Yes, its a cold one out there. But the Biden Administration is engaging in reducing fossil fuel supply and pushing towards “green” energy such as inefficient solar panels, eagle-killing wind turbines, and ocean turbines.

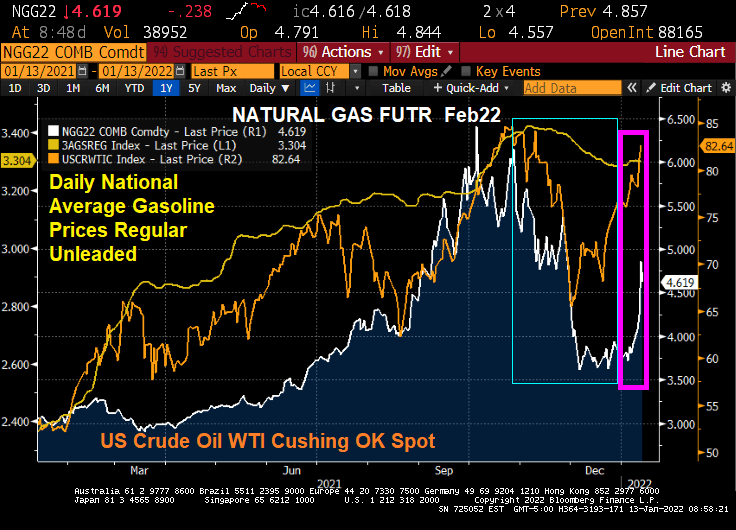

As a consequence, natural gas futures are up 93% from January 1, 2021 while coal futures are up 133% and WTI Crude spot price is up 82%.

Any wonder why food prices are up 40%?

Stay warm. It’s a cold one out there today. And The Federal government doesn’t care.

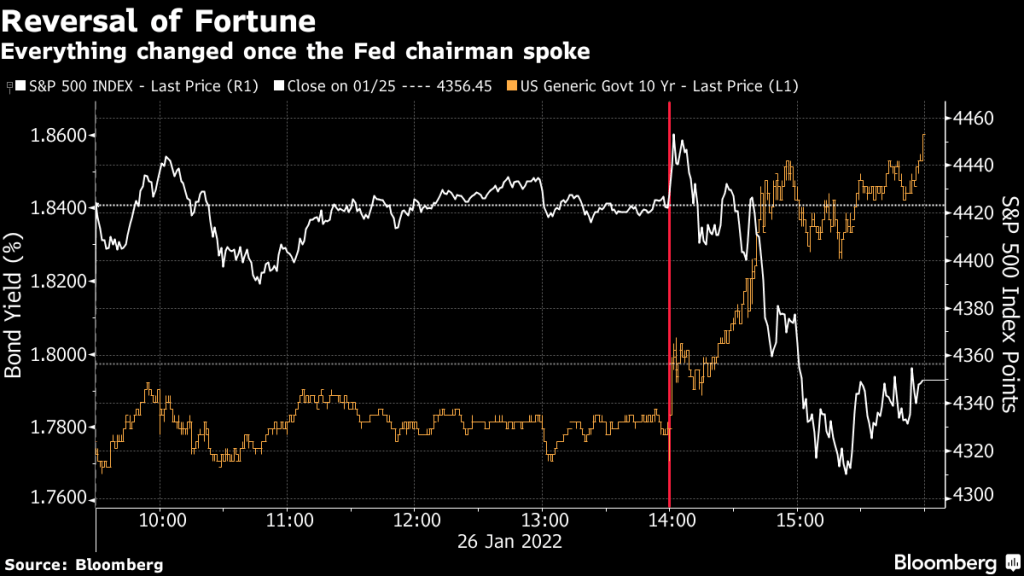

No, not the Klaus von Bulow type of “reversal of fortune” (when he killed his wife). I am talking about a reversal in fortune for America.

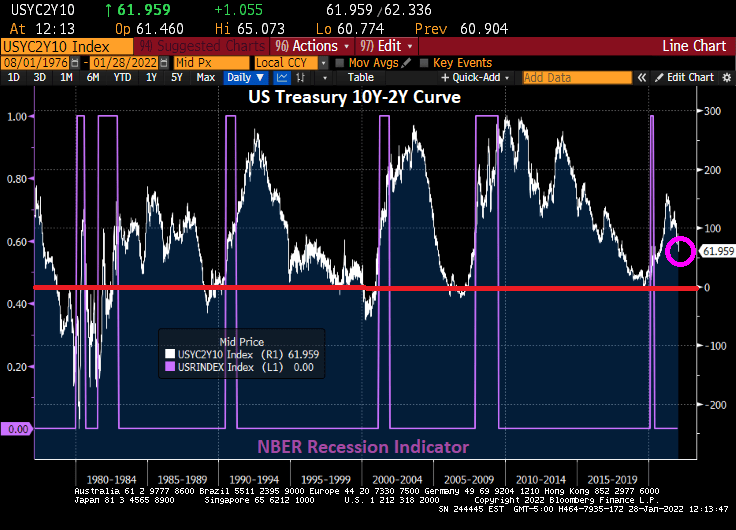

Let’s look at the 10Y-2Y Treasury curve. It typically falls below 0 basis points before every recession. Except the mini-COVID recession of 2020. But notice that the Treasury curve did not recover from the COVID recession as it typically did. More along the lines of 1984-1985.

Speaking of Reversal of Fortune, everything changed once Fed Chair Powell started to speak after Tuesday’s FOMC meeting.

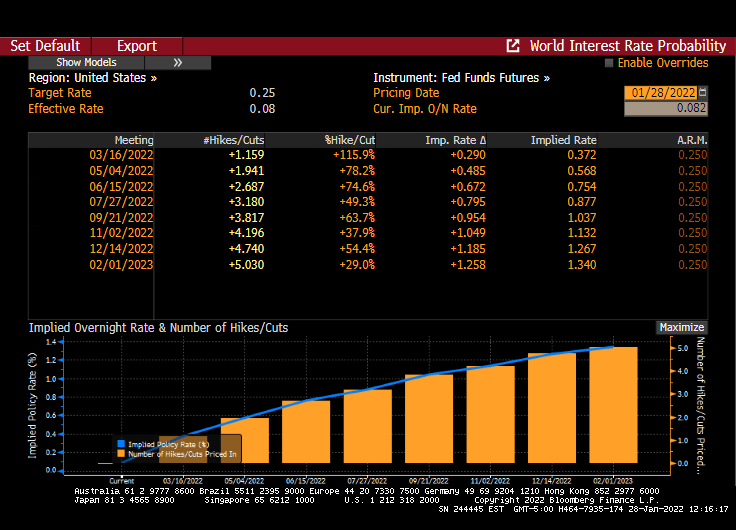

Hmm. Midterm elections, possible Russian invasion of The Ukraine, further problems in China, etc. While The Fed Funds Future data implies that The Fed may raise their target rate 5 times over the coming year, we’ll see.

If 2021 was a great year for the US housing market, 2022 faces “a new normal” marked by a slowing down of home price rises, job layoffs in the mortgage industry, and concerns over rising inflation and interest rate hikes, according to Douglas Duncan (pictured), Fannie Mae’s senior vice president and chief economist.

Duncan said “a shift” was underway in the market and the wider economy, which would result in far more moderate home price appreciation, expected to be between 7% and 7.5% this year due to the ending of fiscal and monetary stimulus.

“One of the elements of the shift is that you’re going to see house prices up, but not nearly as far as they were in the last two years because that was driven hugely by the fiscal and monetary stimulus (now) being removed,” he told MPA.

Ominously, he added that low interest rates “may never be seen again”. Or at least until Biden appoints more doves to The Federal Reserve Board of Governors.

Here is a lesson in Bidenomics. “Going Green” sounds great to some (like Al Gore, Leonardo DiCaprio and Greta Thunberg), but there are costs to not growing America’s energy supply.

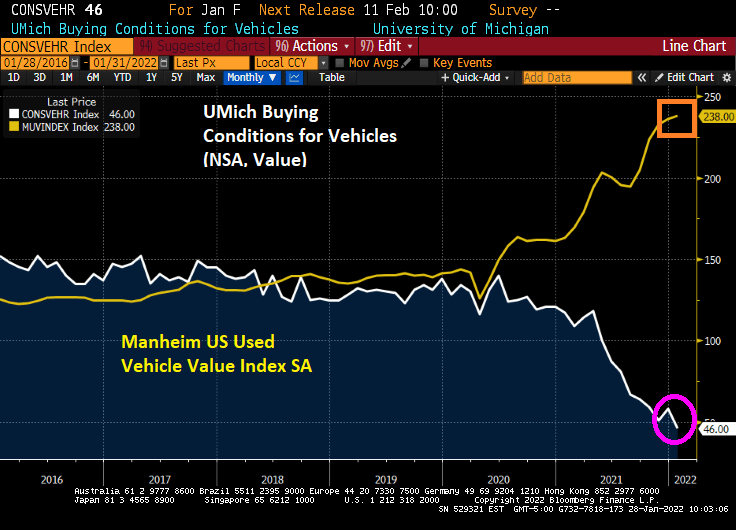

Rising energy costs have helped create the rise in consumer prices and inflation. Not to mention chip shortages for car and trucks. The University of Michigan conditions for vehicles plummeted to 46 (100 baseline) as used vehicles prices sky rocket.

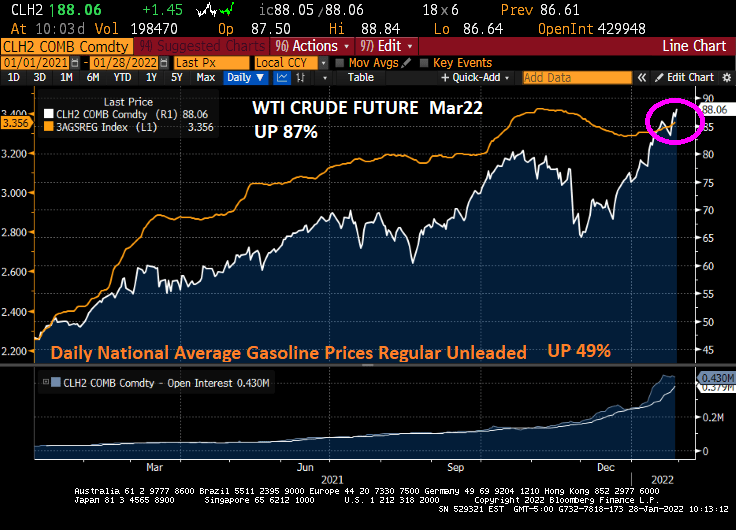

Under Biden’s reign of error, West Texas Crude futures prices have risen 87% (regular gas prices are up 49% even with Biden’s releasing two days of supply from the Strategic Petroleum Reserve.

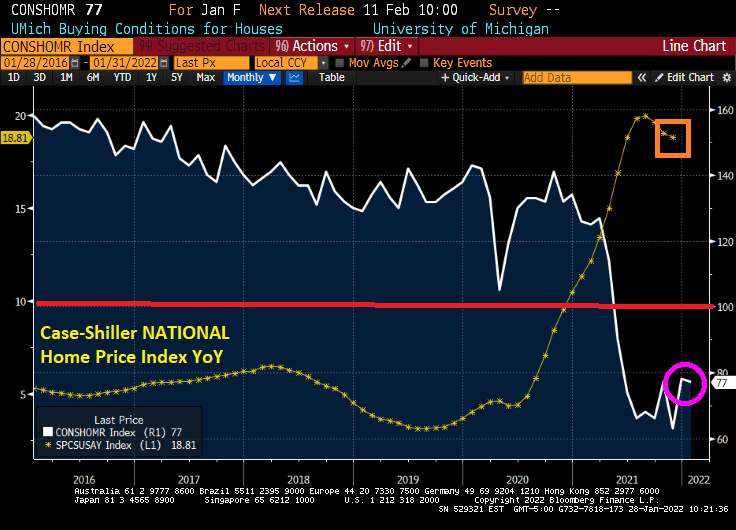

On the housing front, the University of Michigan buying conditions for houses fell to 72 (baseline of 100) as home prices are roaring at a 18.81% YoY clip.

To paraphrase the comic strip “Gasoline Alley,” “Unca’ Joe, what have your done t’ US?”

This is a case of “Too much money” in the economy, courtesy of The Federal Reserve.

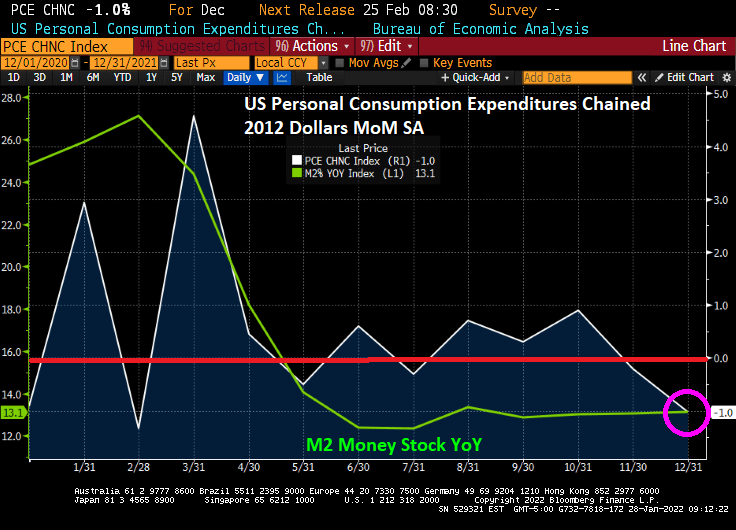

(Bloomberg) — U.S. inflation-adjusted consumer spending fell last month by the most since February, suggesting that Americans tempered their outlays amid the latest Covid-19 wave and the fastest inflation in nearly 40 years.

Purchases of goods and services, adjusted for changes in prices, decreased 1% from November, the Commerce Department said Friday.

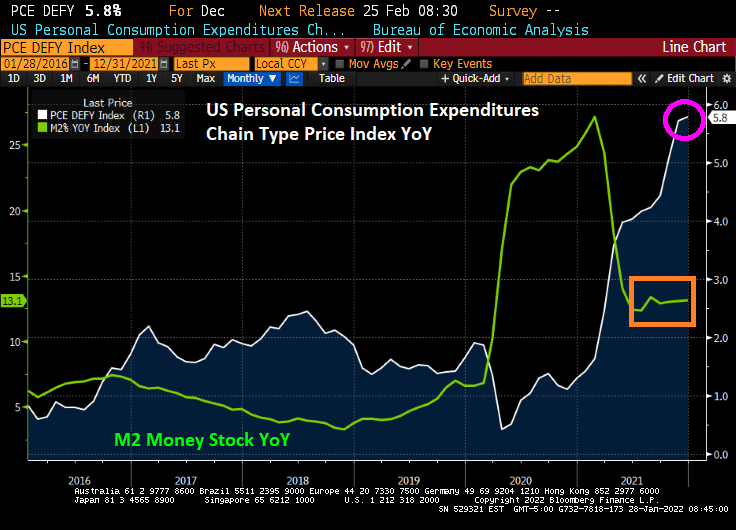

The personal consumption expenditures price gauge, which the Federal Reserve uses for its inflation target, rose 0.4% from a month earlier and 5.8% from December 2020, the most since 1982. Unadjusted for inflation, spending fell 0.6%, while incomes rose 0.3%.

Yes, the PCE Deflator YoY rose to 5.8% as M2 Money Stock is growing at a 13.1% YoY clip.

REAL personal spending declined 1% in December as prices rose in part thanks to the 13.1% growth in M2 Money stock YoY.

Too much money! Time to slow down, Jay Powell! Stop sucking the life out people with inflation.

COVID and its omicron variant (as well as government reactions such as mask and vaccination mandates) are wreaking havoc on the global economy, but particularly in the USA where the Federal government dumped trillions of dollars in fiscal stimulus along with The Federal Reserve’s monetary stimulus into an economy not prepared for it. The result? INFLATION.

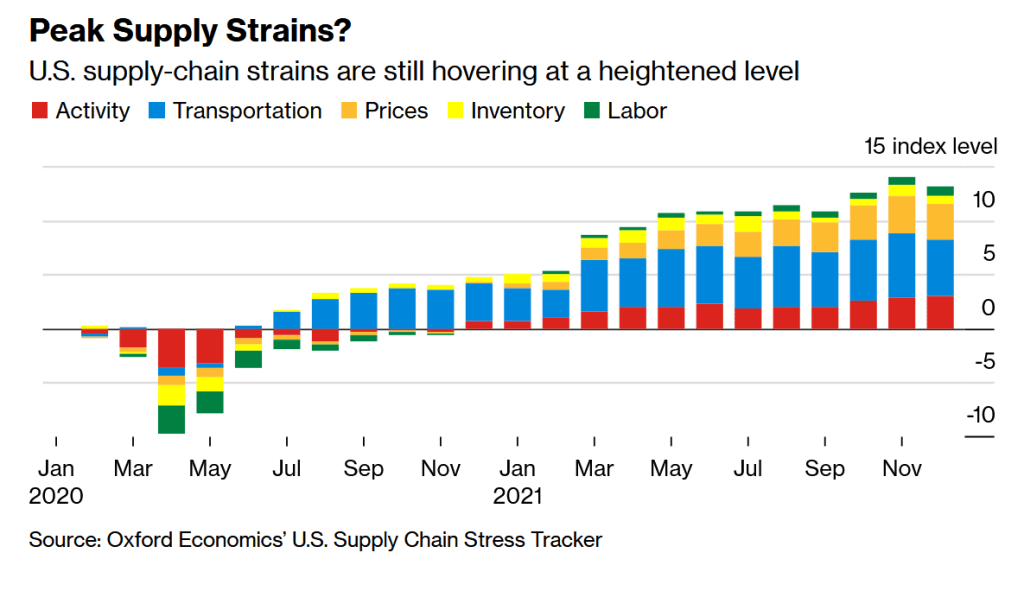

But global supply chains are nearing a turning point that’s set to help determine whether logistics headwinds abate soon or keep restraining the global economy and prop up inflation well into 2022, according to several new barometers of the strains.

Just a week before the start of Lunar New Year, the holiday celebrated in China and across Asia that coincides with a peak shipping season, economists from Wall Street to the U.S. central bank are unveiling a string of models in the hope of detecting the first signs of relief in global commerce.

From Europe to the U.S. and China, production and transportation have stayed bogged down in the early days of 2022 by labor and parts shortages, in part because of the fast-spreading omicron variant.

Among the big unknowns: whether solid demand from consumers and businesses will start to loosen up, allowing economies to finally see some easing in supply bottlenecks. Fresh indicators from the private and official sectors are in high demand because there’s still much uncertainty in industries overlooked by mainstream economics before the pandemic.

Once the realm of trade and industrial organization experts, supply chains “have shifted to center stage as a critical driver of sky-high inflation and a stumbling block to the recovery,” Bloomberg Chief Economist Tom Orlik said. “The profusion of new indices and trackers won’t unblock the arteries of the global economy any quicker. They should give policy makers and investors a better idea of how fast — or slowly — we are getting back to normal.”

The Bloomberg Economics Index

Bloomberg Economics’ latest supply constraint index for the U.S. shows that shortages have trended modestly lower for six months. Even so, strains remain elevated, and the wave of worker absenteeism is adding to the problems at the start of 2022.

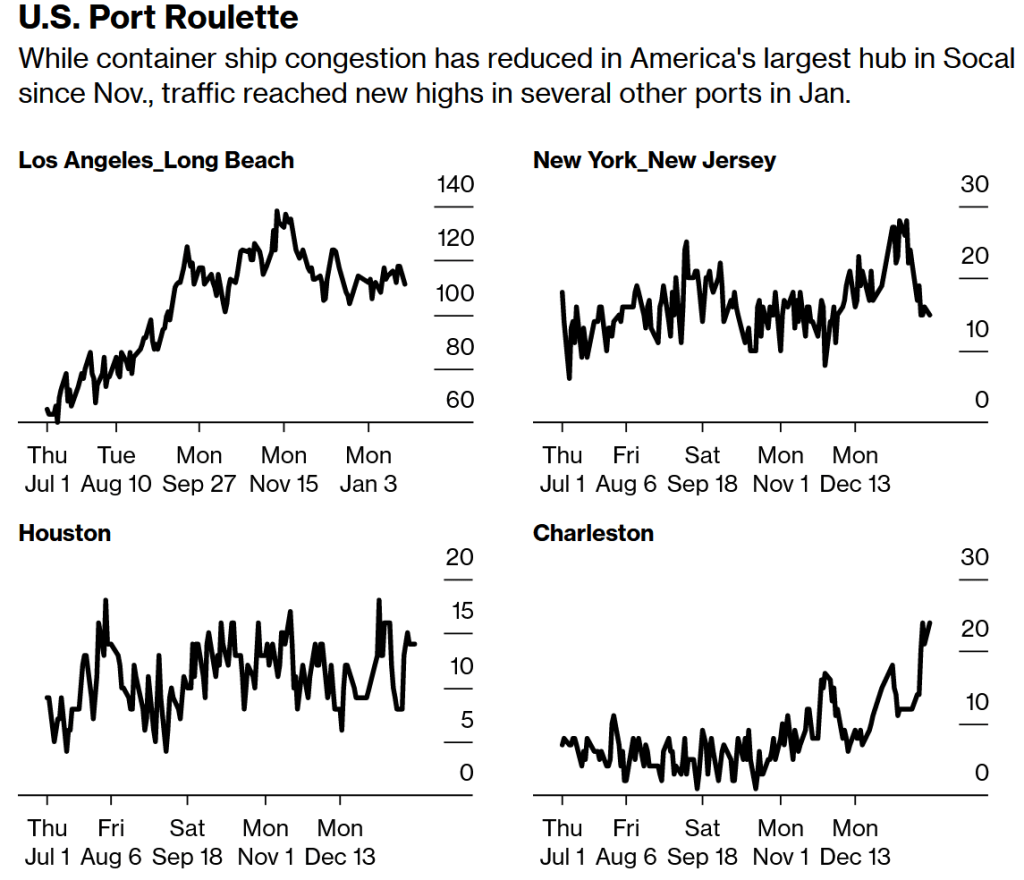

Port traffic tracked by Bloomberg shows container congestion continues to rankle the U.S. supply chain from Charleston, South Carolina, to the West Coast. The tally of ships queuing for the neighboring gateways of Los Angeles and Long Beach, California, continued to extend into Mexican waters, totaling 111 vessels late Sunday, nearly double the amount in July.

Source: Bloomberg, IHS Markit, Genscape

Note: Data counts the total number of container ships combined in port and in offshore anchorage area.

Kuehne+Nagel’s Disruption Indicator

Kuehne+Nagel International AG last week launched its Seaexplorer disruptionindicator, which the Swiss logistics company says aims to measure the efficiency of container shipping globally. It shows current disruptions at nine hot spots is hovering near “one of highest levels ever recorded,” with 80% of the problems happening at North American ports.

Flexport’s Guages

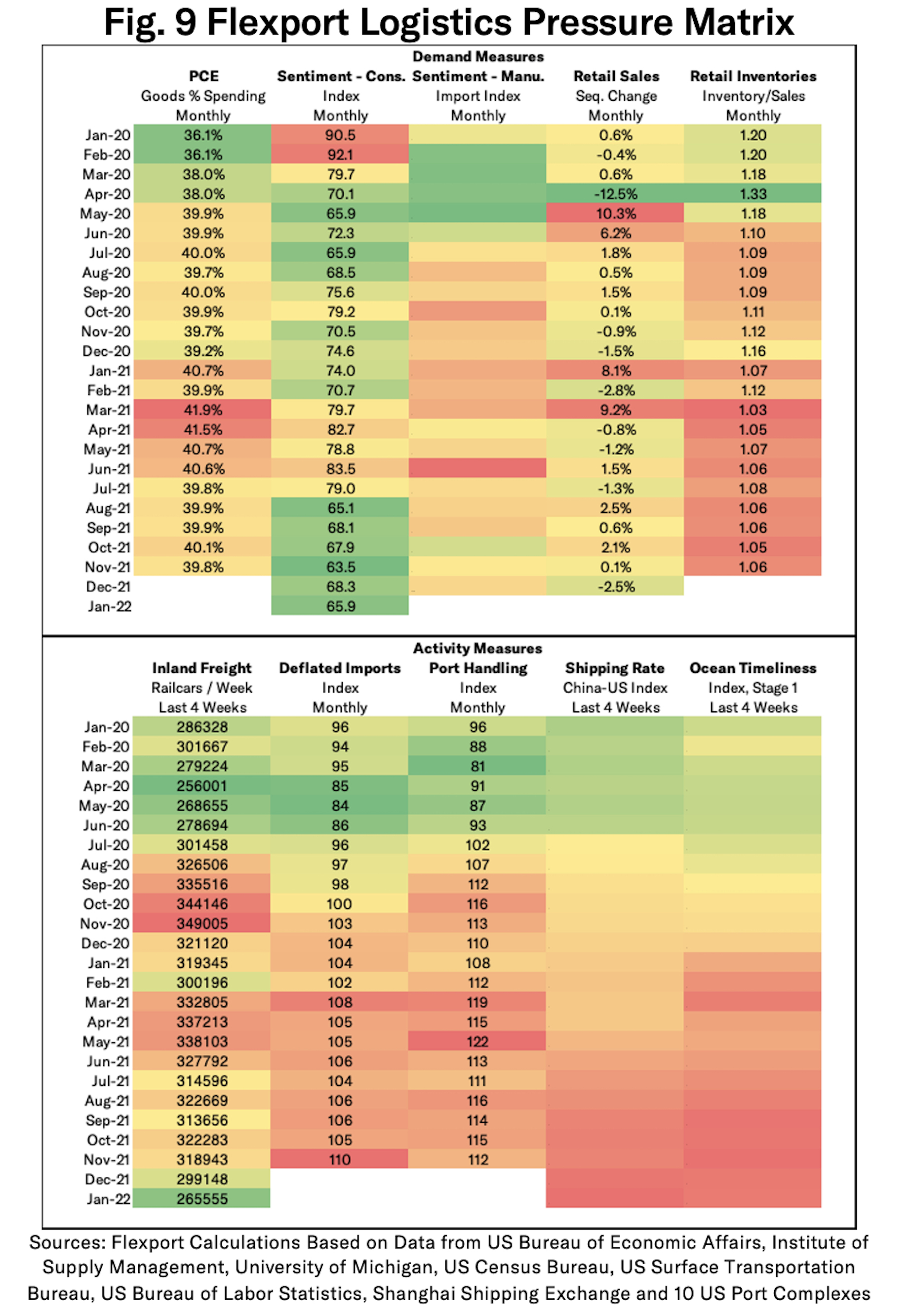

Another freight forwarder, San Francisco-based Flexport Inc., last year developed its Post-Covid Indicator to try to pinpoint the shift by American consumers back to purchasing more services and away from pandemic-fueled goods. The latest reading released Jan. 14 “indicates the preference for goods will likely remain elevated during the first quarter of 2022.”

Flexport has a new Logistics Pressure Matrix with a heat map showing demand and logistics trends, and much of those numbers are still flashing yellow or red. Flexport supply chain economist Chris Rogers said in a recent online post that similar grids for Asia and European markets will be part of the research.

The Federal Reserve’s Stress Monitor

Adding their stamp to the burgeoning genre of supply stress indicators were three Ph.D. economists from the Federal Reserve Bank of New York, with the launch its Global Supply Chain Pressure Index. Rolled out earlier this month, it shows that the difficulties, “while still historically high, have peaked and might start to moderate somewhat going forward.” The New York Fed said it plans a follow-up report to quantify the impact of shocks on producer and consumer price inflation.

Morgan Stanley’s Index

Less than a week later came the Morgan Stanley Supply Chain Index. It lined up with the Fed’s view that frictions have probably peaked, though some of improvement ahead will come from a slowdown in the demand for goods.

“Supply disruptions remain a constraint to global trade recovery, but as firms continue to make capacity adjustments to address them, capacity expansion could mitigate these,” Morgan Stanley economists wrote in a report Jan. 12.

Citigroup’s Tool

Citigroup Inc. last week released research that was less optimistic yet complementary to the New York Fed’s work, which Citi said doesn’t factor the role of surging demand as a contributor to the supply disruptions. Sponsored Content The Collaboration Disconnect Atlassian

Co-written by Citi’s global chief economist Nathan Sheets, a former U.S. Treasury undersecretary for international affairs, the bank’s analysis “gives a more complete, and intuitive, picture of the current situation.” While strains may ease in coming months, Citi said, “these supply-chain pressures are likely to be present through the end of 2022 and, probably, into 2023 as well.”

The Keil Institute’s Flows Tracker

In Germany, the Kiel Institute for the World Economy updates twice a month its Trade Indicator, which looks at flows across the U.S., China and Europe. Its latest reading Jan. 20 shows that along the key trading route between Europe and Asia, there are 15% fewer goods moving than there would be under normal times. The last time the gap was that large was in mid-2020, when many economies were reeling from initial lockdowns, Kiel said.

More recently, “the omicron outbreak in China and the Chinese government’s containment attempts through hard lockdowns and plant closures are likely to have a negative impact on Europe in the spring,” says Vincent Stamer, head of the Kiel Trade Indicator, said in a post last week. “This is also supported by the fact that the amount of global goods stuck on container ships recently increased again.”

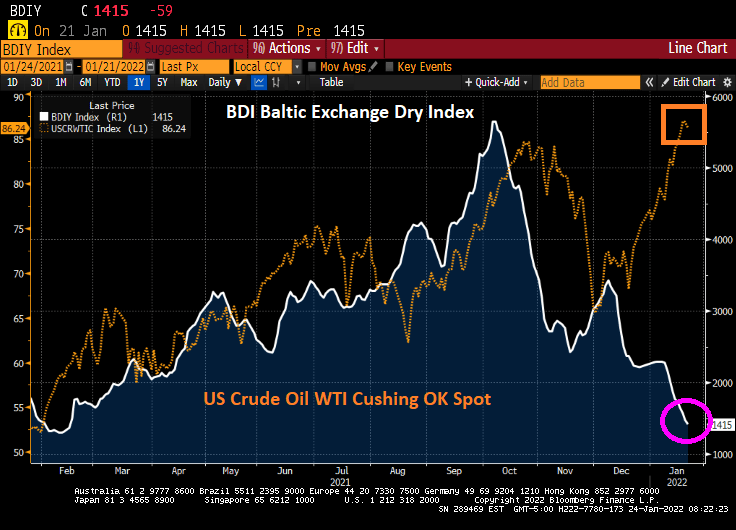

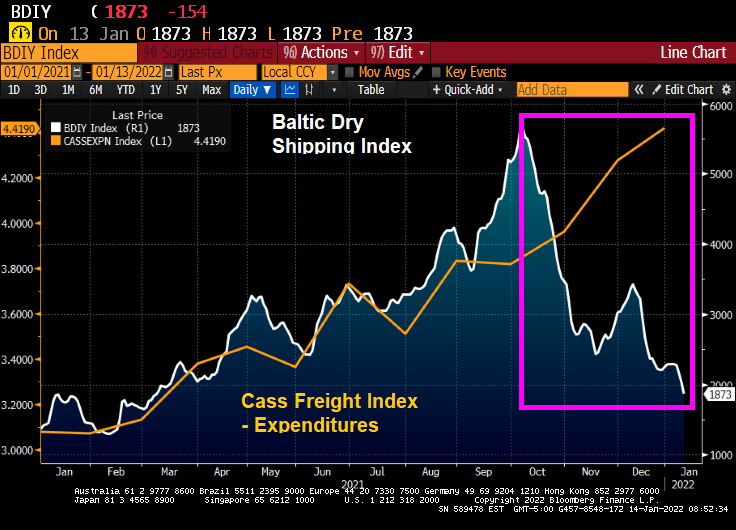

Baltic Dry Index

The Baltic Dry shipping cost index indicates that costs for shipping materials such as iron ore have decline to where it started under Biden, despite West Texas Crude Oil spot prices begin considerably higher thanks to Biden’s anti-fossil fuel policies.

So as the world comes out of Omicron (and whatever COVID variant rises to take its place), we should see a normalization in the supply chain. And with Intel building a new chip factory in New Albany Ohio (aka, outskirts of Columbus). the supply chain woes will eventually subside.

Then again, there is always the Russia-Ukraine tension that may erupt into a disaster. I suggest that President Biden sent Hunter Biden to Moscow to negotiate on behalf of The Ukraine.

Ever wonder why prices are rising so fast? One reason is that with rapidly rising energy prices under the Biden Administration, the costs are getting passed-through to consumers in the form of higher prices.

According to the Cass Corp Freight Index, the total spent in December on shipping goods to their customers in the US spiked by 43.6% from December 2020 to December 2021. Not surprising since energy prices over the past year have soared by almost 50%.

But at the same time, the Baltic Dry index (The Baltic Dry Index (BDI) is a shipping and trade index created by the London-based Baltic Exchange. It measures changes in the cost of transporting various raw materials, such as coal and steel) is crashing thanks to FEAR created by Omicron.

And yes, energy prices are surging again in 2022 after cooling off in Q4 2021.

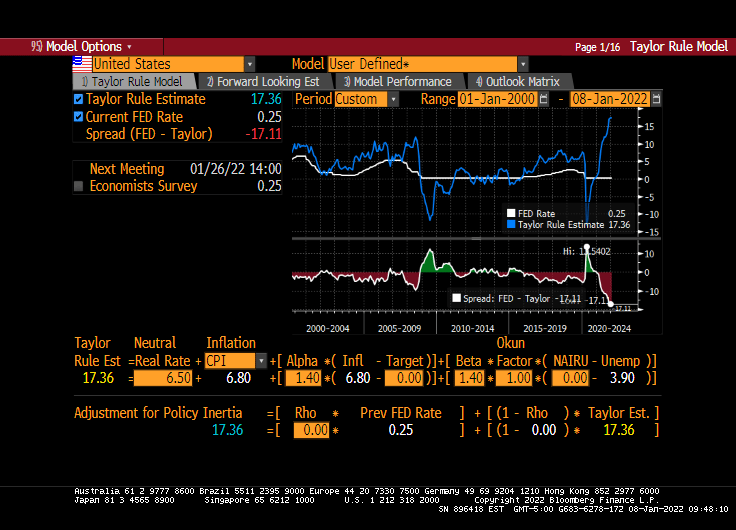

It is somewhat mystifying that markets would be soooooo sensitive to 3 rate increases from The Fed, particularly since the Taylor Rule suggests that The Fed’s target rate should be 17.36%. Even if you don’t like the Taylor Rule or disagree with its inputs, you must admit that the gap between where The Fed is (0.25%) and where they should be (17.36%) is … k-razy.

Housing in the US is getting “simply unaffordable.” And it has gotten far worse over the past year. Thanks to BAD government policies.

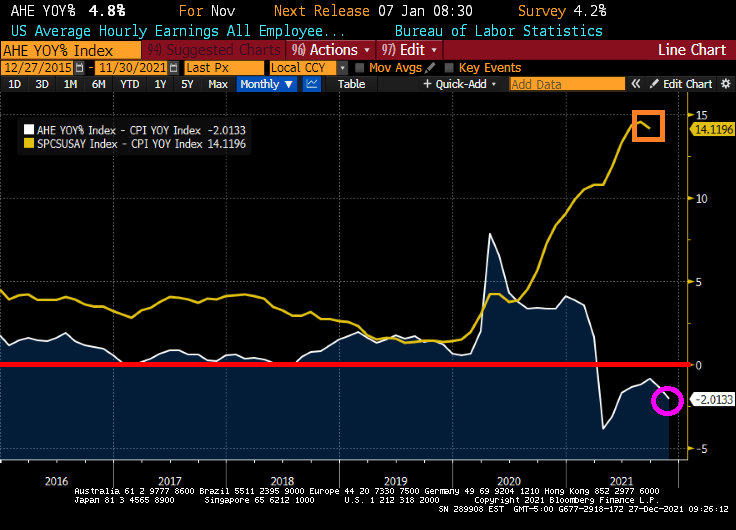

While wage growth is positive, inflation is sucking the life from consumers. REAL average hourly earnings growth is -2.0133%. Even worse, home prices are rising at a 14.12% pace in REAL terms. So, wages are losing to inflation and housing is pulling away from renters in terms of affordability.`

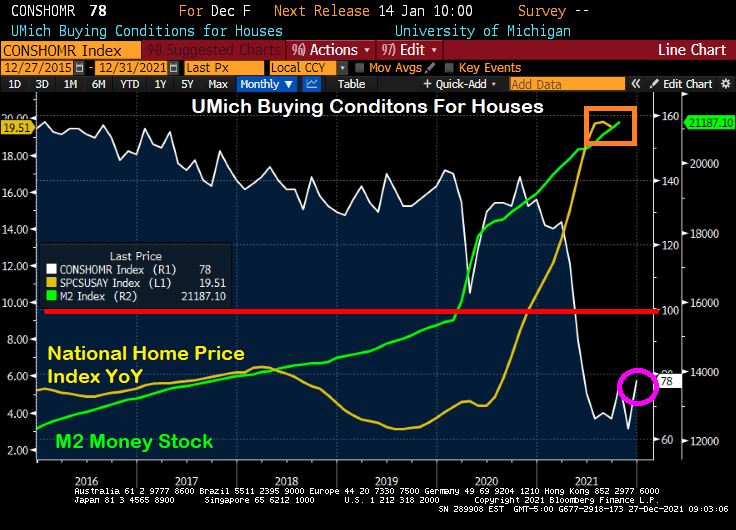

So it is not surprising that the University of Michigan consumer survey for “Buying Conditions For Housing” remains below 100 (meaning that more people think buying conditions for housing are negative than positive). With the Case-Shiller National home price index growing at a 19.51% YoY pace, it is no wonder that consumers are getting scared of the housing market.

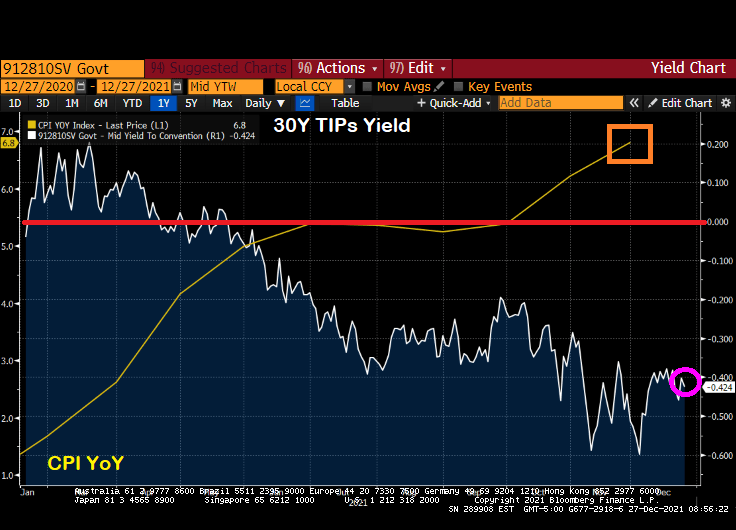

Yes, US inflation is at a 40-year high and the 30-year Treasury Inflation Protected (TIP) yields is at -0.424%. That says quite a bit about the pickle US consumers are in.

US consumer confidence overall has declined to the lowest level since just after the financial crisis and housing bubble burst of 2008-9.

Doctor, Doctor (Yellen), please don’t try to make housing more “affordable” which will result in housing being even LESS affordable.

But I do like how Biden took credit for lowering gasoline prices a little after his anti-energy policies drove up gasoline prices in the first place from $2.20 to $3.40 a gallon, a 55% price increase. Thanks for nothing, Joe!

And with Omicron raging (with few reported deaths), Anthony Fauci, President Biden’s top medical adviser, indicated support for making vaccinations a requirement for domestic fights.

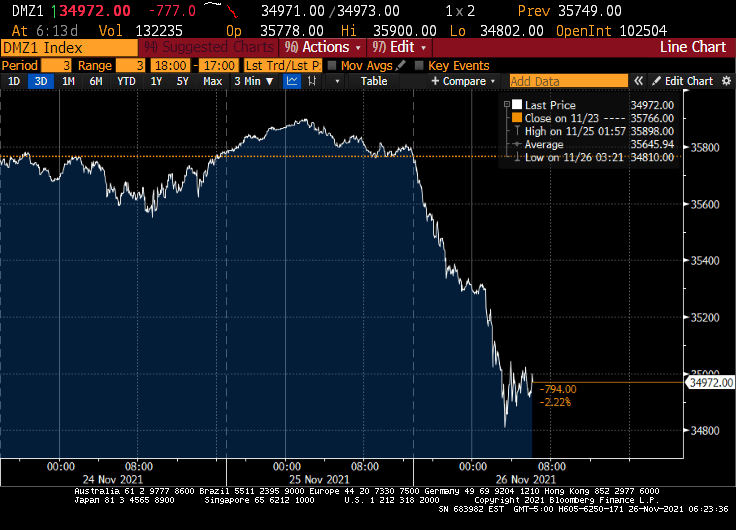

Gut-wrenching inflation is already priced in, but yet another COVID outbreak (and the possibility of more economic shutdowns, more vax mandates and more stern lectures from Anthony Fauci) are spooking markets.

Down Futures are down 777 as I write this note.

The 10-year Treasury yield is down 11.2 basis points.

And West Texas Intermediate crude prices are down 6.62%.

You must be logged in to post a comment.