Biden’s leading “economist” Lael Brainard loves to brag about the strong economy under Bidenomics, and then pulled a brain freeze when asked about crashing savings rates as consumers struggle with inflation.

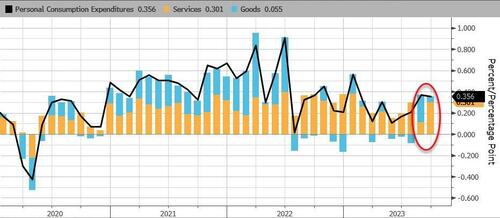

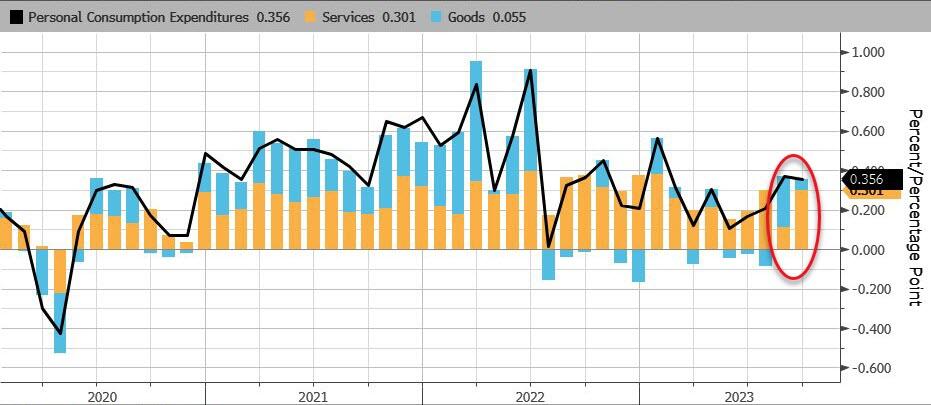

The good news? One of The Fed’s favorite inflation indicators – Core PCE Deflator – slowed to 3.7% YoY in September (its lowest since May 2021). Headline PCE was flat at 3.4% YoY. Both were in line with expectations… But 3.4% is still far too high compared to The Fed’s target of 2%.

Source: Bloomberg

Now for the bad news. However, while the YoY data slowed, Core PCE rose by 0.3% MoM – the biggest MoM jump in four months.

Services inflation excluding housing and energy accelerated to 0.4%, from 0.1% in the prior month.

The overall PCE price index, meanwhile, rose 0.4%, bolstered by higher energy prices.

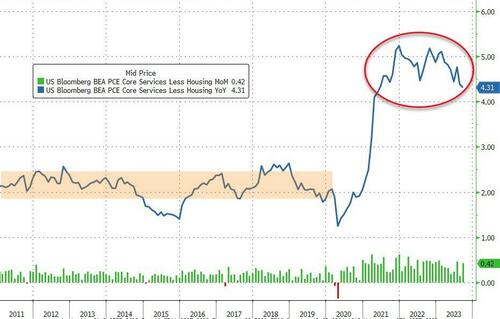

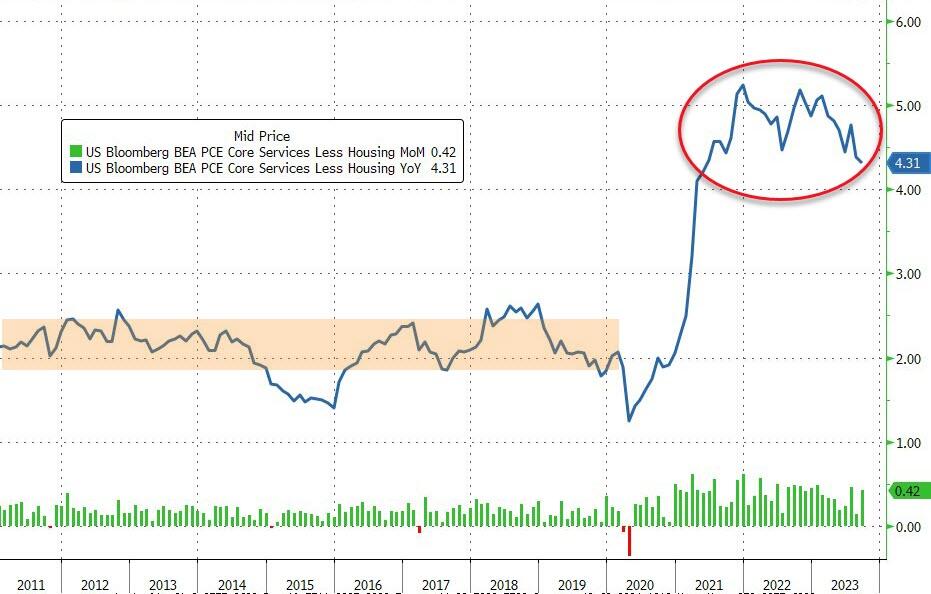

Even more focused, is the Fed’s view on Services inflation ex-Shelter, and the PCE-equivalent shows that it is slowing/trending lower but very much still stuck at high levels (and rose a large 0.4% MoM)…

Personal Consumption soared 0.7% MoM while incomes grew at only 0.3% MoM…

Source: Bloomberg

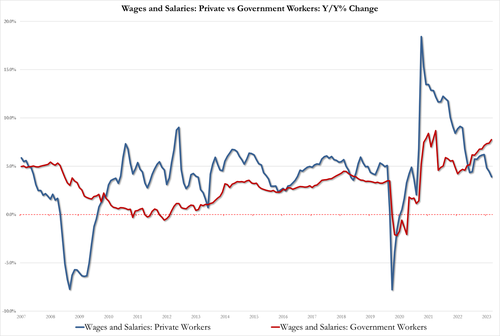

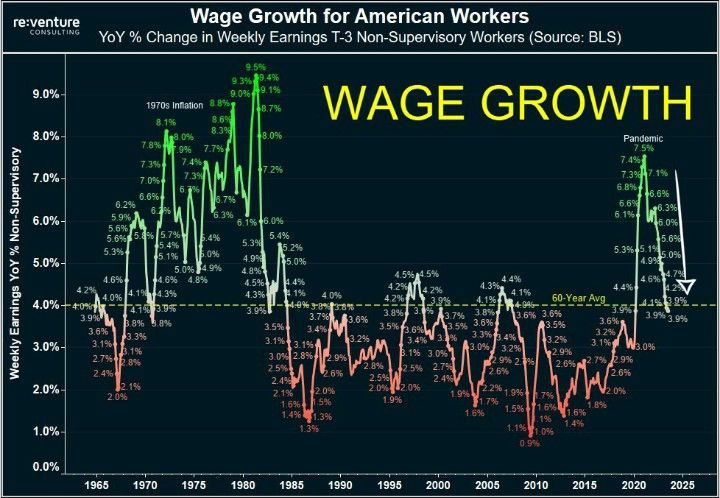

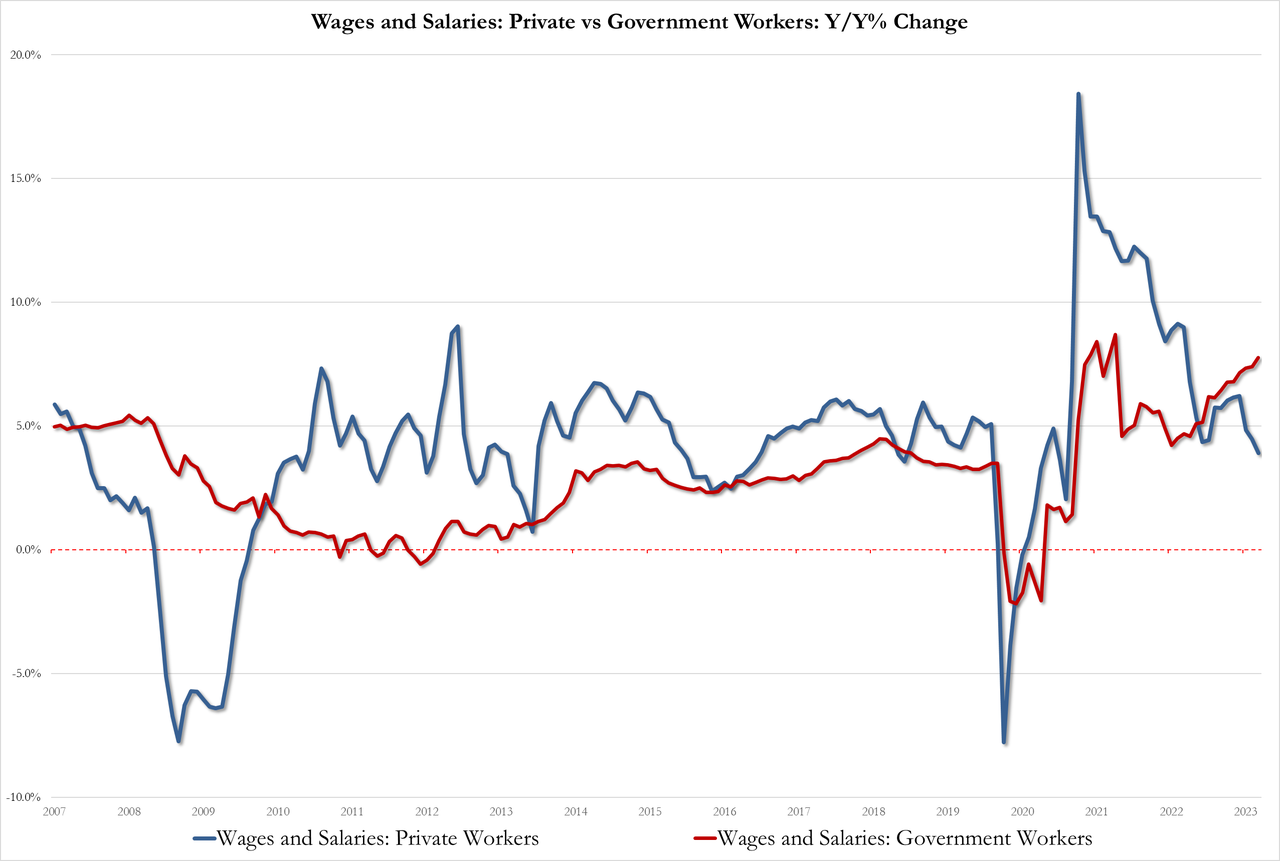

Focusing on the income side alone, private workers wages plunged to 3.9%, down from 4.5% and the lowest since Feb 2021.

So where is the offset to hot wages you may ask? Why government workers: wages of govt workers are up 7.8% YoY vs 7.4% in August and approaching the record high of 8.7% in Oct 2021

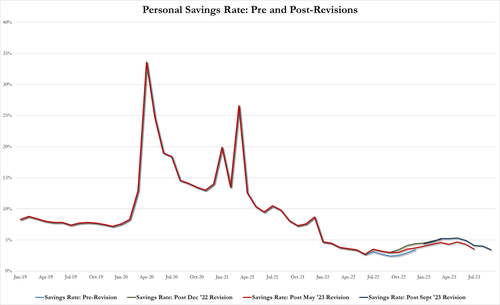

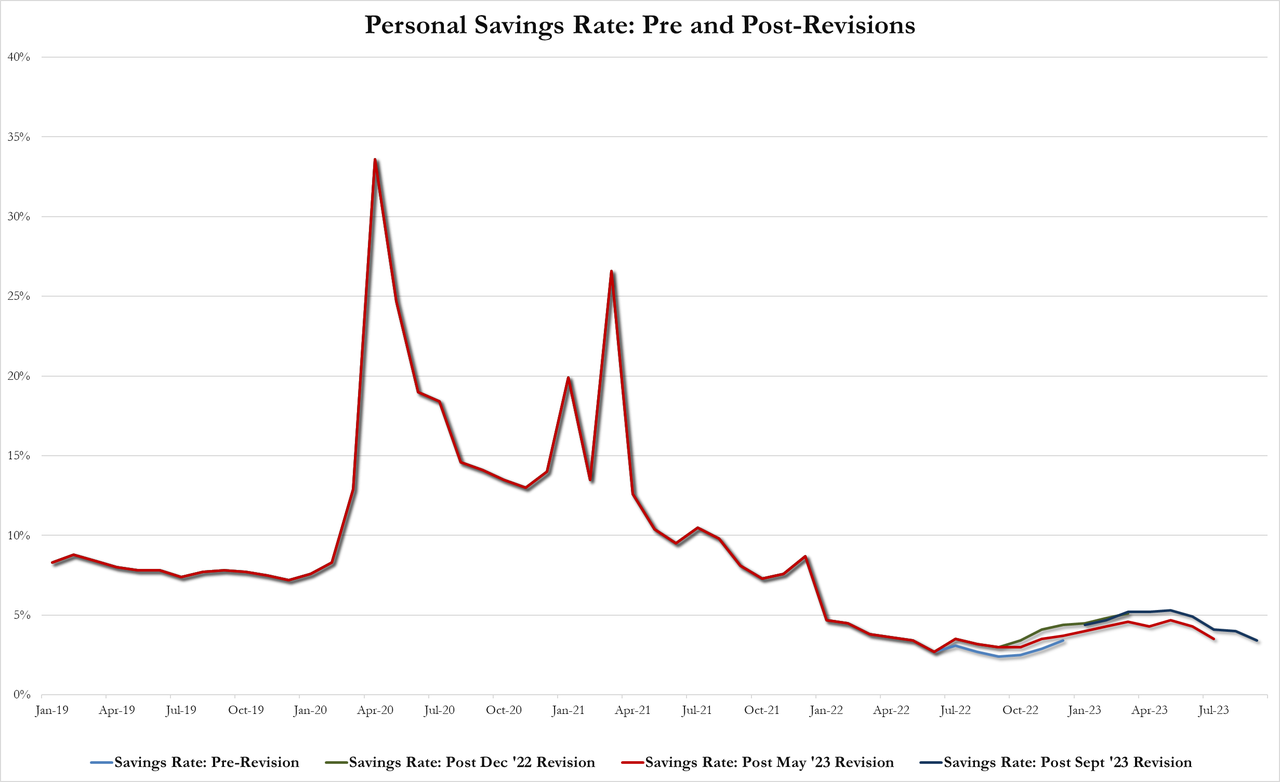

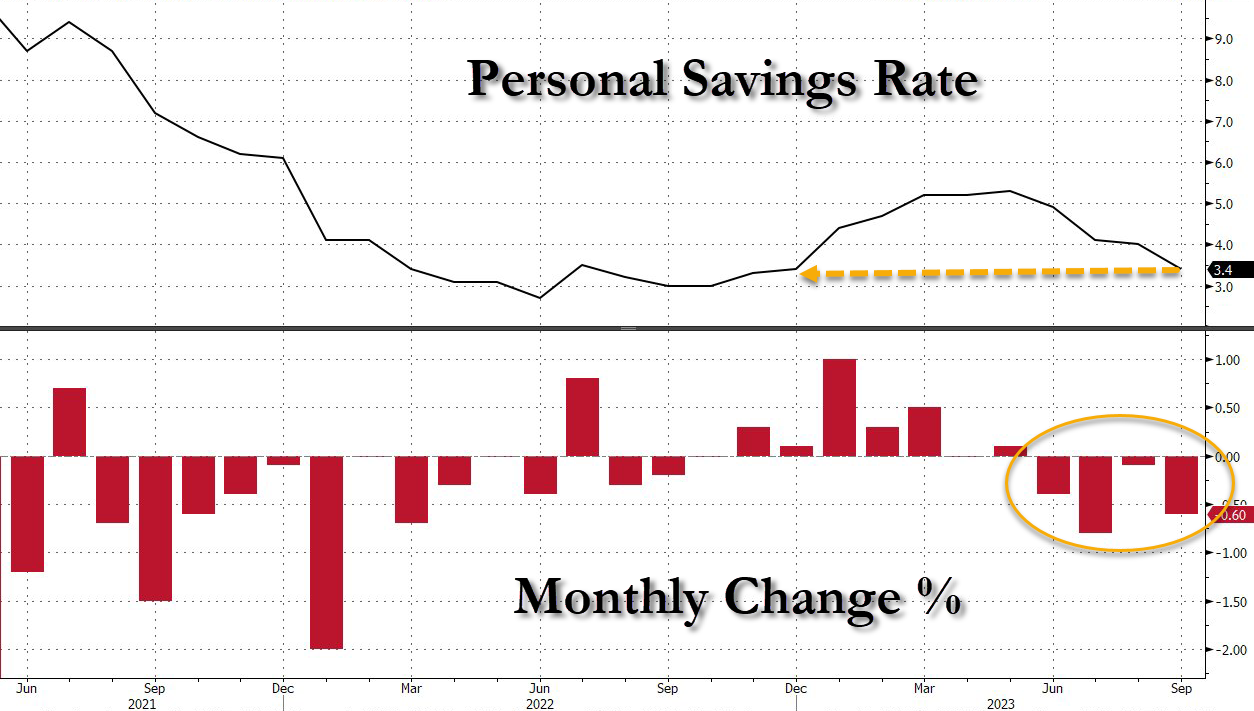

All of which means the personal savings rate collapsed even further, from 4.0% to 3.4% of DPI…

Source: Bloomberg

The savings rate is down 4 straight months, back near record lows… AND this is after artificial revisions that artificially boosted the savings rate 3 times in the past year (see above chart)

The US is teetering on World War III with tensions soaring in the Middle East, Ukraine, and southeast Asia. And Biden wanders off to Rehobeth Beach Delaware to relax … while over 200 Americans are still held hostage by terrorist group Hamas. The bad news? Biden is back in Washington DC trying to make the border crisis even worse by demanding funding for “border security” in the form of transporting illegal immigrants to US cities. Is The Squad running The White House??

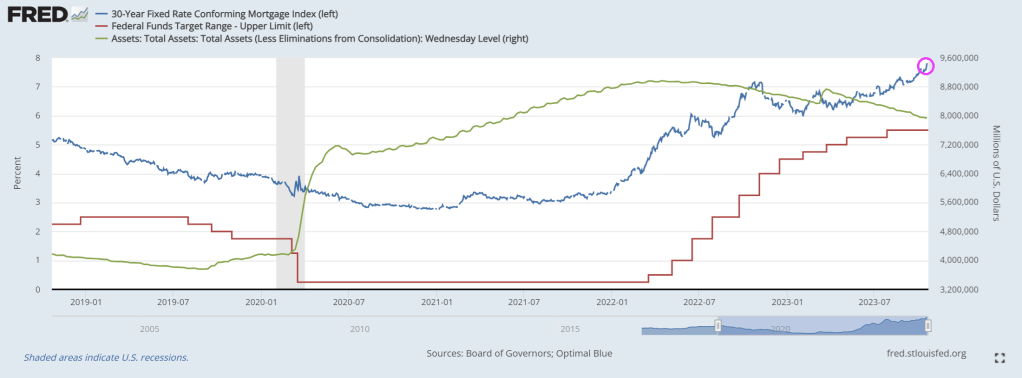

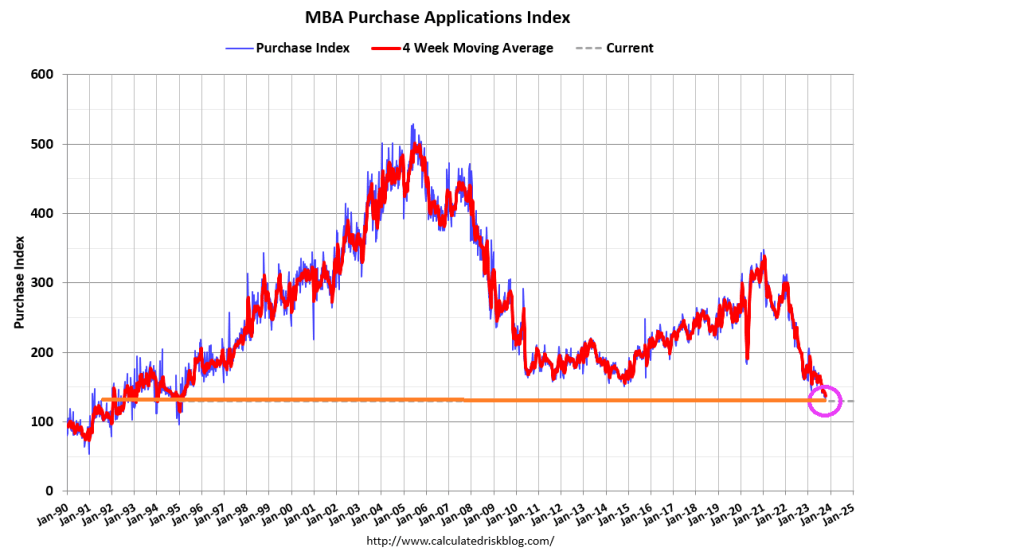

But on the housing/mortgage front, we have another week of declining mortgage demand/applications as mortgage rate hit almost 8%.

Mortgage applications decreased 1.0 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending October 20, 2023.

The Market Composite Index, a measure of mortgage loan application volume, decreased 1.0 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 1 percent compared with the previous week. The Refinance Index increased 2 percent from the previous week and was 8 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 2 percent from one week earlier. The unadjusted Purchase Index decreased 2 percent compared with the previous week and was22 percent lower than the same week one year ago.

Mortgage rates followed Treasuries higher, with the 30-year fixed mortgage rate jumping 20 basis points to 7.9 percent – the highest since 2000. Rates have now risen seven consecutive weeks at a cumulative amount of 69 basis points.

Hey Joe, I’ll bet those 200+ US hostages held by Hamas aren’t enjoying ice cream cones.

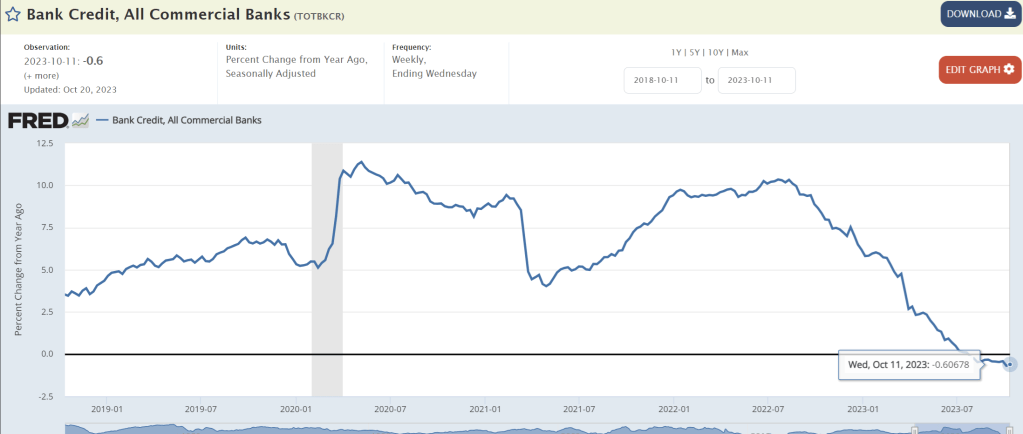

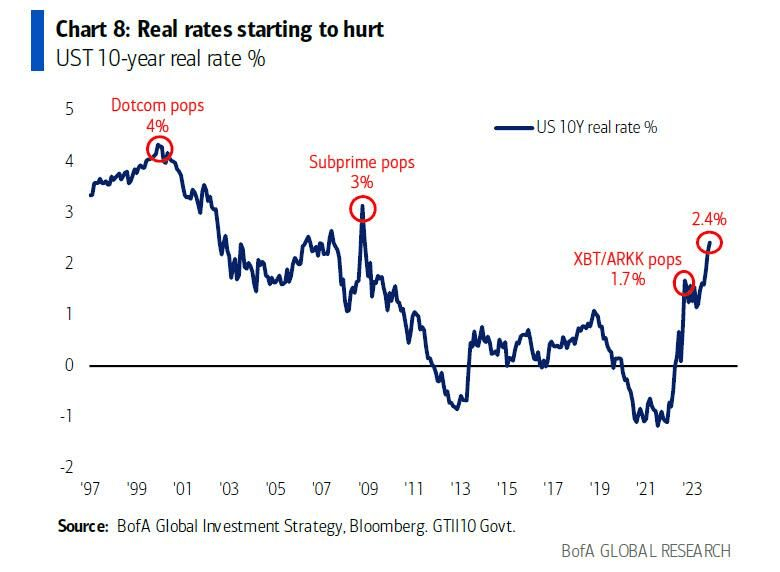

Back in red? As US fiscal policy deteriorates further thanks to endless Federal spending (not to mention seemingly endless wars under Biden and Nobel Peace Prize winner Obama), we are seeing pain in the bank lending business.

Commercial and industrial (C&I) loan lending standards is tightening (blue line) to levels typically seen in recessions. Even though Barclays HY-10Y spreads remains low.

Bank credit growth remains negative for the twelve straight week.

Billions Biden’s spending spree has led to the budget gap has doubled in the last year.

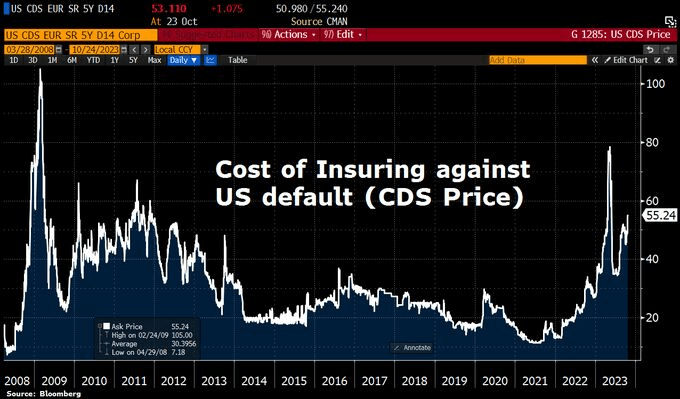

CDS is now at 55.24, highest after the Covid shock.

Under Biden/Yellen’s economic model, the appropriate themesong is “Hell’s Bells.”

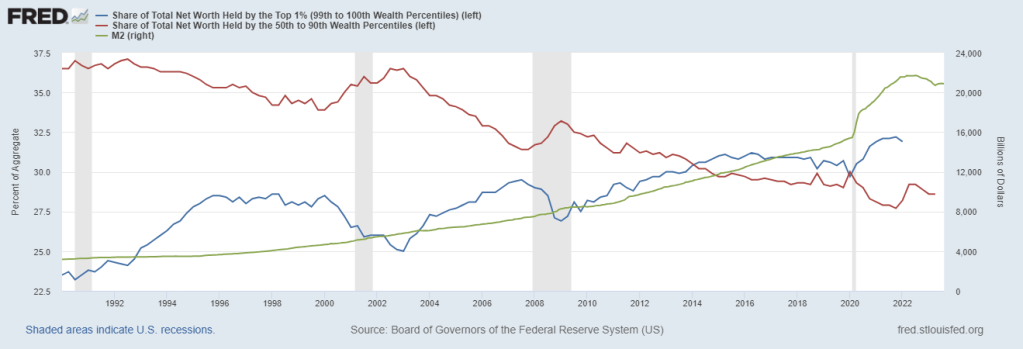

Bidenomics has been a massive windfall for the top 1% of households in terms of wealth due to the emphasis on green energy transformation. But for the 99%, Bidenomics has been a disaster (unless you consider low-paying job creation a victory).

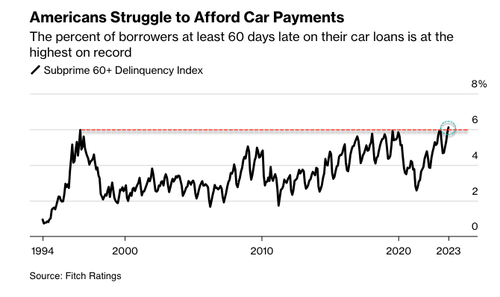

The auto sector, considered a leading economic indicator, pinpoints the arrival of the crushing auto loan crisis and even the possibility of the onset of the next recession. In late January, we Fitch revealed tat consumers are falling behind on auto payments – the most since the peak of the Great Financial Crisis. Fast forward nine months later, to September, that rate just hit the highest level in nearly three decades.

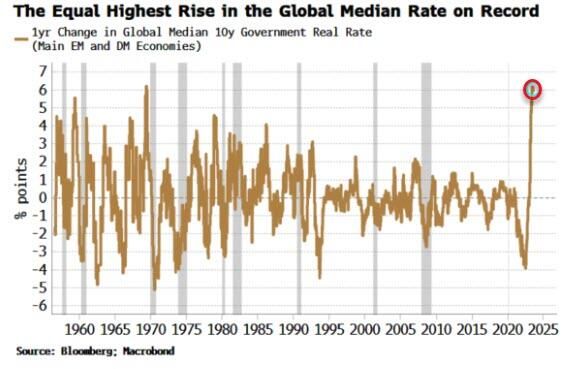

And with interest rates rising the fastest in history,

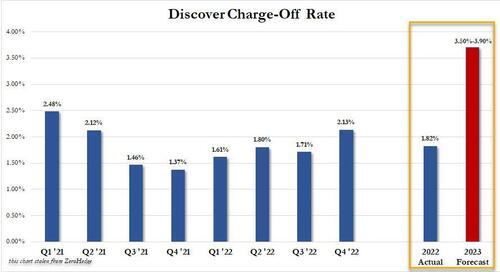

And Discover projected charge off rate for 2023 would more than double from its current 1.82% to as much as 3.90%!

In what could be the early innings of the auto loan crisis, something we called a “perfect storm” earlier this year, Bloomberg cites new Fitch data:

The percent of subprime auto borrowers at least 60 days past due on their loans rose to 6.11% in September, the highest in data going back to 1994, according to Fitch Ratings.

Source: Bloomberg

“The subprime borrower is getting squeezed,” said Margaret Rowe, senior director with Fitch.

Rowe said, “They can often be a first line of where we start to see the negative effects of macroeconomic headwinds.”

What has been widely known is the consumer has been funding car purchases with even more debt to afford record-high prices, with many monthly payments exceeding $1,000. Factor in the Federal Reserve’s most aggressive interest rate hiking cycle in a generation, elevated inflation, and the restarting of the federal student loan payments, tens of millions of consumers are under immense pressure this fall.

An endless stream of retailers, such as Walmart, Nordstrom, Macy’s, and Kohl’s – all of whom have recently warned about a consumer slowdown. Banks have also raised concerns, such as Morgan Stanley’s Mike Wilson, who believes the consumer is ‘falling off a cliff.’ And the latest high-frequency data from Barclays shows card spending has taken another leg down.

As delinquencies rise, Cox Automotive forecasts that 1.5 million vehicles will be seized this year, up from 1.2 million in 2022. That’s still below pre-pandemic levels, but the numbers could soar if a recession materializes in 2024.

Bloomberg cited Bankrate data that shows consumers with excellent credit can lock in an average interest rate of around 5.07% for a new car and 7.09% for a used vehicle. Those with bad credit should expect a new car rate of 14.18% and 21.38% for a used car.

The perfect storm we described earlier this year is unfolding.

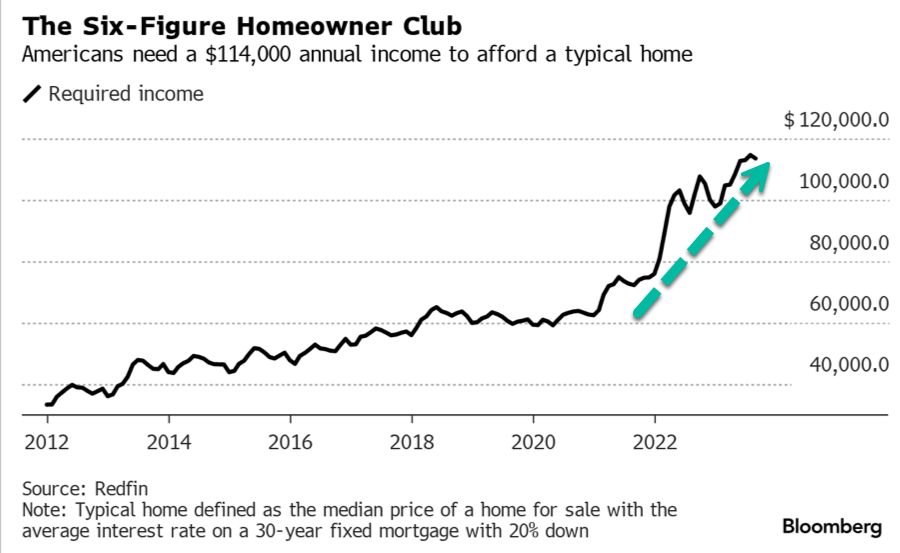

At least residential mortgage delinquency rates remain low. With elevated home prices, the incentive to default on a loan is limited.

So The Perfect Storm hasn’t hit residential real estate … yet. But with households needing $114,000 in annual income to afford a typical home …

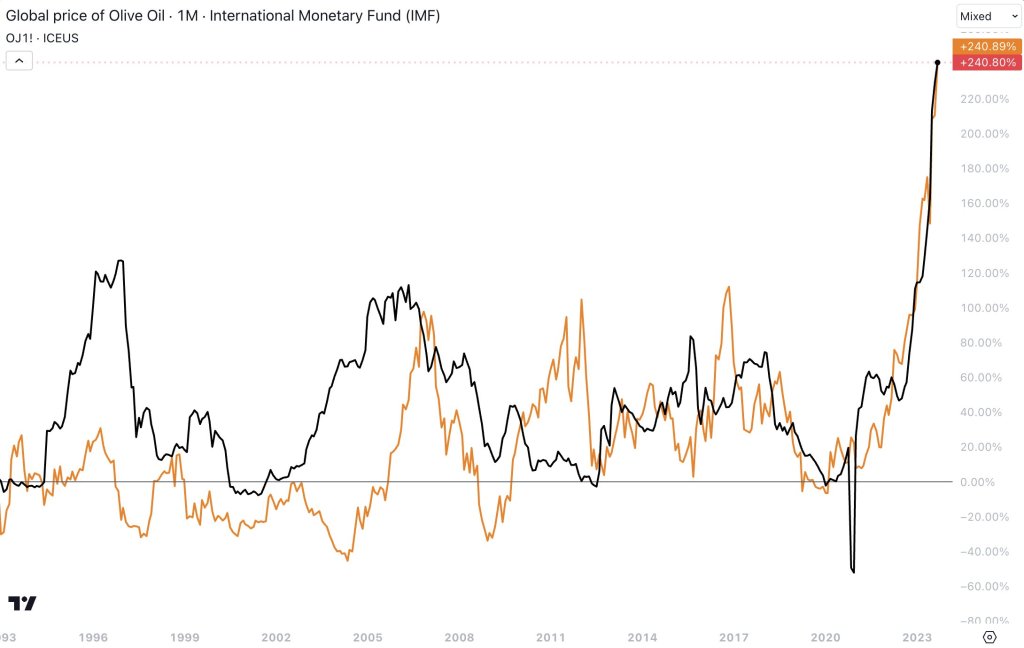

But at least home prices aren’t rising as fast as olive oil and orange juice!! Wow, that excesssive stimulypto by The Fed and Federal government is really screwing things up in the economy.

Biden is like George Clooney in “The Perfect Storm” sending the US out into stormy, violent seas while obessing about Ukraine and protecting Iran/Hamas.

Mortgage applications decreased 6.9 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending October 13, 2023. Applications decreased to their lowest level since 1995, as the 30-year fixed mortgage rate increased for the sixth consecutive week to 7.70 percent – the highest level since November 2000.

The Market Composite Index, a measure of mortgage loan application volume, decreased 6.9 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 7 percent compared with the previous week. The Refinance Index decreased 10 percent from the previous week and was 12 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 6 percent from one week earlier. The unadjusted Purchase Index decreased 5 percent compared with the previous week and was 21 percent lower than the same week one year ago.

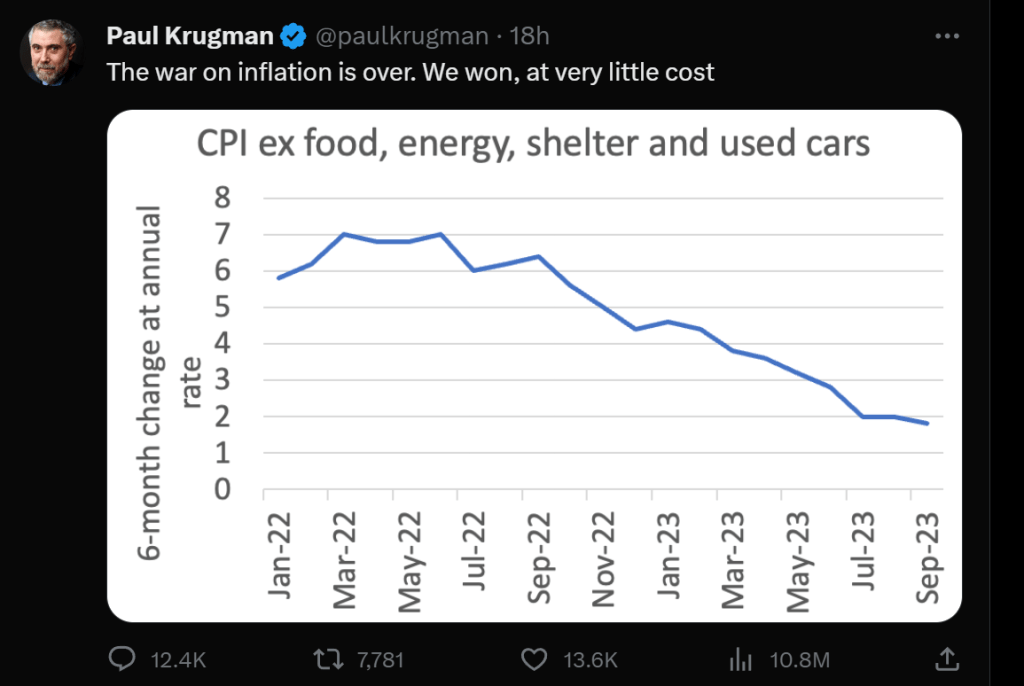

Paul Krugman, Nobel Laureate in economics and media celebrity, made a terrible claim yesterday when he pronounced that “The war on inflation is over. We won, at very little cost.” Krugman’s proclamation was trumpeted by The View’s Joy Behar Joy who claimed that everything is going great in the country! The economy is “booming” and people are having an “easier time” putting bread on the table. Huh? Easier than a month ago maybe, but not easier since 2021 under Bidenomics.

Hmm. Suppose that during World War II the Germans had stopped after they invaded and captured Paris on June 14, 1940. The war could have been over, but France was lost to Germany amidst thousands of dead and loss of property. That is not a victory, but a crushing defeat.

Just like my Paris example, Krugman’s claim the war on inflation is over and we won AT VERY LITTLE COST was grossly misleading and a big kerplunk (thud). Why? For one, the average American family is $7,400 POOR than in January 2021 when Biden became President. So, it looks like we know the cost of inflation and it was steep, not “very little cost.” Well, very little cost to elitist millionaires like Krugman.

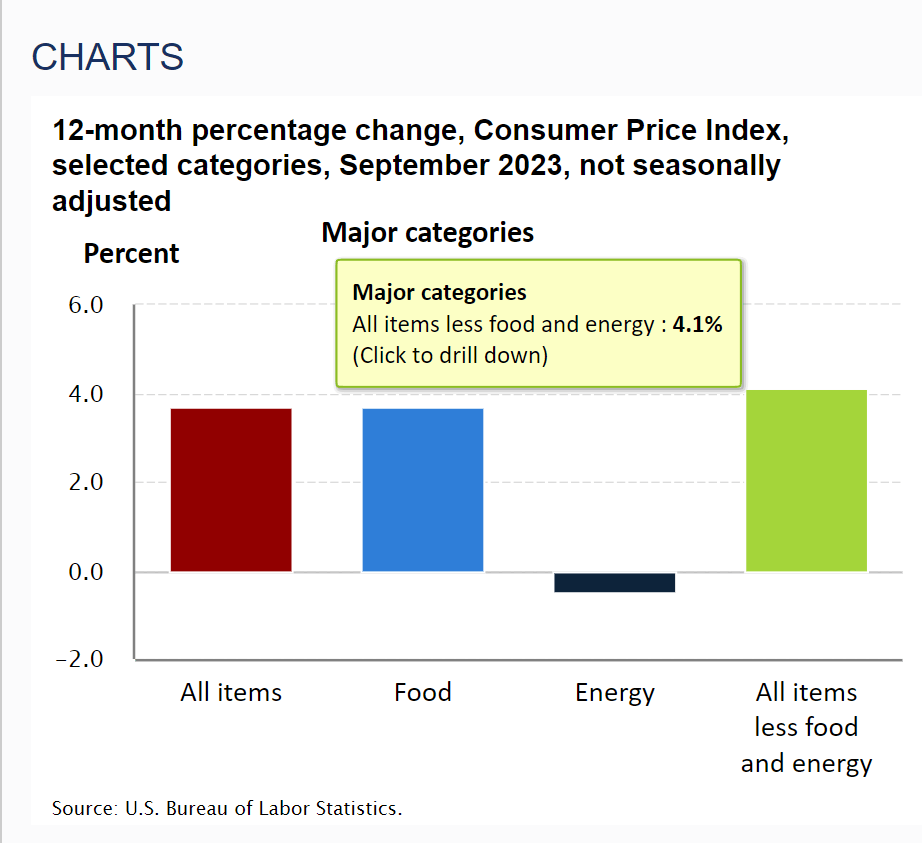

Krugman loves the recent inflation report from the BLS. Specifically, the 12-month change in the Consumer Price Index Less Food And Energy for September was 4.1%. Krugman focuses on the recent 6-month change being less than 2%. In Krugman’s mind, this is victory … core inflation has been tamed and inflation is at The Fed’s target rate of 2%.

But before Krugman pops the champagne cap on the 1959 Dom Perignon for $42,350 (while the rest of us are drinking E&J Gallo’s Thunderbird), bear in mind that he is referring to the RATE OF GROWTH in prices, not the highly elevated levels of prices. Victory against inflation would be if prices returned to December 2020 levels.

I pointed out yesterday that “real” wages contracted 0.1% YoY (after 3 months positive) in September. It is important to note that real wage growth was negative from 2021 until 3 months ago, but has gone negative yet again. Victory??

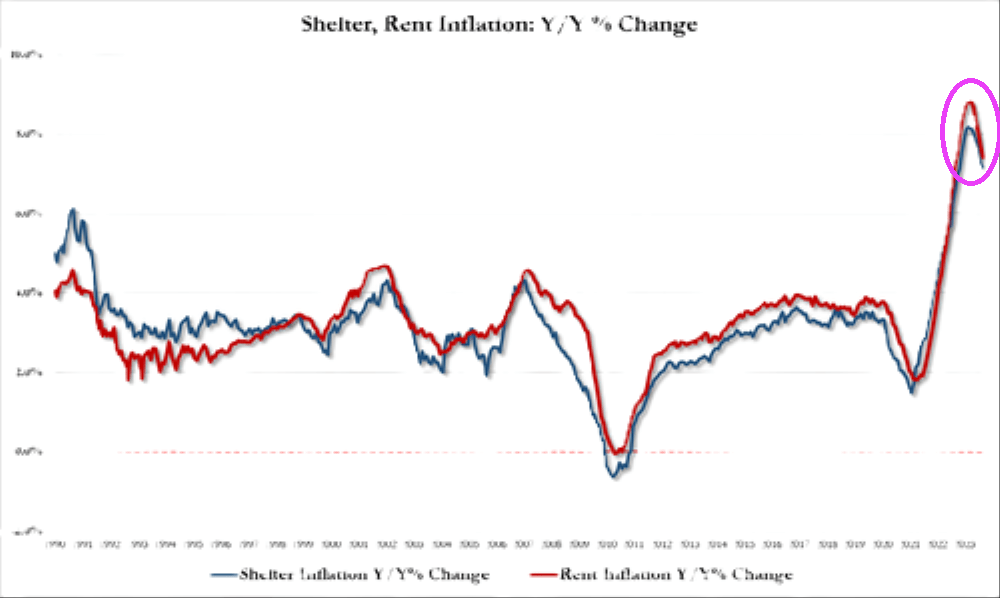

Krugman prefers core inflation, removing food, housing and energy. You know, the three things most Americans actually care about. Take shelter (or rent of residence) where rent is growing at a sizzling 7.1% YoY.

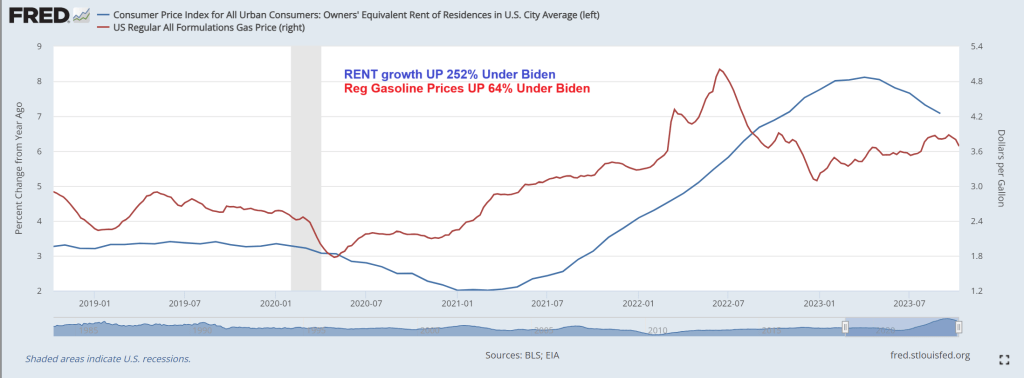

Under Biden and Congress’ reckless spending splurges (and inane Federal energy policies), regular gasoline prices are up 64%. Growth in rent of residence has grown 252%! So, Professor Krugman, Americans are far worse off than before Biden was President.

If prices return to December 2020 (or pre-Covid levels), I will declare a victory. But for right now, symbollically, the German army is occupying France and Paris with horrible suffering for the French people. In other words, Americans are still far worse off under Biden even though inflation is finally slowing.ew

Speaking of France and World War II, maybe we should consider Joe Biden as today’s Pierre Laval, leader of Vichy France since Biden seems more concerned with pleasing Klaus Schwab and The World Economic Forum than America’s middle class and low wage worker (like Laval was concerned with that German leader Adolf Hitler thought).

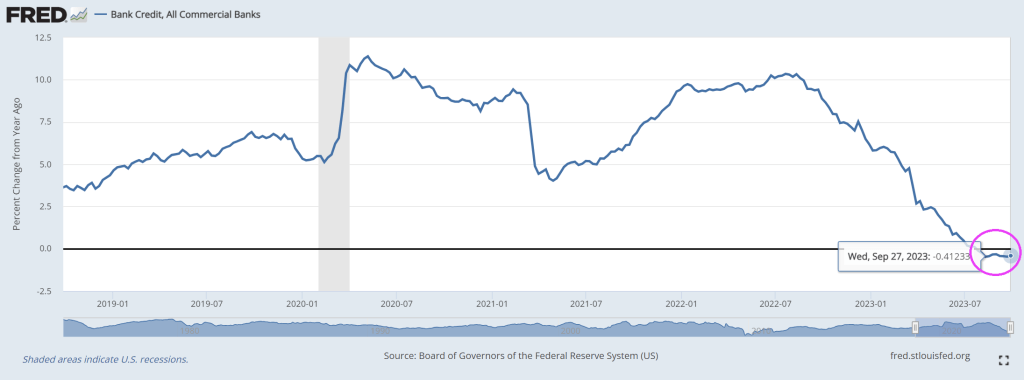

Bidenomics is failing catestropically. Example? As interest rates rise to fight Biden’s Federal spending splurges, bank credit growth slowed to -0.41% YoY for the 10th straight week of negative credit growth.

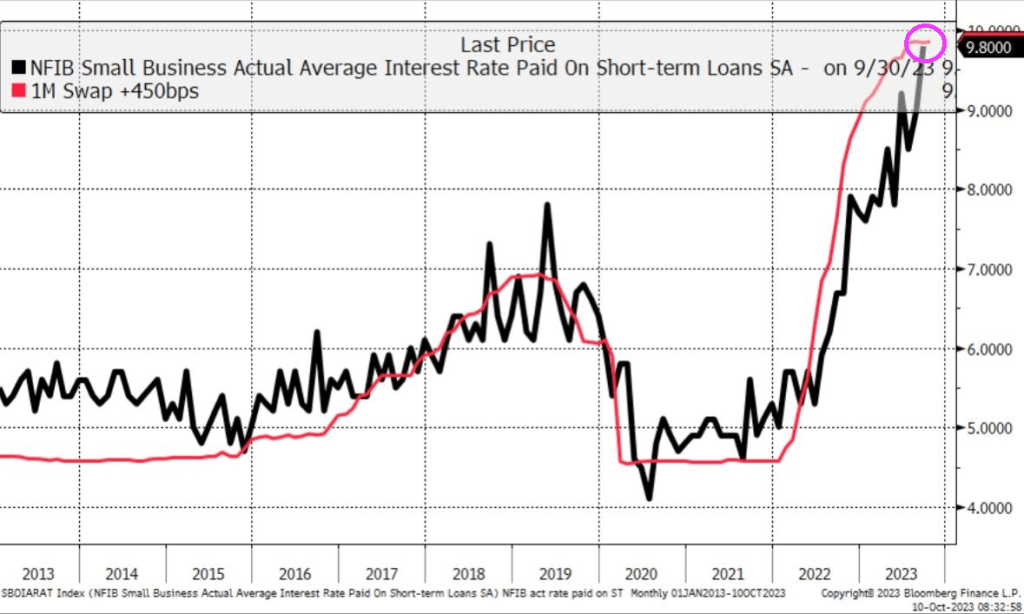

While interest paid on short-term loans almost 10%!!

“Jimmy, watch me tank the economy even worse than you did!”

Joe Biden is the Buzz Lightyear of the economy … and not in a good way. Under Biden and the Congressional spending sprees, the US debt is going to infinity … and beyond!

Twenty days.

That’s how long it took the Biden administration to add another half-trillion dollars to the national debt.

Bidenomics certainly requires a lot of borrowing and spending.

On September 15, the debt quietly blew passed $33 trillion. On October 5, it pushed above $33.5 trillion.

Don’t forget about the $194+ TRILLION in unfunded liabilities that politicians promised the non 1%.

By the way, it only took Biden and his willing accomplices in Congress three months to drive the national debt from $32 trillion to $33 trillion.

As of October 5, the debt stood at $33,513,382,512,663.51.

This is an unimaginable amount of money.

To put things into some perspective, the total output of the US economy as measured by GDP was only $25.46 trillion. That means the US economy would have to grow by 33.5% to cover the national debt.

At $33 trillion, the US national debt is more than the total economies of China, Japan, Germany, and the UK combined.

Looking at it another way, as of Oct. 10, every US citizen would have to write a $99,839 check in order to pay off the debt, and every American taxpayer is on the hook for $258,257.

Part of the reason the debt has increased so fast since June is because the Treasury is still rebuilding cash reserves that were depleted during the debt ceiling fight. But the fact remains – the federal government spends too much money.

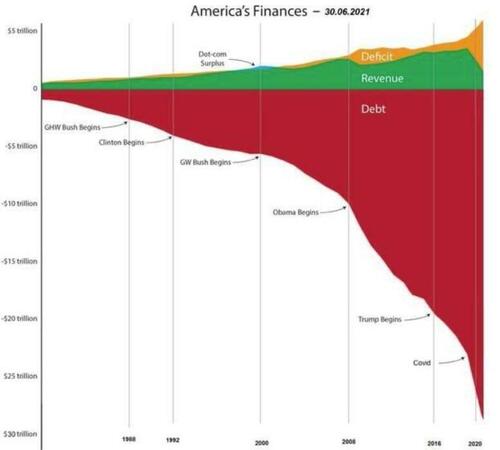

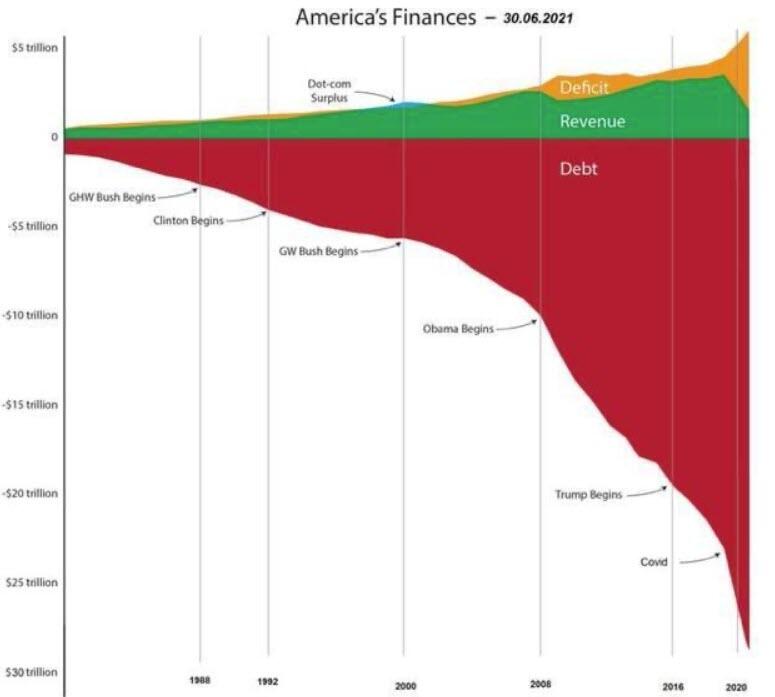

It’s hard to overstate just how bad the US government’s fiscal situation has become. We have a trifecta of surging debt, massive deficits, and declining federal revenue. The chart below provides a visual perspective – and it doesn’t even account for the last few years.

This relentless increase in debt is happening when the economy is supposedly strong. Typically, a strong economy generates more tax revenue, and deficits shrink. But this isn’t really a strong economy. It is a house of cards built on debt. Fiscal stimulus is helping to prop it up.

That means there is no end in sight to this upward-spiraling national debt.

The biggest issue is the federal government spending addiction. In August alone, the Biden administration spent over $527 billion.

In fact, the US can’t even afford the interest on the debt.

Uncle Sam’s interest expense is already rising at an astronomical rate, and it’s set to explode.

The federal government has paid well over half a trillion dollars ($630 billion) on interest payments alone in fiscal 2023, with one month left to go. Interest on the debt paid in July exceeded the amount spent on national defense that month. Uncle Sam is well on the way to spending more on interest payments than any line item other than Social Security and Medicare.

The average interest rate on the debt is now at the highest level since 2011, coming in at 2.92% as of the end of August. But that’s still relatively low, and the debt is more than double what it was back in the good ol’ days of 2011.

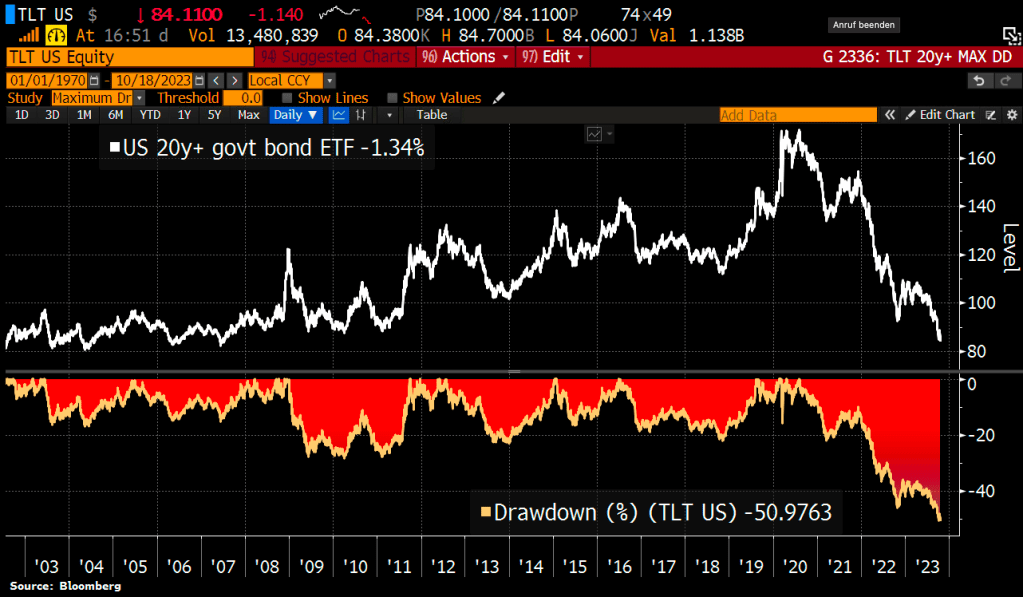

Meanwhile, the average interest rate is poised to climb rapidly. A lot of the debt currently on the books was financed at very low rates before the Federal Reserve started its hiking cycle. Every month, some of that super-low-yielding paper matures and has to be replaced by bonds yielding much higher rates. That means interest payments will quickly climb much higher unless rates fall.

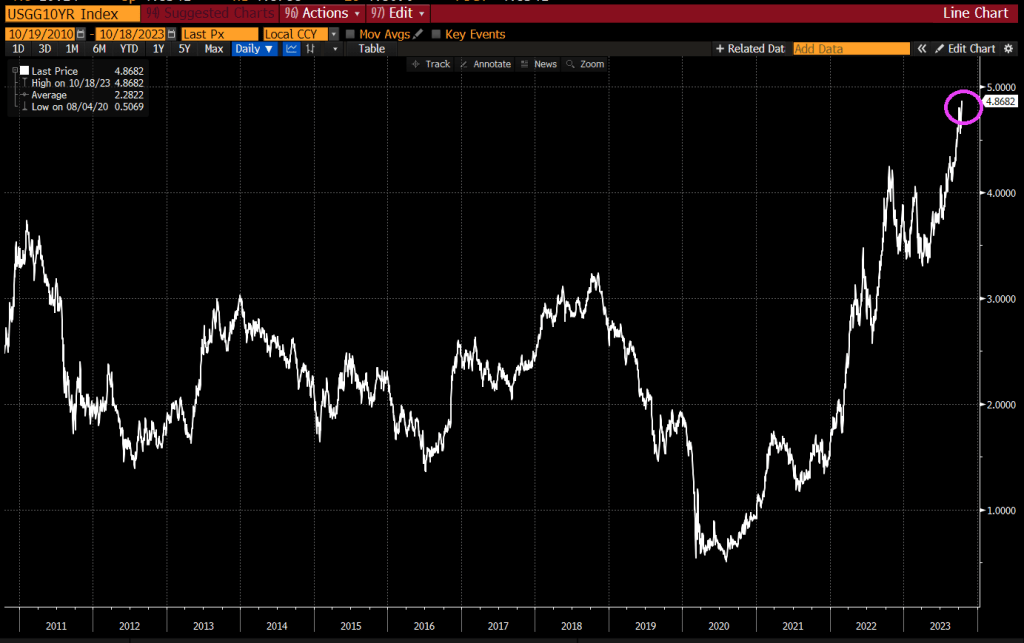

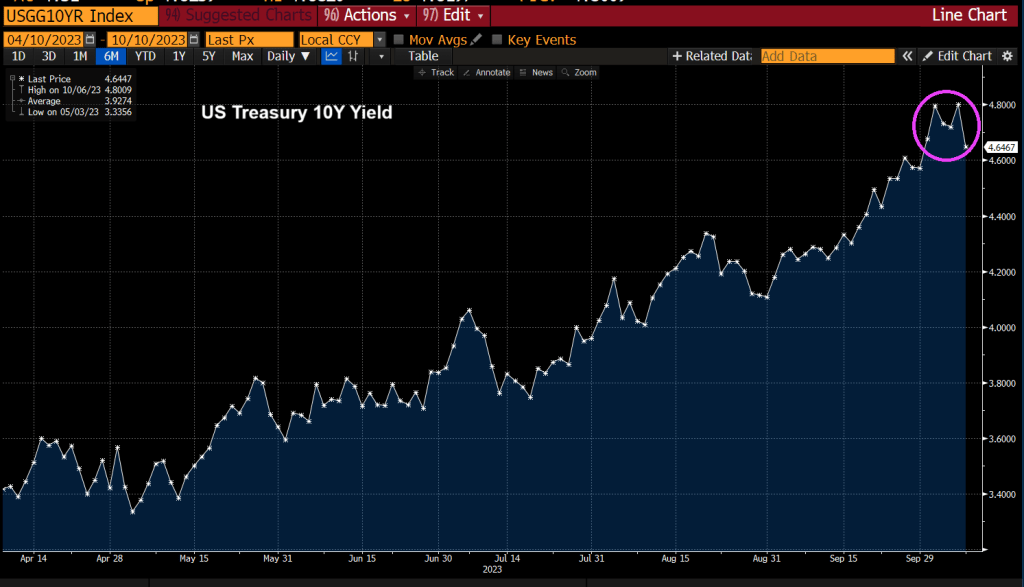

To give you an idea of where we’re heading, T-bills currently yield about 5.5%, the two-year yield is over 5% and the 10-year currently yields around 4.7%.

This has driven interest payments as a percentage of total tax receipts to over 35%. In other words, the government is already paying more than a third of the taxes it collects on interest expense.

If interest rates remain elevated, or continue rising, interest expenses could climb rapidly into the top three federal expenses. (You can read a more in-depth analysis of the national debt HERE.)

People tend to yawn at the ever-increasing national debt, but it is a ticking time bomb. Who knows how much time is left, but the timer is ticking relentlessly toward zero.

Like President Biden enjoying a barbeque at The White House with a live band (probably NOT Justin Moore singing “Small Town USA”) while Hamas declared war on Israel and Americans are being held hostage with the promise of public executions of hostages livestreamed. Nothing that “Empathy Joe” does ever surprises me anymore, but I am surprise that various Federal Reserve Presidents will speak today while Hamas terrorizes Israeli and US citizens.

It could be that investors think that Talking Heads at The Fed will claim that Fed rate increases are over. Then again, the Iran/Hamas terror campaign against Israel is spookking markets, driving up oil and gold prices and driving up “flight to safety” in US Treasuries.

President Biden called on Americans in Israel to book a commercial flight home, even though Israel has cancelled all flights. Does Old Joe even read the news??

“Two-job Joe” should be Biden’s new nickname for his economy wrecking ball known as Bidenomics.

The economic disaster known as Bidenomics (code for wealth transfers to the donor class) can be seen in the following chart. Non-elite households are struggling to cope with higher gasoline, food and house prices (rent) under Bidenomics.

As a result, the number of people holding 2 FULL-TIME JOBS hit an all-time high of 447,000 people. Biden spokesperson Karine Jean Pierre is likely to say “See? Bidenomics is working! Not every person is holding 2 full-time jobs to afford that Ford all-electric Lightning F-150 pickup truck!”

At the same time, wage growth YoY is crashing from Covid stimulus highs to pre-Covid levels.

It is getting harder and harder for non-elites to buy that Ford F1-150 all-electric Lightning Platinum for $94,000 plus tax. And you still have to pay $500 for the Ford Mobile Power Cord. OMG! For $94k, they couldn’t throw in the power cord?????

Does F stand for Failed? The honorary vehicle for Bidenomics!!

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.