Three regional Fed reports I like to watch are New York’s Empire State Outlook, Philly Fed’s Outlook and Richmond Fed’s outlook. Today, The Richmond Fed released their manufacturing outlook and … it declined to -11.

So the big three are all down (Philly down to -8.9 while NY’s Empire State outlook is down to -32.9.

On the Treasury front, the US 10Y-3M yield curve inverted further (a signal of impending recession) just tanked to -126.462 basis points.

The Conference Board’s Leading Indicator should be called The Bleeding Indicator given that the leading index has declined to 10 straight months. This is happening as The Fed tightens monetary policy to combat inflation.

Leading indicators include economic variables that tend to move before changes in the overall economy. These indicators give a sense of the future state of an economy.

First, US default risk as measured by credit default swaps remains elevated (primarily because Biden and Democrats refused to cut wasteful spending or reign in non-retirees on Social Security). And NY Fed’s Reverse Repos remain elevated.

And then we have Citi’s economic surprise index for the US at -17 as The Fed slows money growth to 0%.

I wish I knew a place where inflation and insane Federal government spending and policies doesn’t exist.

The Thrill Is Gone from the US housing market as M2 Money growth fells to 0%.

US Existing Home Sales fell -1.5% from November to December (MoM) to 4.02 SAAR units sold. That translates to a depressing -34% decline since December 2021 (YoY).

On the positive side, these numbers are better than expected (-3.4% MoM expected). Still, these numbers are pretty dismal.

Existing home sales MEDIAN PRICE fell to $366.9k as M2 Money growth vanishes. And inventory of existing homes for sale remains lower than pre-Covid levels.

Let’s see what Powell and the Gang (aka, The Federal Reserve Board of Governors) does with interest rates going forward.

Today, the 10-year Treasury yield is up 7.1 basis points, but the real action is in Europe where sovereign yields are up 11.5 bps in France, 9.8 bps in Germany and 18.6 bps in Italy.

December’s housing construction numbers are a mixed bag. On the one hand, US housing starts are down -1.36% from November to December, but down -21,8% since December 2021 (YoY).

The good news? 1-unit (single family detatched) rose 11.26% from November to December (MoM). But 5+ (multifamily) starts are down -18.91% MoM.

But 5+ unit PERMITS are up 7.14%. Perhaps Hunter Biden can now rent an apartment rather than pay his father $50,000 a month in rent for Joe’s Wilmington Delaware house.

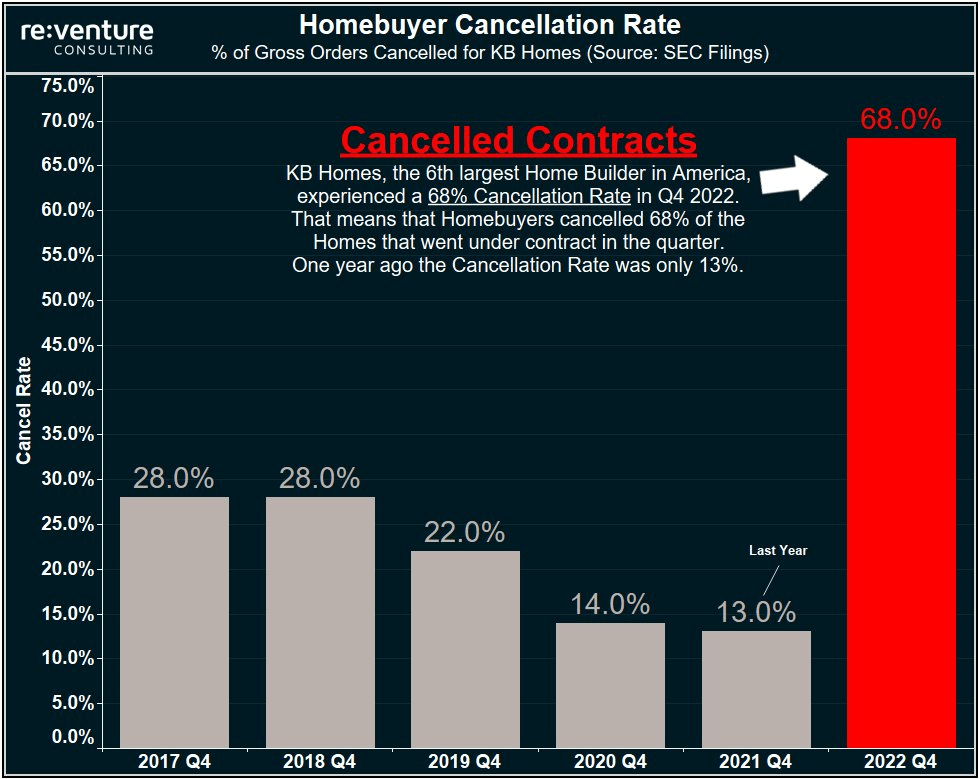

KB Homes experienced a 68% cancellation rate in Q4 2022.

This version of The Scream is one of four made by Edvard Munch, and the only one outside Norway. It is coming up for auction at Sotheby’s in New York.

Mortgage applications increased 27.9 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending January 13, 2023. But mortgage applications are 60% lower than the same week last year.

The Refinance Index increased 34 percent from the previous week and was 81 percent lower than the same week one year ago. The seasonally adjusted Purchase Index increased 25 percent from one week earlier. The unadjusted Purchase Index increased 32 percent compared with the previous week and was 35 percent lower than the same week one year ago.

Here are the stats.

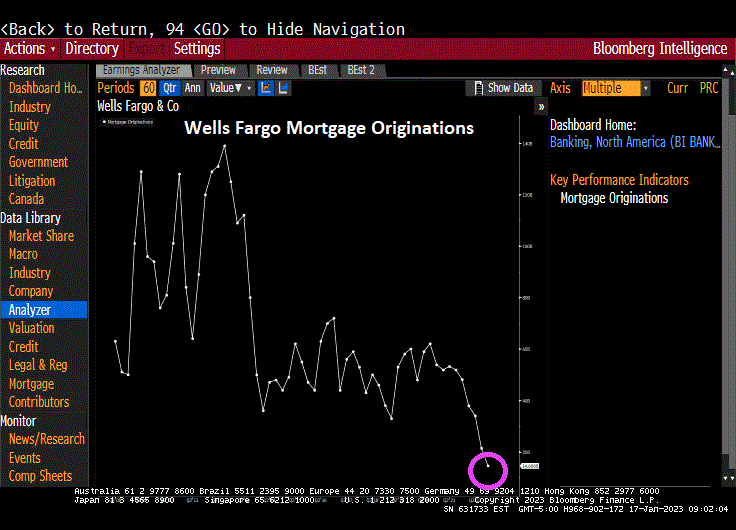

One lender in particular, Wells Fargo, smells blood in the economic waters, and has cut back mortgage originations.

Just remember, mortgage applications generally rise in the first part of the year until May, then start slowing until the last week of the year. This is called seasonality. But despite the fast growth this year, purchase applications are still down -35% compared to last year at this time.

Its that time again when Congress does its Kabuki Theater drama about raising the US debt limit. Of course, everyone in Congress and the Biden Administration want to spend trillions of dollars so they will hike the debt limit.

With the US government facing the danger of a payments default later this year, Congress has a variety of paths to avert economic disaster and boost the debt ceiling.

All of them would likely involve going right up to the market-rattling brink, according to current and former lawmakers and aides.

The timeline kicks off within weeks, when Treasury Secretary Janet Yellen is expected to advise that the government will deploy extraordinary accounting measures to avoid running out of cash. Those steps are forecast to be exhausted after July.

Republicans now in control of the House are demanding deep spending cuts as the price for an increase in the ceiling, while President Joe Biden and congressional Democrats reject such an outcome.

Nothing has been the same since the financial crisis of 2008 and the ascension of all-time big spender Nancy Pelosi as House Speaker. Budget deficits have never been the same. The last budget surplus was under House Speaker Newt Gingrich. But since the financial crisis of 2008, Federal spending seems to have increased its trajectory.

Note that mandatory spending (Medicare, Social Security, etc) is growing like a wild fire while discretionary spending is seemingly flat. So, it mandatory spending that Congress will pretend to cut.

Yes, it is Medicare for our aging population that has blown out of control.

Then we have defense spending. The Ukraine spending should come from this pot, but forces decisions to make between Ukraine and taking care of our Navy (to compete with the growing Chinese navy).

Of course, as The Fed fights inflation, we are seeing the COST of Federal debt soaring since Covid.

Yes, Congress NEEDS to cut back the spending, particularly on Social Security and Medicare (not to mention Ukraine spending), but it is all Kabuki theater. Queue the screams of “Republicans will take away …”.

I wish everyone in Congress were like Kentucky U.S. Senator Rand Paul, not the other spendaholic Kentucky Senator.

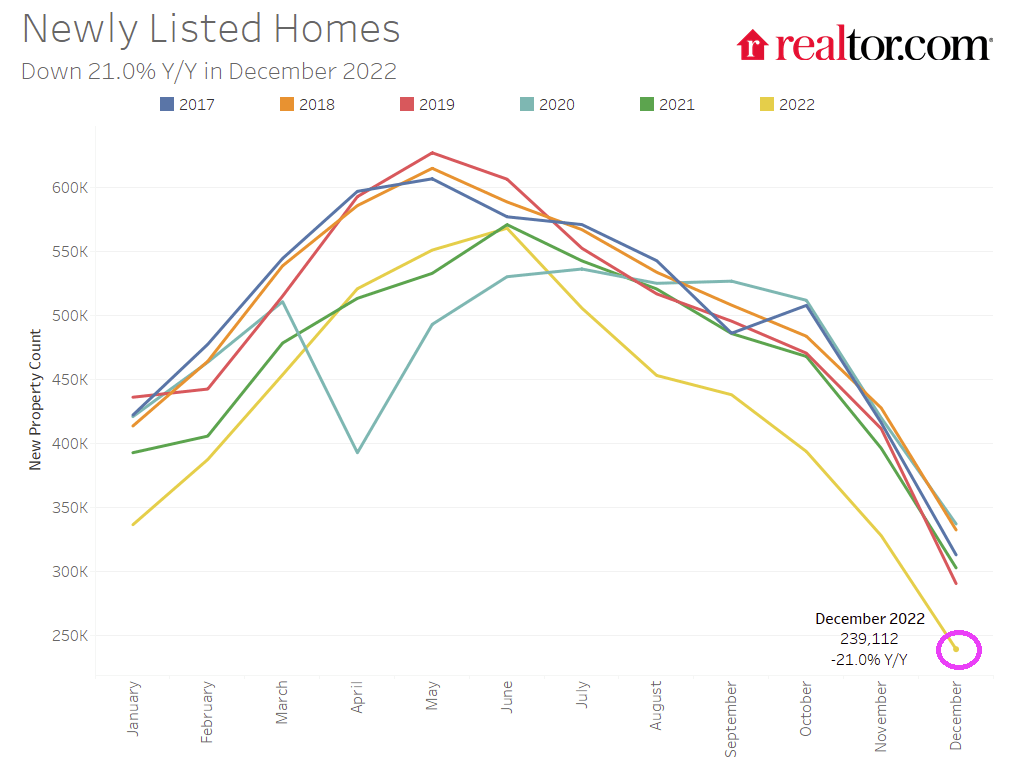

As The Federal Reserves attempts to combat inflation, the withdrawal of monetary stimulus is creating problems in the housing market. For one, as mortgage rates have risen, newly listed homes declined -21% YoY in December.

And yes, the 2022 vintage is the worst in 6 years as The Fed counterattacks inflation. And mortgage rates rose to over 7% before calming down to around 6.50%.

It is the start of a new year and, like clockwork, residential mortgage applications are rising (at least until May). But it is important to realize that purchase mortgage demand is down 44% from the same week last year (YoY). And refinancing mortgage applications are down 86% YoY.

Mortgage applications increased 1.2 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending January 6, 2023.

The Refinance Index increased 5 percent from the previous week and was 86 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 1 percent from one week earlier. The unadjusted Purchase Index increased 47 percent compared with the previous week and was 44 percent lower than the same week one year ago.

You can see the beginning of the new year in pink outline, purchase apps up 47% since the previous week (WoW). But you can see the general decline in both purchases and refinancing applications YoY as M2 Money growth stalls.

Talk about seasonality! If you want to feel optimistic about the mortgage market, just look at the first week of 2023. Declining mortgage rates are helping fuel short-term mortgage demand.

The Federal Reserve will be the backstop of the Treasury market this year to alleviate dysfunction resulting from its increasing size and the retreat of regular buyers.

That’s the view of Credit Suisse Group AG analyst Zoltan Pozsar, who in a note to clients Friday predicted the Fed will restart asset purchases during the summer of 2023.

In Pozsar’s analysis, relative-value funds won’t buy Treasuries unless they cheapen a lot relative to overnight index swaps, and banks with sagging reserves are more likely to tap the funding markets than to buy Treasuries. FX-hedged buyers have been “priced out,” and geopolitical events have reduced large reserve managers’ appetite for US debt, he said.

Flagging demand from marginal buyers will depress demand for Treasury auctions, sparking selloffs in equities, credit and emerging markets, according to Pozsar.

“This is a ‘checkmate-like’ situation,” he wrote. “The Fed won’t be a pivot and the terminal rate may have to go higher still, neither of which augurs well for either risk assets or Treasuries.”

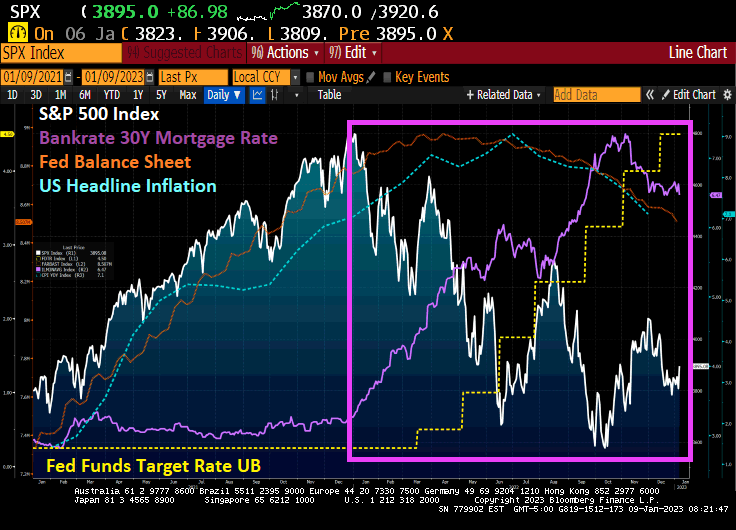

As The Fed started to raise rates (yellow line) to fight inflation (blue dashed line), the S&P 500 index started to fall. Note that The Fed’s balance sheet (purple line) is mirroring the inflation rate.

Fed Funds Futures point to Zoltan’s reversal in June 2023.

Will The Fed pivot? Zoltan says yes, the talking Fed heads say no.

You must be logged in to post a comment.