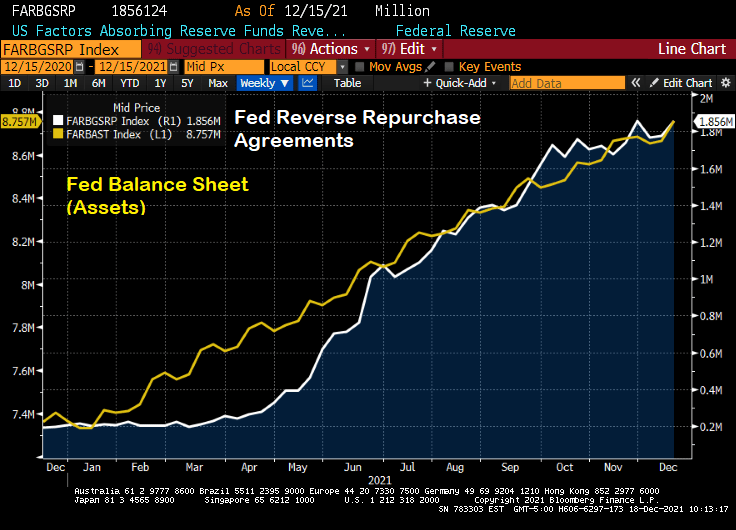

I love listening to Fed talking heads (or Fear The Talking Fed). They mostly seem to acknowledge that inflation is a problem and that the excessive monetary stimulus should be reduced.

But then I see the chart of The Fed’s balance sheet and The Fed’s reverse repo operations.

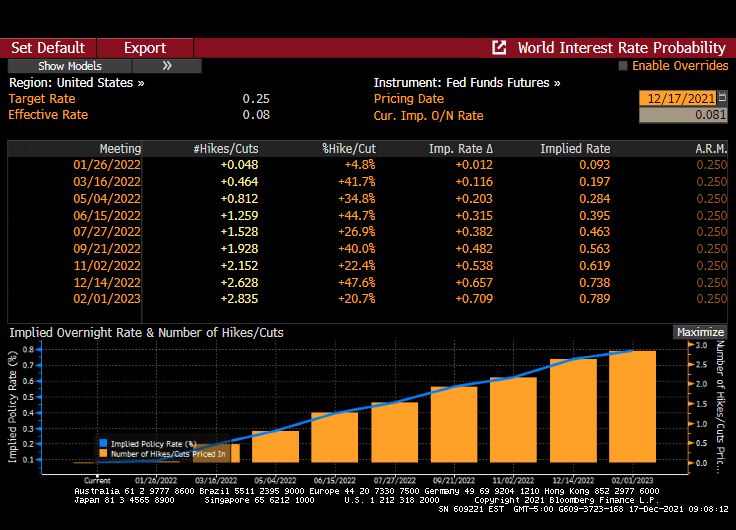

Then we have Federal Reserve Governor Christopher Waller saying that Th Fed could start raising interest rates as early as its March 15-16 meeting, after deciding to end asset purchases sooner than planned. My question is … why wait until the March meeting?

Is it fear of the Omincron Variant (which sounds like a Frederick Forsyth thriller)? Does The Fed not want to rock the boat prior to the Christmas season? The US is at or near full employment, so what is the real reason for delaying a rate increase until March or June? Or the fear that Congress won’t pass Biden’s Build Back Better Act?

Fed Funds Futures infer that one rate hike will occur at the June Fed Open Market Committee (FOMC) meeting and one at the November meeting.

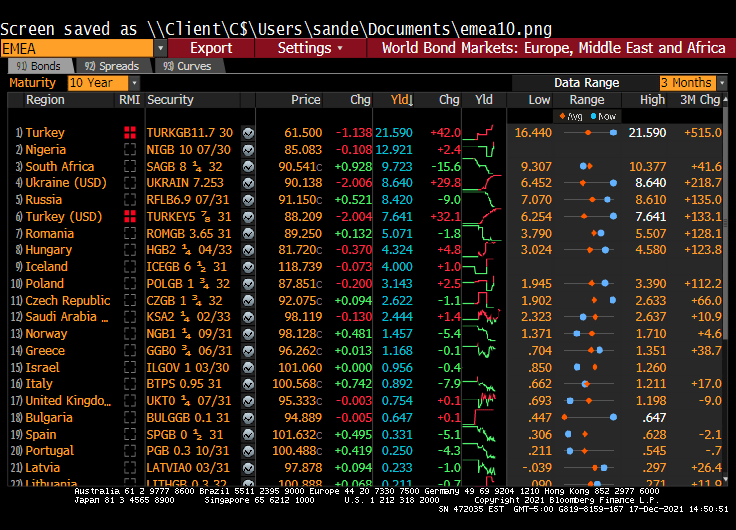

Turkey (the nation, not the bird) is now the Venezuela of Europe/Middle East, where insane government policies are destroying both nations.

(Dow Jones) — Turkey’s central bank intervened to arrest the plunge in the country’s currency, which lost as much as 8% of its value against the dollar on Friday in an ongoing crisis that is straining the country’s financial system.

The crash followed another decision by the central bank on Thursday to cut interest rates under pressure from President Recep Tayyip Erdogan, who favors lower rates as a part of a vision to grow the Turkish economy. Mainstream economists have urged the government to raise interest rates to control Turkey’s rising inflation, which reached more than 21% last month, according to official statistics.

The ongoing plunge is putting increasing pressure on ordinary Turks who have seen their savings evaporate, and adding to pressure on the banking system which has high levels of foreign-currency-denominated loans to repay within the next 12 months.

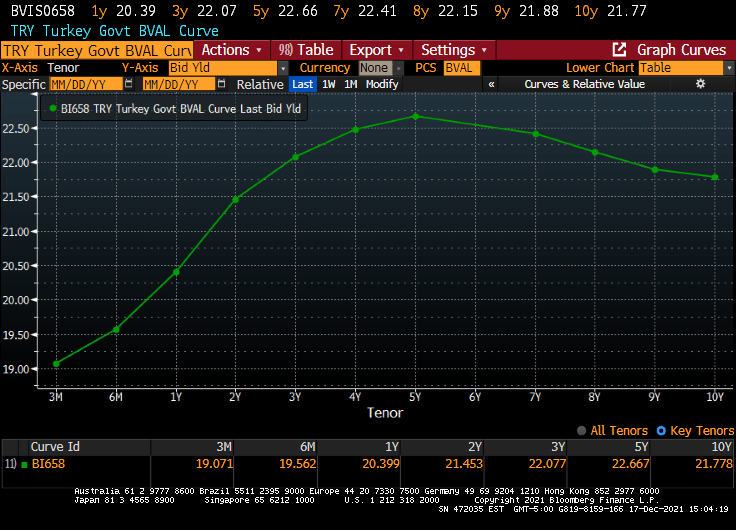

Wow. Turkey’s 10-year sovereign yield rose 42 BPS today to 21.590%. Turkey is looking like the Venezuela of Europe and the Middle East.

The Turkish sovereign curve in their home currency is humped.

But the Turkish yield curve (in US Dollars) looks more like the US Treasury actives curve.

The Turkish Lira is crashing against the US Dollar.

Meanwhile, the Central Bank of Turkey is cutting their repo rate as inflation soars. WTF???

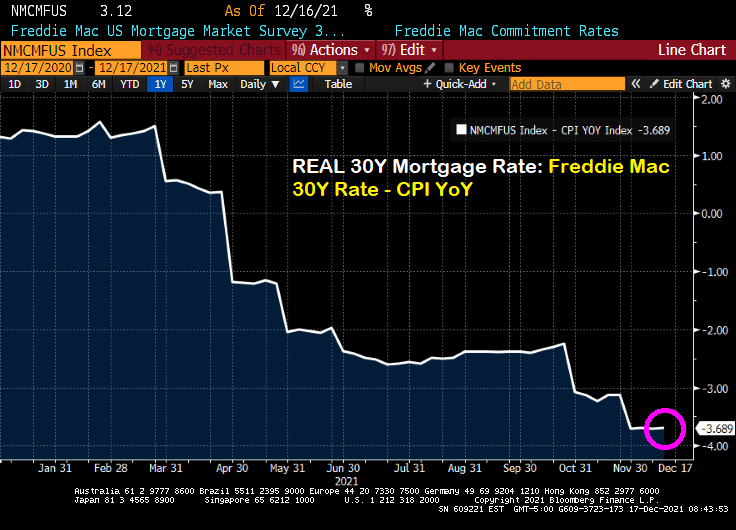

The Freddie Mac 30-year mortgage commitment rate rose to 3.12%. But once we subtract the gut-wrenching inflation rate, the REAL 30-year mortgage rate is -3.689%.

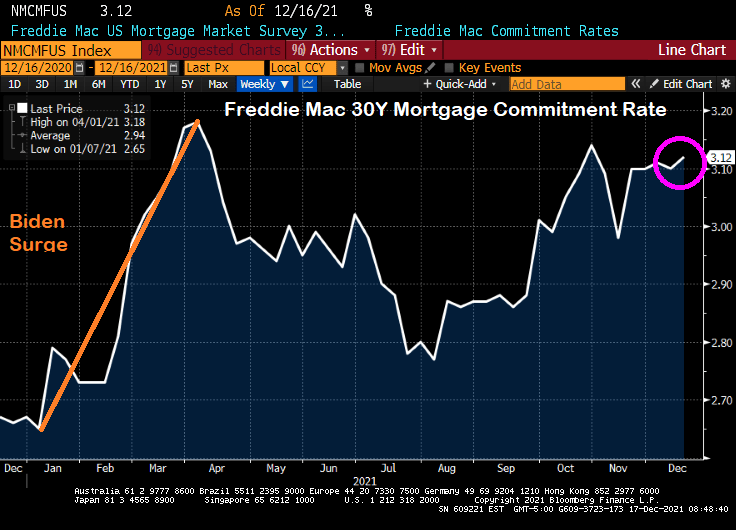

The nominal Freddie Mac 30-year commitment rate rose to 3.12% which is still lower than 3.18% back on April 1, 2021 after surge in rates following Biden’s taking the office of Presidency in January.

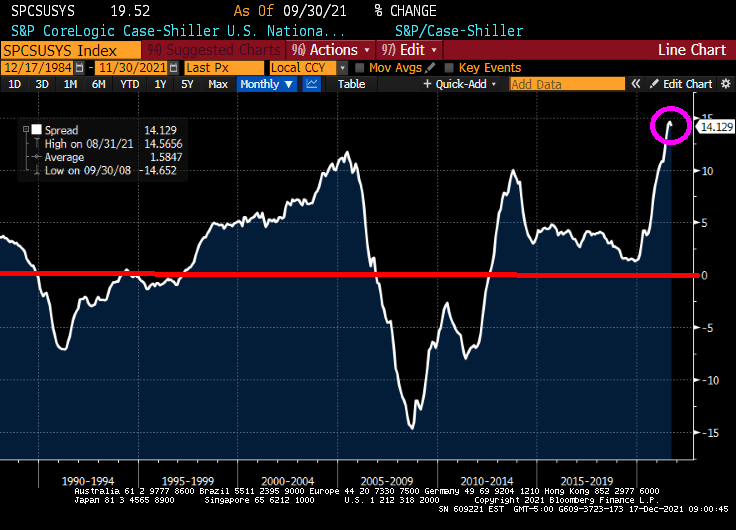

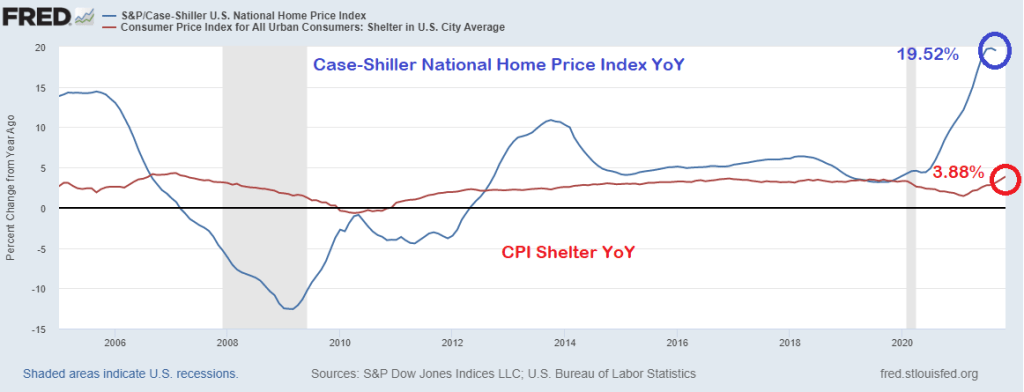

Meanwhile, the REAL Case-Shiller National home price index (CS National YoY – CPI YoY) is growing at the fastest rate in history. Great if you already own a home, but lethal if you are renting and want to move to homeownership.

Meanwhile, REAL wage growth is at -1.94% YoY.

Well, Chairman Powell and The Gang failed to raise the Fed Funds Target Rate yet again, but let us know that they will tighten someday soon. The Fed Funds Futures are signalling a rate hike at the June 2022 meeting and another at the November meeting.

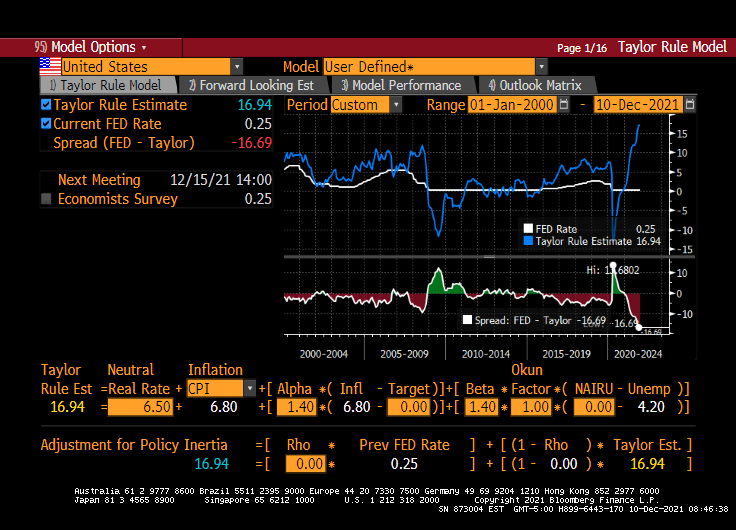

While The Fed couldn’t care less about the Taylor Rule, it is still interesting to note just how out of touch The Fed FOMC is with reality. The Taylor Rule indicates that their target rate should be 16.94% rather than the current target rate of 0.25%.

Keeping the target rate unchanged in the face of gut-wrenching inflation is a bold strategy, Cotton.

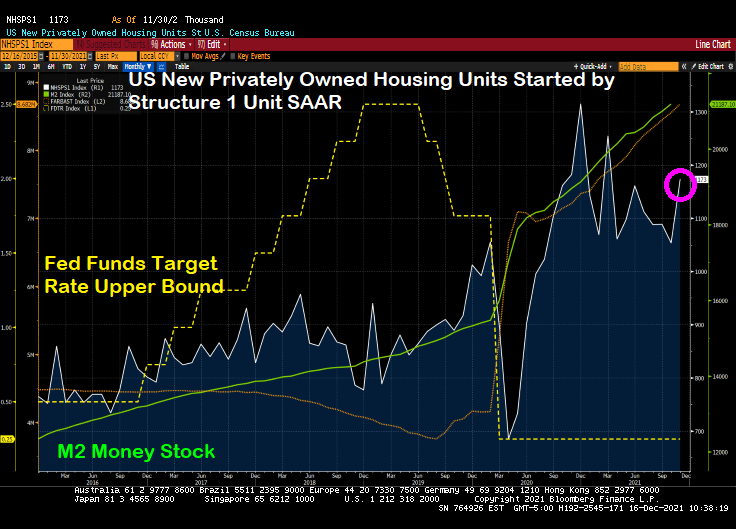

The Federal Reserve’s massive stimulus combined with Federal spending has led to US housing starts rising 11.8% in November. Housing starts remain elevated compared to pre-COVID levels.

1-unit starts rose 11.29% while 5+ (multifamily) starts rose 12.1% in November. All areas in the US saw growth except for the Midwest where starts fell by 7.27%.

Yes, with Powell leaving rates untouched … again … in The Fed’s effort to … not scare markets. Inflation be damned. Powell is the God of Hellfire!

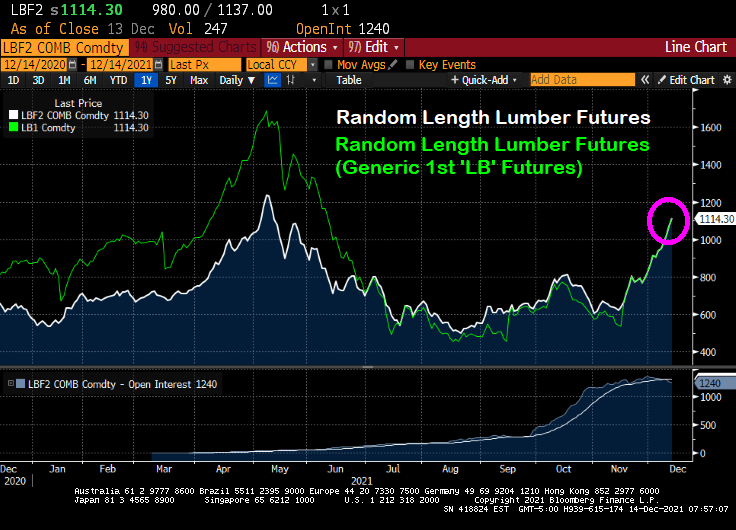

According to Markets Insider, lumber prices are up 127% from its most recent low. With demand high and supplies low, record low interest rates still drive homeowners to the market, so much that builders are struggling to keep up.

Note the surge in lumber futures prices back in April and May 2021 that eased. But lumber futures prices are gaining steam again.

Let’s see what happens to lumber prices and new home prices if and when The Federal Reserve decides to takes its gargantuan foot off the monetary accelerator pedal.

In other housing-related news, China’s Evergrande remains in the news as its stock price founders.

Inflation-adjusted return of Treasuries fell to lowest since the 1980s. For bond investors, this is their version of Kevin’s Famous Chili from The Office! Or The Fed’s Famous Chili!

(Bloomberg) — Treasury investors are losing more money than they have in four decades, once inflation is taken into account. And if markets are right, they’re unlikely to come out ahead for years.

The federal government’s debt has already lost about 2% outright over the past year as the Federal Reserve started removing pandemic-era stimulus from the economy and inched closer toward raising interest rates. But on top of that, the consumer price index has surged 6.8%, putting investors even deeper in the hole.

Taken together, that’s resulting in the worst real returns — or those adjusted for inflation — since the early 1980s, when then Fed Chair Paul Volcker was in the midst of fighting a wage-price spiral. What’s more, the dynamic isn’t expected to change: The bond market is projecting that 10-year Treasury yields will hold below the inflation rate for the next decade, meaning any investment income will be more than wiped out by the rising cost of living.

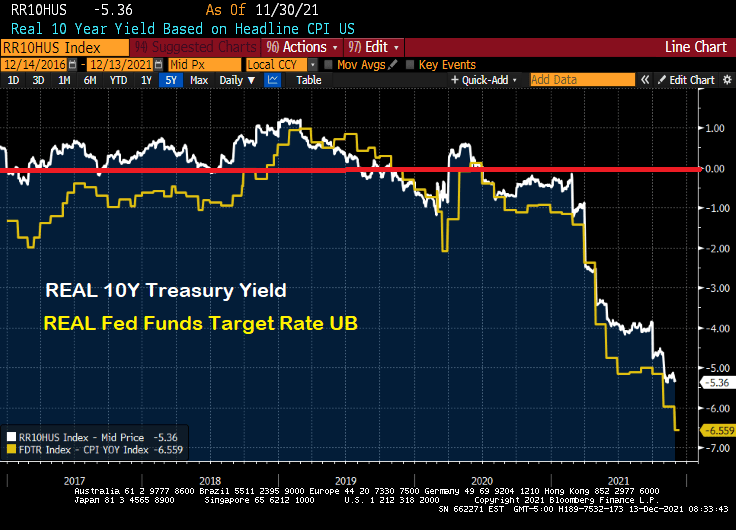

If we look at the REAL 10-year Treasury yield and REAL Fed Funds Target Rate, they are both negative.

Let’s see if Powell spills his famous chili on Wednesday at 2:00PM EST. The Fed keeps saying they are serious about controlling inflation, just like Kevin Malone.

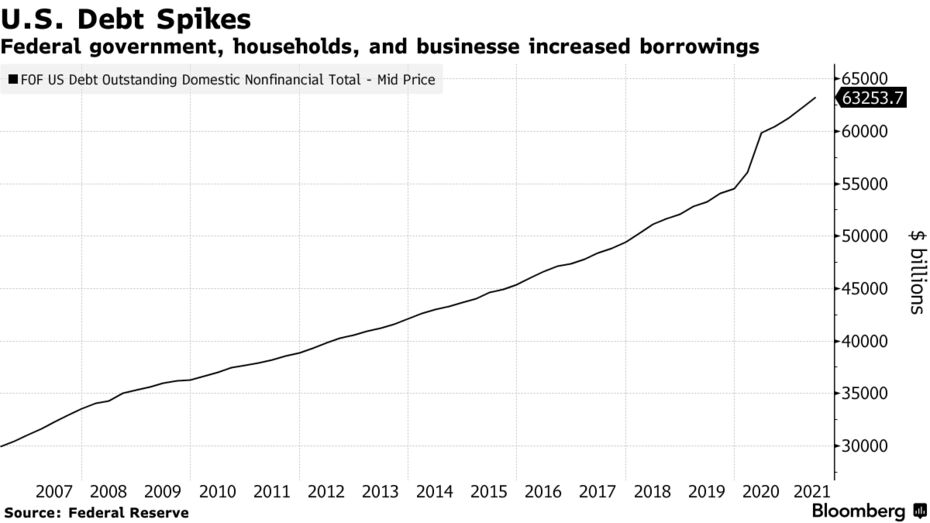

The U.S. went on a borrowing binge last year and the hangover could make it harder for the Federal Reserve to fight inflation without crashing the economy.

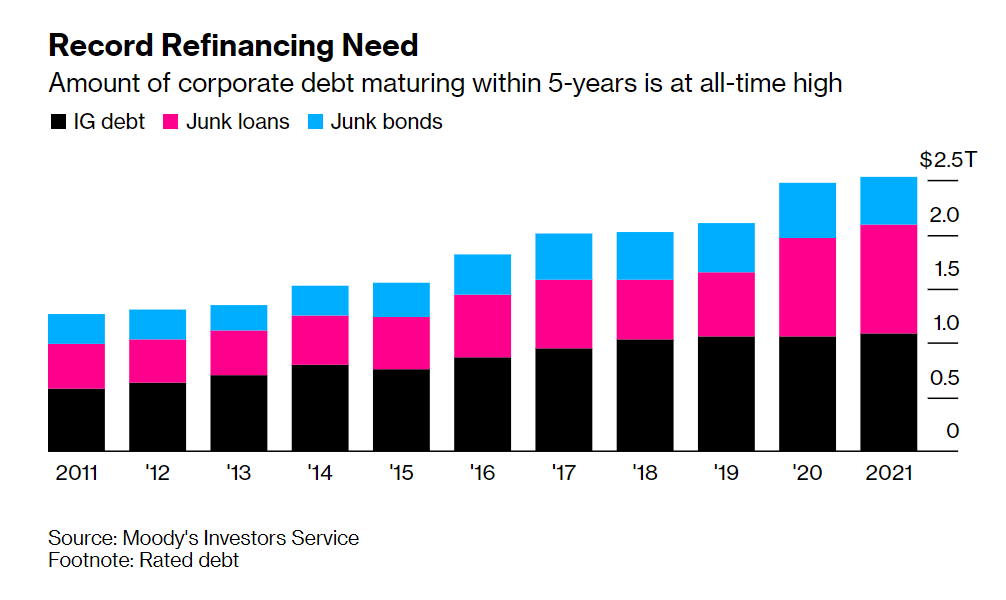

Corporate debt has surged $1.3 trillion since the start of 2020 as borrowers took advantage of emergency Fed action as the pandemic spread, slashing interest rates and backstopping financial markets to keep credit flowing. More debt held by more companies suggests potential risks as borrowing costs rise from currently low levels.

That could create financial stability concerns for Fed Chair Jerome Powell and his colleagues as they debate removing pandemic support in the face of what a report Friday showed were the hottest price rises in almost 40 years. And a tough task: Not since Alan Greenspan’s time has the U.S. central bank tried to navigate the economy back to price stability from too-high inflation.

Powell’s challenge is to try to curb price pressures without large costs to employment or growth, a move that would likely anger both political parties and blotch his record with the first Fed-assisted hard landing since the 1990-1991 downturn.”

The Fed’s Financial Stability Report on Nov. 2 noted that key measures of vulnerability from business debt, including leverage and interest cover ratios, were back at pre-pandemic levels.

To be sure, big firms that used the opportunity to issue longer-dated bonds at lower rates have strengthened their balance sheets.

Source: Moody’s Investors Service

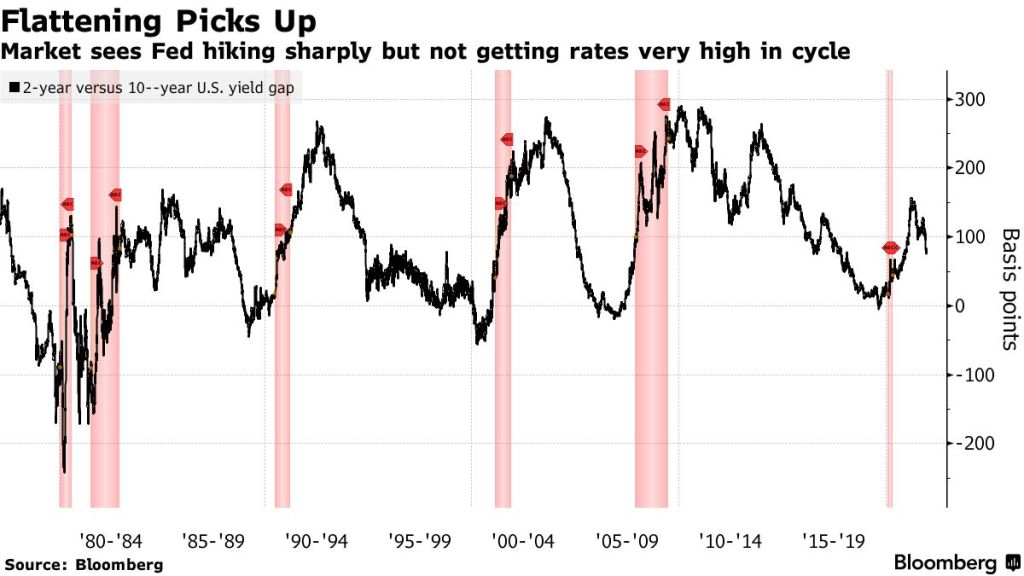

The Federal Reserve is laying the groundwork for the start of a cycle of interest-rate hikes that the bond market warns might be unusually constrained in how far it can go, setting the two on a collision course where one will eventually have to give.

The Treasuries yield curve — or the spread between short-term and long-term interest rates — looks set to be the flattest at the beginning of a Fed tightening cycle in a generation if the central bank begins raising its benchmark overnight rate in mid-2022 as now forecast. The two-year, 10-year spread is about 83 basis points, with futures indicating 55 basis points in June.

The problem facing Powell and The Fed is that they are stuck in a trap. They can’t raise their target rate more than just a little (say 50 basis points) and shrinking their enormous balance sheet is really their only option. And that may fail if the 10 year Treasury yield starts to rise too rapidly or gets too high.

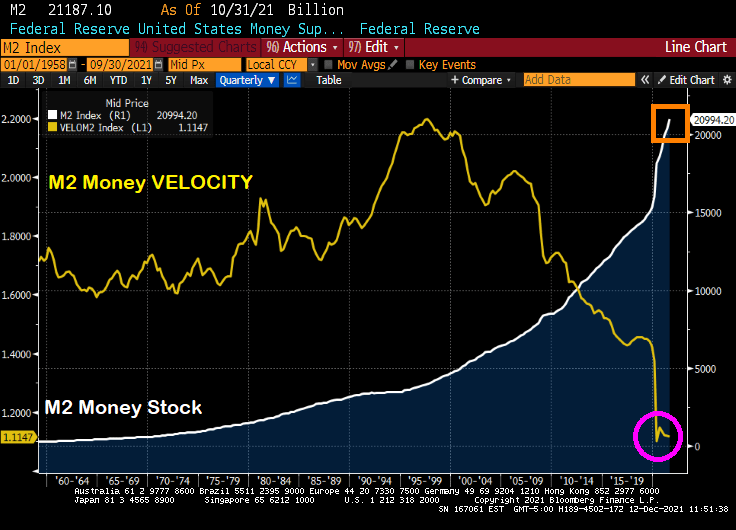

Here is one of the traps facing Powell and the Gang after their Covid printing splurge: dying M2 Money Velocity.

It will only get worse as Congress and the Biden Administration keep spending like drunken ORCs from Lord of the Rings. Particularly when the Penn-Wharton Budget Model finds that Build Back Better will reduce the long-term GDP by 2.8 percent, reduce wages by 1.5 percent, and reduce work hours by 1.3 percent. The only thing it will expand is government debt, by 25 percent.

The Washington DC spending Gollums need to control their urges.

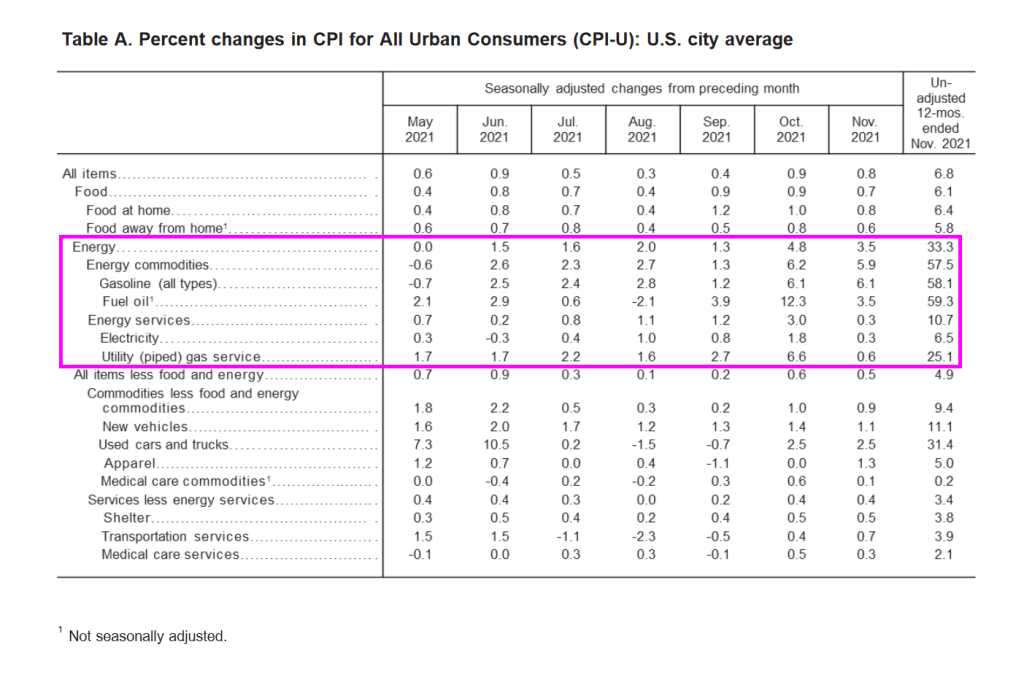

But that 6.9% YoY is very misleading because of the strange way the Bureau of Labor Statistics measures the largest asset in most households’ expenditures: housing.

The BLS measures inflation in housing using the Shelter measurement. Which was only 3.88% YoY. The problem is that the Case-Shiller National Home Price Index was 19.52% in its last reading. That is quite a discrepancy.

So, if we substitute the Case-Shiller National home price index for the CPI Shelter, we get an inflation rate of greater than 11%.

The U.S. is poised to enter Year Three of the pandemic with both a booming economy and a still-mutating virus. But for Washington and Wall Street, one Covid aftershock is starting to eclipse almost everything else.

Already-hot inflation is forecast to climb even further when November data comes out on Friday, to 6.8%. That would be the highest rate since Jimmy Carter was president in the early 1980s — and in the lifetimes of most Americans.

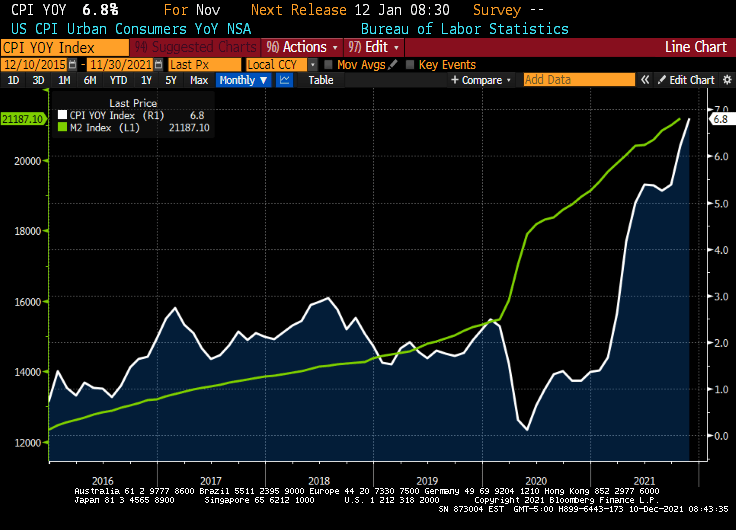

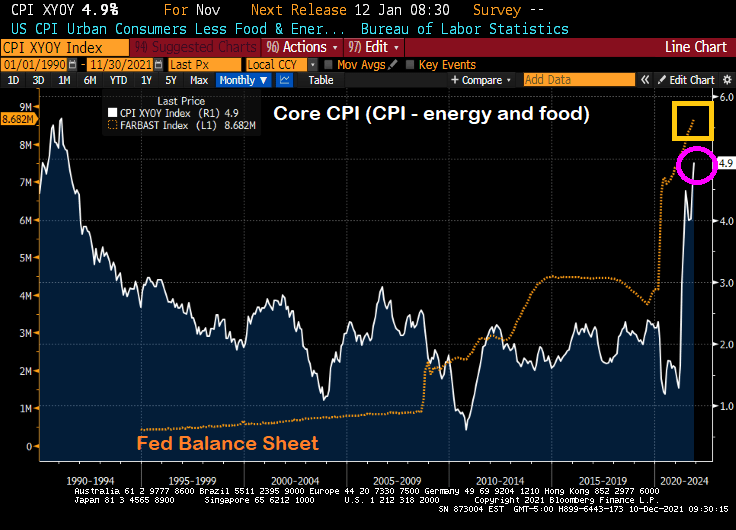

And the CPI change since last year, according to the Federal Reserve of St Louis FRED is a staggering 16.262%.

And with U.S. Jobless Claims plunge to 52-year low, its about time that The Fed begins removing the humongous monetary stimulus.

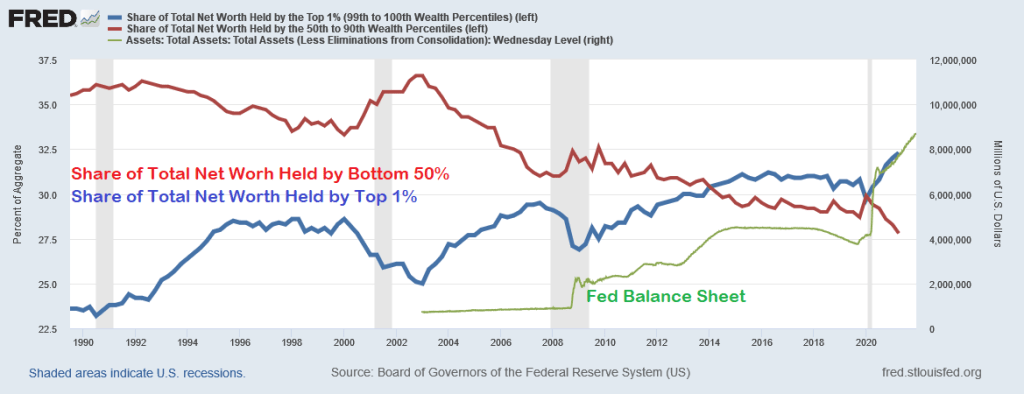

After all, largely thanks to Federal Reserve policies, we have seen the greatest wealth redistribution in US history … to the top 1%.

You must be logged in to post a comment.