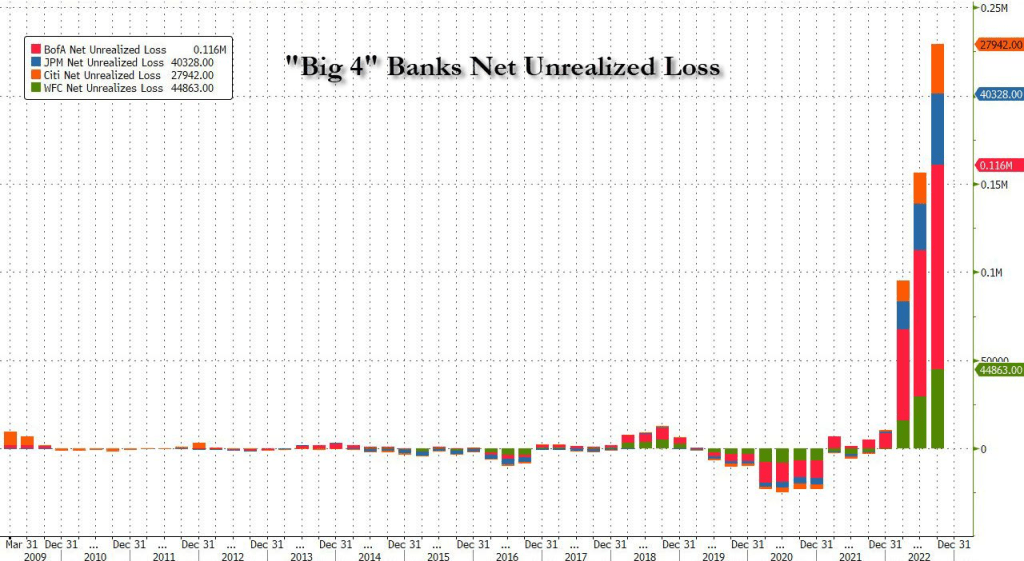

Despite cries from Summers, Yellen and other the DC illuminati (Biden is oddly silent), US banks are NOT fine. In fact, banks in general are suffering from Fed rates increases due to holding of long-term Treasuries and MBS.

In fact, The Federal Reserve’s fight against inflation is causing serious problems, as exemplified by AOC. No, not THAT AOC. but bank Accumulated Other Comprehensive Income.

Accumulated Other Comprehensive Income (AOCI) are special gains and losses that are listed as special items in the shareholder equity section of a company’s balance sheet. The AOCI account is the designated space for unrealized profits or losses on items that are placed in the other comprehensive income category.

On the regulatory call reports, AOCI is added to regulatory capital. Since SVB’s AOCI was negative (because of its unrealized losses on AFS securities) as of Dec. 31, it lowered the company’s total equity capital. So a fair way to gauge the negative AOCI to the bank’s total equity capital would be to divide the negative AOCI by total equity capital less AOCI — effectively adding the unrealized losses back to total equity capital for the calculation.

Getting back to our list of 10 banks that raised similar red margin flags to those of SVB, here’s the same group, in the same order, showing negative AOCI as a percentage of total equity capital as of Dec. 31. We have added SVB to the bottom of the list. The data was provided by FactSet:

Or this chart of vulnerable banks from Morningstar of unrealized losses and liquidity risk.

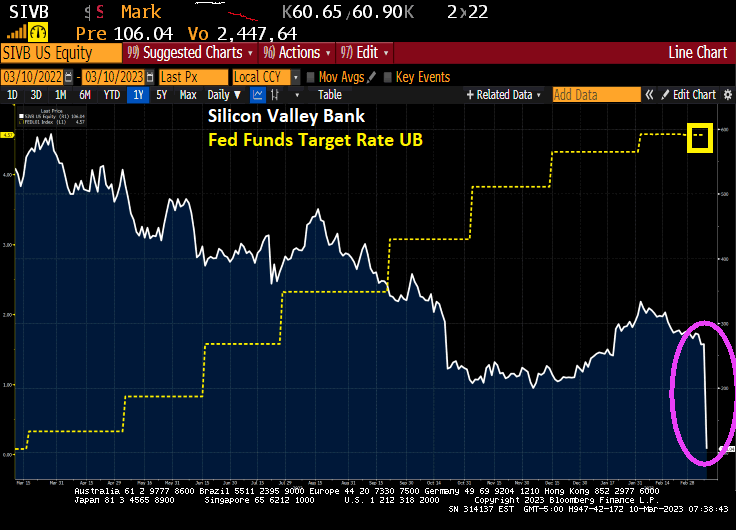

Here is a snapshot of SVB’s balance sheet. Or UNbalanced sheet.

After Congress passed the greatly flawed Dodd-Frank banking legislation, bailouts of banks are prohibited. But bank BAIL-INs still exist. Banks use money from their unsecured creditors, including depositors and bondholders, to restructure their capital to stay afloat. Put simply, they can convert their debt into equity to increase their capital requirements. Although depositors run the risk of losing some of their deposits, banks can only use deposits in excess of the $250,000 protection provided by the Federal Deposit Insurance Corporation (FDIC).

In any case, the FDIC and Fed are weighing a special vehicle after SVB swiftly collapses. Special vehicle? Sounds an awful like the mega bank bailout of 2008 under Hank Paulson.

No, not THIS AOC!

You must be logged in to post a comment.