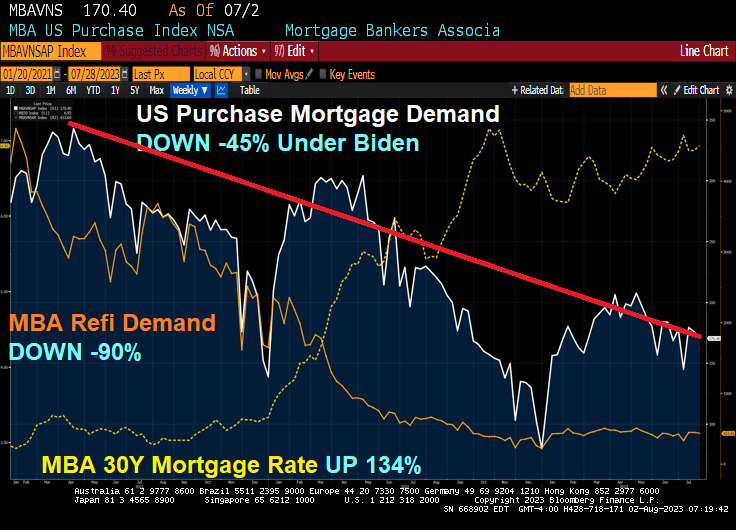

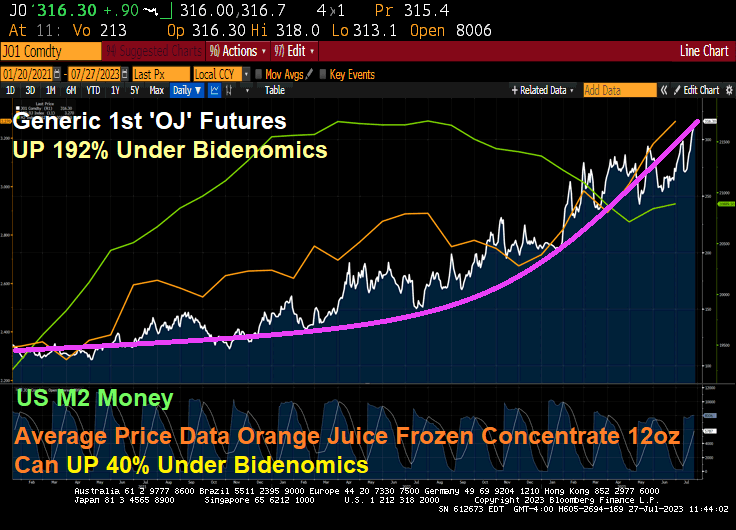

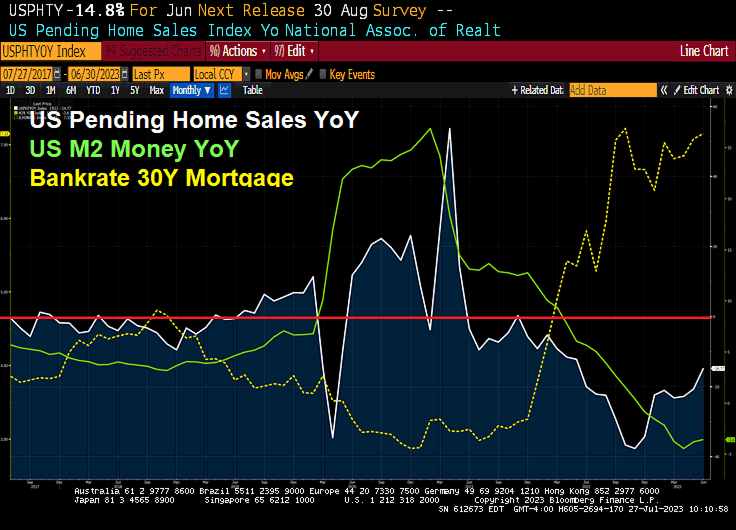

Inflation under Biden has been very painful for the US middle class and low wage workers. That inflation has resulted to surging mortgage rates thanks to The Fed’s counterattack.

The result? Mortgage rates are up 134% under Bidenomics, while mortgage purchase demand is down -45% since Biden was selected. And mortgage refinancing demand is down a staggering -90%!

Mortgage applications decreased 3.0 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending July 28, 2023.

The Market Composite Index, a measure of mortgage loan application volume, decreased 3.0 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 3 percent compared with the previous week. The Refinance Index decreased 3 percent from the previous week and was 32 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 3 percent from one week earlier. The unadjusted Purchase Index decreased 3 percent compared with the previous week and was 26 percent lower than the same week one year ago.

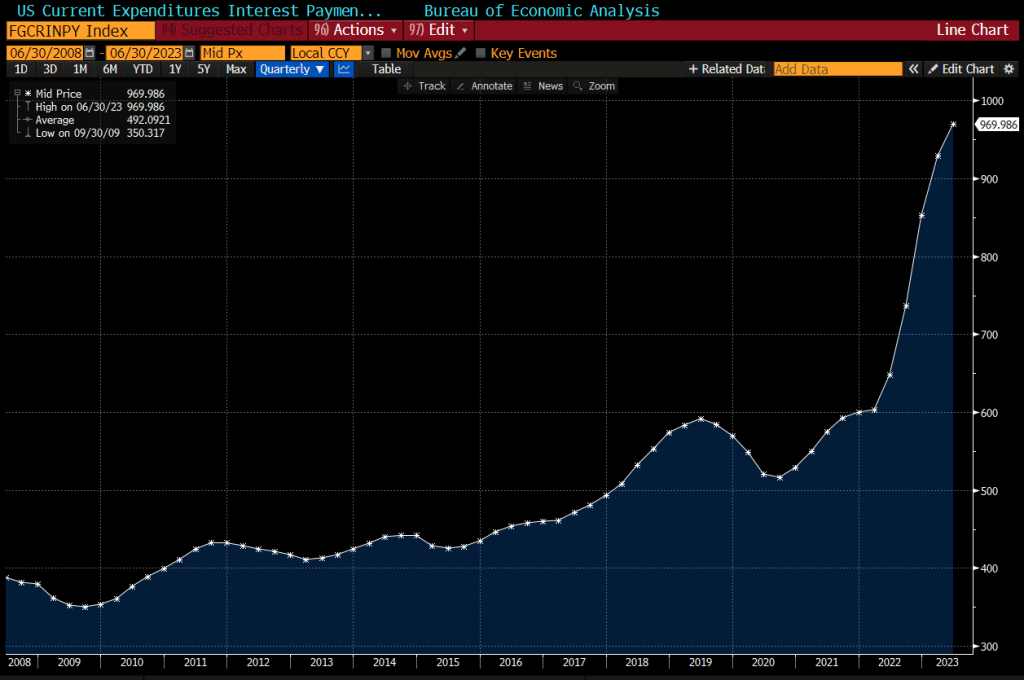

US interest expenses have surged by about 50% in the past year, to nearly $1 trillion on an annualized basis.

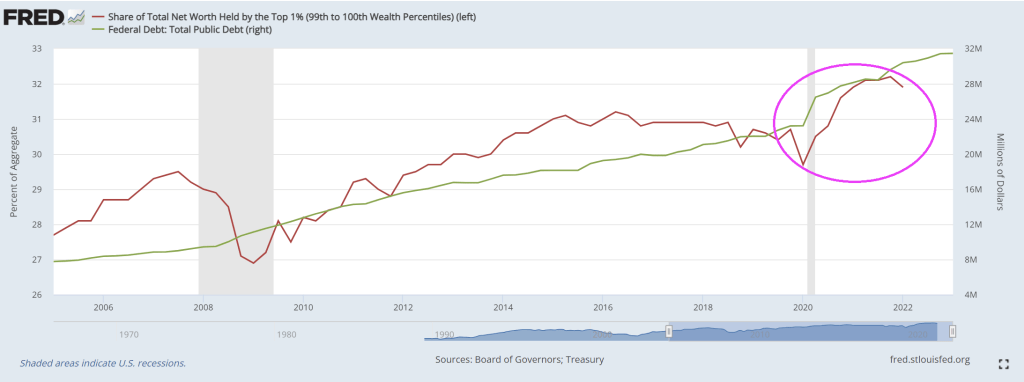

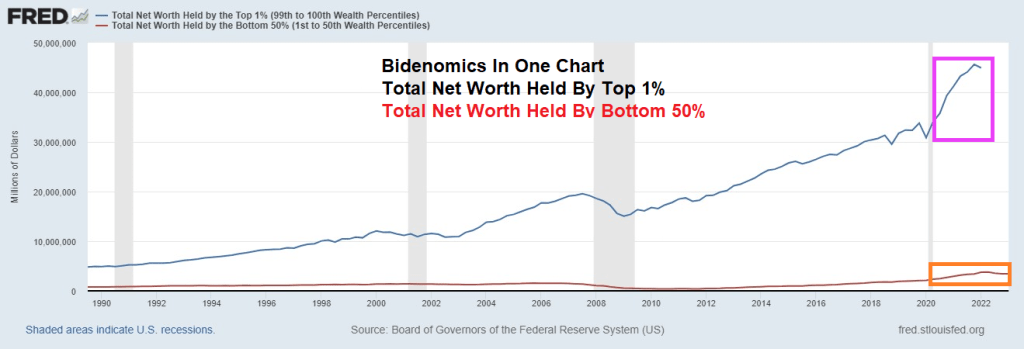

Look at the share of net worth by the top 1% as Treasury borrows more money.

Oddly, Biden is not talking about about putting US government policies up for sale to the highest bidders. But don’t worry. Biden is the King of Corruption in the District of Corruption (Washington DC).

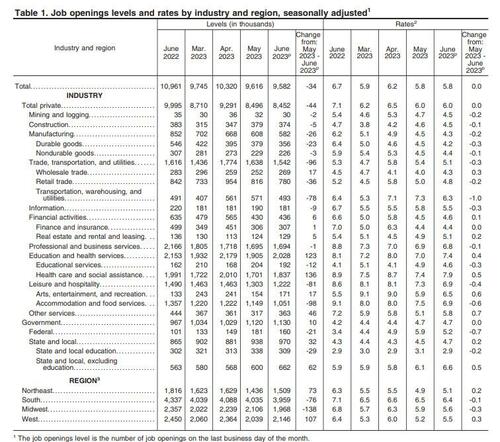

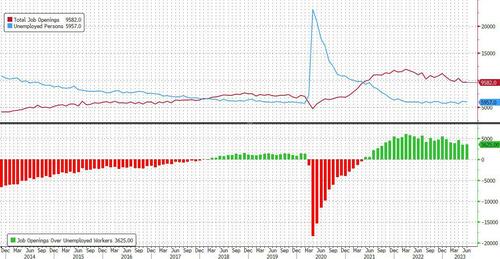

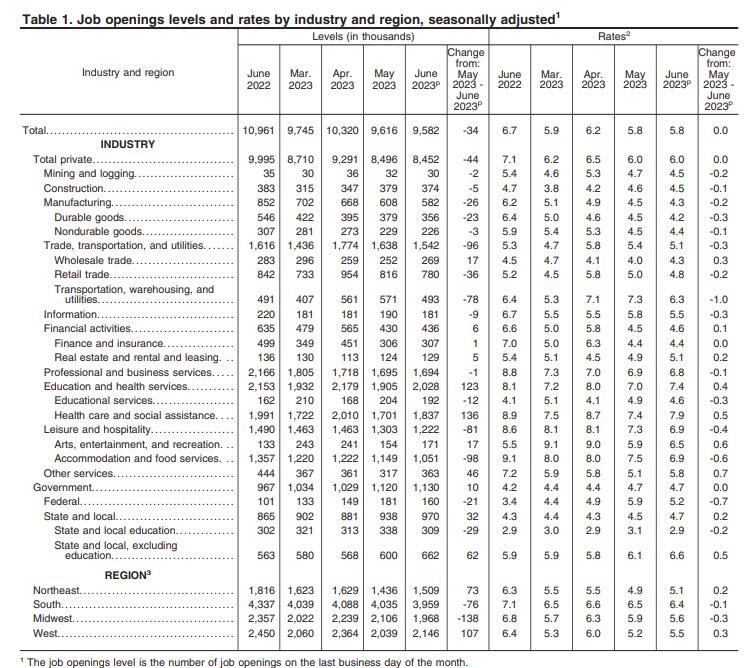

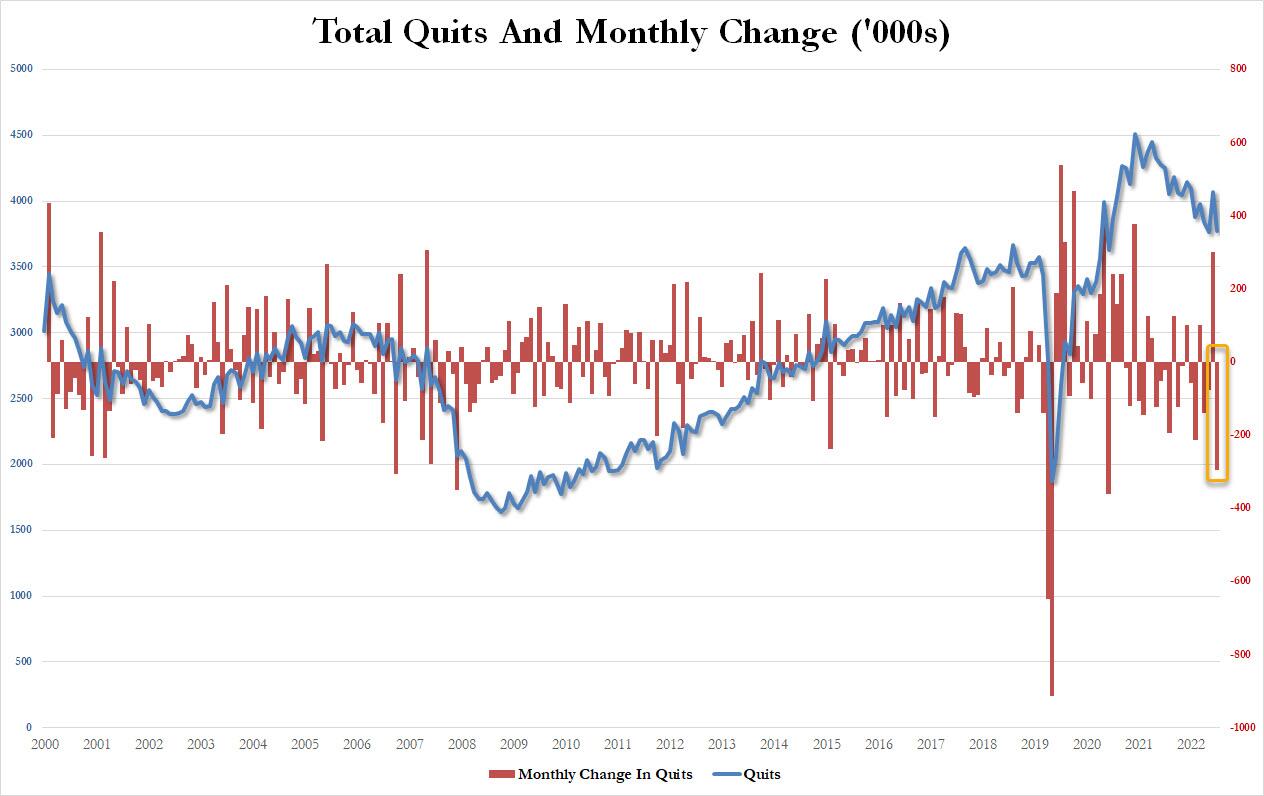

The number was about 1.4 million below the 11 million from a year ago and below the consensus estimate of 9.6 million, a rare miss in a series which has been best known for decisively beating Wall Street’s expectations.

According to the BLS, the largest increases in job openings was in health care and social assistance (+136,000) and in state and local government, excluding education (+62,000). Job openings decreased in transportation, warehousing, and utilities (-78,000), state and local government education (-29,000), and federal government (-21,000)

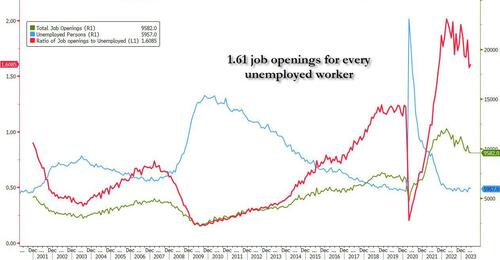

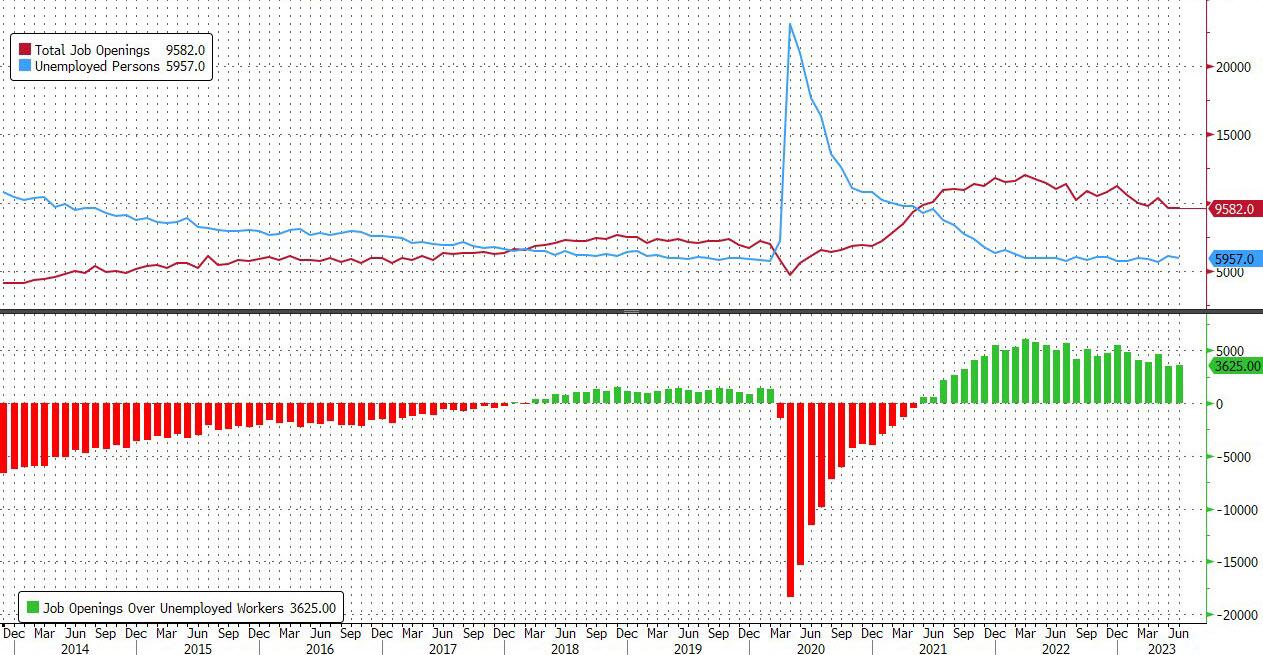

The slide in the number of job openings meant that after rising to the highest since January 2023 in April, in June the number of job openings was just 3.7625 million more than the number of unemployed workers, the lowest since Sept 2021.

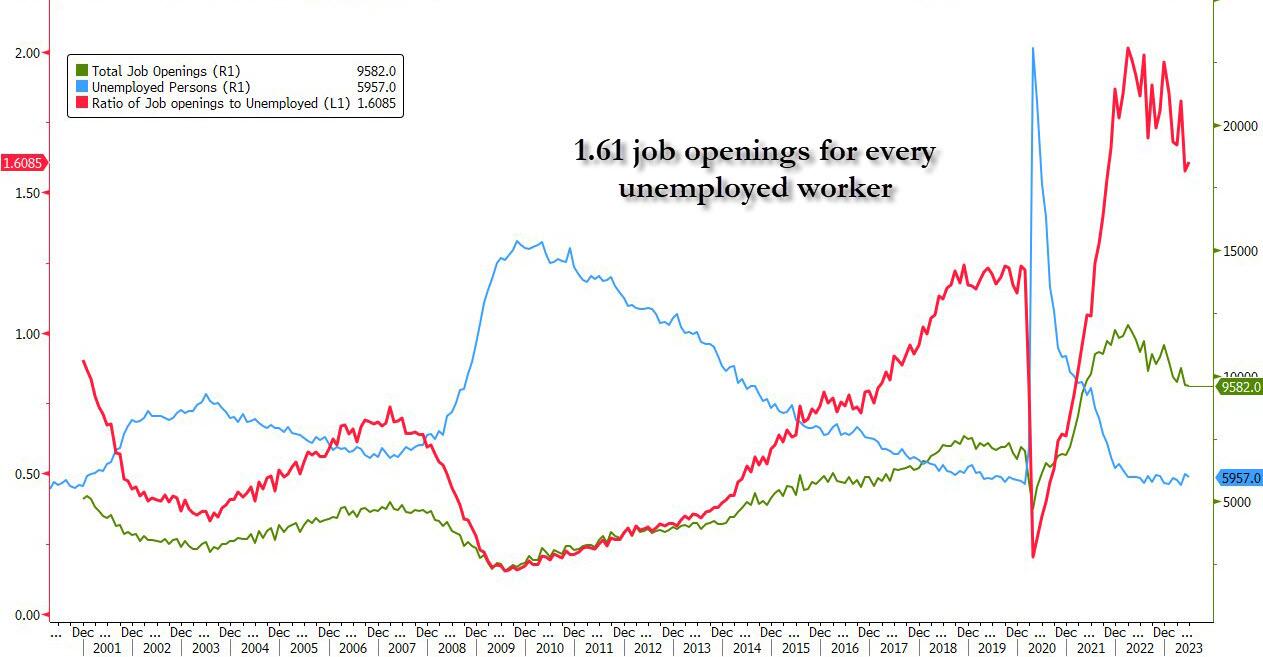

Said otherwise, after rising to 1.82 openings for every worker in April, in June the number dropped to just 1.61, which would have been the lowest level since Oct 2021 if it weren’t for last month’s sharp downward revision.

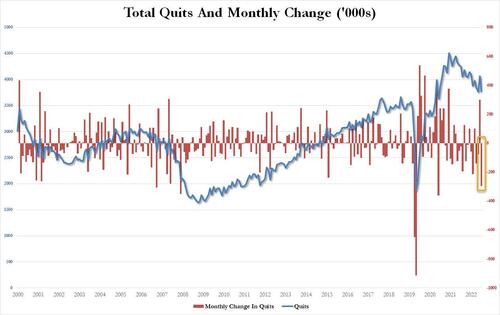

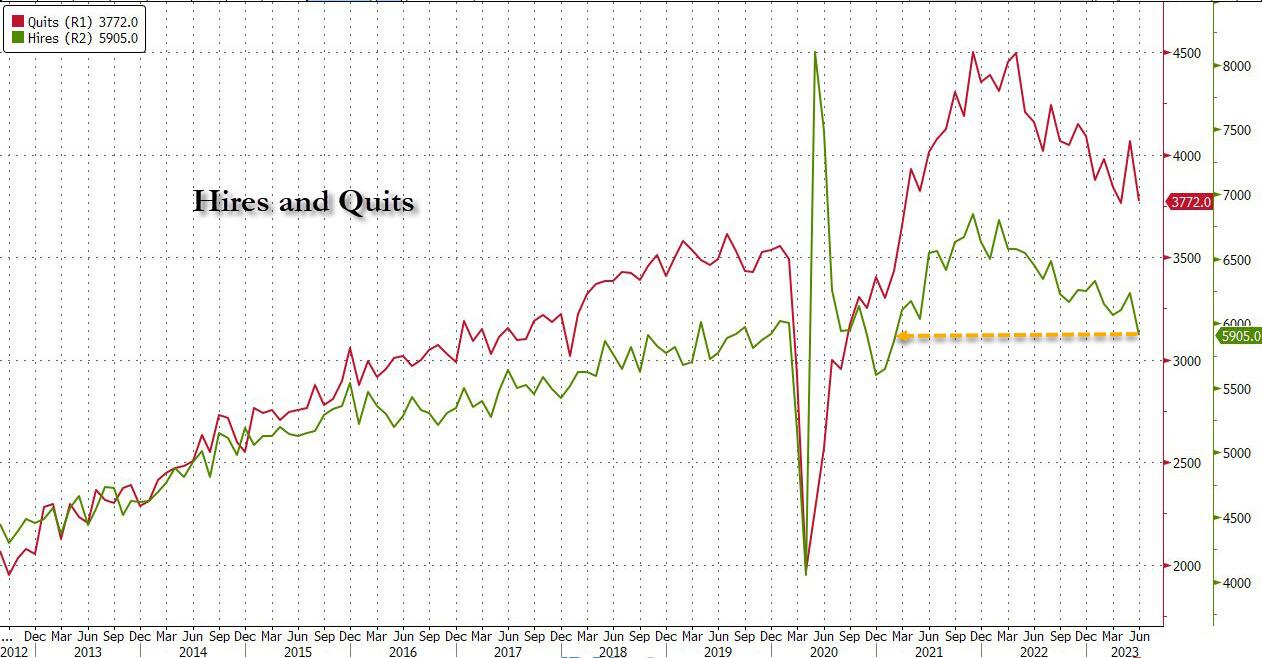

Yet even as the number of job openings dropped only modestly from the (sharply) downward revised print for May (because under Biden, no number is ever revised stronger), conflicting data remained and in June, the number of people quitting their jobs – an indicator traditionally associated with labor market strength as it shows workers are confident they can find a better wage elsewhere – unexpectedly tumbled by 295K to just 3.772MM, the biggest monthly drop since May 2021.

According to the BLS, the number of quits decreased in several industries, with the largest decreases in retail trade (-95,000), health care and social assistance (-75,000), and construction (-51,000). The number of quits increased in arts, entertainment, and recreation (+20,000).

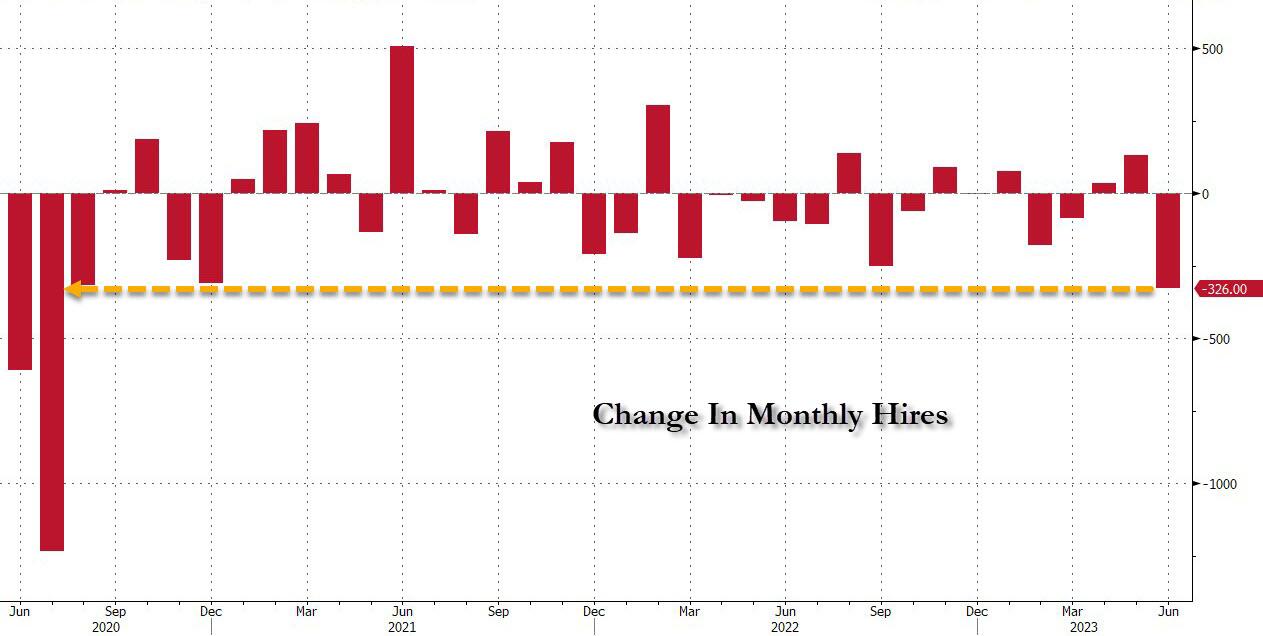

And just in case some still believe Biden’s strong jobs lie, the number of hires also tumbled in June, crashing by 326K – the biggest monthly drop since July 2020…

… to 5.905MM, the lowest since February 2021.

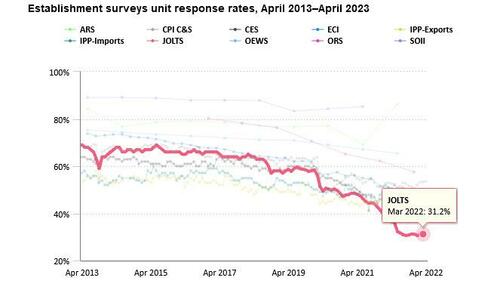

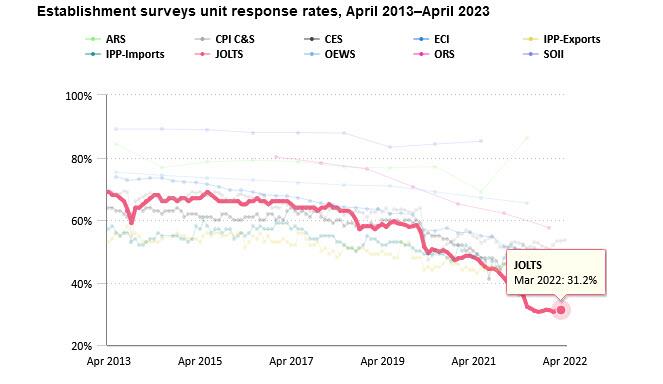

Of course, as we have explained on multiple occasions previously, none of the above data actually matters or is credible for the simple reason that the response rate of the JOLTS survey is stuck at a record low 31.2%. Which means that only those who actually have job openings to report do so, while two-thirds of employers are either non-responsive or their mail is quietly lost in the mail.

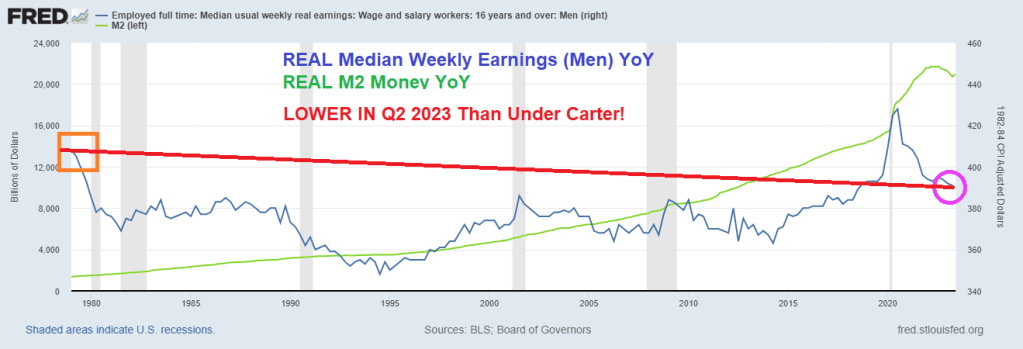

President Jimmy Carter is usually the bar for terrible Presidents. Under Carter, the US experienced economic stagnation and soaring inflation. At least it led to the election of Ronald Regan!

So, Biden’s much mentioned Bidenomics have produced REAL MEDIAN WEEKLY EARNINGS FOR MEN that is currently below 1979 levels under Jimmy Carter.

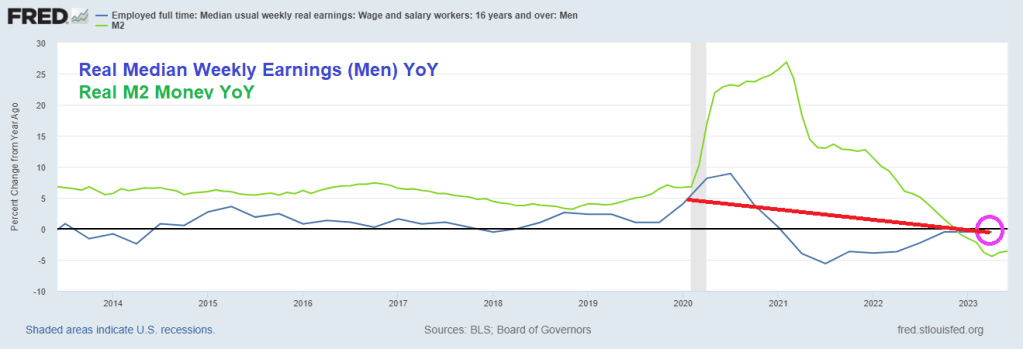

Even worse for Bidenomics, REAL MEDIAN WEEKLY EARNINGS GROWTH FOR MEN was -4.45% In April 2023, while the last reading prior to Covid under Trump was 6.674% YoY in February 2020. So, Bidenomics isn’t even back to Trump levels for men.

I like this chart which I call “Yellenomics” because it illustrates The Fed’s Folly of money printing and its impact on real earnings. After the Trump wage growth boom, real median weekly earnings for men has been steadily declining.

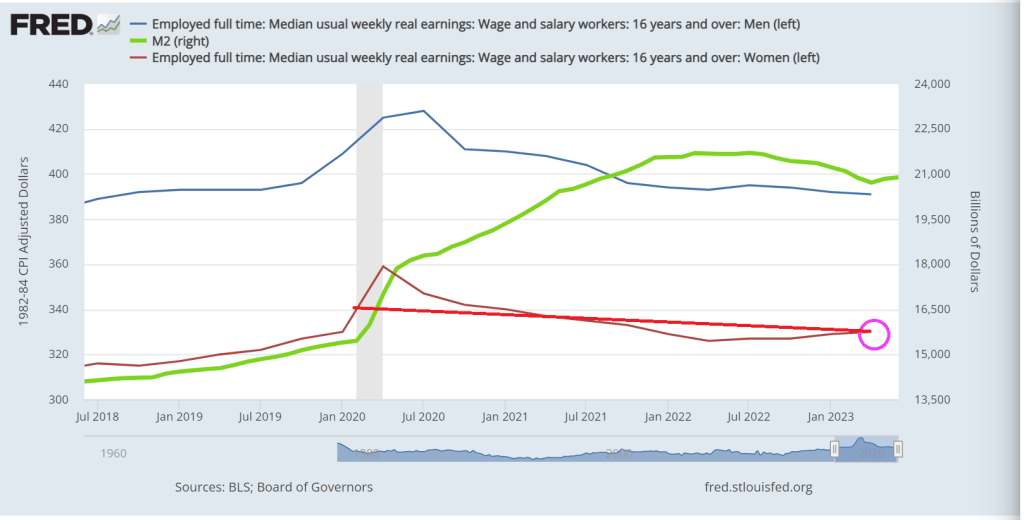

Women, on the other hand, did show a gain since Carter, but still lower than the last month before Covid struck. Women’s real median weekly earnings growth YoY since Q2 2021 are down -5%. So, Bidenomics has been less sucky for women than men.

Reminds me of The Yardbird’s classic “I’m A Man.” Worse off under Biden than under Jimmy Carter. Although The Yardbird’s “Over Under Sideways DOWN” is more emblematic of Bidenomics.

Bidenomics should be renamed Corruptionomics given Biden’s habit of selling government influence to anyone willing to waive a few million.

Bidenomics, aka the Federal government takeover of the US economy with Soviet-style economic central planning, is highly dependent on loose Federal Reserve monetary policy (Janet Yellen and Powell’s wild overreaction to the massively inappropriate Covid shutdowns),

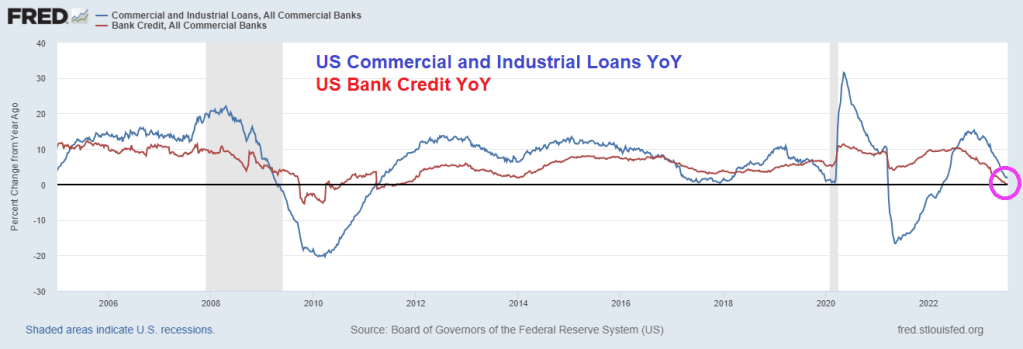

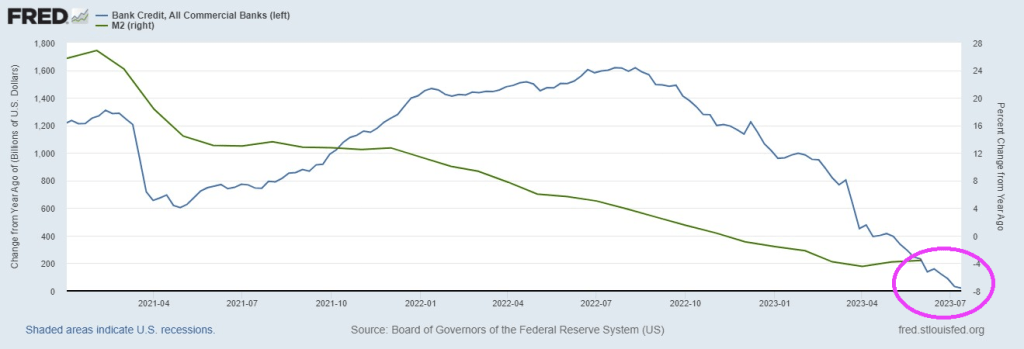

So, how is Bidenomics working out? On the bank lending front, commercial and industrial (C&I) lending growth is crashing along with bank credit growth YoY.

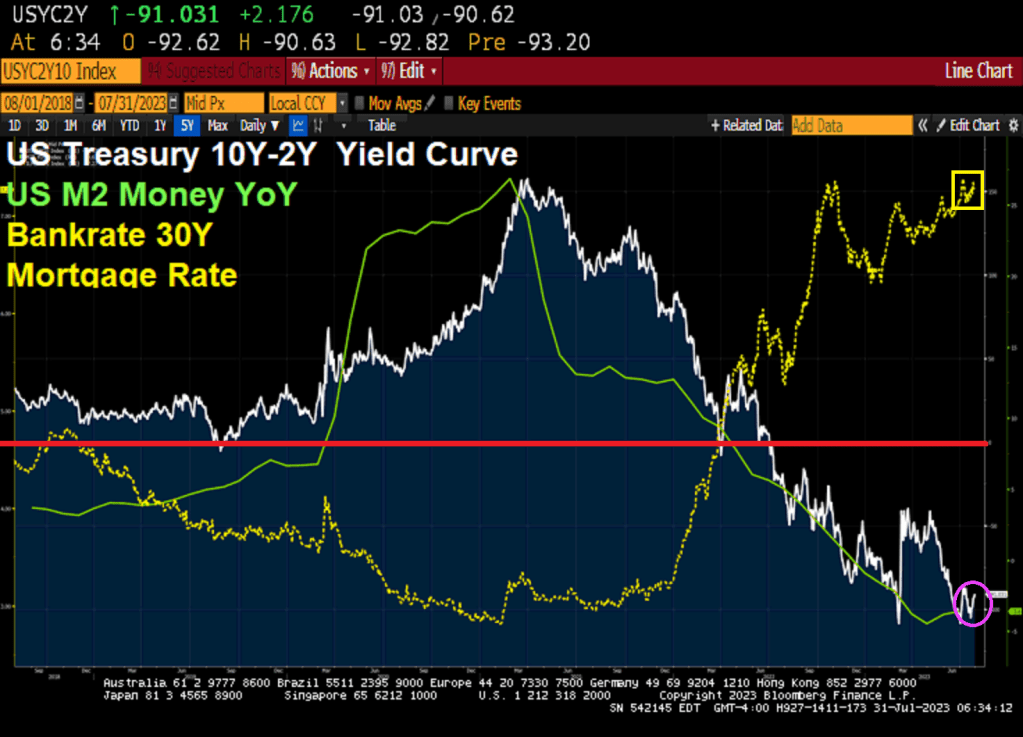

The US Treasury 10Y-2Y yield curve remains deeply inverted at -91.031 basis points and M2 Money growth has crashed. The 30 year mortgage rate is hovering around 7.27%.

The Republicans’ little red book is showing people escaping big crime and tax states like New York and California for lower tax, lower crime states like Florida and Texas. But to Democrats who are really bad at math, 7+7 = 0?

California and New York have sustained population declines during Covid and after, that have long-term implications for local economies. The exodus means workers with six-figure salaries in technology, finance, real estate, and entertainment are going elsewhere, which will reduce tax revenue for the state.

MyEListing.com, an online real estate portal, used IRS migration data to reveal California and New York lost $343 million and $299 million in 2021, respectively, due to the surge in migration outflows.

The beneficiaries of the outflow are Florida and Texas, which took in $12.4 billion and $10.7 billion, respectively.

“Despite its numerous attractions, from the booming tech industry and world-class universities to beautiful landscapes and cultural richness, California’s high personal income tax rates seem discouraging for many high-wealth individuals. This, coupled with the state’s high cost of living, will likely fuel a wealth migration out of California,” MyEListing wrote in the report.

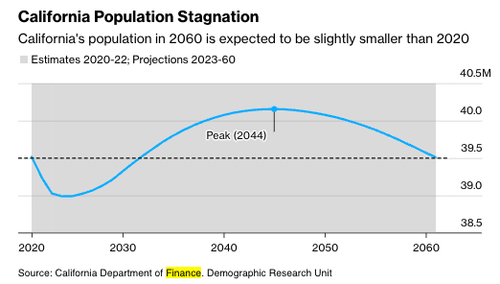

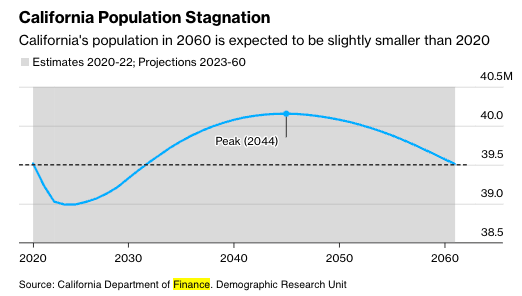

The exodus from California is so severe that state demographers forecasted the total population will be the same today as in 2060.

If left unchecked, the largest outflows of residents from specific metro areas could experience a fiscal crisis. Such a development would be tragic for Democrat-controlled cities already plunging into crisis as progressive politicians fail to enforce law and order.

Joe Biden said that Republicans will impeach him in the House of Representatives since inflation is coming down. Huh? No Joe, it is because your are the most corrupt President in history, a compulsive liar and your economic policies are pure World Economic Forum mandates (open borders, Central Bank Digital currency, green energy, etc). Biden started off his Presidency by declaring war on fossil fuels that helped drive prices through the roof. And the middle class are paying the price.

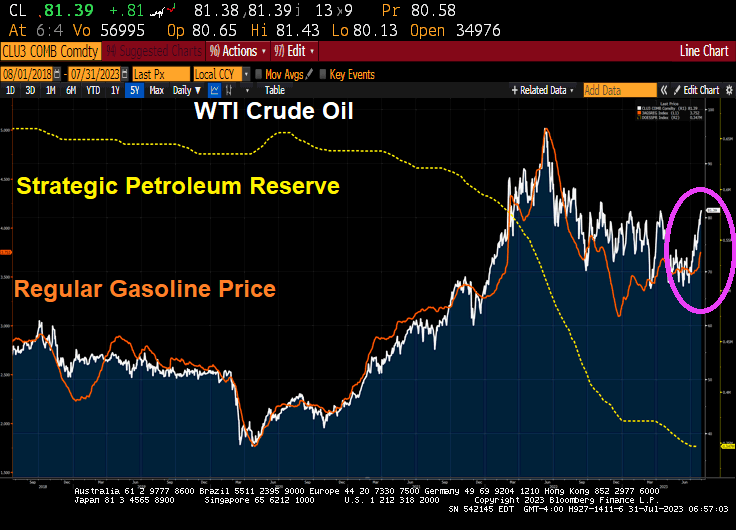

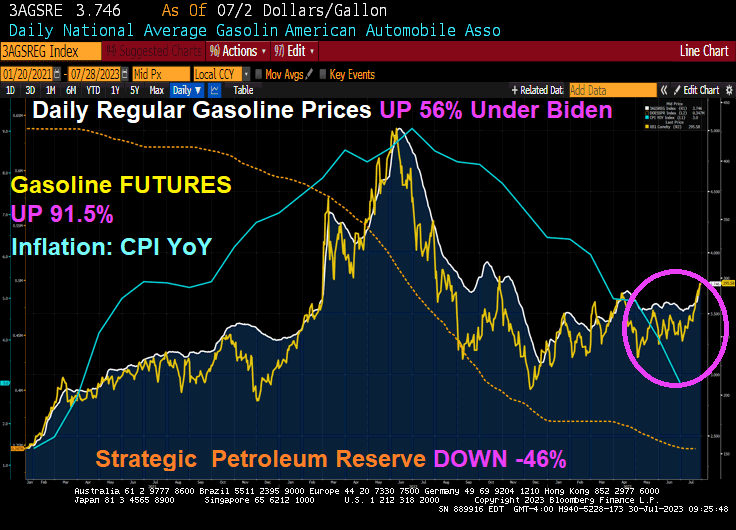

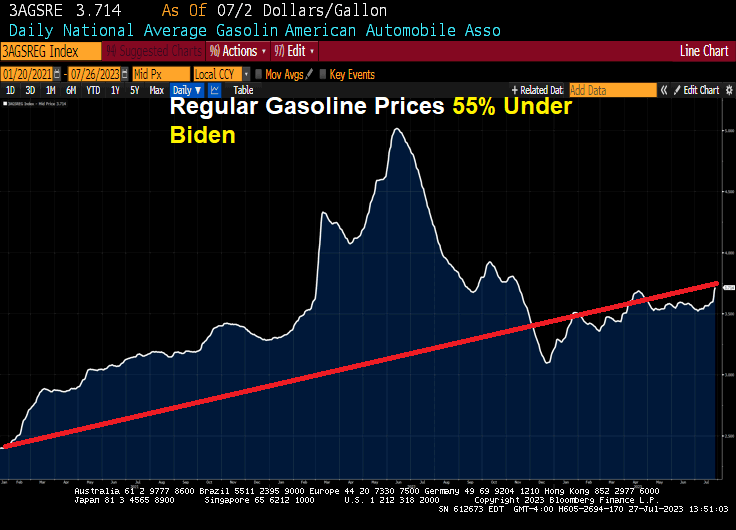

But as inflation cools (blue line) thanks in part to Biden draining the Strategic Petroleum Reserve (orange line), Biden can gloat. But remember, gasoline prices remain 56% higher under Biden’s Reign of Error. Even worse, gasoline FUTURES are up 91.5% under Biden. Yikes!

But look at how gasoline prices and gasoline futures have risen in July (pink circle). The last inflation report showed that inflation has declined to 3% (still higher than The Fed’s 2% target), gasoline prices are up almost 5% since July 19, 2023.

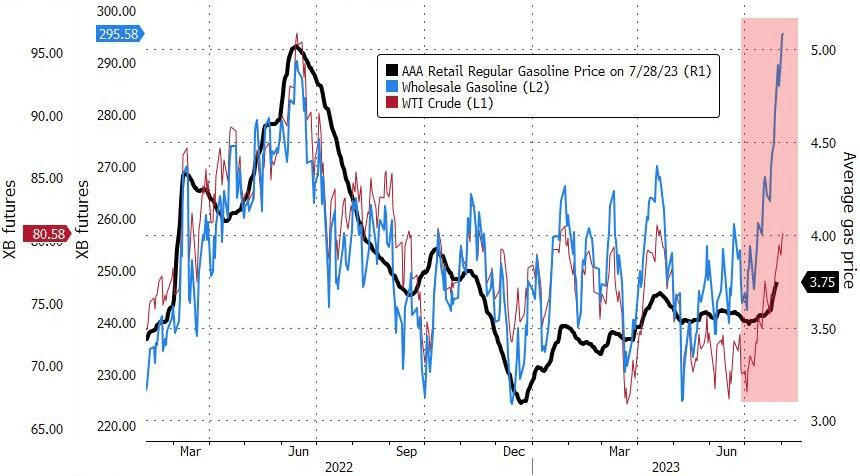

Gasoline, meanwhile, started the year at less than $2.50 per gallon. This week, gasoline topped $2.90 per gallon and may yet reach $3.

WTI Crude Oil futures have broken through the $80 barrier … again. Heating oil futures are up 1.43% today with WTI Crude futures up 0.61%.

So as energy prices keep rising (and Biden’s EPA keeps issuing green energy edicts and fails to recognize that our power grid can’t support all the electric cars and trucks envisioned by the Obama/Biden green dreamers). As such, energy prices will keep rising and with it … inflation.

Commercial real estate (CRE), particularly office space, reminds me of the Arthur Brown tune “Fire!” except that Jerome Powell of The Federal Reserve is the God of Hellfire! While fighting inflation caused by … The Federal Reserve and insane Federal spending (aka, Bidenomics). Call this the Over, Under, Sideways Down economy. The top 1% are doing quite well, while the lower 50% of net worth households are struggling.

The Q1 2023 NCREIF Office property (value) index shows declining office value since Q2 2022 as The Fed began raising its target rate to combat inflation.

From Trepp, we have this shocking table showing the decline the average total value loss over the span of around a decade. The oldest buildings experienced the largest reduction in value of 60%, and the newest experienced the least (but quite substantial) reduction of 52%. Although the newest buildings performed the best relatively, their 52% value reduction is easily the most concerning, and displays truly how much distress is present in the office sector. This group has the highest percentage of Class A buildings, but its reduction value over the past decade is still approximately on par with buildings constructed over half a century prior. With north of $150 billion in securitized maturities beyond 2023, these trends set a gloomy tone for their future and the performance of office properties as a whole.

Then we have this alarming headline from Trepp: “Commercial Mortgage Sector Faces Another Wall of Maturities as $2.75 Trillion Rolls by 2027.” An estimated $528.7 billion of commercial mortgages mature this year, according to Trepp data, which projects that next year, maturities will increase to $532.8 billion. The projections are based on data for the first quarter compiled using the Federal Reserve’s flow of funds and made various assumptions regarding loan terms for each of the major lender categories. The data would indicate that the market is facing a wall, if not a mountain of maturities that would make the 2015-2017 wall of maturities look almost inconsequential. During that period, roughly $1.1 trillion of loans were scheduled to come due. But attention was focused on the CMBS market, as more than $335 billion of loans were set to mature during the period.

Well, REAL gross domestic income fell -0.8% YoY in Q1 2023 as M2 Money growth crashes. Not a good sign for the US economy or commercial real estate.

Of course, office properties are suffering from almost out-of-control crime in major American cities and the desire of workers to work from home rather than commute to work in cubicles.

But never fear! We have massively corrupt and compulsive liar Joe Biden as President!! He is the President of The 1%! Not the other 99%.

Bidenomics, massive spending on green energy mandates while curbing fossil fuel consumption, has been a true wonder for the top 1% of net worth (let’s call them The Elites). And Bidenomics, like Obamanomics, relied on super generous Federal Reserve money printing.

The result? Total Net Worth held by the top 1% has grown rapidly since the Covid outbreak and Fed monetary expansion (plus Congress going wild spending). The bottom 50%? They improved in terms of net worth

So, The Elites (top 1%) want The Fed to keep on printing money, since their net worth soars.

Meanwhile, US bank credit is crashing as The Fed slows M2 Money growth.

Not only is credit growth grinding to a halt, but unrealized losses on bank investment securities continues to worsen.

If you didn’t see this, then check out House testimony of extraterrestrial visitations to Earth. This has been happening since the 1950s (allegedly), so why NOW is there sudden interest in aliens? Deflection away from the horrible scandal of Biden taking money from foreign actors? Likely answer? Biden and Mayorkas will send Treasury Secretary Janet Yellen to negotiate with alien invaders giving them anmesty, free school, free food, free healthcare and directions on how to register to vote. And giving aliens preferential trade status. All for “10% for The Big Guy!”

The Biden Administration is gushing about Q2’s Real GDP report of 2.4% QoQ. Wow, after trillions of dollars of stimulus spending and The Fed going wild with monetary stimulus, all we got was 2.4% growth??

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.