Nothing has been the same since the housing bubble of the 2000s, the resulting banking meltdown and the takeover of the economy by The Federal Reserve.

And since the 2000s housing bubble and financial crisis, The Federal Reserve has taken control of the economy resulting in M2 Money Velocity crashing to historic lows.

Policy blunders perpetrated by the Biden White House have made a bad problem worse.

For instance, oil prices are higher for two reasons. First, U.S. production has declined by about two million barrels per day since 2019, even as demand has recovered from the COVID-19-induced downturn. Oil markets are global, so the fall-off in output would not necessarily jack prices up, but our declining output needs to be offset by an increase elsewhere.

Enter OPEC, which has not restored output to the level necessary to bring down prices, despite repeated pleas from Biden.

Meanwhile, Biden has done a lot to discourage a resurgence in U.S. drilling and production. He has cancelled pipelines, threatened oil and gas producers with higher taxes, taken promising acreage out of play, such as the Arctic Natural Wildlife Refuge, slow-walked leasing and new drilling permits and, most recently, imposed new methane-curbing rules that make drilling more expensive.

What sensible person would invest in the oilfield in the face of such unrelenting hostility? Drilling activity is up, but nowhere near where it should be at $82 per barrel oil.

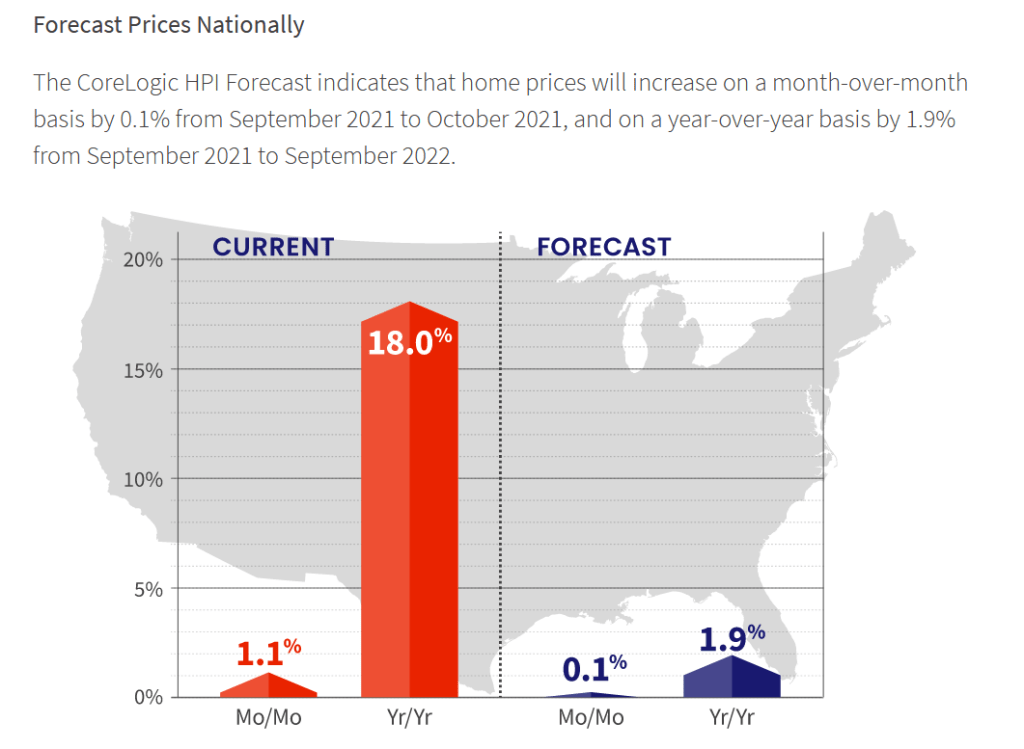

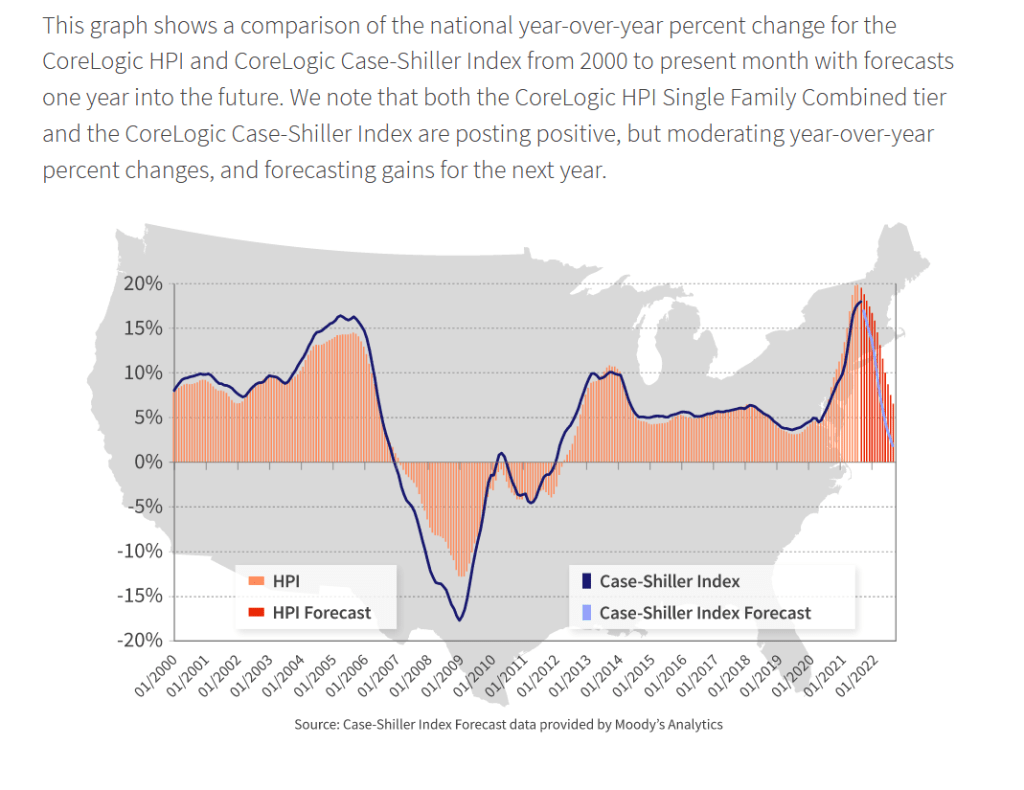

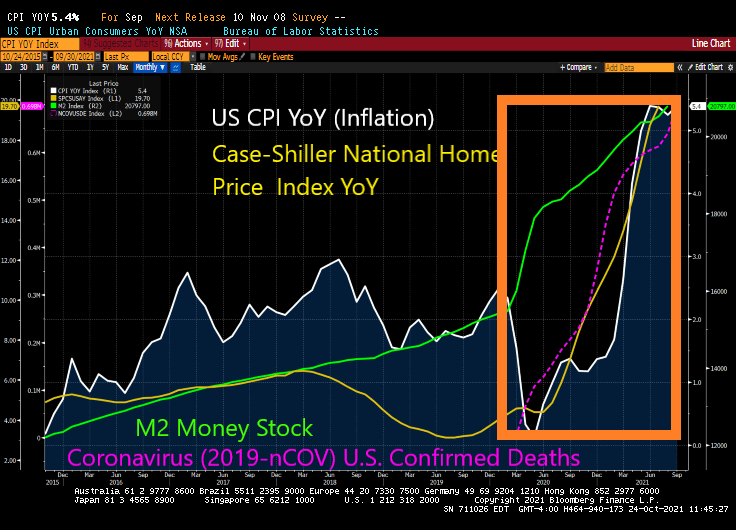

Another boost to inflation came from housing. With “shelter” accounting for some 40 percent of the CPI, economists have warned that fast-rising home prices would eventually seep into higher inflation readings. In October, we saw this occur, with the increase in the cost of shelter accelerating to 0.5 percent from September, an annualized rise of 3.48 percent. The CPI owners equivalent rent of residence rose to 3.13% YoY. Too bad home prices are increasing at almost 20% YoY.

One reason home prices have been increasing at nearly 20 percent per year is that the Federal Reserve has continued to buy up $15 billion worth of mortgage-backed bonds each month, keeping mortgage rates artificially low. The result has been a booming market, driving home prices, and now rents, higher.

At long last, the Federal Reserve has announced it will begin to throttle back its bond-buying program, including the purchases of mortgage-backed bonds. Critics think the Fed is behind the curve, having seriously underestimated price pressures.

Biden does not control the Fed, but he has made no secret of his preference for the easy money policies that have helped prop up the economy, and the stock market. Fed Chair Jerome Powell’s term ends in February; Biden has recently interviewed not only Powell but also Fed Governor Lael Brainard, a known dove and Obama appointee, for the position.

That these are the only two candidates he seems to be considering sends a clear signal. He will choose growth over stability, even if it means that inflation continues to accelerate. Unhappily, Powell is listening.

Finally, Biden has not only encouraged monetary excess, but has also endorsed big-spending packages that have put money in consumers’ pockets but also kept workers on the sidelines. The biggest shortage we have in this country today is labor. The labor participation rate is mired at 61.6 percent, 1.7 percentage points below the level in February 2020.

Studies have shown that the slew of benefits contained in the Cares Act and subsequent relief bills, including incremental unemployment benefits, expanded child tax credits and rent moratoriums, have offered Americans up to $100,000 per year while not working. These payments may have been necessary early in our recovery from the pandemic, but no longer are needed.

And then people are surprised that grocery prices are getting so f&^*ing high???

Wu-Xia employs an approximation that makes a nonlinear term structure model extremely tractable for analysis of an economy operating near the zero lower bound for interest rates. It can be used to summarize the macroeconomic effects of unconventional monetary policy (ZIRP + QE). The Shadow Rate is now -1.7021%.

And you wonder why we have inflation and house prices going into orbit?

With inflation also going into orbit, we see that breakeven 10 year inflation rate rising above the 5Y5Y (nominal forward 5 years minus US inflation-linked bonds forward 5 years). In other words, the US has abnormally high inflation and is expected to grow and NOT be transitory.

The Shadow knows … that the US is hyperstimulated. And inflation isn’t going away anytime soon.

With The Federal Reserve leaving its target rate at 0.25%, but hinting at a tapering (slowdown) of asset purchases, I thought it would be good to present where The Fed sits at the moment.

You can see the rise in the effective Fed Funds rate from 2016 to early 2020, then KABOOM! COVID struck, the effective Fed Funds rate crashed while The Fed dramatically increased their purchases of Treasuries and Agency MBS. Both Treasury and Agency MBS purchases are projected to decline by mid-2022. The Fed’s target rate (purple line) is project to rise to 1% after 2023.

Where SHOULD The Fed Funds Target rate be? How about 8.80% instead of 0.25%.

So we still have over-stimulypto with The Fed projected to raise rates at a snail’s pace.

Face it, Wall Street wants interest rates low, even if inflation burns out of control.

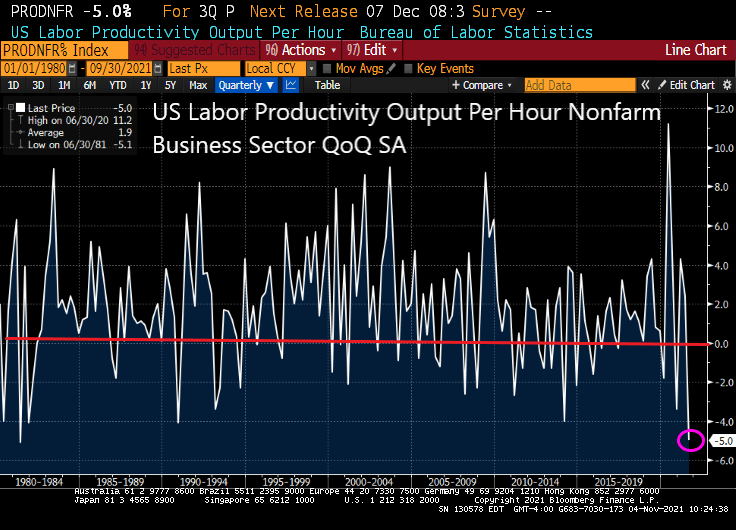

The last time we saw US labor productivity out per hour this low was in 1981 when President Reagan inherited stagflation from President Jimmy Carter.

As unit labor costs soar +8.3%.

Any wonder that the 1% have been doing so well relative to the bottom 50% in terms of wealth since entrance of The Fed in 2008 with zero-interest rate policies (ZIRP) and assets purchases (QE). And also after Covid struck.

“That will be $10,000 for your Big Mac, fries and a soda, please!”

Nothing has been the same since Covid struck in early 2020.

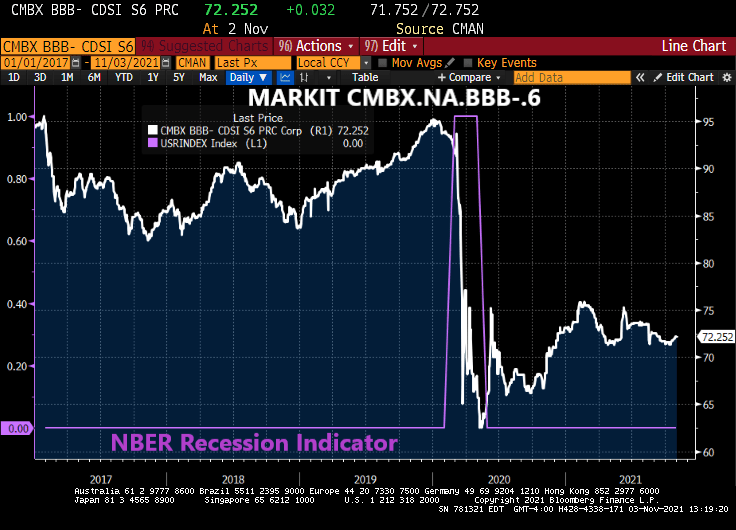

CMBX BBB-, the reference basket for CMBS 6, was climbing to around $95 prior to the Covid outbreak and resulting recession. The CMBX reference basket is now at $72.25.

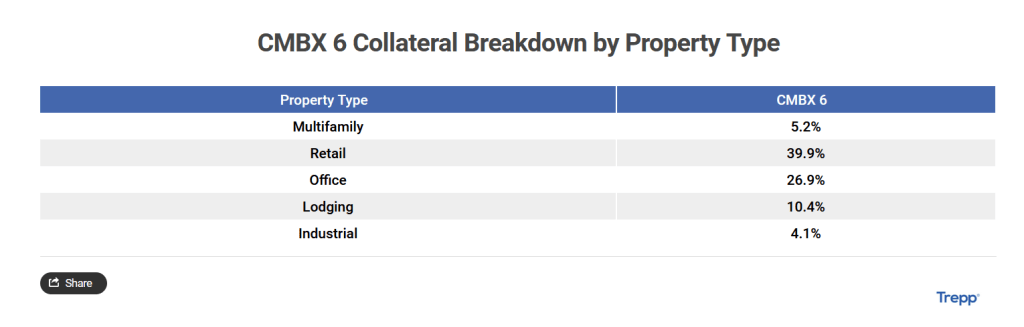

CMBX 6 is largely composed of retail and office, both hit hard by Covid and the ensuing lockdowns and fearmongering by the Federal government and main street media.

But the forecast for home price growth is for 1.9% YoY in 2022.

As home price growth crashes back to earth as wages don’t keep pace with home prices.

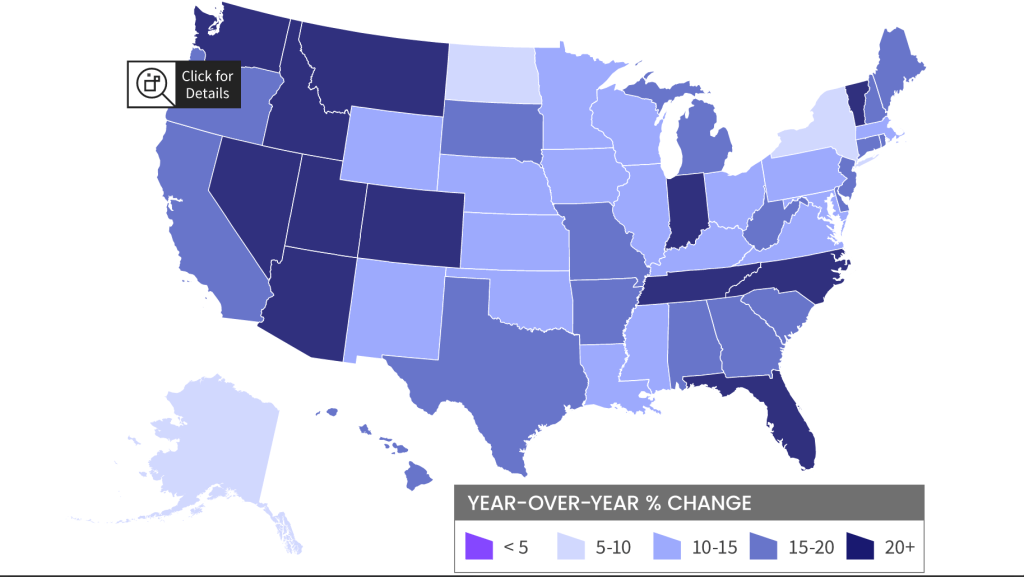

Home prices have been growing in most states out west where The Fed’s money pump has resulted in a boom in second homes and people escaping high tax California and Oregon for Nevada, Idaho, Arizona (again), Utah and Montana. The east coast is seeing the Carolinas booming along with Florida and Indiana. Escape from New York?

Escape from LA … to Arizona, Nevada, Idaho and Utah?

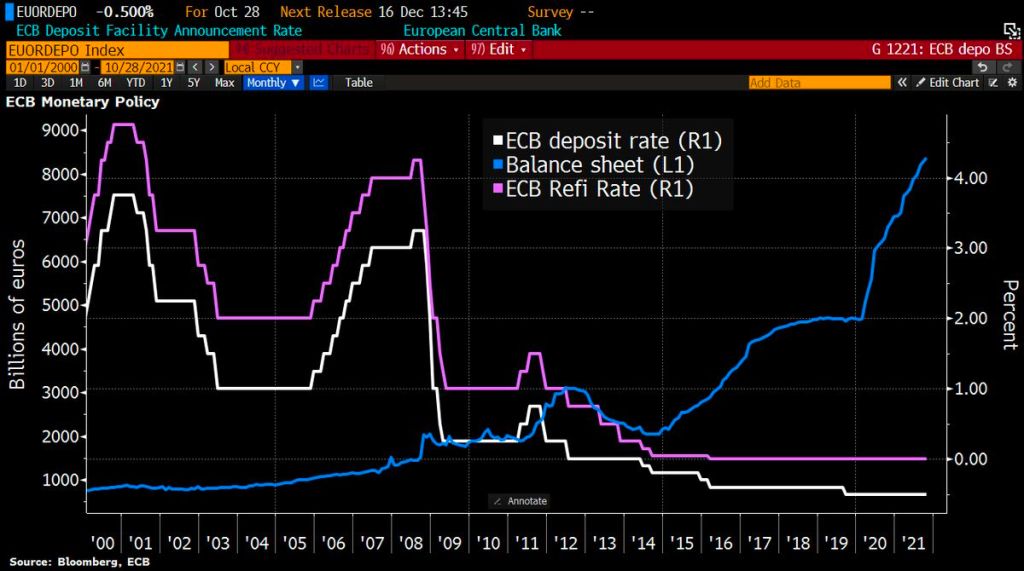

With central banks around the world signalling tighter policy amid rising prices, Lagarde said the ECB had done much “soul-searching” over its stance but concluded that inflation was still temporary, so a policy response would be premature.

Soul-searching? The ECB is just doing what Powell and the Fed (aka, Jerome Jett and the Blackhearts) are doing. Keeping the foot on the monetary gas pedal in the face of inflation.

Let’s start Eurozone inflation. It is now sitting a 4.10% YoY. And core inflation is sitting at 2.10% YoY. Inflation is now the highest since 2009 while core inflation is at the highest since 2001.

Like the Federal Reserve, the ECB still has its foot on the monetary accelerator pedal despite booming inflation.

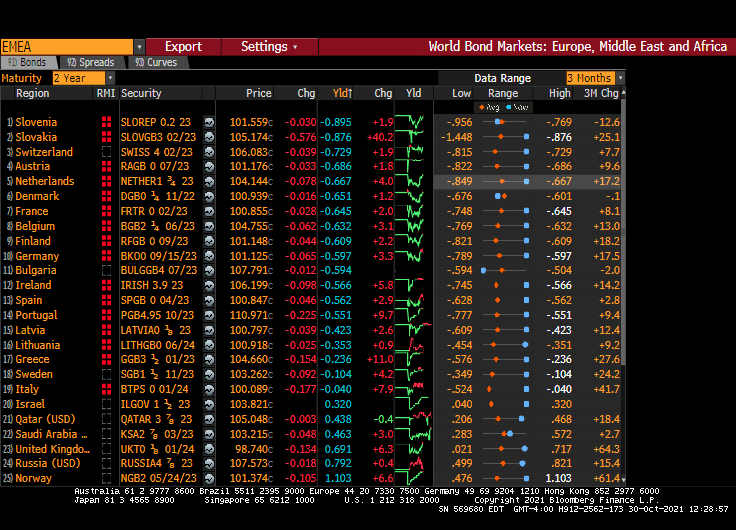

So, Christine, 19 nations in “Europe” having negative 2-year sovereign yields isn’t low enough for you?

The ECB’s platform in Frankfurt reminds me of a bad TV quiz show where participants try to guess prices next year. Call it “The Price Is Wrong.”

Unless, of course, the ECB sees a massive depression ahead.

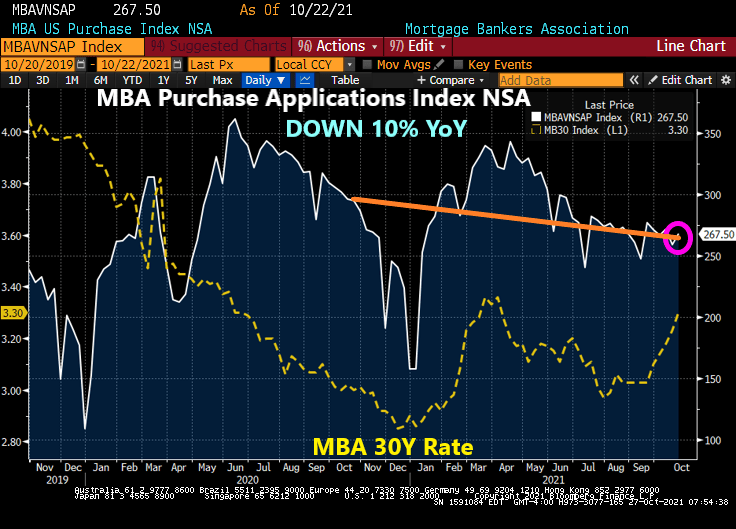

Mortgage purchase applications rose 3.24% from the previous week, according to data from the Mortgage Bankers Association. However, purchase applications are down 9.3% from

Mortgage refinancing applications declined -1.57% from the previous week as mortgage rates rose from 3.23% to 3.30%.

The Federal Reserve is helping to create inflation, particularly since their unorthodox surge in money supply around the Covid outbreak in early 2020. Home prices as of the latest Case-Shiller report are rising at nearly 20% year-over-year.

To add to the problem of The Fed’s overzealous money printing we have The Biden Administration (and puppy-torturer/killer Anthony Fauci) issuing Covid vaccine edicts that are wreaking havoc in labor markets further clogging the economic pipelines.

Between The Fed ZIRP policies and Biden/Fauci’s vax mandates, we are starting to see the rise (again) of the infamous MORTGAGE TILT EFFECT!

The Tilt Effect comes about as expected inflation gets priced into mortgage rates, the mortgage payment rises as the mortgage rate rises (of course), but the higher mortgage payment occurs with EXPECTED inflation in the future.

But not quite yet. Despite CPI inflation growing at 5.4% YoY, Freddie Mac’s 30-year mortgage survey rate is only 3.01% … for now.

As inflation continues to rise (thanks to ongoing Fed ZIRP policies and governments mandating Covid vaccine in order to keep your job, we should eventually see mortgage rates rise … leading to a return of THE TILT EFFECT. Which in turns make housing even MORE unaffordable.

We have tried numerous mortgage contracts in the past (mostly to offset Carter-era inflation) such as the PLAM (price-level adjusted mortgage) and the GPM (graduated payment mortgage). Now we have the PLUM (price level unadjusted mortgage) which is subject to the TILT EFFECT.

You must be logged in to post a comment.