US existing home sales in November collapsed by -38.6% YoY as M2 Money growth runs out of gas.

The above chart is similar to yesterday’s “Ski Slope” chart of US home prices YoY.

Unfortunately, pending home sales YoY are the worst in recorded history.

What will President Biden do about this dire situation? Our “Vacationer in Chief” is off on yet another vacation to St. Croix in the US Virgin Islands, so probably nothing. Now that Biden is sunbathing, what will his Treasury Secretary Janet Yellen do?

The market began downshifting earlier this year as the Federal Reserve started hiking its benchmark interest rate, with the goal of easing high inflation that’s been driven in part by skyrocketing housing costs.

Rates for 30-year, fixed mortgages reached 7.08% in October — and again in November — though they have since retreated, Freddie Mac data show. With borrowing costs roughly double where they were at the start of the year, and inflation leaving less savings to put toward a down payment, homebuyers have pulled back. Sellers are also reluctant to list their properties, yet houses that are on the market are lingering and getting discounted as demand slumps.

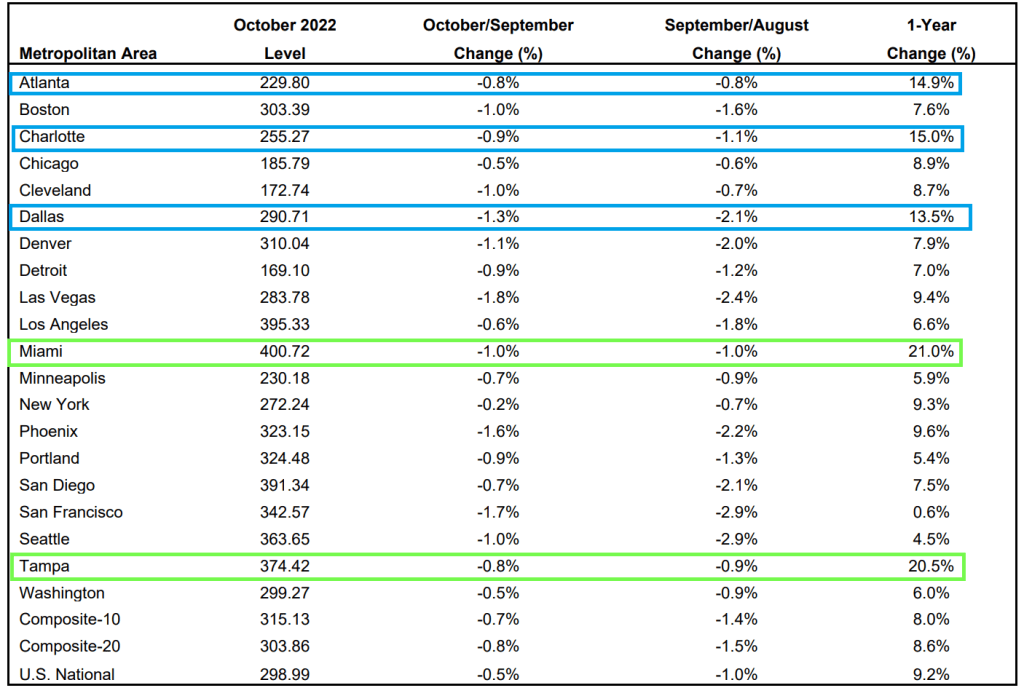

The Case-Shiller National Home Price Index “cooled” to 9.24% YoY growth as The Federal Reserve tightens its monetary noose.

Of the top twenty metro areas, both Miami and Tampa Florida were up over 20% YoY. Hot ‘Lanta, Charlotte and Dallas were over 10% YoY. Mordor on the Potomac was up “only” 6% and all other metro areas were under 10%.

But if we look at October/September changes, all metro areas are down (MoM) with San Francisco the worst.

Finally, The Federal Reserve’s massive balance sheet is still out in force.

Look at this chart of the Case-Shiller National home price index again The Fed’s balance sheet. Uh-oh.

Let’s look at San Francisco (my hometown) since The Federal Reserve began interest rate tightening.

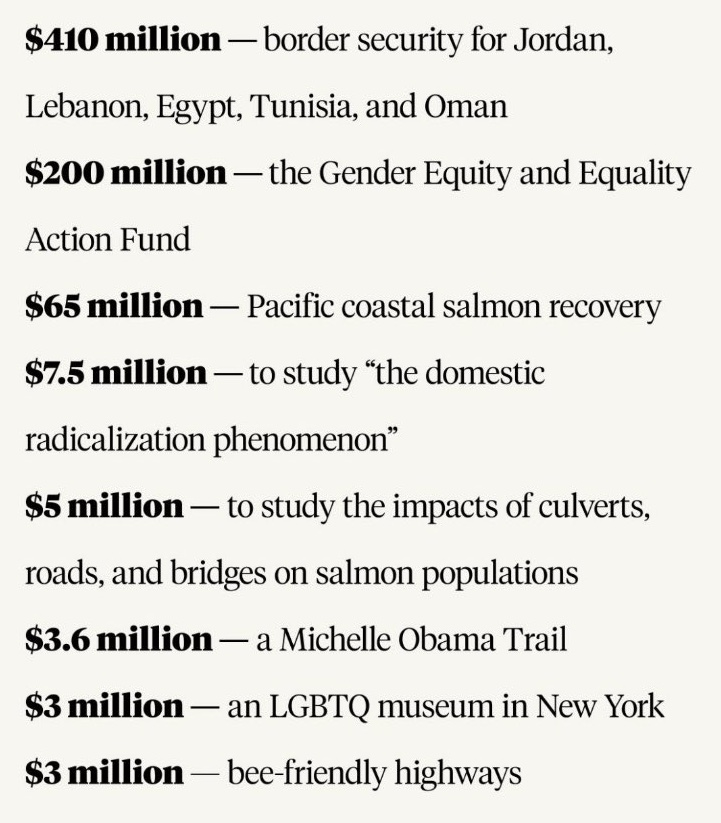

Here are the Lords of Darkness (Schumer and Pelosi) who concocted this witch’s brew of crony payoffs that will be ulitmately signed by El Stupido (Biden).

Do I detect a trend in the US Leading Economic Indicator data?

The Conference Board’s US Leading Economic Indicator was released this morning and it wasn’t pleasant. The US Leading Index was down -1% MoM in November.

On a year-over-year basis, it is down -4.5% YoY as The Fed withdraws its massive monetary stimulus.

The good news … for military contractors … is that Biden and Congress have given Ukraine’s Zelenskyy ANOTHER $47 BILLION.

On a year-over-year (YoY) basis, US real GDP rose to a measly 1.9%. US core PCE YoY fell slightly to 4.93%. M2 Money growth is at 2.6% YoY.

The Misery Index (U-3 inflation rate + inflation) remains elevated and above 10% (it currently clocks-in at 12%), far above the pre-Covid reading of around 5%.

Here is the rest of the story. On a quarter-over-quarter basis, real GDP rose to 3.2% QoQ. Personal consumption rose 2.3% QoQ. Core PCE (Personal Consumption Expenditures) rose to 4.7% QoQ. If we use core PCE as a measure of inflation, inflation is rising.

Here is a video of Fed Chair Jerome Powell (doubling as President Joe Biden) saying creating inflation and then raising interest rates to fight it “It’s for the best.”

One of the big problems with Federal goverment and Federal Reserve monetary stimulus is … it wears out. Just look at M2 Money growth.

US existing homes sales fell -7.70% in November to 4.09 million units SAAR. And since the same month last year, existing home sales are down -35.4% YoY.

Existing home sales were the lowest in November since 2010.

The good news? The median price of existing homes fell to 3.21% YoY. The bad news? The ark is really bad pointing to a bad December. Inventory for sale (orange line) remains below pre-Covid shutdown levels.

The mortgage market is behaving like today’s bomb cyclone in terms of the weather. Bomb cyclone in that mortgage rates have dropped 7.16% on October 21, 2022 to 6.34% on December 16, 2022 (a drop of 82 basis points), but mortgage purchase and refinancing applications are not increasing like one would hope.

Mortgage applications increased 0.9 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending December 16, 2022.

The Refinance Index increased 6 percent from the previous week and was 85 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 0.1 percent from one week earlier. The unadjusted Purchase Index decreased 3 percent compared with the previous week and was 36 percent lower than the same week one year ago.

But remember, The Federal Reserve is going to be lowering their target rate after they keep raising it.

(Bloomberg) — Bank of Japan Governor Haruhiko Kuroda just gave investors a glimpse of what to expect when the world’s boldest experiment with ultra-loose monetary policy comes to an end.

In the face of sustained market pressure, Kuroda shocked markets Tuesday by saying he’ll now allow Japan’s 10-year bond yields to rise to around 0.5%, double the previous upper limit of 0.25%.

Whether this is a strategic tweak to buy time for his yield-curve control settings until his decade-long term ends in Aprilor the start of the end for his unprecedented monetary easing remains to be seen.

Here are the BOJ’s rate. bands being widened.

The yen?

And with the ECB, Fed and now Bank of Japan all tightening, we are seeing sovereign yields rising across the board.

The Japanese sovereign yield curve is upward sloping unlike the humped US Treasury yield curve.

US housing starts plunged -16.4% since the same time last year (aka, YoY) as The Federal Reserve continues tightening its monetary policy.

Since October (aka, MoM), housing starts only dropped -.049% in November. 1-unit detached starts were down -4.06%. But multifamily (5+) starts were up 4.85% MoM.

Building permits were down -11.24% from October to November (baby, its cold outside!) and down -22.4% since November 2021 (aka, YoY).

Rising mortgage rates courtesy of The Federal Reserve’s tightening to fight Bidenflation has led to a Covid-level plunge in the NAHB Homebuilder Market Index.

Everything seems to be going down with a sinking M2 Money growth.

And today, the 10-year US Treasury yield is up over 10 bps. Watch out mortgage rates!

You must be logged in to post a comment.