“The data is basically screaming at us to go 50 but the geopolitical events were telling you to go forward with caution. So those two factors combined pushed me” to support the 25 basis points increase, he said. “Going forward that will be an issue whether to think about going 50 in the next couple of meetings or not. But the data certainly seem to suggest that we move in that direction.”

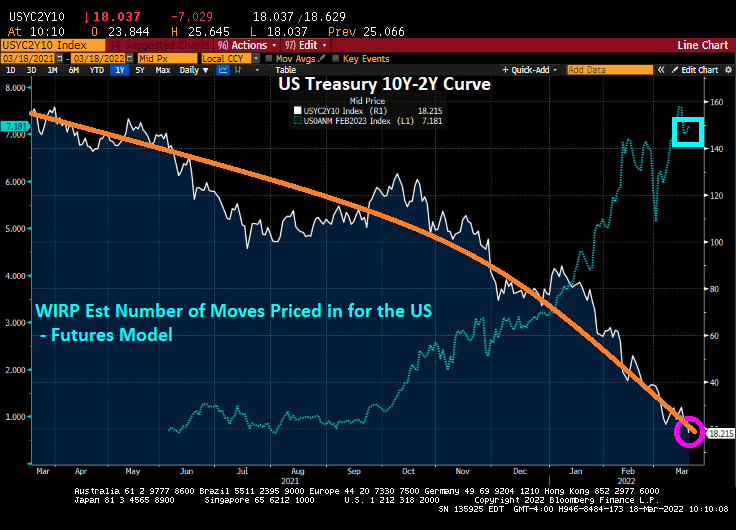

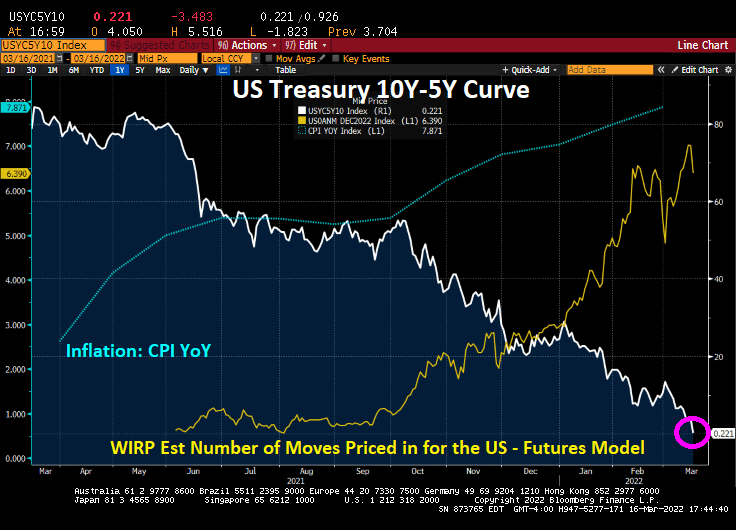

WIRP is pricing in over 7 rate increases by February 2023 as the Treasury yield curve (10Y-2Y)

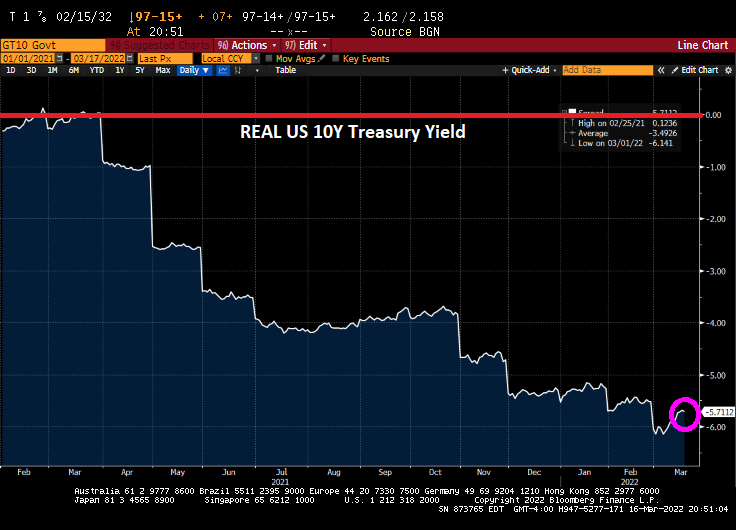

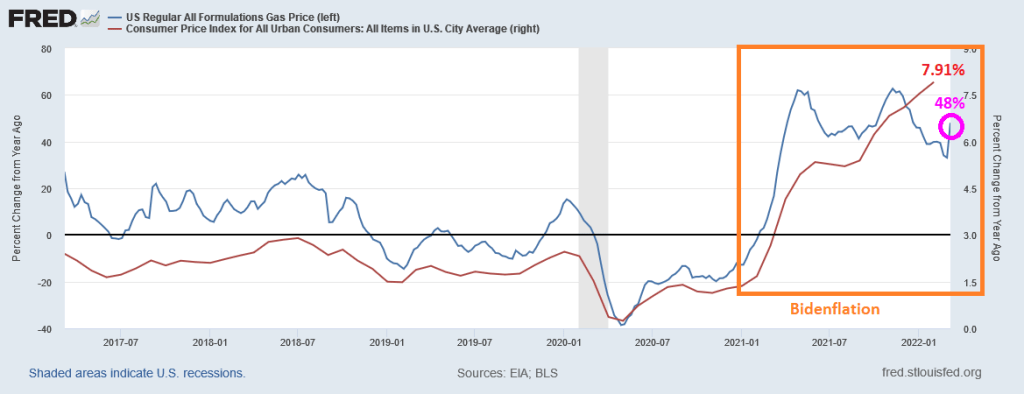

Well, Powell and The Fed Gang failed to tackle inflation with its 25 basis point increase in their target rate. The result? Inflation is still roaring and REAL Treasury yields remain NEGATIVE (nominal Treasury yields – inflation).

In fact, the US Treasury 10-year yield hovering around 0% when Biden first became President, then the inflation kraken was unleashed leading to progressively declining 10-year Treasury yields. As on late night, the REAL 10-year Treasury yield is -5.71%.

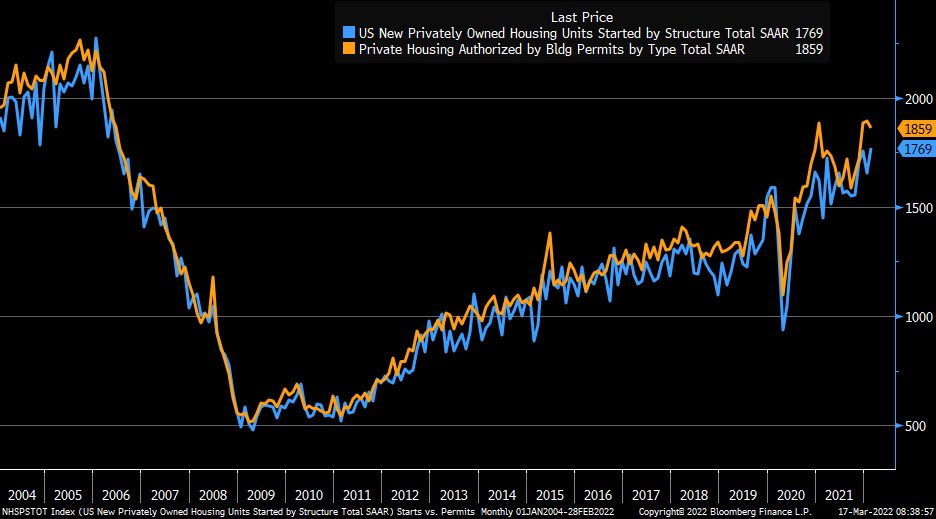

REAL mortgage rates (Bankrate 30Y rate – inflation) were positive at the beginning of the Biden Administration, but have sunk to -3.40%.

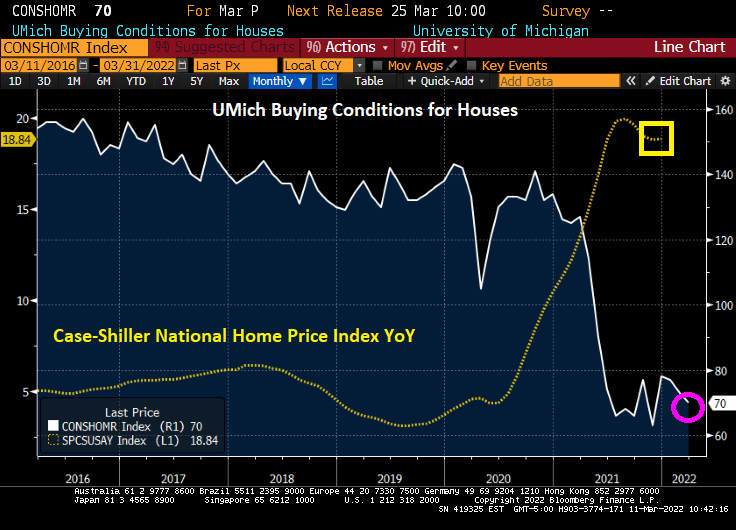

With negative REAL mortgage rates (and continued Fed Stimulypto), we saw February housing starts rise 6.8% in February.

The Fed is apparently jittery about Russia invading Ukraine (mentioned in The Fed minutes) as well as the possibility of China invading Taiwan (NOT mentioned in The Fed minutes).

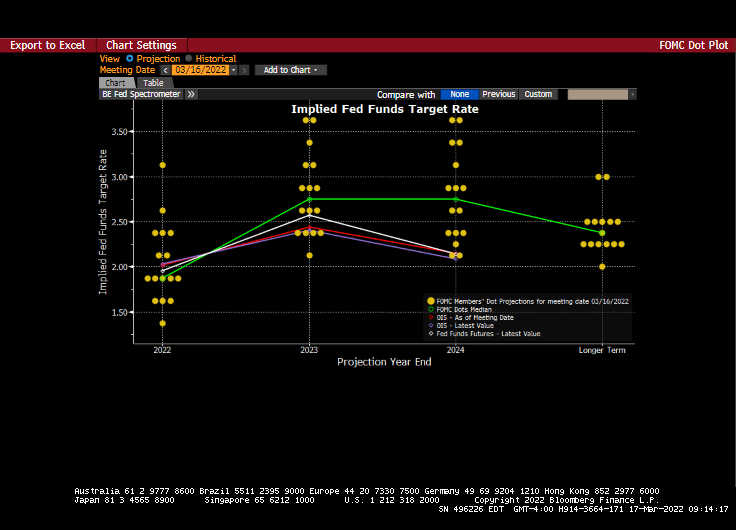

But if we look at the Fed DOTS plot, we see a rise in The Fed Funds Target rate in 2022 (7 rate hikes), more rate hikes in 2023 and 2024 and then a slowing in the longer term (as if voting members have a clue about the long-run economy).

The WIRP (Fed Funds Futures) is signalling 7 MORE rate increases over the coming year.

Biden is relying on Powell And The Fed Gang to provide ample liquidity in the markets, particularly before the midterm elections in November (hint: Biden doesn’t want Powell to rock the boat).

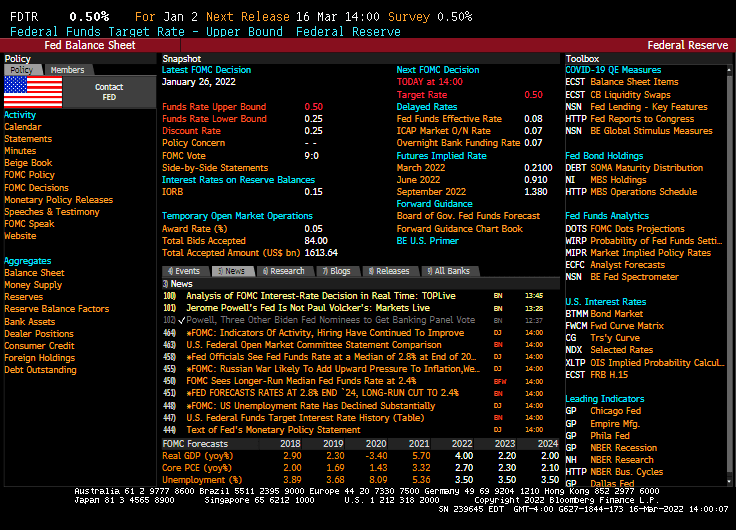

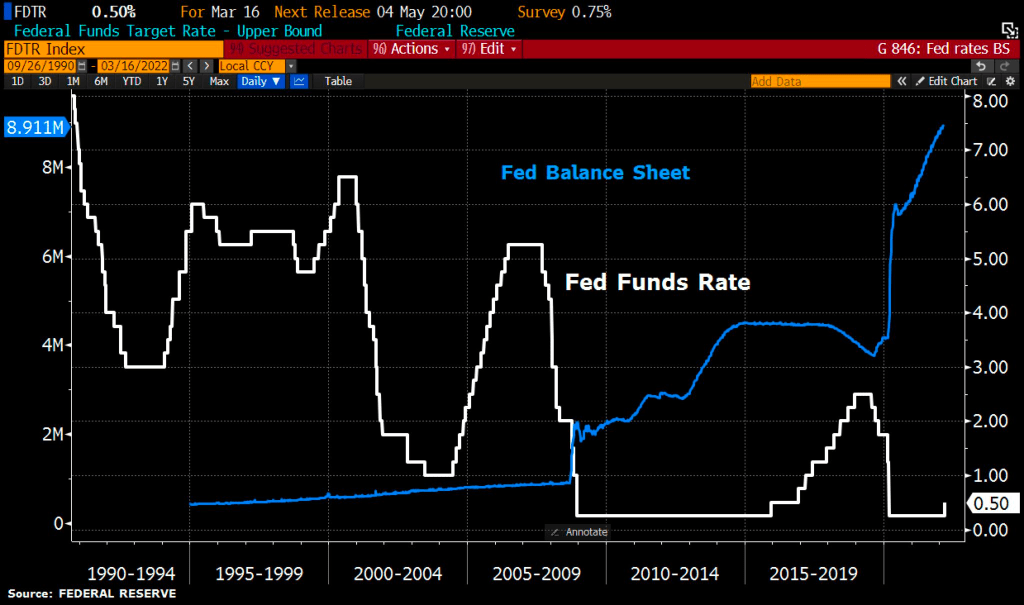

So, The Federal Reserve raised their target rate by … as expected … 25 basis points to 50 basis points.

The Taylor Rule suggests that the target rate should be 11.96%. So, Powell and The Gang are getting closer! /sarc

The short-term reaction to the measly rate increase? The Dow declined (but still in positive territory for the day) and the benchmark 10-year Treasury yield spiked to 2.23%.

On Powell’s surrender to inflation, the US Treasury 10Y-2Y curve continued to flatten.

You can see The Fed’s sloth-like response to blood-curdling inflation in the lower right-hand part of the chart.

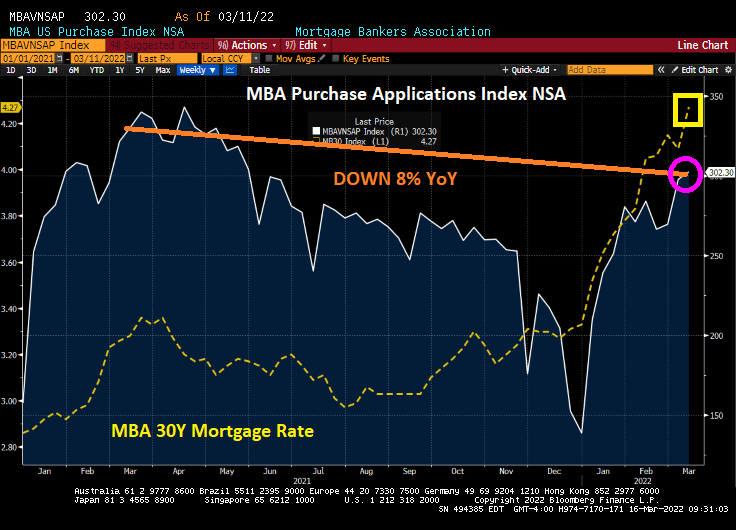

Mortgage applications decreased 1.2 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending March 11, 2022.

The seasonally adjusted Purchase Index increased 1 percent from one week earlier. The unadjusted Purchase Index increased 2 percent compared with the previous week and was 8 percent lower than the same week one year ago.

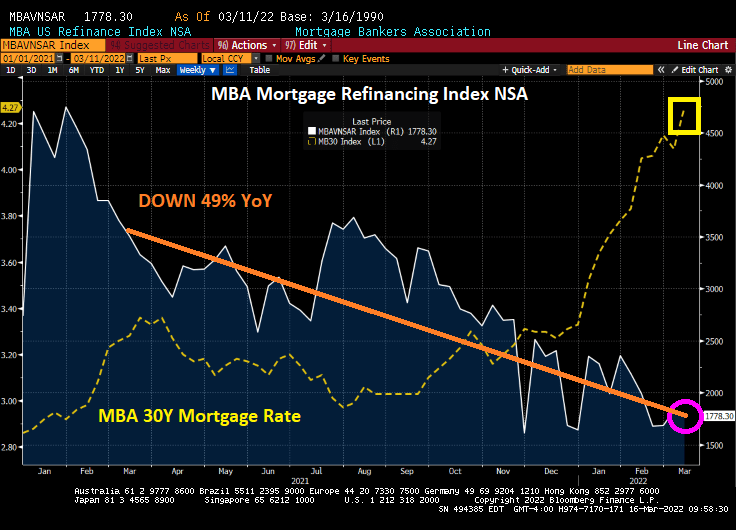

The Refinance Index decreased 3 percent from the previous week and was 49 percent lower than the same week one year ago.

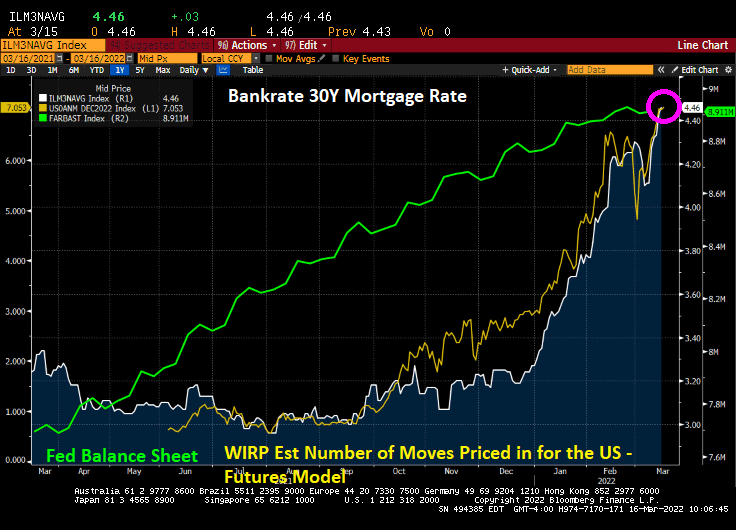

Bankrate’s 30-year mortgage rate has surged to 4.46%.

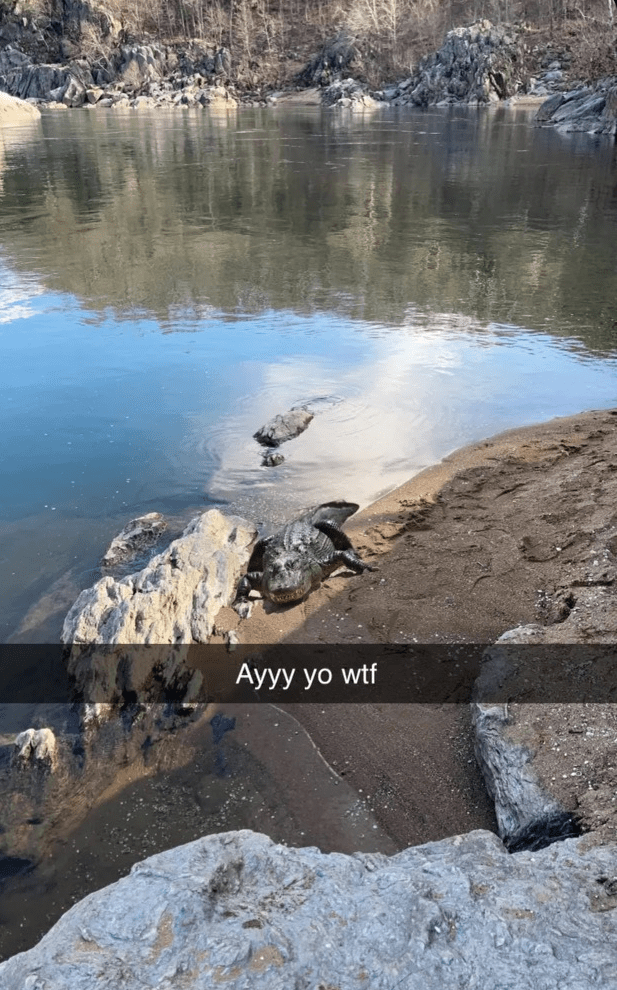

Here is a photo of alligators in Great Falls, Virginia, up-river from Washington DC. They are likely congregating for the Fed Open Market Committee (FOMC) announcement today.

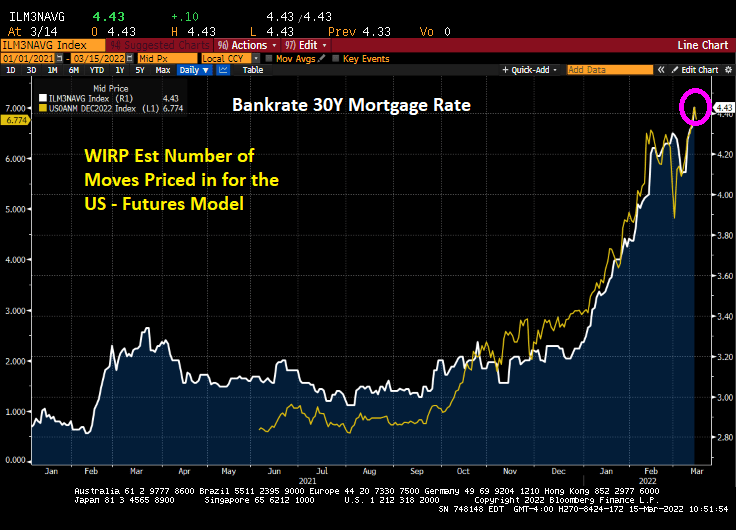

Bankrate’s 30-year mortgage rate rose to 4.43%, up 55% under Biden/Pelosi/Schumer’s reign of error. Thanks to the rising Fed rate hikes priced-in the market.

The US Producer Price Index (PPI) final demand rose 10% YoY in February, further evidence of spiraling inflation under Biden/Pelosi/Schumer’s reign of error.

And speaking of Senate Majority Leader Chuck Schumer (D-NY), the Empire State Manufacturing Survey (General Business Conditions) crashed to -11.8.

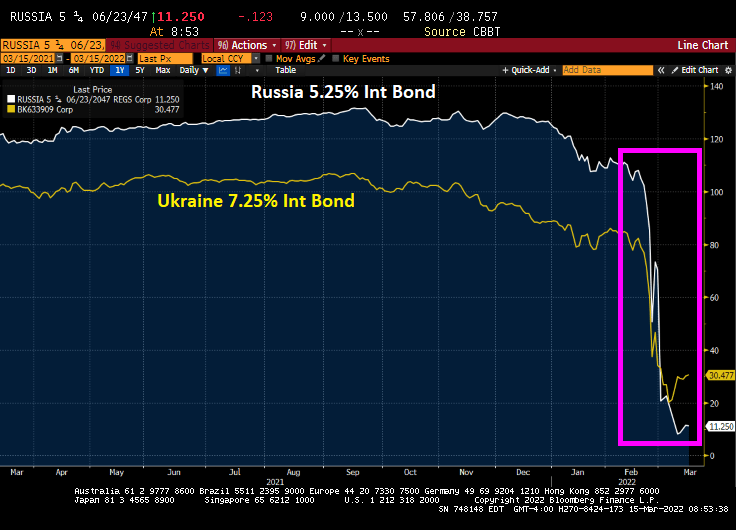

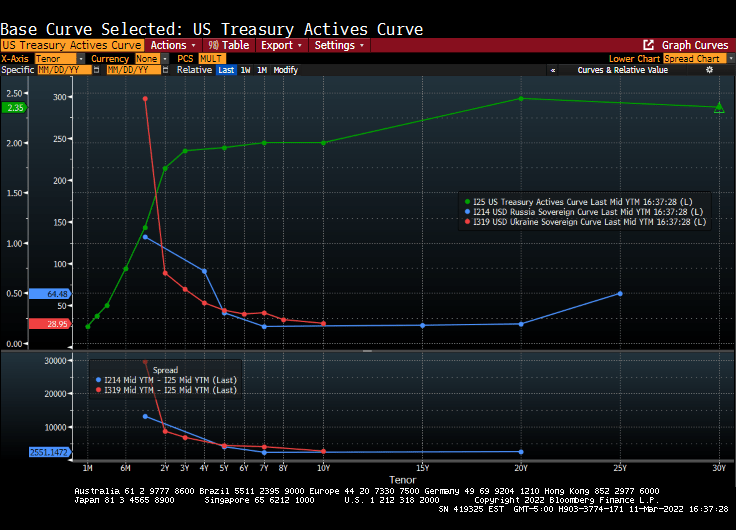

And Russia is losing the economic demolition derby with Ukraine (at least for sovereign debt).

I am still trying to figure out what House Speaker Nancy Pelosi (D-San Francisco) meant by “When we’re having this discussion, it’s important to dispel some of those who say, well it’s the government spending. No, it isn’t. The government spending is doing the exact reverse, reducing the national debt. It is not inflationary.”

Really Nancy?

Here is a chart of Federal government outlays and inflation. Massive expenditures and growth in Federal debt and the resulting inflation. Nancy?

Yes, it is the much anticipated Fed Week! The Fed Open Market Committee (FOMC) will announce it decision (probably the first rate hike under Biden of 25 basis points).

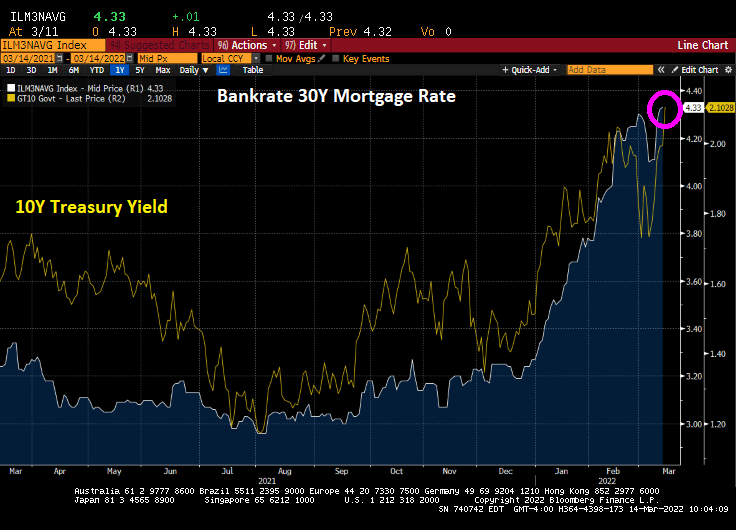

This morning, the 10-year Treasury yield rose by 11.1 basis points and the Bankrate 30Y mortgage rate rose to 4.33%.

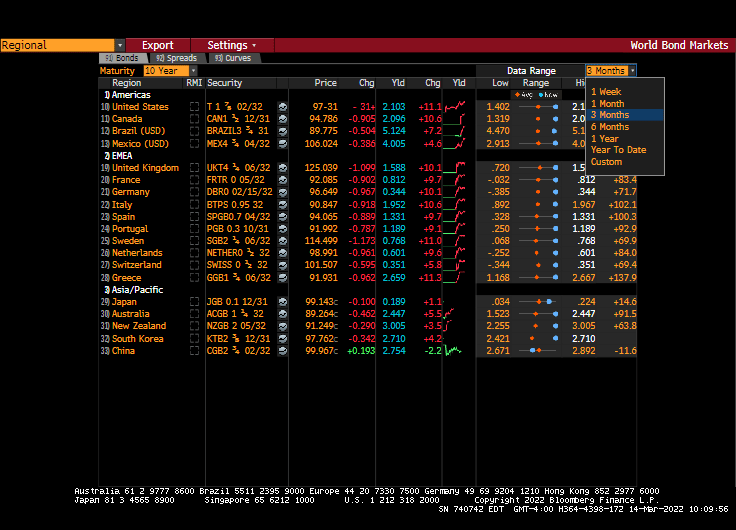

Actually, sovereign yields are up around 10 basis points in the US, Canada, and across the pond.

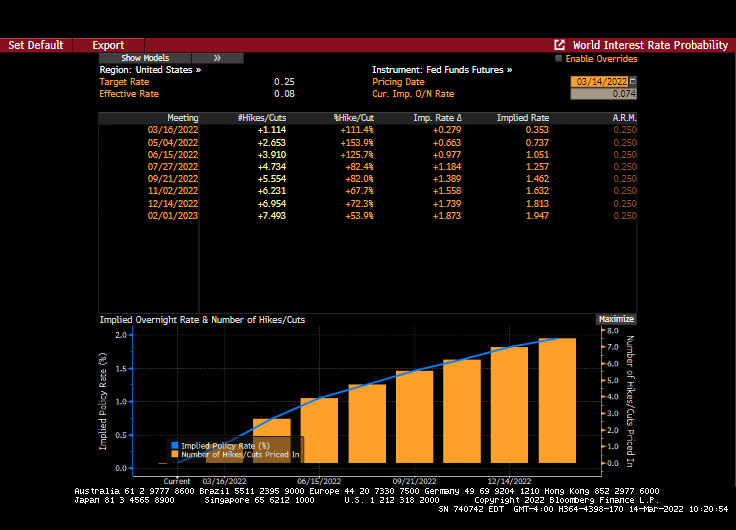

Fed Funds Futures are pointing to 7 rate hikes over the next year with 1.114 rate hikes on Wednesday. That means The FOMC may raise rates MORE than the 25 basis points expected my many (including me).

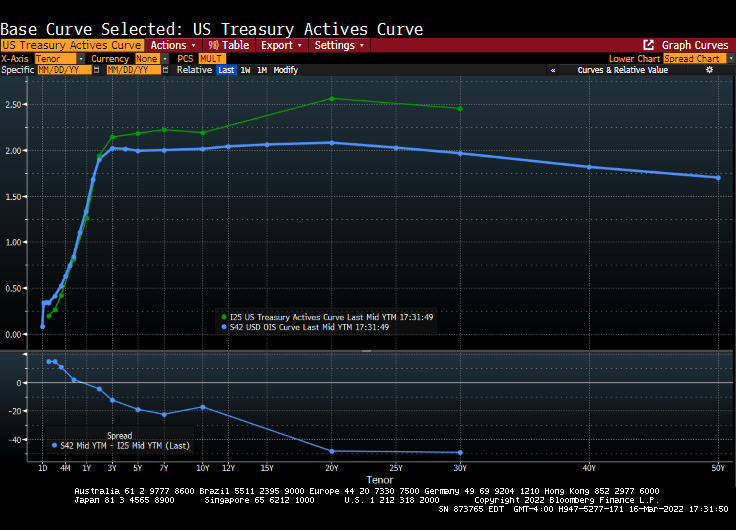

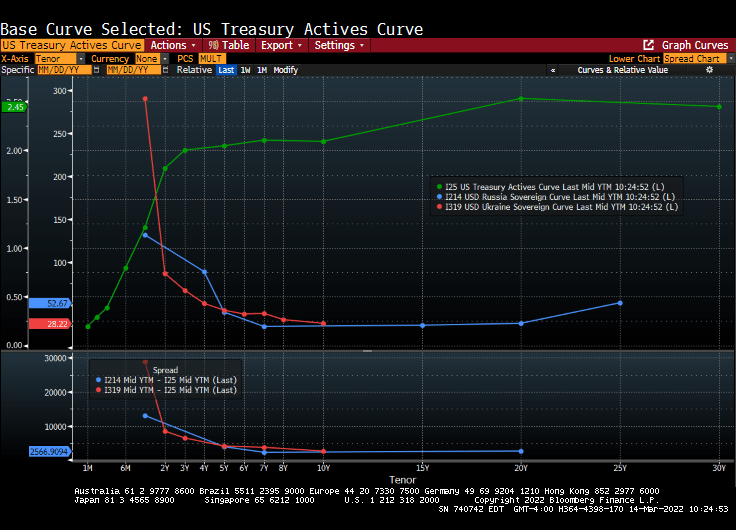

The US Treasury actives curve remains steeply upward sloping while both the Russian and Ukraine sovereign curves are steeply inverted and crashing.

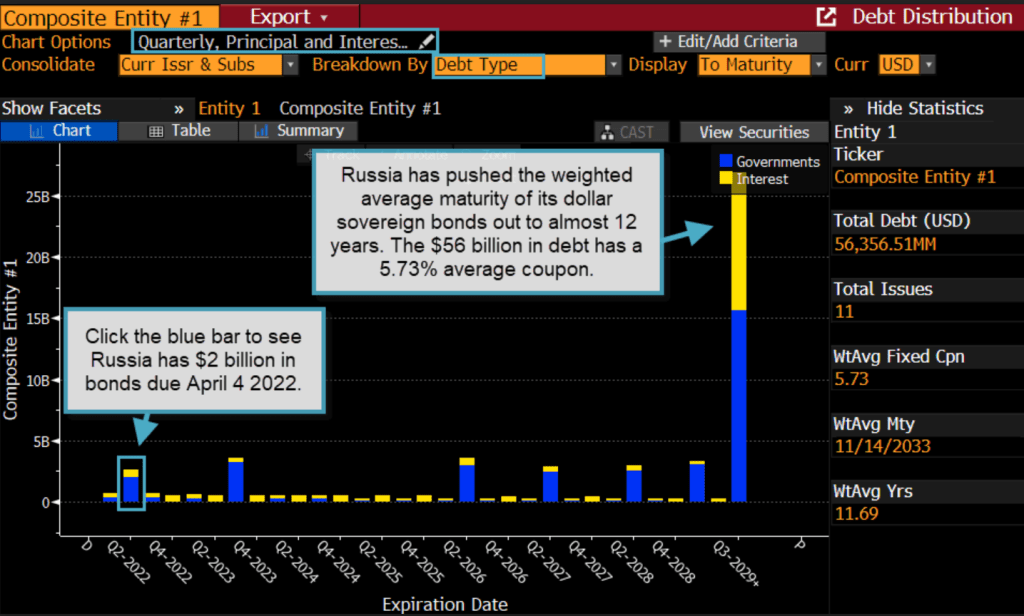

Russia has pushed the weighted average maturity of its dollar sovereign bonds out to almost 12 years.

The most hilarious headline of the day is a Bloomberg opinion piece: “Fighting Inflation May Require the Fed to Be Brutal: Clive Crook” How about the Biden Administration relaxing oil drilling and pipeline restraints? Otherwise, brutal translates into causing a recession. Great suggestion, Clive! … NOT!

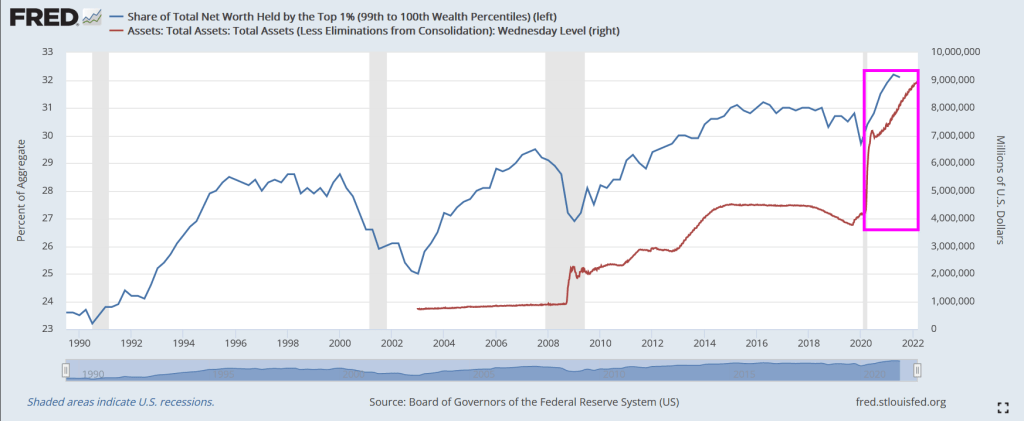

Following the financial crisis of 2008/2009, The Federal Reserve began their dramatic purchase of assets such as Treasuries and Agency mortgage-backed securities (AgencyMBS). And then Covid struck and The Fed went berserk with asset purchases.

So, who benefited the most? The top 1% or the bottom 50%?

Answer? The top 1%. The share of total net worth spiked dramatically after the Fed infusion.

Even the bottom 50% benefited with The Fed’s Covid stimylpto, but no where near how the top 1% benefited.

World Economic Forum’s elitist Klaus Schwab approves of this message!

On an unrelated note, the US Treasury yield curve is strongly UPWARD sloping, while Russia’s and Ukraine’s yield curves are inverted and collapsing.

You must be logged in to post a comment.