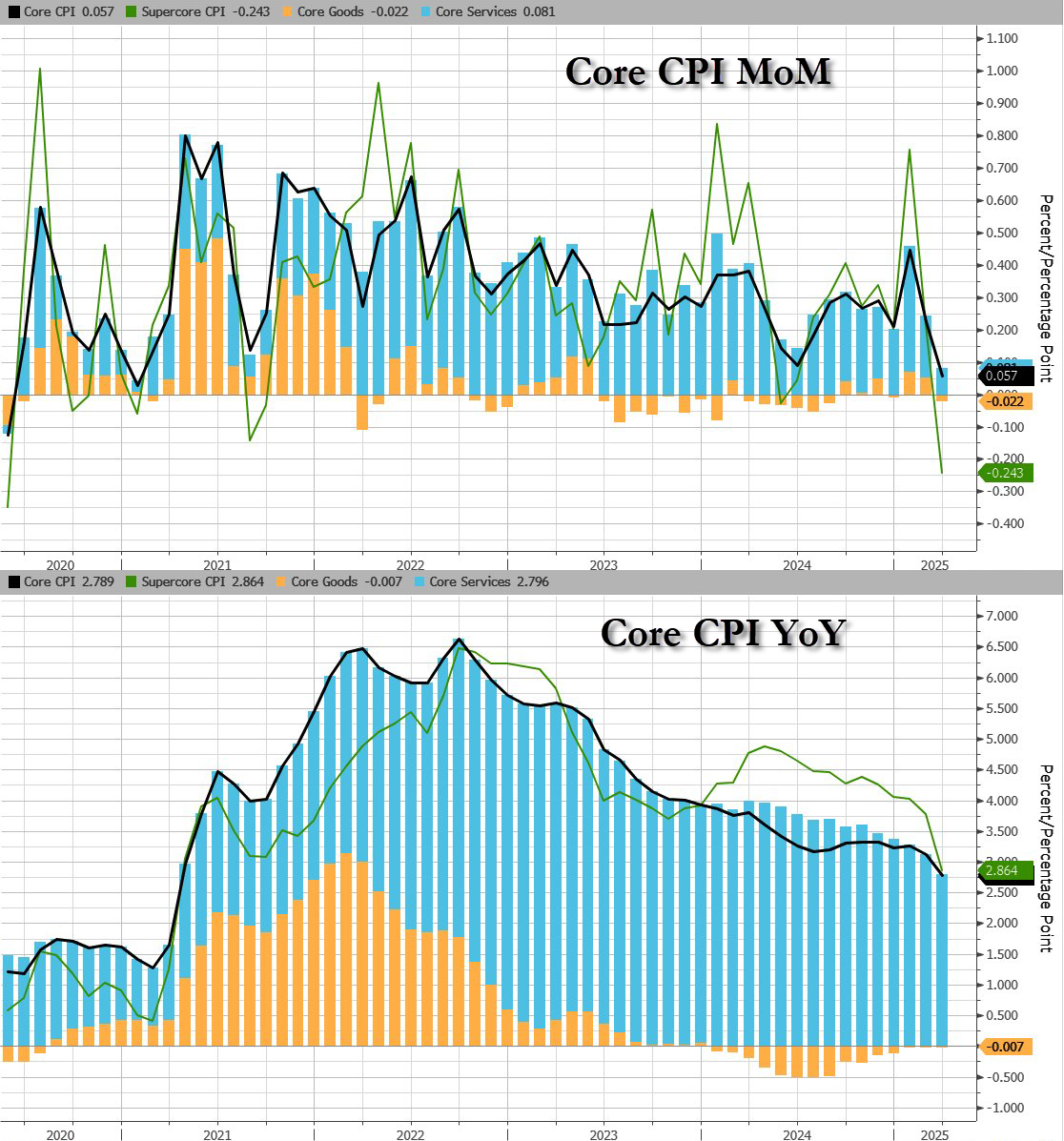

Core CPI also printed cooler than expected (+0.1% MoM vs +0.3% MoM exp), pulling the YoY print down t0 +2.8% YoY – the lowest since March 2021…

Source: Bloomberg

Services inflation tumbled…

Source: Bloomberg

CPI breakdown:

Headline:

CPI decreased 0.1% after rising 0.2% in February, and below the +0.1% estimate. Over the last 12 months, CPI rose 2.4%, below the 2.5% estimate.

Energy CPI fell 2.4% in March, as a 6.3% decline in the index for gasoline more than offset increases in the indexes for electricity and natural gas.

Food CPI rose 0.4% in March as the food at home index increased 0.5% and the food away from home index rose 0.4 percent over the month.

Core CPI:

The index for all items less food and energy rose 0.1% in March, following a 0.2% increase in February.

Indexes that increased over the month include personal care, medical care, education, apparel, and new vehicles.

The indexes for airline fares, motor vehicle insurance, used cars and trucks, and recreation were among the major indexes that decreased in March.

Core CPI details (MoM increase):

The shelter index increased 0.2% over the month.

The index for owners’ equivalent rent rose 0.% in March and the index for rent increased 0.3%.

The lodging away from home index fell 3.5 percent in March.

The personal care index rose 1.0%in March.

The index for education rose 0.4% over the month, as did the index for apparel.

The new vehicles index also increased over the month, rising 0.1%.

The index for airline fares fell 5.3% in March, after declining 4.0% in February.

The indexes for motor vehicle insurance, used cars and trucks, and recreation also fell over the month.

The household furnishings and operations index was unchanged in March.

The medical care index increased 0.2% over the month.

The index for hospital services increased 1.1% in March and the index for physicians’ services rose 0.3% over the month. In contrast, the prescription drugs index fell 2.0% in March.

Core CPI details (YoY increase):

The index for all items less food and energy rose 2.8 percent over the past 12 months.

The shelter index increased 4.0 percent over the last year, the smallest 12-month increase since November 2021.

Other indexes with notable increases over the last year include motor vehicle insurance (+7.5 percent), medical care (+2.6 percent), recreation (+1.9 percent), and education (+3.9 percent).

While goods inflation is flat (zero-ish), services cost inflation is fading fast…

Source: Bloomberg

Shelter and Rent inflation is slowing fast:

Shelter inflation +0.3% MoM, +3.99% YoY, down from 4.25% in February (lowest since Nov 2021)

Rent inflation +0.3% MoM, +3.99% YoY, down from 4.09% in February (lowest since Jan 2022)

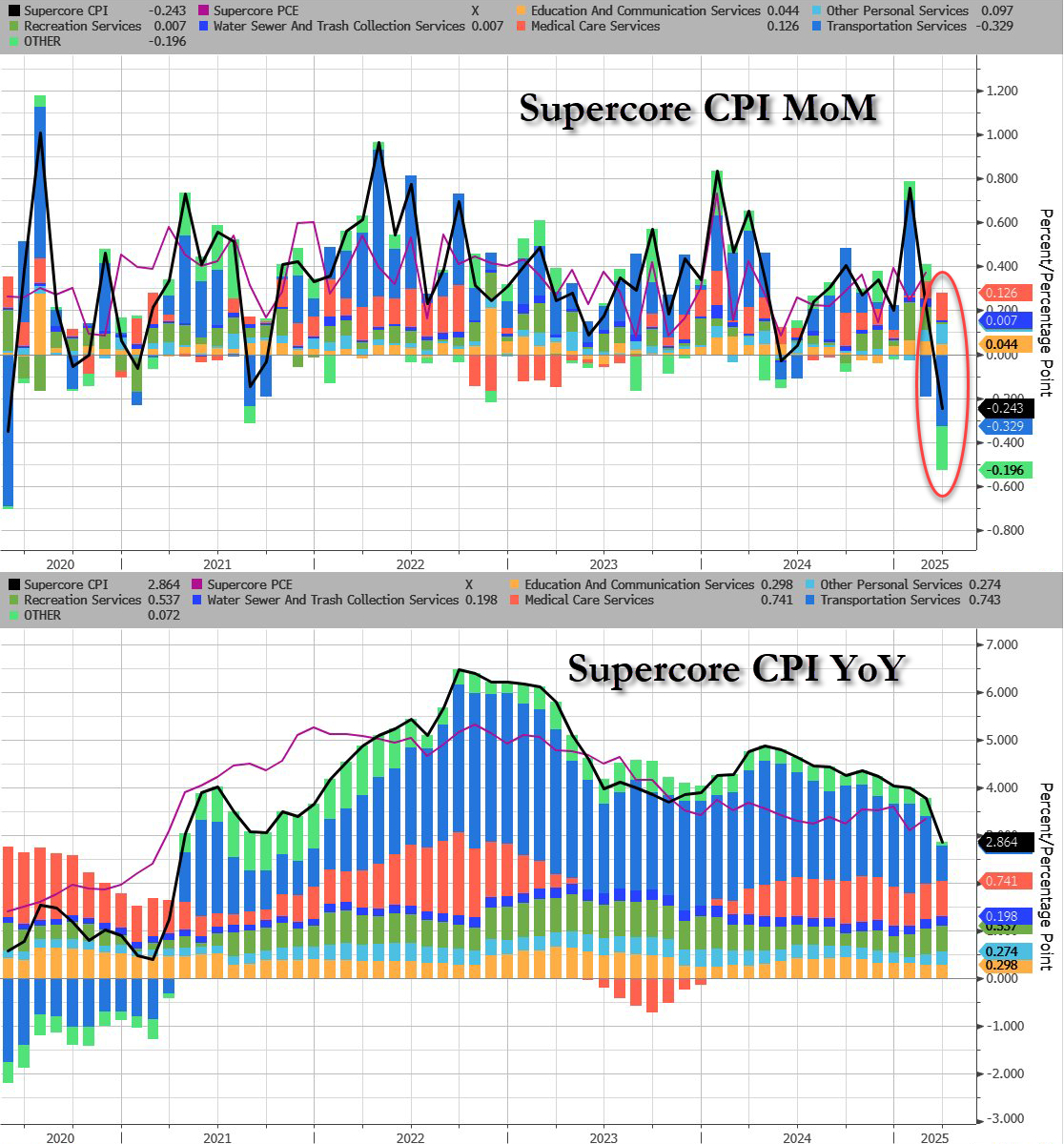

The so-called SuperCore CPI – Services Ex-Shelter – dropped 0.1% MoM dragging it down to +3.22% YoY – the lowest since Dec 2021…

Source: Bloomberg

Source: Bloomberg

Drill Baby Drill (and tariffs recession fears) have dragged energy prices lower and pulled CPI lower with it…

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.