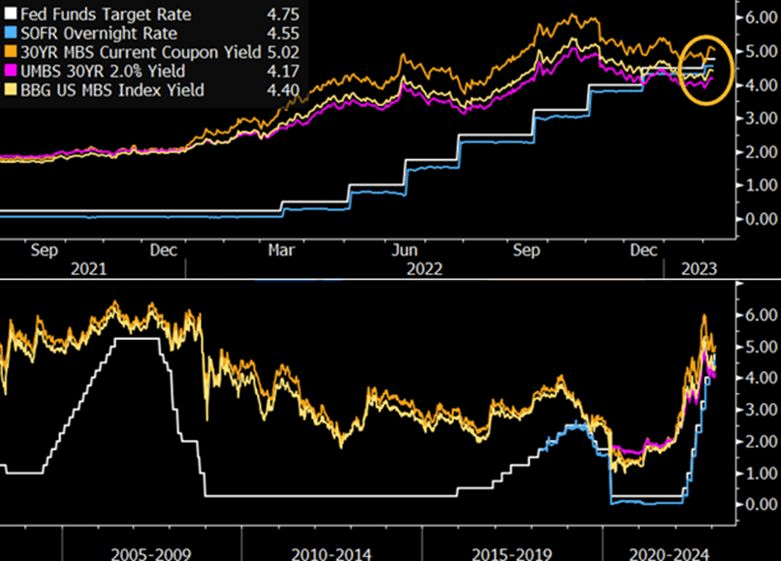

The most recent tightening by the Federal Reserve has pushed the federal funds target rate above mortgage-backed securities yields for the first time in history. Though this poses clear challenges of carry for MBS holders, selective investments in specified pool and collateralized mortgage obligations (CMOs) could provide incremental returns.

While Biden brags (redundant) about lowering inflation (that his energy policies and massive Federal spending caused), apparently he never learns. Now we learn from Mish that the Biden Administration is ready to unleash a $27 billion green slush fund on the US middle class.

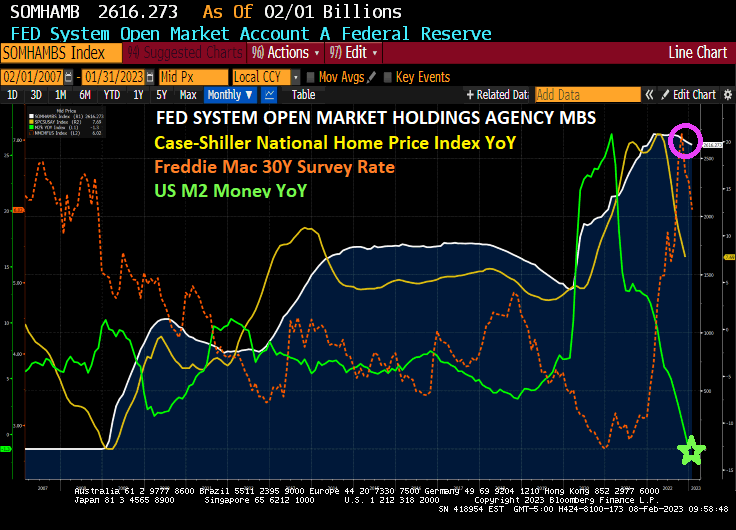

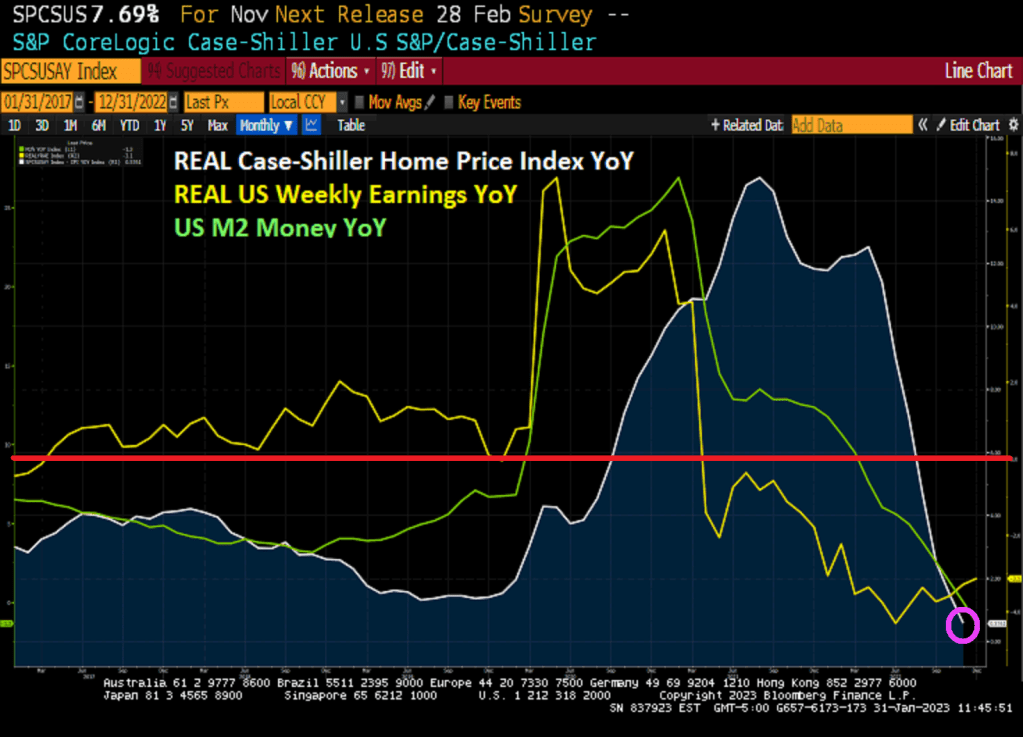

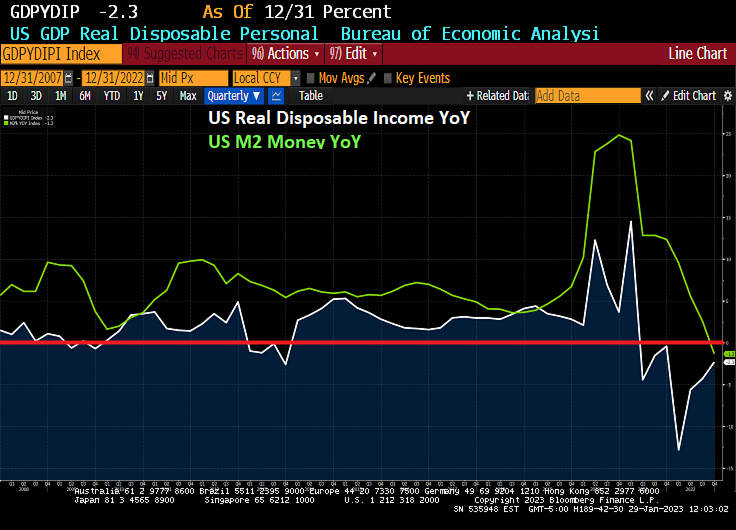

Inflation started under Biden, but the massive expansion in money supply (M2) begin with Covid in 2020.

Once this latest spending splurge kicks in, we will see rising inflation again. After all, Biden and Congress have gotten the taste for massive spending bills (like vampires) and spending likely won’t slow down.

You must be logged in to post a comment.