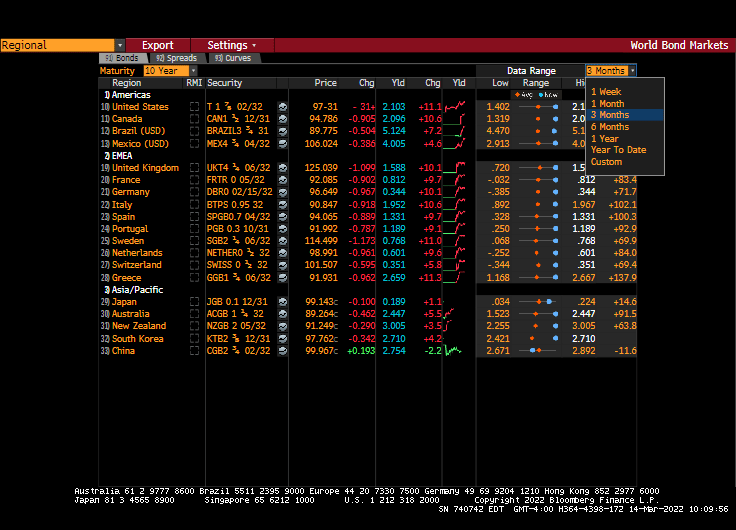

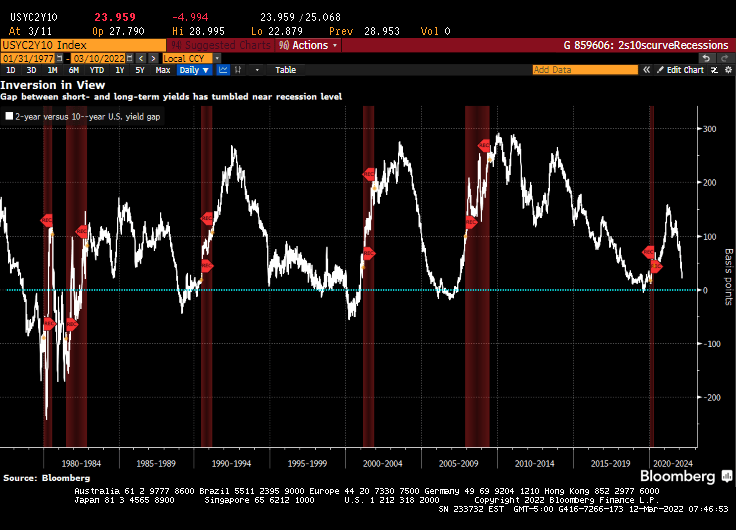

The US Treasury yield curve (10Y-2Y) is rapidly approaching inversion at 20.5 bps (where the 10-year yield is lower than the 2-year yield). But the 10Y-3M curve is generally steepening at 173.33 bps.

Of course, the driving force behind the flattening of the 10Y-2Y curve is the rapidly rising 2-year Treasury yield (orange line). The last time the 10Y-2Y curve inverted was in 2019, prior to the COVID outbreak in early 2020.

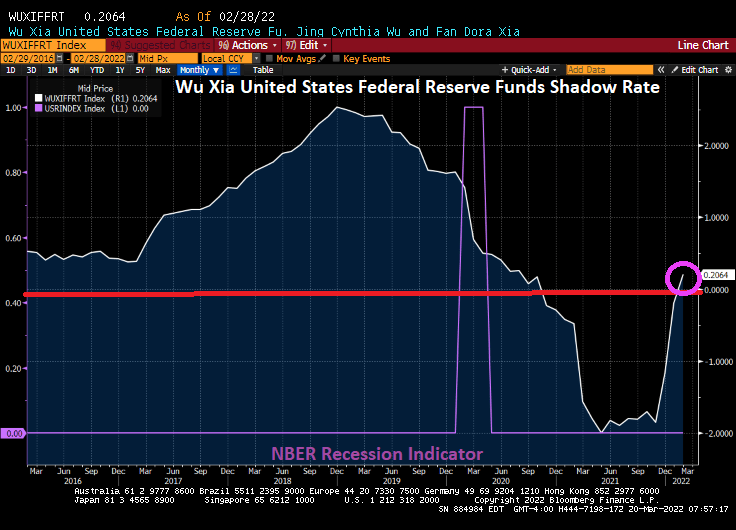

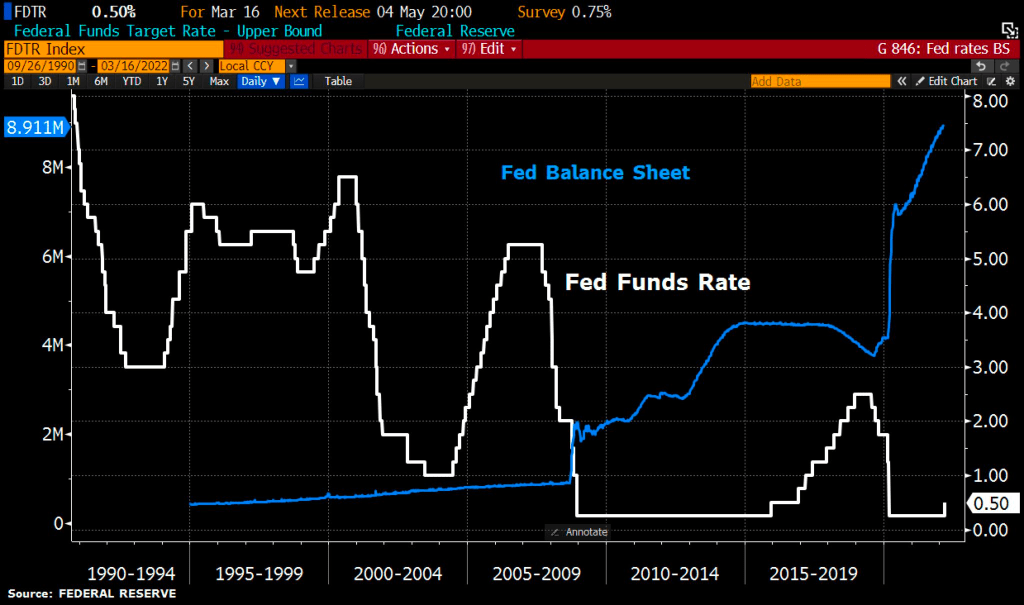

The Wu Xia United States Federal Reserve Funds Shadow Rate has finally climbed back into positive territory.

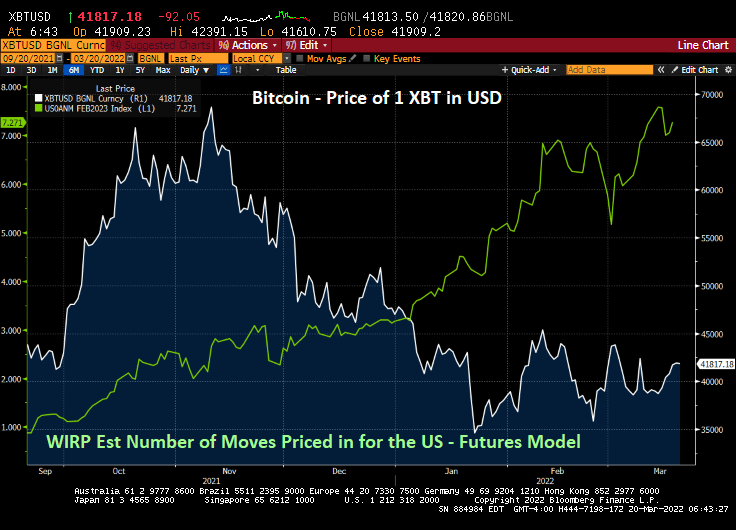

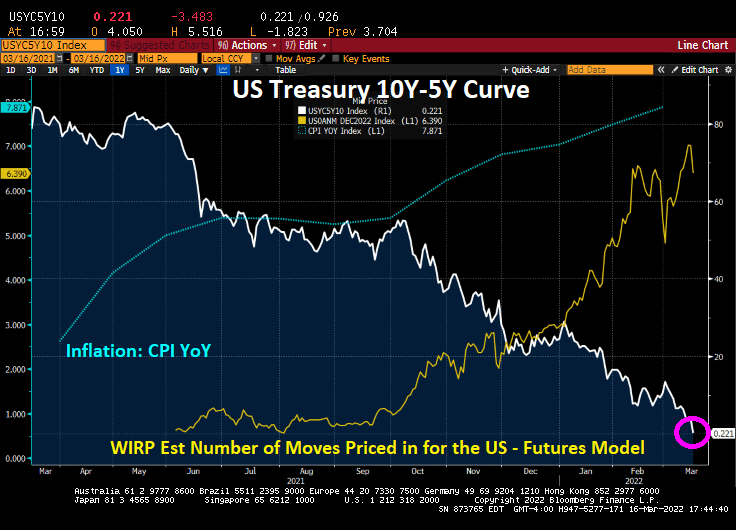

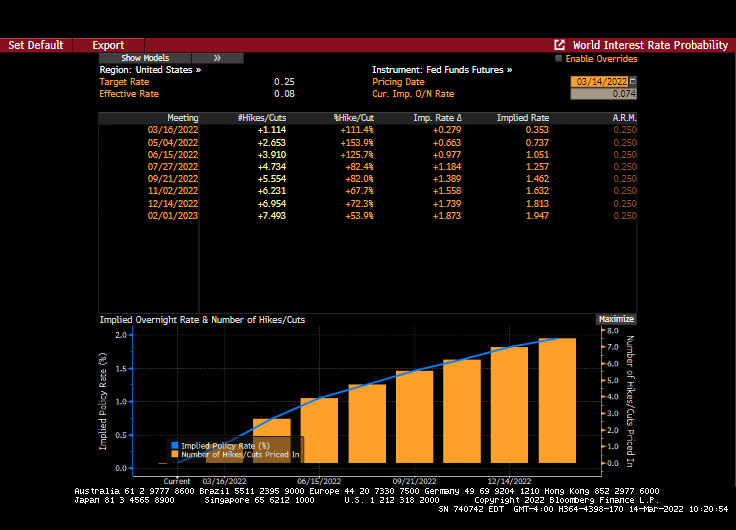

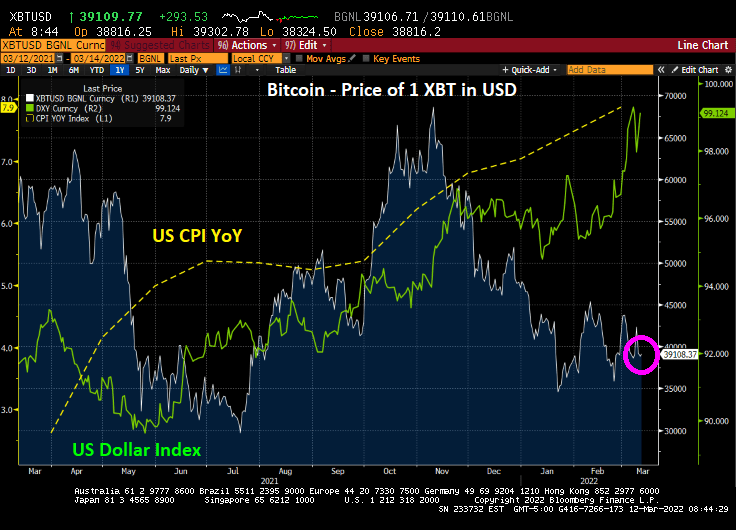

At last look, The Federal Reserve is forecast to raise their target rate 7 times over the coming year. And with the increasing forecast of rate hikes, we are seeing the cryptocurrency Bitcoin fall from near $70,000 to $41,817.

President Biden announced that he will be issuing an executive order to combat rising energy prices (the rising energy prices that he caused in the first place with … executive orders). Let’s see what happens next.

The news just keeps getting worse and worse. Russia is still assaulting Ukraine, WTI Crude prices are above $100 a barrel and climbing, the Cleveland Browns signed Deshaun Watson to replace Baker Mayfield at quarterback, etc.

But back to energy prices. Since Biden was sworn-in as President, WTI Crude Oil futures are up 125%, regular gasoline prices are up 89%, and diesel fuel prices are up 155%. Diesel is important since America uses diesel-powered trucks to transport goods to market.

Globally? The world inflation rate has grown from 2% in January 2021 to 6.82%. Global food prices are up 24%.

Yes, WTI Crude and Brent Crude are above $100 per barrel.

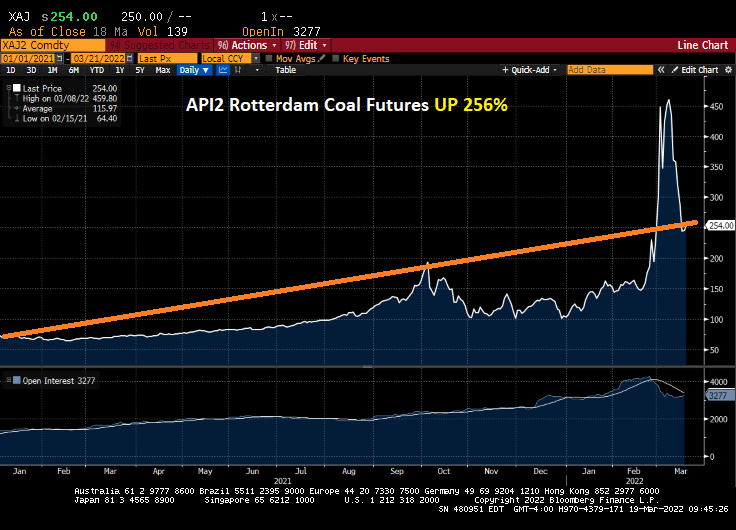

And coal prices are up 256% under Shoeless Brainless Joe.

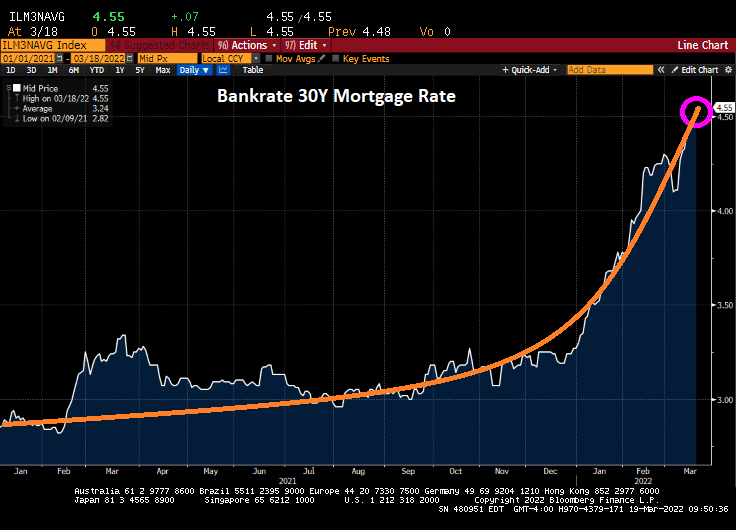

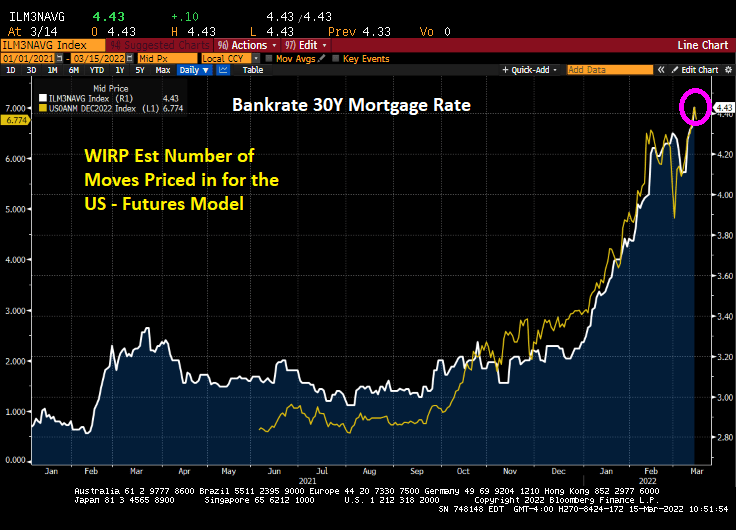

Mortgage rates? Bankrate’s 30-year mortgage rate is now above 4.50%.

Let’s see if Dr. StrangeFedpolicy raises rates as aggressively as signaled.

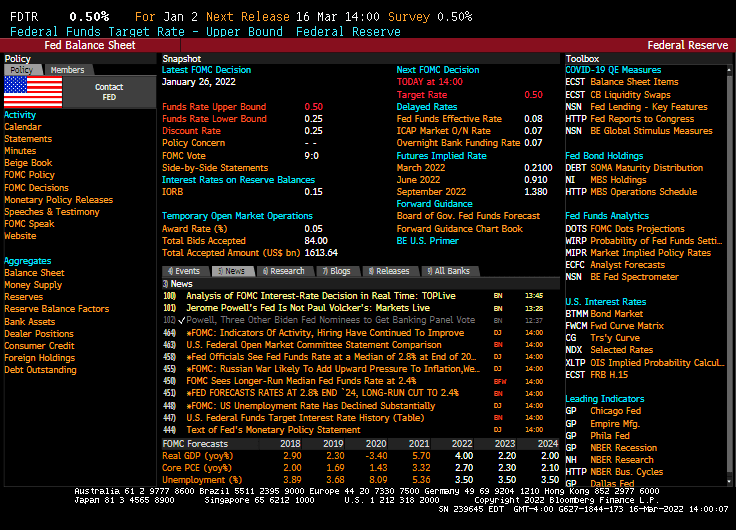

So, The Federal Reserve raised their target rate by … as expected … 25 basis points to 50 basis points.

The Taylor Rule suggests that the target rate should be 11.96%. So, Powell and The Gang are getting closer! /sarc

The short-term reaction to the measly rate increase? The Dow declined (but still in positive territory for the day) and the benchmark 10-year Treasury yield spiked to 2.23%.

On Powell’s surrender to inflation, the US Treasury 10Y-2Y curve continued to flatten.

You can see The Fed’s sloth-like response to blood-curdling inflation in the lower right-hand part of the chart.

Bankrate’s 30-year mortgage rate rose to 4.43%, up 55% under Biden/Pelosi/Schumer’s reign of error. Thanks to the rising Fed rate hikes priced-in the market.

The US Producer Price Index (PPI) final demand rose 10% YoY in February, further evidence of spiraling inflation under Biden/Pelosi/Schumer’s reign of error.

And speaking of Senate Majority Leader Chuck Schumer (D-NY), the Empire State Manufacturing Survey (General Business Conditions) crashed to -11.8.

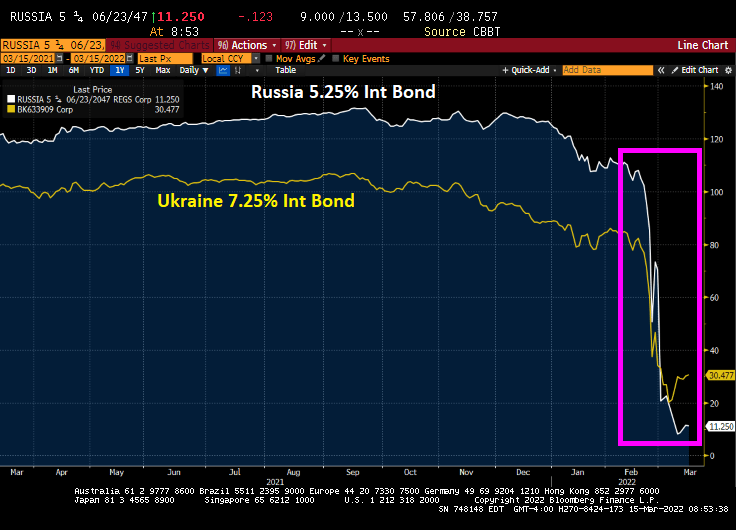

And Russia is losing the economic demolition derby with Ukraine (at least for sovereign debt).

I am still trying to figure out what House Speaker Nancy Pelosi (D-San Francisco) meant by “When we’re having this discussion, it’s important to dispel some of those who say, well it’s the government spending. No, it isn’t. The government spending is doing the exact reverse, reducing the national debt. It is not inflationary.”

Really Nancy?

Here is a chart of Federal government outlays and inflation. Massive expenditures and growth in Federal debt and the resulting inflation. Nancy?

Yes, it is the much anticipated Fed Week! The Fed Open Market Committee (FOMC) will announce it decision (probably the first rate hike under Biden of 25 basis points).

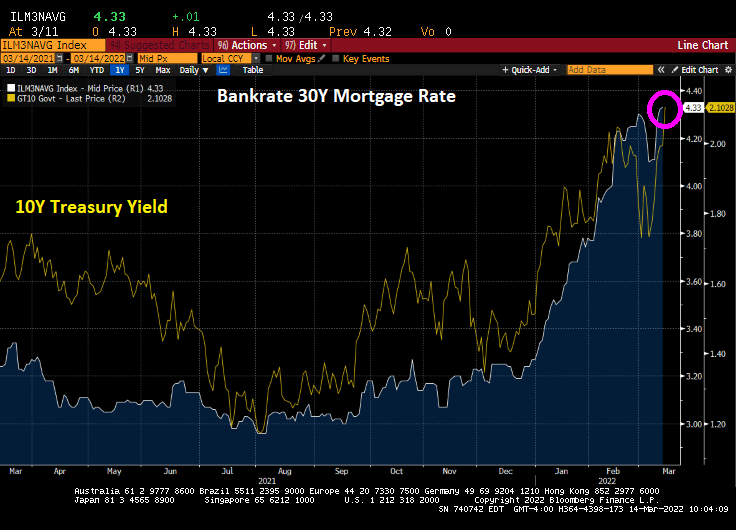

This morning, the 10-year Treasury yield rose by 11.1 basis points and the Bankrate 30Y mortgage rate rose to 4.33%.

Actually, sovereign yields are up around 10 basis points in the US, Canada, and across the pond.

Fed Funds Futures are pointing to 7 rate hikes over the next year with 1.114 rate hikes on Wednesday. That means The FOMC may raise rates MORE than the 25 basis points expected my many (including me).

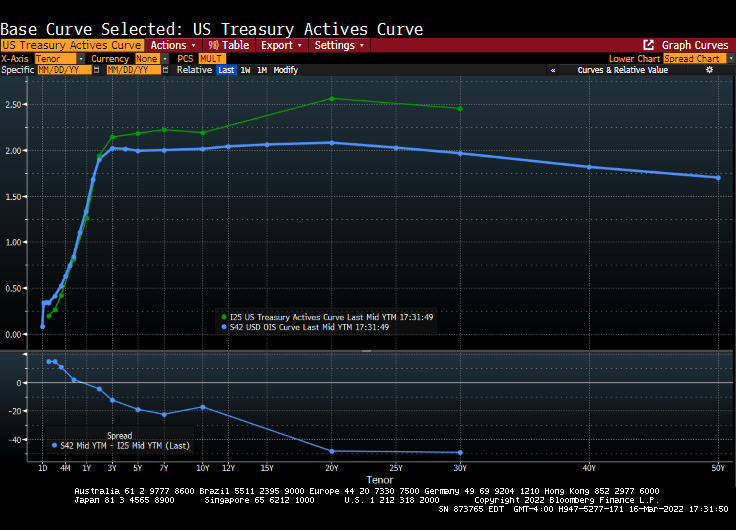

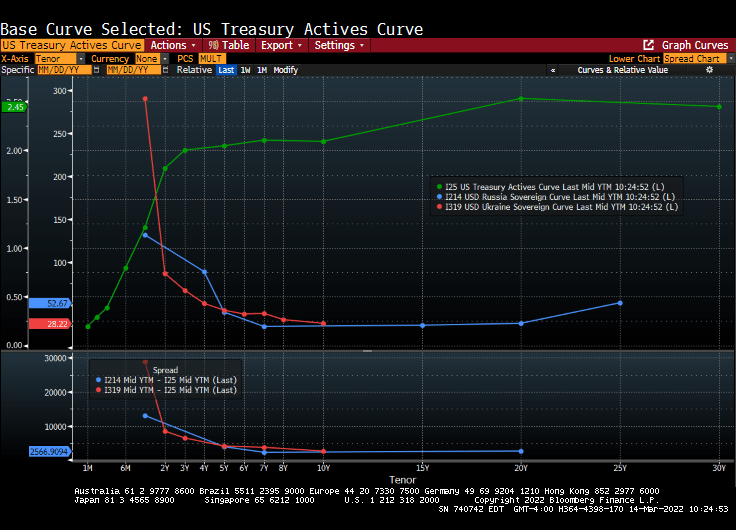

The US Treasury actives curve remains steeply upward sloping while both the Russian and Ukraine sovereign curves are steeply inverted and crashing.

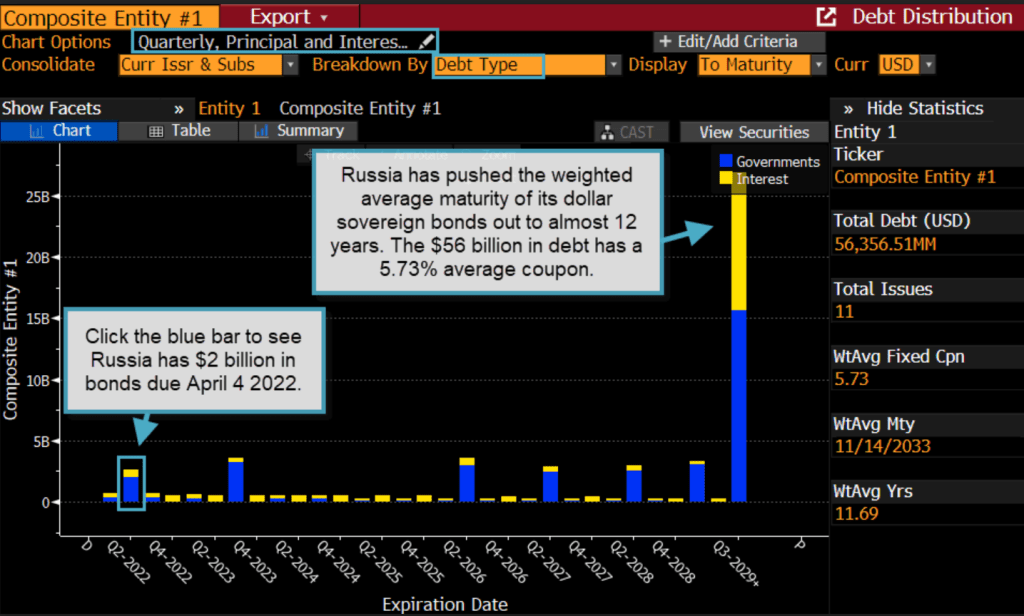

Russia has pushed the weighted average maturity of its dollar sovereign bonds out to almost 12 years.

The most hilarious headline of the day is a Bloomberg opinion piece: “Fighting Inflation May Require the Fed to Be Brutal: Clive Crook” How about the Biden Administration relaxing oil drilling and pipeline restraints? Otherwise, brutal translates into causing a recession. Great suggestion, Clive! … NOT!

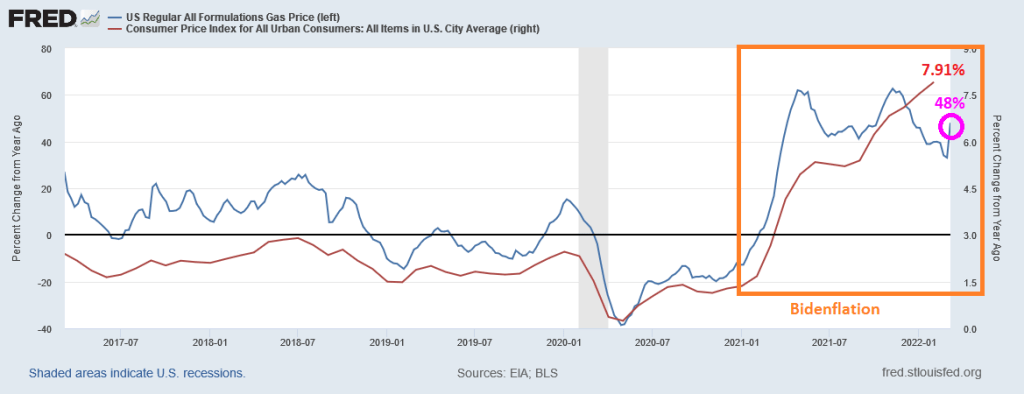

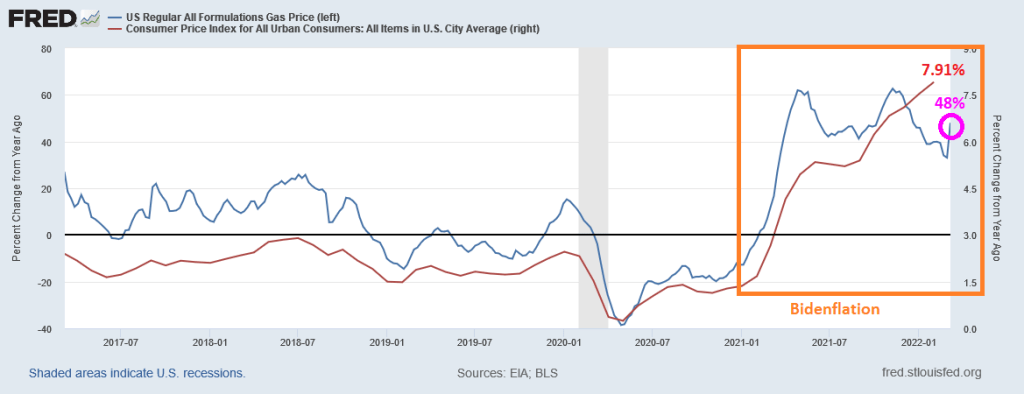

Well, so much for rising gasoline prices being the fault of Vlad “The Ukrainian Impaler” Putin and Russia invading Ukraine. In fact, gasoline prices were rising at a 62% YoY pace in April 2021, well before Russia’s invasion of Ukraine.

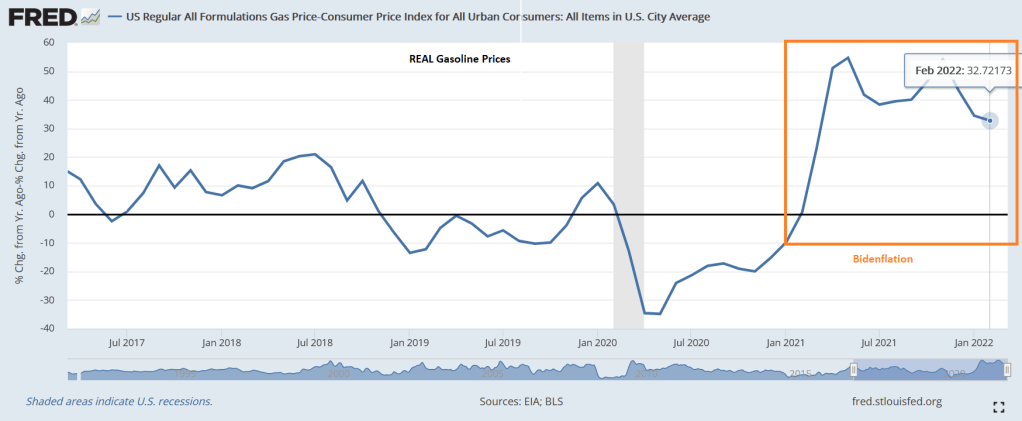

REAL gasoline prices (nominal gasoline prices less inflation) are up 32.72% YoY in February.

Press secretary Jen Psaki can take the opportunity to proclaim that REAL gasoline prices have actually declined in February.

I keep waiting for the Biden Administration and Congress to launch price controls and supply rationing rather than simply allow the Keystone Pipeline to be built and allow drilling on Federal lands.

US Speaker of the House and American Oligarch Nancy Pelosi together with Senate Majority Oligarch Charles Schumer passed yet another massive spending bill that seemingly benefited them and not the American middle class.

This legislation would provide $774.4 million for the Members Representational Allowance, known as the MRA, which funds the House office budgets for lawmakers, including staffer salaries. This $134.4 million, or 21 percent, boost over the previous fiscal year marks the largest increase in the MRA appropriation since it was authorized in 1996, according to a bill summary by the House Appropriations Committee. For paid interns in member and leadership offices, the House would get $18.2 million.

This is especially unfortunate given at inflation is growing at 7.9%. If we remove food and energy (two important categories for consumers and retirees), core inflation is growing at 6.4% YoY. As such, Social Security COLA doesn’t even keep pace with CORE inflation, let alone food and energy costs.

In August, Speaker Nancy Pelosi announced staffers’ salaries could exceed those of lawmakers. Members in both the House and Senate, with the exception of leadership, make an annual salary of $174,000. Staffers can make up to $199,300.

After an 11-year drought, congressional earmarks are back with vengeance.

The $1.5 trillion, 2,741-page omnibus spending package is loaded with funding for lawmaker pet projects, some of which could help incumbents in this fall’s elections.

The legislation includes more than 4,000 earmarks, according to a list of projects provided to The Hill by a Senate Republican aide that spanned 367 pages.

One of the biggest winners was New York — thanks to Senate Majority Leader Charles Schumer (D-N.Y.), who is up for reelection this year.

Schumer’s name is attached to 59 earmarks totaling nearly $80 million in the omnibus’s transportation and housing and urban development (HUD) section alone, according to a review by The Hill. He successfully requested funding for the projects either individually or with other lawmakers from his home state.

Is wild-spending Pelosi actually “The Bride of Chucky (Schumer)”?

Coindesk: The foundations of Bretton Woods II crumbled last week when the G7 seized Russia’s foreign exchange reserves, the investment bank said.

The Russian-Ukrainian war will create a new world financial order from which Bitcoin is set to benefit, according to Credit Suisse.

Zoltan Pozsar, global head of short-term interest rate strategy at the giant investment bank, wrote in a Monday report that Western sanctions on Russia are likely to cause a paradigm shift in the way the world organizes money and reserves, a “Bretton Woods III” kind of scenario.

“From the Bretton Woods era backed by gold bullion, to Bretton Woods II backed by inside money, to Bretton Woods III backed by outside money,” the strategist wrote.

Pozsar argues that the fall of Bretton Woods II ensued last week as G7 countries decided to seize Russia’s foreign exchange (FX) reserves, leading to a rise of outside money – reserves kept as commodities – over inside money – reserves kept as liabilities of global financial institutions.

“We are witnessing the birth of Bretton Woods III – a new world (monetary) order centered around commodity-based currencies in the East that will likely weaken the Eurodollar system and also contribute to inflationary forces in the West,” the report states.

Russia, a surplus agent in the financial system, can now no longer make use of the hefty FX reserves it accumulated through its commodity exports over the decades to defend its falling ruble or aid its local economy. Moreover, Russia’s ability to export its commodities has been severely hurt due to the “buyer’s strike” in the West.

“What we are seeing at the 50-year anniversary of the 1973 OPEC supply shock is something similar but substantially worse – the 2022 Russia supply shock, which isn’t driven by the supplier but the consumer,” the strategist wrote. “The aggressor in the geopolitical arena is being punished by sanctions, and sanctions-driven commodity price moves threaten financial stability in the West.”

Pozsar argues that while Western central banks cannot close spreads between Russian and non-Russian commodity prices as sanctions lead them in opposite directions, the People’s Bank of China can “as it banks for a sovereign who can dance to its own tune.”

“If you believe that the West can craft sanctions that maximize pain for Russia while minimizing financial stability risks and price stability risks in the West, you could also believe in unicorns,” Pozsar wrote.

As outside money keeps trumping inside money, this crisis will likely emerge and end differently than all others ever since Nixon broke off the gold standard in 1971 – which marked the end of the era of commodity-based money.

Meanwhile, US Treasury Secretary Janet Yellen said the U.S. dollar is in no danger of losing its status as the world’s dominant reserve currency as a result of sanctions imposed against Russia over its invasion of Ukraine.

“I don’t think the dollar has any serious competition, and is not likely to for a long time,” Yellen told reporters in response to questions following a speech in Denver on Friday.

Some commentators, including Credit Suisse Group AG interest-rate strategist Zoltan Pozsar, have warned sanctions that blocked Russia’s access to its foreign currency reserves could drive other countries away from the dollar.

Well, what Zoltan says may be true, but not so far. Bitcoin has been plunging since November 2021 as inflation keeps rising.

Zoltan: “..and Bitcoin (if it still exists then) will probably benefit from all this.” The US Treasury yield curve is listing towards inversion, a signal of impending recession.

You must be logged in to post a comment.