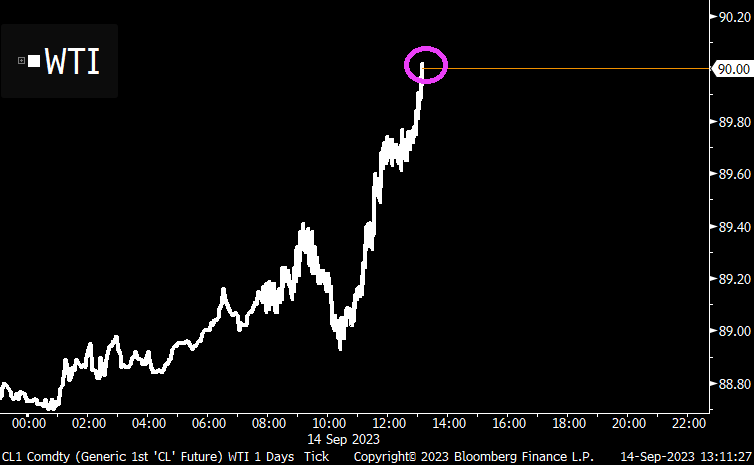

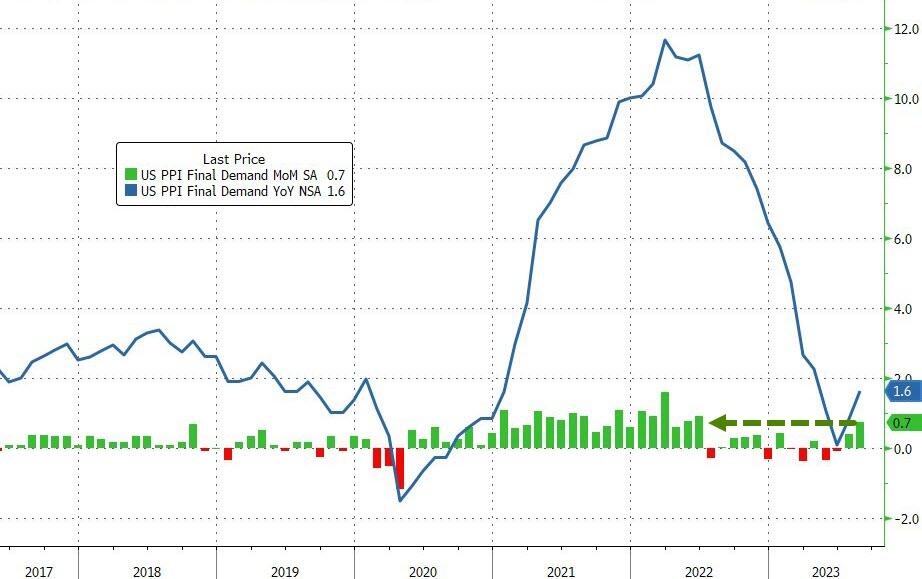

Producer Prices rose 0.7% MoM in August (up from +0.3% in July and hotter than the +0.4% exp). That is the hottest PPI since June 2022, and pushed YoY prices up 1.6%…

Source: Bloomberg

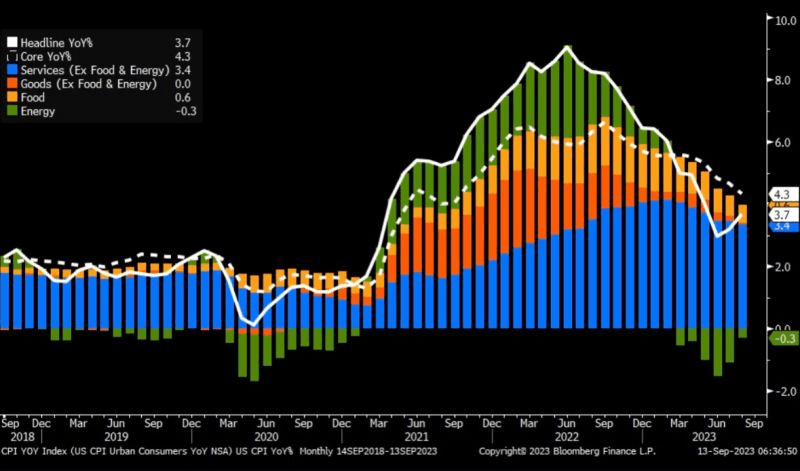

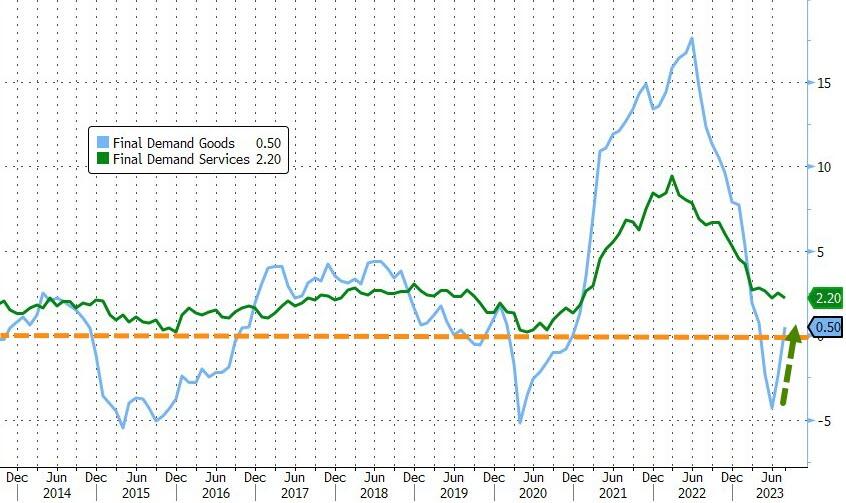

Goods prices are reaccelerating fast, now back into inflation YoY (as Services cost growth slowed only modestly)…

Source: Bloomberg

As a reminder, much of last month’s PPI rise was driven by a big jump in portfolio management costs – as stocks soared. August saw a further rise in those costs…

Source: Bloomberg

More problematically, the pipeline for PPI appears to have inflected as intermediate demand is re-accelerating…

The Federal Reserve, the most powerful Socialist machine on the planet, is considering rate their target rate after some bad economic news.

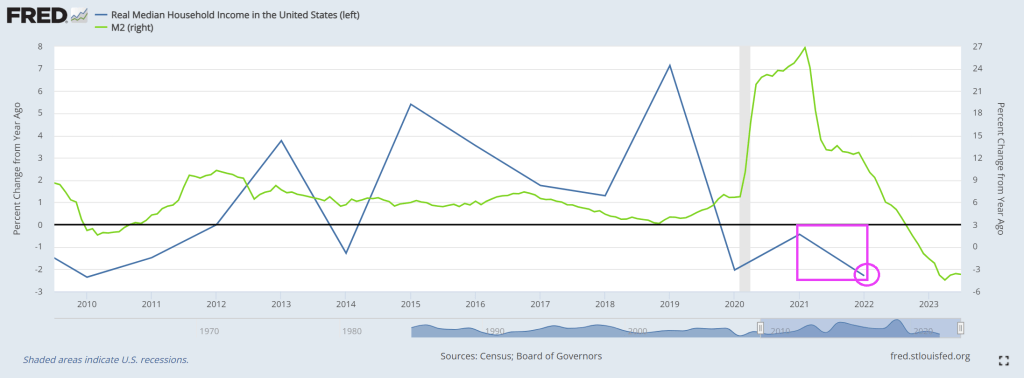

First, real median household income (released yesterday for 2022) showed a decline of -2.3%. That is the worst decline 2010 when Biden was Vice-president. Notice that real median household income has never been positive under Biden (I doubt if PressSec Jean Pierre will brag about this!)

This is particulary dangerous since it was the worst correction in home prices since two rather nasty recessions of 1970 and 2008 (The Great Recession and financial crisis). This correction occured as M2 Money growth (green line) went negative.

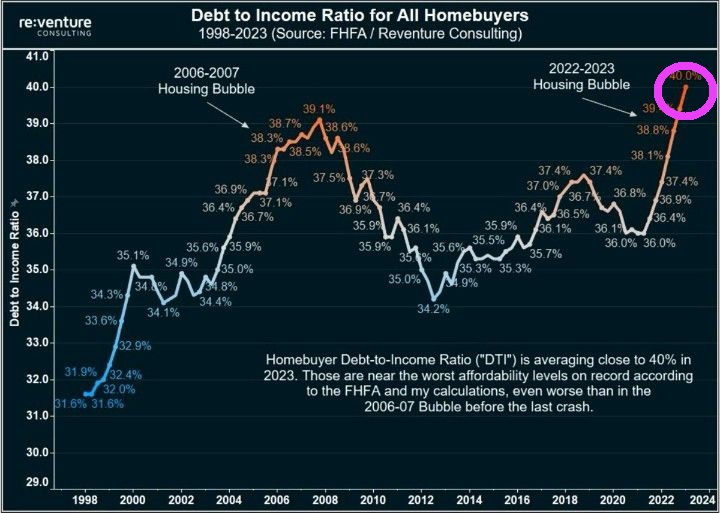

With Fed rate hikes, debt to income ratios are the highest in history.

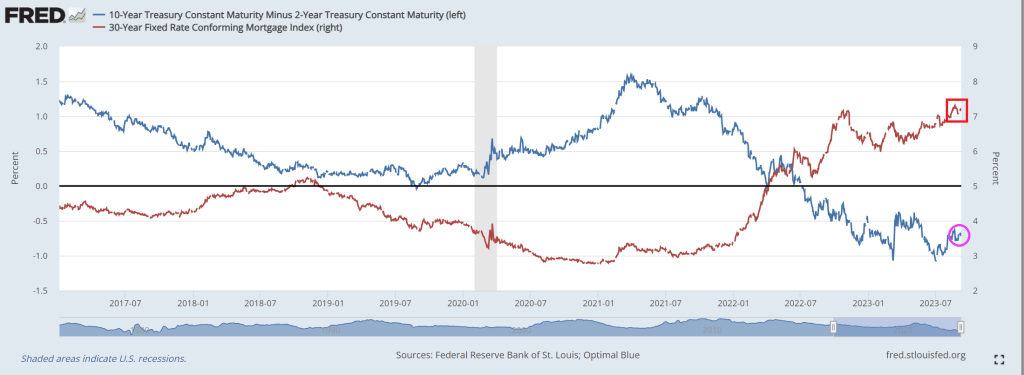

Mortgage rates are above 7% under Biden and Powell (not Baden-Powell, the founder of the Boy Scouts).

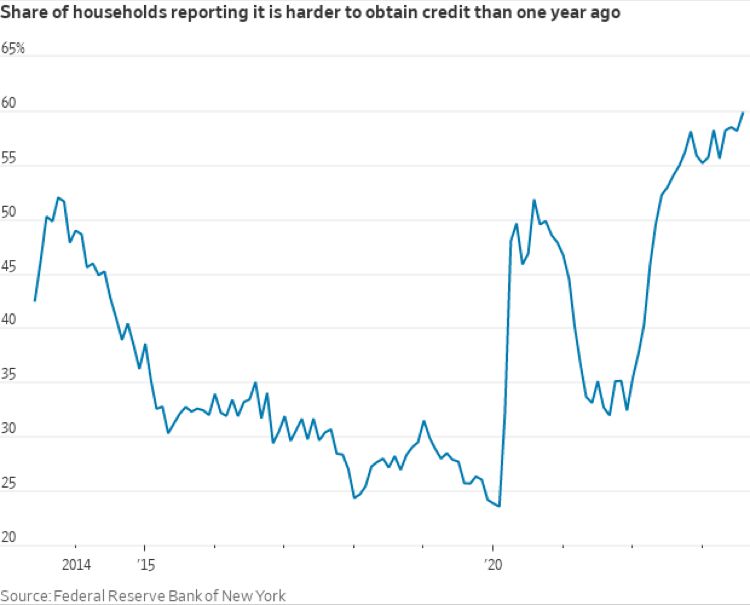

But not only are mortgage rates above 7%, but the mortgage credit box is tightening.

Actually, I have to Spain numerous times and love visiting Barcelona. But the US debt fiasco under Biden and Congressional spending sprees has led to … US credit default swap being priced worse than Spain’s CDS.

With Biden/Congress orgy of spending (and a declining economy in many important respects), the US is seeing Federal debt near $33 TRILLION and even worse, unfunded Federal liabilities (promises, promises) are at $193 TRILLION, almost 6 times the current Federal debt load.

If you are into archaelogy and fossils, Nancy Pelosi (83) has announced that she is running for re-election to The House. Hasn’t San Francisco suffered enough under Feinstein, Newsom and Mayor Breed?

What a mess Biden and his Progressive backers have made. And we are forced to suffer the consequeinces of his policies. Or follies!

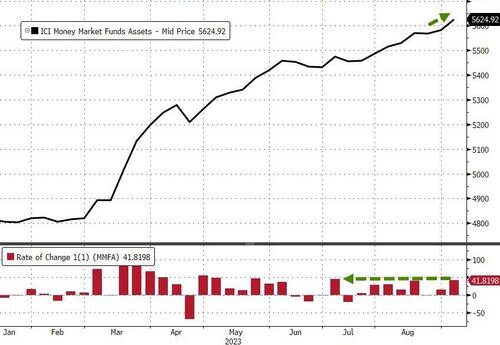

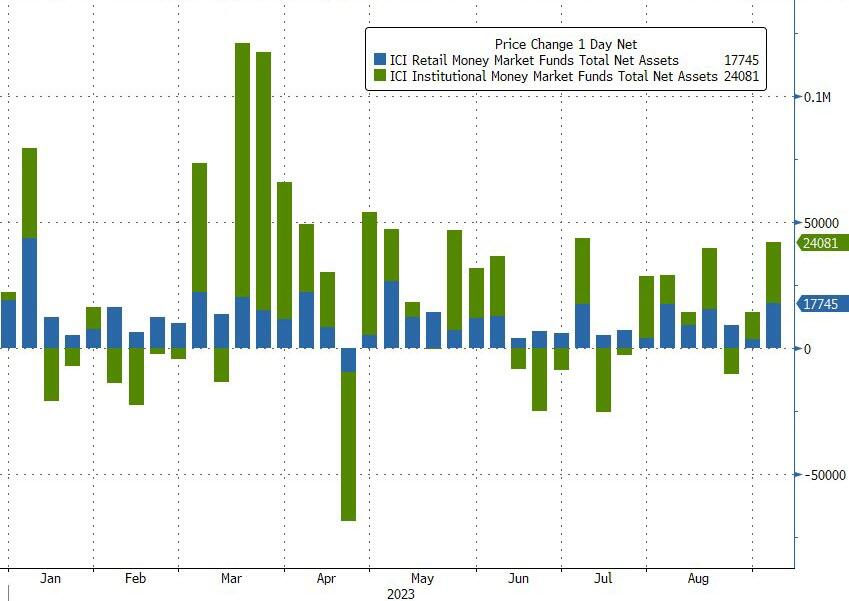

Money-market funds saw inflows for the 7th week of the last 8 with a $42BN jump (the most in 2 months) to a new record high of $5.625TN…

Source: Bloomberg

The inflow was dominated by a $24BN increase in Institutional fund assets while Retail also saw a sizable $17.7BN increase…

Source: Bloomberg

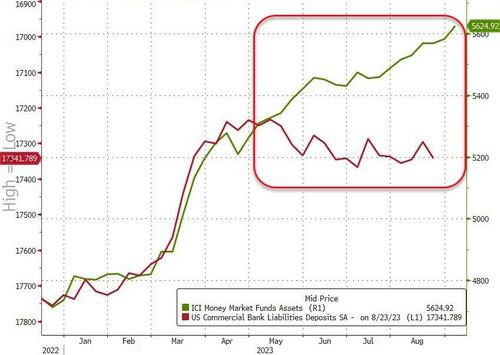

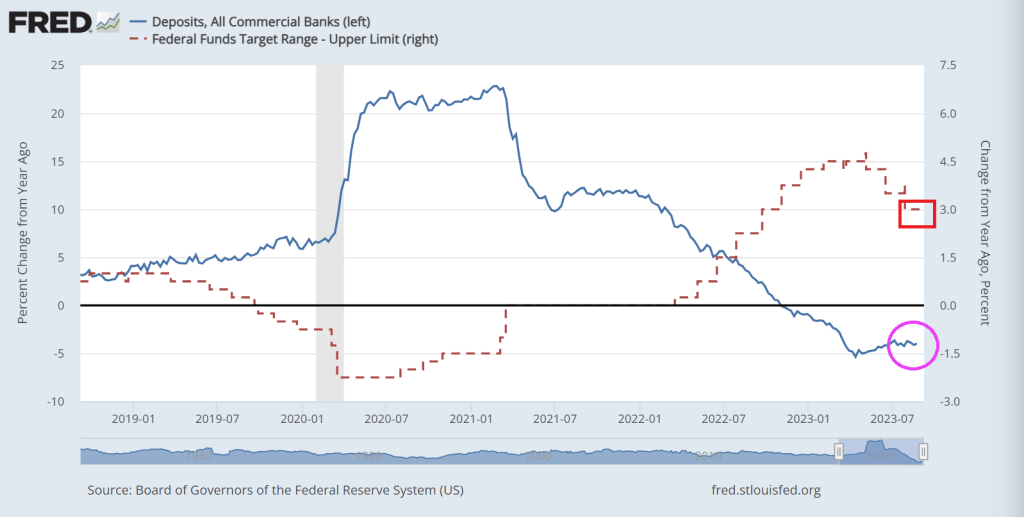

And the divergence between money-market fund assets and bank deposits continues to grow…

Source: Bloomberg

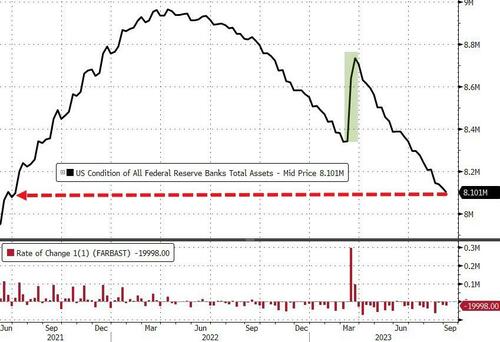

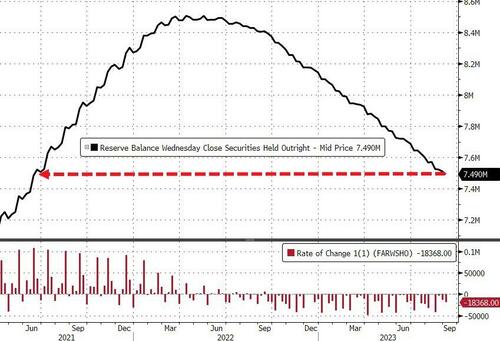

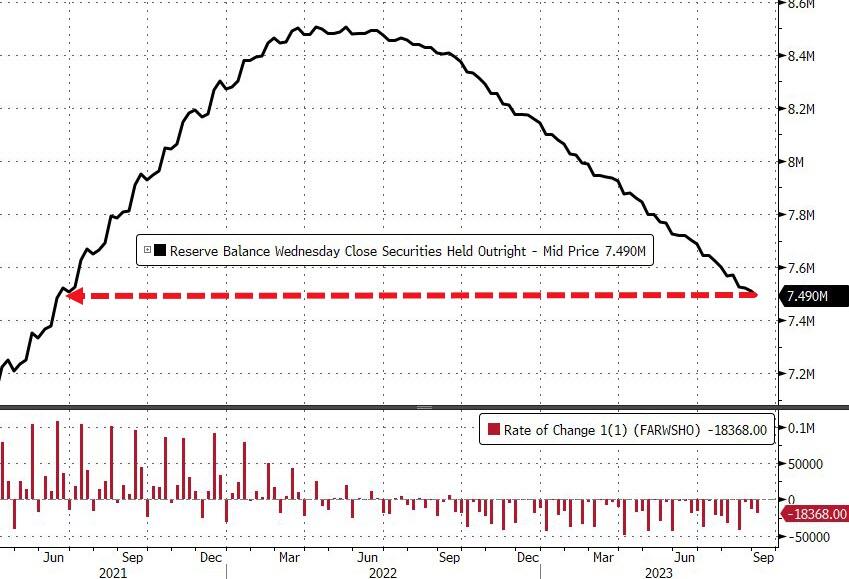

And while we actually saw huge deposit outflows (on a non-seasonally-adjusted basis) – despite The Fed’s seasonally-adjusted deposits increase – The Fed balance sheet shrank by another $20BN last week to its smallest since June 2021…

Source: Bloomberg

The Fed’s QT program continues apace with$18.4BN sold last week to its smallest since June 2021…

Source: Bloomberg

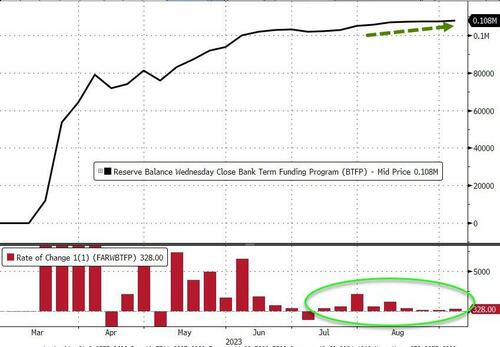

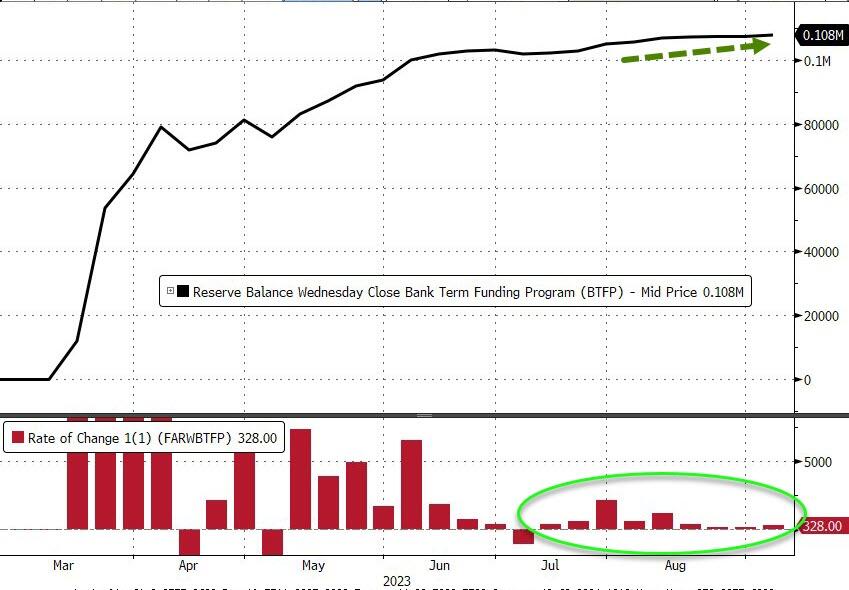

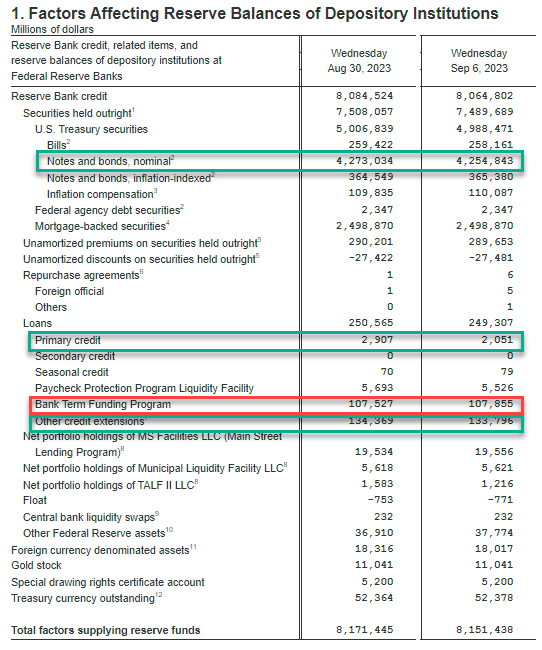

Usage of The Fed’s emergency bank funding facility jumped by $328 Million last week to a new high of $108BN…

Source: Bloomberg

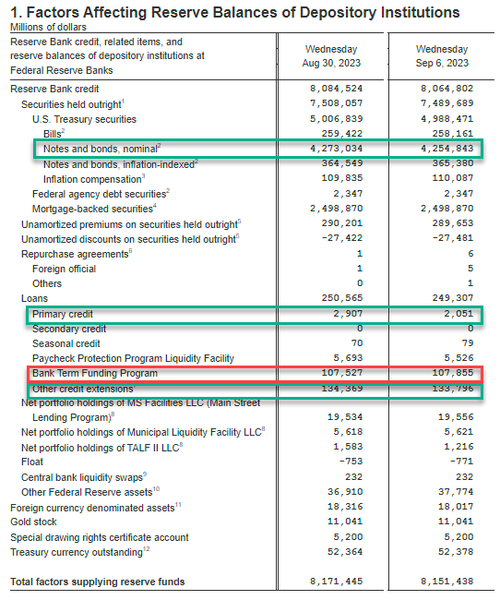

Fed BS weekly change:

Fed balance sheet QT (Notes and bonds decline): $4.255 trillion, down $18,2BN

Discount Window $2.1BN, down $800M from $.29BN

BTFP new record $107.9BN, up $400MM

Other Credit Extensions (FDIC Loans): $133.8BN, down $0.6BN from $134.4BN

Finally, US equity markets and bank reserves at The Fed have converged a little recently, but the gap remains wide (thanks to the plunge in reverse repo balances)…

Source: Bloomberg

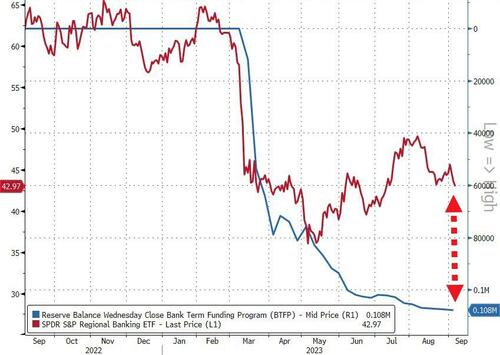

Tick, tock, banks!

Source: Bloomberg

You have six months to figure out how to clean up the $108 Billion hole in your balance sheet that you’re currently paying The Fed’s exorbitant rates to fill.

Bank deposit growth remains negative as The Fed tightens its overly accomodative monetary policy.

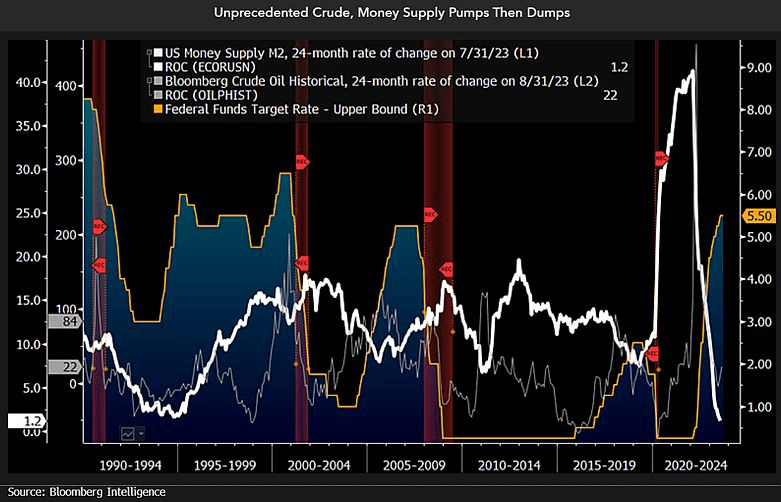

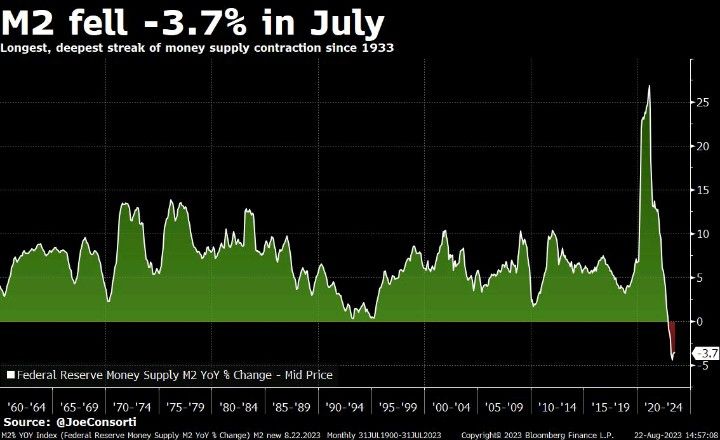

And then we have this chart showing plinging M2 Money (white line fever).

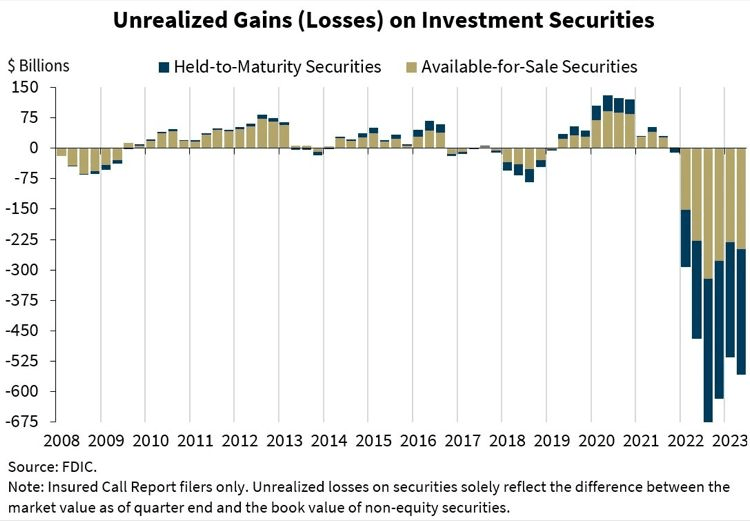

And the horrific unrealized losses on bank’s books.

Bidenomics is failing America. Primarily because Biden was one of the stupidest members of the US Senate. Not to mention nasty. Great President, America! /sarc

Speaking of Bidenomics, US mortgage purchase demand just declined to the lowest level in 28 years.

Mortgage applications decreased 2.9 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending September 1, 2023.

The Market Composite Index, a measure of mortgage loan application volume, decreased 2.9 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 5 percent compared with the previous week. The Refinance Index decreased 5 percent from the previous week and was 30 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 2 percent from one week earlier. The unadjusted Purchase Index decreased 5 percent compared with the previous week and was 28 percent lower than the same week one year ago.

This is not good.

Bank deposits, a source of bank lending, are down -4% YoY as The Fed tightens rates.

Here is Lefty Frizzell’s original version of the Bidenomic’s themesong “If you’ve got the money, honey,I’ve got the time.” Like big donors receiving green energy subsidies. But not middle class mortgage borrowers.

The cost of living has been soaring, and our standard of living has been steadily going down.

Coping with inflation is tough for American households where consumer debt is up 19.$ under Biden while the free-spending Federal government’s public debt is up only 16.5%.

“In July 2023, 61% of U.S. consumers live paycheck to paycheck, unchanged from June 2023, but 2 percentage points higher than July 2022. Generally, more consumers of all income brackets reported living paycheck to paycheck in July 2023 than last year,” Alia Dudum, a money expert at LendingClub told FOX Business.

Now, 78% of consumers earning less than $50,000 a year and 65% of those earning between $50,000 and $100,000 were living paycheck to paycheck in July, both up from a year ago, LendingClub found. Of those earning $100,000 or more, only 44% reported living paycheck to paycheck.

Because consumers have so little disposable income these days, retailers all over the nation are experiencing difficulty.

In fact, UBS is projecting that 50,000 stores could close in the United States by the end of 2027…

Analysts at investment bank UBS are forecasting that some 50,000 U.S. stores are likely to close by the end of 2027, because of expected cutbacks in consumer spending, tighter credit and the continued shift to ecommerce.

Store closings could accelerate to 70,000 to 90,000 if retail sales turn out to be weaker than expected, according to UBS.

Actually, I think that losing 50,000 stores is a wildly optimistic scenario.

Hopefully I am wrong about that.

The housing market has also been going haywire.

According to Fortune, the month of August “will become the worst month for housing affordability this century”…

On Monday, the average 30-year fixed mortgage rate reached 7.48%, marking the highest level since the year 2000. Even prior to this recent surge in mortgage rates, housing affordability, as monitored by the Atlanta Fed, had already deteriorated beyond the levels seen at the housing bubble’s peak in 2006. Once this latest mortgage rate surge is factored in, August 2023 will become the worst month for housing affordability this century.

Wow.

Thanks Delaware Joe Biden (as opposed to Country Joe Stalin).

Home prices are going to have to come down, and in some areas they have already fallen quite a bit…

Homeowners are sitting on a negative equity timebomb after losing $108.4 billion on their property values this year, experts say.

The average borrower saw their home equity plummet by $5,400 in the first quarter of 2023 compared to last year – with households in Washington, California and Utah worst affected.

Do you remember the housing crash of 2008 and 2009?

Well, now the next housing crash is here, and it isn’t going to be fun.

For a while there, Joe Biden and his minions could at least boast about the employment market.

But now large companies all over America are laying off workers, and it is being reported that a staggering 1.223 million native-born Americans lost their jobs during the months of July and August…

Staggering figures have revealed that over 1.2 million US-born workers lost their jobs last month while the foreign-born workforce increased by nearly 700,000 – as migrants continue to flood across the border under the Biden administration.

Data from US Bureau of Labor Statistics show that between July and August, there was a staggering decrease of 1.223 million native-born people in the workforce – which is a low not beaten since the jobs crash when Covid hit in April 2020.

The numbers that I have shared with you are nothing to brag about.

But Joe Biden is going to keep trying to pull the wool over the eyes of the American people anyway.

Unfortunately for Biden, it has become quite clear that most Americans have lost faith in him. According to the same Wall Street Journal poll that I mentioned above, 73 percent of U.S. voters now believe that Biden “is too old to run for president”…

For Biden, one of his biggest challenges is age. The Wall Street Journal poll found that about 73% of voters think Biden is too old to run for president while only 47% think Trump is too old. Thirty-six percent of voters think that Biden is mentally up for the job while 46% of voters think Trump is mentally capable of being president.

We have never seen numbers like this for any other president.

Sadly, Biden fully intends to run again. (Especially since half-wit Jill Biden is allegedly running The White House).

And the Democrats will get behind him, because at this point no other candidate is posing a serious threat to Biden. Wait, not Gavin Newsom who almost single handedly destroyed California or Michelle Obama who has absolutely no qualifiications?? Other than being Barry Soetoro’s wife?

The glories of Bidenomics is on fully display. Despite what Lyin’ Biden says, Bidenomics is only working for the elites (top 1%). How Soviet/CCP command economy of him!

Here is an ugly chart showing Bidenomics in action! We all know that Covid unleashed a torrent of Fed monetary stimulus AND Federal spending on Covid relief and green energy subsidies (most to large Democrats donors). BUT we now have experienced 3 consectutive quarters of negative gross domestic income (GDI) growth. And nominal GDI growth is falling with falling M2 Money growth.

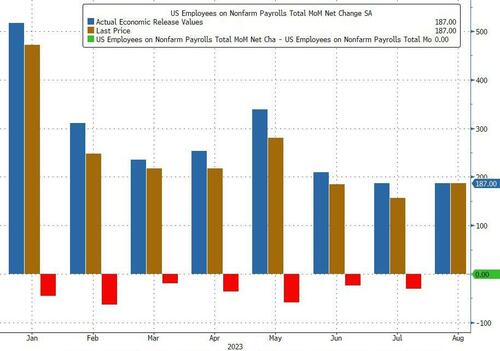

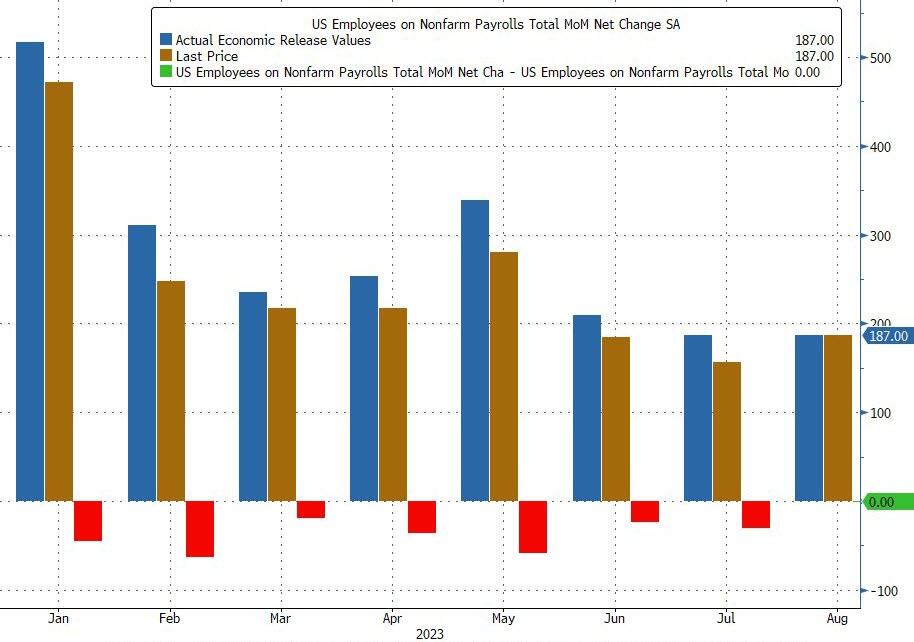

And today’s jobs report for August showed that only 187k jobs were added.

Superficially this would have meant an unchanged print from last month when the BLS also reported 187K jobs, however in keeping with recent trends that number was revised – drumroll – lower again, to 157K, meaning that every single monthly payrolls print in 20-23 has been revised lower (see chart below), a 12-sigma probability and virtually impossible unless there was political pressure to massage the data higher initially and then revise it lower when nobody is looking. (As if the mainstream media is at all honest!)

But wait there’s more: while July was revised down by 30K from +187,000 to +157,000, June was revised even more, by 80,000, from +185,000 to +105,000, which means that a number that was originally reported as 209K has been reivsed 50% lower, to 105K and a collapse vs original expectations of 230K. Here, the BLS was proud to report that “with these revisions, employment in June and July combined is 110,000 lower than previously reported.”

And we have The Conference Board’s confidence index at -65. Yikes!

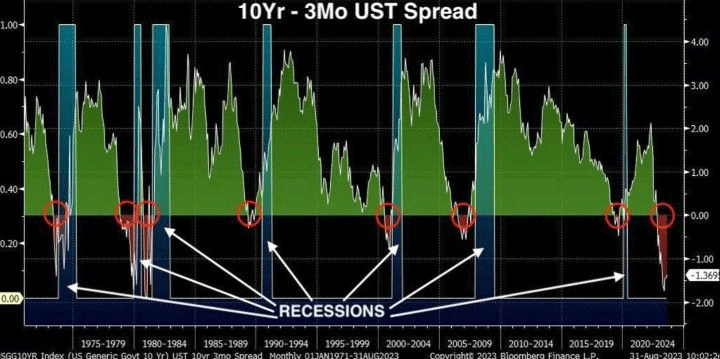

Finally, we have the 10Y-3M UST spread SCREAMING recession!

So, the economy is slowing under Bidenomics and Cadavar Joe.

Will Cadavar Joe actually go out on the campaign trail and debate ANY Democrat or Republican?? Remember, this is the man with the nuclear launch codes.

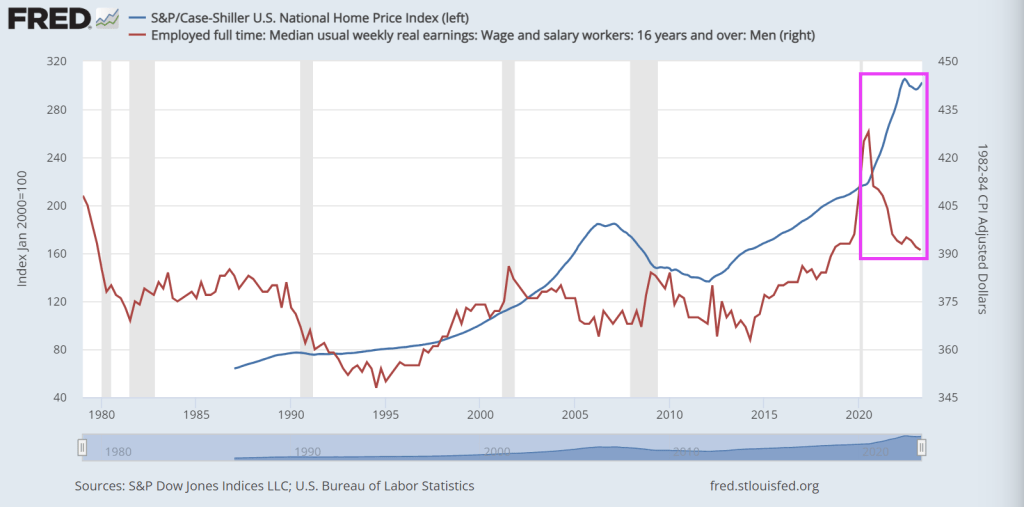

If we look at the Case-Shiller National home price index against real weekly wage growth, you can see the problem clearly. Since Covid and The Fed’s overreaction by providing staggering monetary stimulus, home prices shot up while real median weekly earnings collapsed.

Buying a house requires a much bigger slice of people’s income now — making this the most unaffordable housing market since 1984, by one measure.

And that crushing lack of affordability isn’t expected to improve much in the near future.

At today’s rates, buying a median-priced home would require a monthly principal and interest payment of $2,440 for those making a 20% down payment, according to Black Knight, a mortgage technology and data provider.

That’s $1,172 a month more in mortgage payments from just two years ago, before the Federal Reserve raised its benchmark lending rate 11 times in 18 months, Black Knight found. It’s a 92% increase — and is taking a growing chunk out of household budgets already facing inflation on many fronts.

Currently, 38.6% of the median household income is required to make the monthly payment on the average home purchase, making housing the least affordable it’s been since 1984, according to Black Knight.

“To put today’s affordability levels in perspective, it would take some combination of up to a 28% decline in home prices, a more than 4% reduction in 30-year mortgage rates, or up to a 60% growth in median household incomes to bring home affordability back to its 25-year average,” said Andy Walden, vice president of enterprise research and strategy at Black Knight.

Must as well face it, we’re addicted to gov. Or at least Fed monetary stimulus.

Just look at Personal Interest payments under Bidenomics.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.