The Marty Stuart/Travis Tritt song “This One’s Gonna Hurt You (For A Long, Long Time)” seems appropriate for the plight of the middle and lower income classes in the face of high inflation. How do you spell the combination of President Biden’s policies and The Fed’s inaction on inflation? T-R-O-U-B-L-E … for the middle and lower income classes.

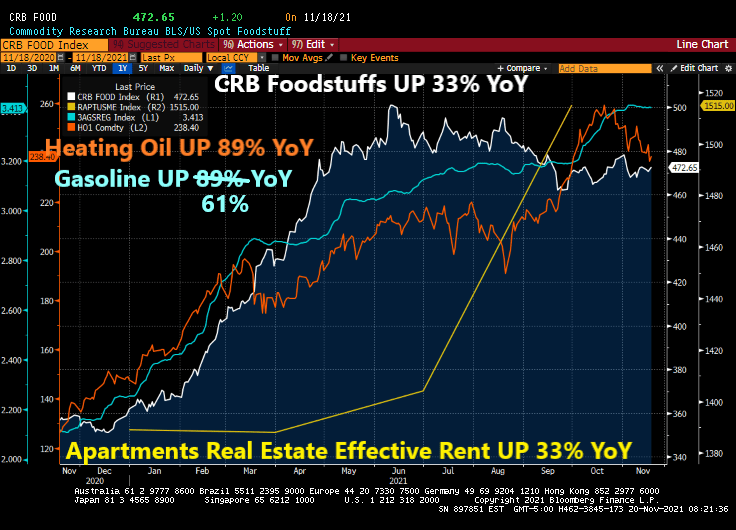

Over the past year, since the election of Joe Biden, the household consumption bundle (food, rent, heating, gasoline) have all risen dramatically in terms of prices. Food is up 33%, heating oil is up 89%, regular gasoline is up 61%, and effective apartment rents are up 33%.

Meanwhile, the 1% are sitting high on a mountain top obvious to the pain caused by The Federal Reserve and Biden Administration. Here is the growth in wealth by the 1% since the housing bubble burst and financial crisis compared with the bottom 50%.

A problem facing renters is the rapid growth of home prices particularly since the COVID epidemic. At least M2 Money has “slowed” to 12.80% YoY while home prices are raging at almost 20% YoY. But hopefully home price growth will slow with declining M2 growth.

Compendium of Fed Chair Jerome Powell and President Biden on vacation.

Nothing has been the same since the housing bubble of the 2000s, the resulting banking meltdown and the takeover of the economy by The Federal Reserve.

And since the 2000s housing bubble and financial crisis, The Federal Reserve has taken control of the economy resulting in M2 Money Velocity crashing to historic lows.

Combine vaccine mandates that lower the workforce and the flood of economic and monetary stimulus by the geniuses in Washington DC, and we have a Thanksgiving problem.

Supplies of food and household items are 4% to 11% lower than normal as of Oct. 31, according to data from market-research firm IRI. That figure isn’t far from the bare shelves of March 2020, when supplies were down 13%.

For grocery shoppers this holiday season, it means that someone with 20 items on their list would be out of luck on two of them.

Although U.S. supermarket operators started purchasing holiday items early, aiming to avoid shortages, many holiday essentials are already in short supply.

Turkeys are very low in stock. By the end of October turkeys were over 60% out of stock—lower than the same time last year by more than 30 percentage points. A spokesperson for Butterball LLC, one of the largest U.S. turkey processors, said the company has been experiencing similar labor and supply challenges as other organizations and industries.

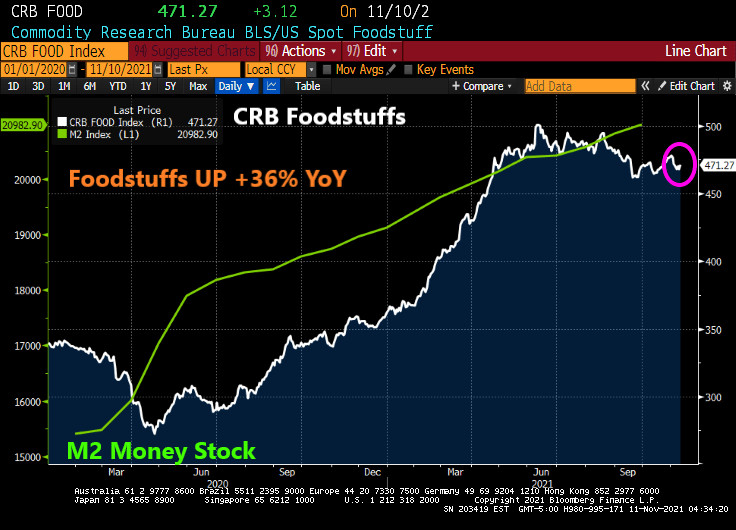

Even if you can find a turkey, prices on foodstuffs in general are up 36% from last year.

And to get to the grandparents’ house of Thanksgiving, gasoline prices (regular) are up 24.5% from last year.

Biden could lower inflation by 1) stop mandating vaccines, 2) stop shutting off energy pipelines and oil exploration, 3) stop spending trillions of dollars other than Social Security, Medicare and defense.

Frankly, Thanksgiving has gotten so expensive due to Biden’s Reign of Error that I am thinking of alternatives to turkey. Like a Jersey Mike’s turkey and provolone sub.

President Biden wants to know if you are Tuff Enough to stand rapidly rising energy prices as he shuts down American supply?

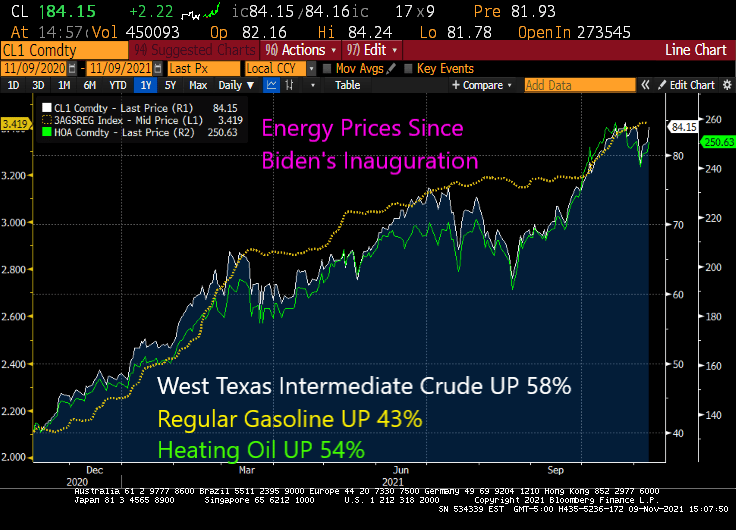

Since Biden’s inauguration, West Texas Intermediate crude prices have soared by 58%, regular gasoline prices have soared by 43% and heating oil has soared by 54%.

Meanwhile, US households are told to put on more blankets and drive less while the DC elites (like Obama, Kerry and Yellen) fly around the world in fossil-fuel guzzling jets lecturing everyone on the need to get rid of fossil fuels.

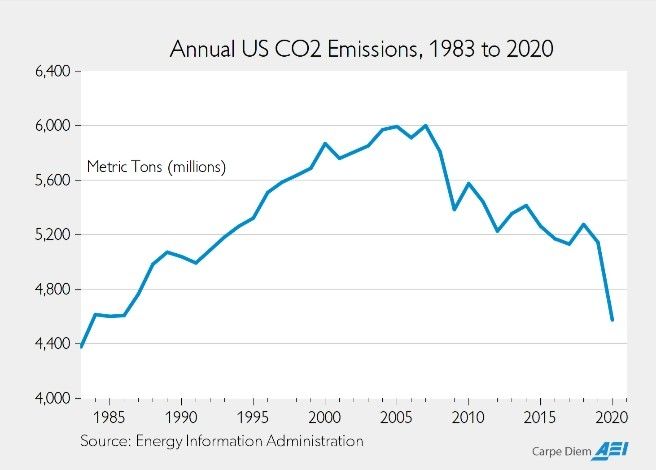

Odd, since annual CO2 emissions have declined significantly from 2007 levels.

And with a wave of her magic wand, Treasury Secretary Janet Yellen (aka, the Incredible Janet Yellenstone) will make inflation magically return to less than 2% after mid-2020.

Treasury Secretary Janet Yellen said she expects price increases to remain high through the first half of 2022, but rejected criticism that the U.S. risks losing control of inflation.

Inflation is expected to ease in the second half as issues ranging from supply bottlenecks, a tight U.S. labor market and other factors arising from the pandemic improve, Yellen said on CNN’s “State of the Union” on Sunday. The current situation reflects “temporary” pain, shesaid.

“I don’t think we’re about to lose control of inflation,” Yellen said, pushing back on criticism by former Treasury Secretary Lawrence Summers this month. “Americans haven’t seen inflation like we have experienced recently in a long time. But as we get back to normal, expect that to end.”

On Friday, Federal Reserve Chair Jerome Powell sounded a note of heightened concern over persistently high inflation as he made clear that the central bank will begin tapering its bond purchases shortly but remain patient on raising interest rates.

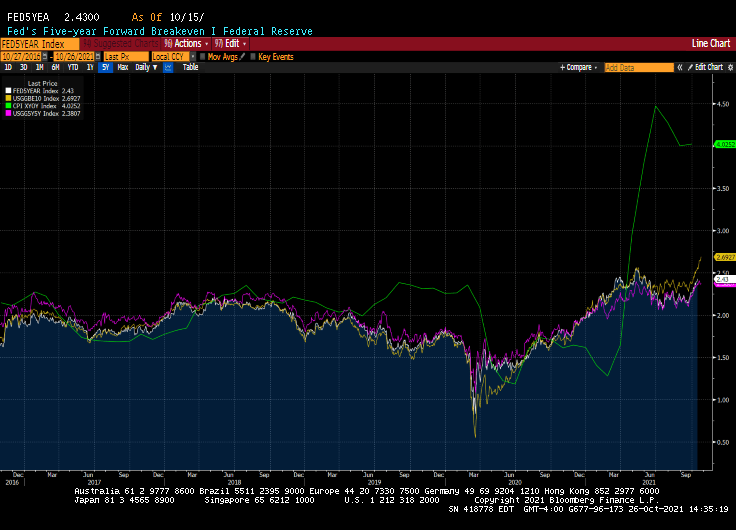

The S&P 500 Index posted its first decline in eight days, while benchmark Treasuries rallied to send 10-year yields down by the most in more than two months. Inflation expectations remain elevated — the 10-year breakeven rate of 2.64% is within 15 basis points of the record high reached in 2005 — and rates traders maintained bets the Fed will hike at least once within a year.

Powell said policies are “well-positioned” to manage a range of outcomes.

So Janet, are you saying that home price growth is going to slow to 2% YoY after mid-2022? Or that the Biden Administration is going to build the Canadian pipeline to help ease energy costs? Or that west coast ports get magically unclogged? Or that chips for cars will magically begin appearing?

I forget. The Fed doesn’t consider housing or energy prices in their inflation measurements. So, Yellen and The Fed ignore that most important expenditures for households.

The Fed’s breakeven inflation rates are considerably lower than current core inflation (green line).

No wonder Yellen and Powell can make inflation magically disappear. Don’t count it!

Federal Reserve Chair Jerome Powell sounded a note of heightened concern over persistently high inflation as he made clear that the central bank will begin tapering its bond purchases shortly but remain patient on raising interest rates.

“The risks are clearly now to longer and more persistent bottlenecks, and thus to higher inflation,” Powell said Friday during a virtual panel discussion hosted by the South African Reserve Bank and moderated by Bloomberg’s Francine Lacqua.

“I would say our policy is well-positioned to manage a range of plausible outcomes,” he said. “I do think it’s time to taper and I don’t think it’s time to raise rates.”

Good luck with that, Jay! You are going to raise the short-end of the yield that will lead to a flattening of the Treasury yield curve. But you are going to continue to buy Treasuries and Agency MBS in order to monetize the rampant spending by Congress and the Biden Administration? C’mon man!

You can see where Powell spoke today. It is when gold tanked along with the 10-year Treasury yield. Both rebounded a bit, but the 10-year Treasury yield continue its fall to 1.6324%.

The US dollar (green) fell when Powell opened his pie-hole. But Bitcoin (blue) fell in advance as if they knew what Powell was going to say.

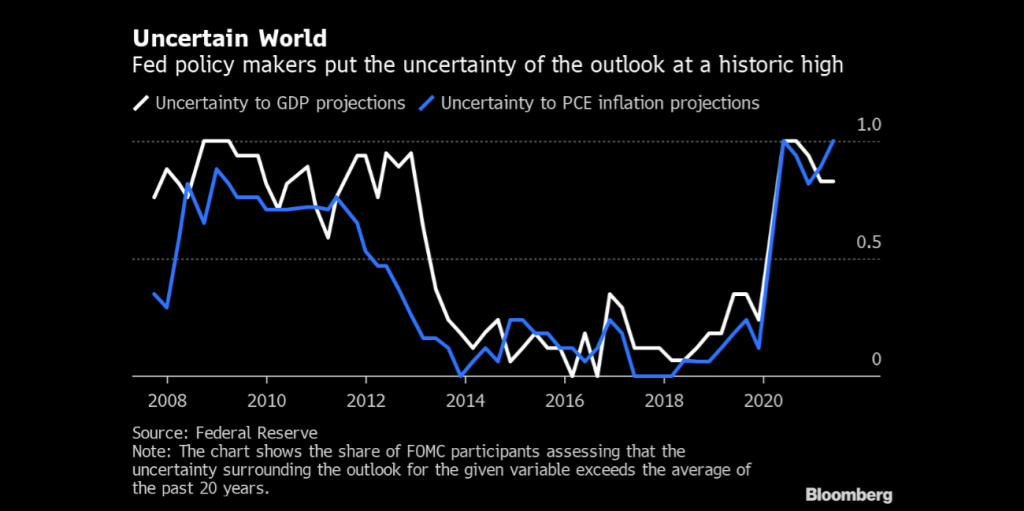

Has The Federal Reserve lost control of the economy? And inflation? The answer is likely yes. Why?

The Covid crisis has been played by the Federal government as an excuse for insane levels for spending coupled with massive monetary stimulus from The Federal Reserve.

As an example of The Fed losing control is US savings. The Fed’s model is to drive savers into consumption, therefore raising production and increasing GDP growth. But alas, The Fed can’t overcome the fear faced by consumers with Covid, Covid shutdowns, and rapidly rising prices.

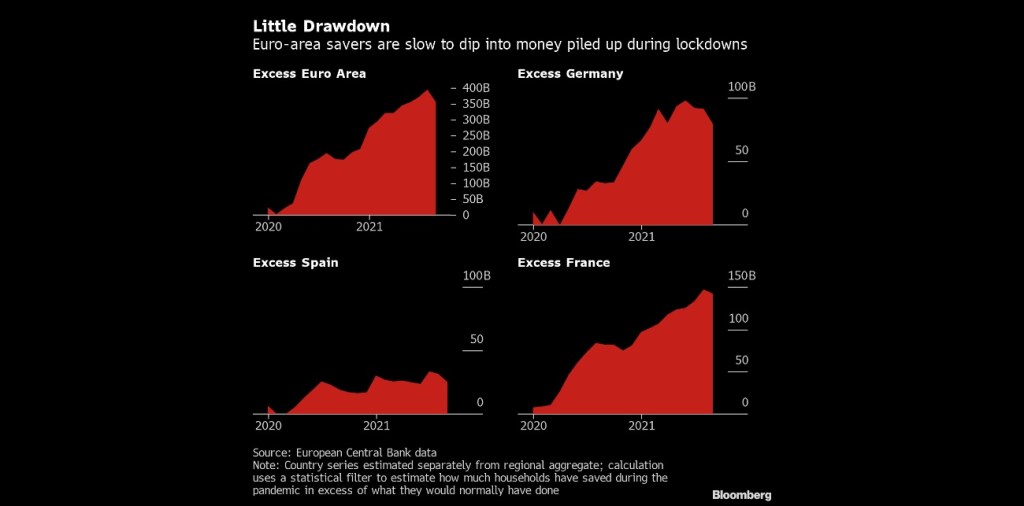

(Bloomberg) — Consumers in Europe and the U.S. aren’t rushing to spend more than $2.7 trillion in savings socked away during the pandemic, dashing hopes for a consumption-fueled boost to economic growth on both sides of the Atlantic.

In the wake of lockdown easing during the northern hemisphere’s summer holiday season, excess savings in euro-area bank balances declined only marginally in August, and Italy still recorded an increase, according to calculations by Bloomberg Economics. In the U.S. there has also been no drawdown, the figures show.

The absence of a consumption surge that had been anticipated by some economists may speak against the prospect of a lasting inflation shock feared by central banks. While higher balances could help households cope with skyrocketing heating bills, tepid demand might temper businesses’ ability to push through permanent price increases.

In the USA, we see accumulated savings despite near-zero deposit rates at banks.

To be sure, The Fed reacted (or overreacted) to the Covid outbreak by increasing the money supply and their purchase of Treasuries and Agency MBS as the Federal government went on a wild spending spree.

But with trillions in Stimulypto Federal spending and Fed money printing, the bottlenecks in the economy (which apparently weren’t known before … ) have contributed to massive price increases that aren’t going away any time soon.

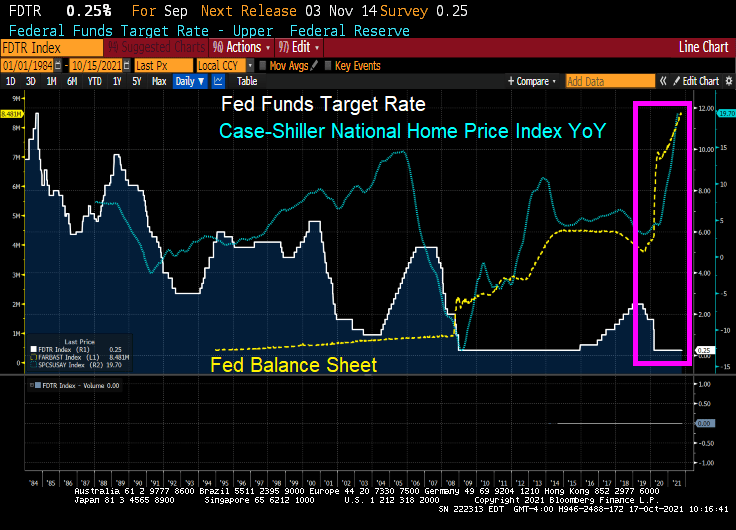

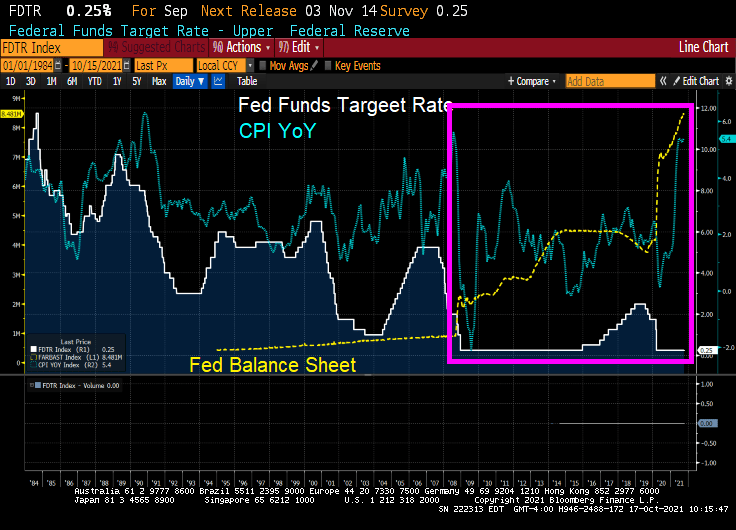

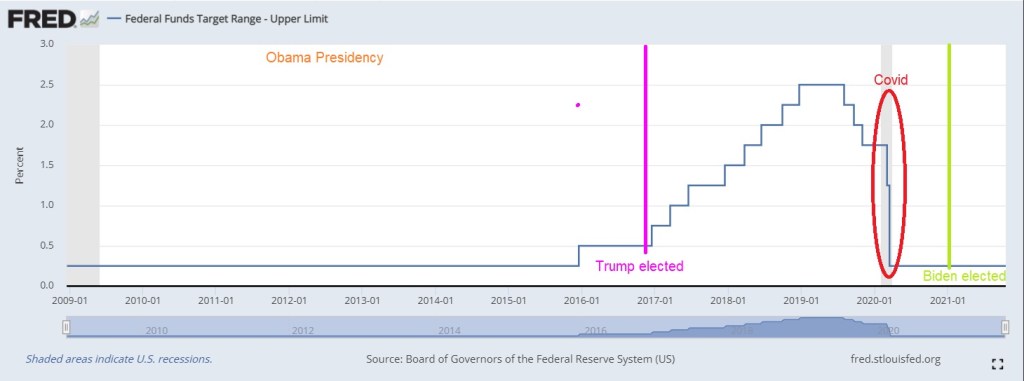

Notice how Fed monetary policies changed after the housing bubble burst and ensuring financial crisis/Great Recession. Before 2008, The Fed periodically whipsawed their Fed Funds target rate. But since late 2008, we have seen hardly any move from The Fed (except for 2017-2020 while Trump was President). For Obama,

Here is a look at The Fed’s record under Obama, Trump and Biden. The Fed raised their target rate only once under Obama until Trump was elected. Then The Fed raised rates 8 times. Then began lowering them again (5 times) leading to a big drop when Covid stuck. So for Trump, The Fed changed their target rate 13 times compared to 1 rate change under Obama and none under Biden.

And the above chart is only The Fed’s target rate. My point is that Yellen failing to raise rates under Obama has resulted in this over DC-Stimulypto we are seeing today.

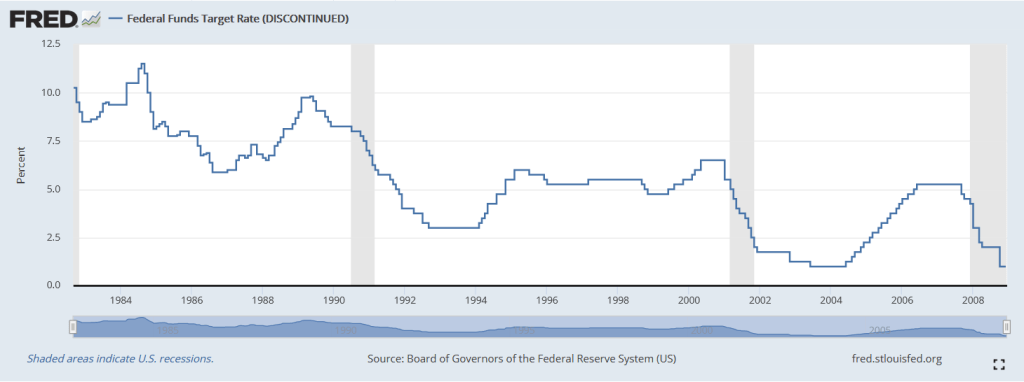

Note the difference in Fed policies BEFORE the financial crisis. We need to return to a normal Fed policy rather than the hyper-inflationary zero-rate, QE policies since 2008.

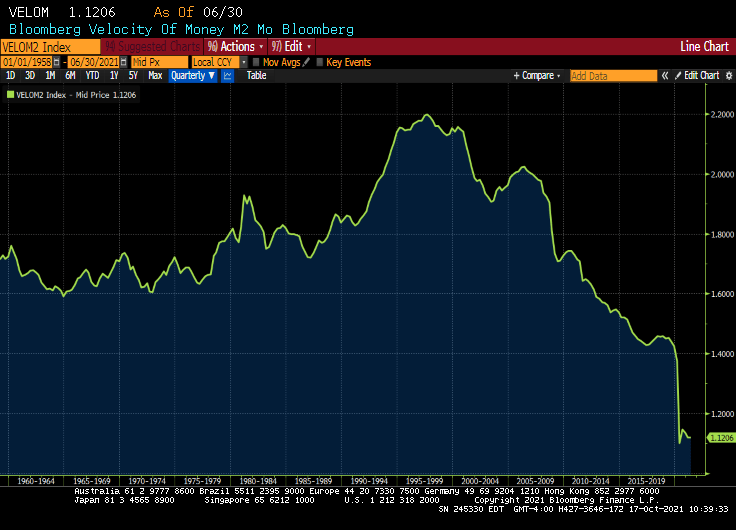

M2 Money velocity (GDP/M2 Money) remains near an all-time low.

But given DC’s spending spree and all-time lows for M2 Money Velocity, The Fed is going to need to keep purchasing trillions in debt at low interest rates. The abnormal Obama years (Bernanke/Yellen) are the NEW abnormal. Or should I say abby normal policies?

Dr. Frederick FrankensteinAre you saying that I put an abnormal brain into a seven and a half foot long, fifty-four inch wide GORILLA?

So, yes, Bernanke and Yellen put into place abnormal policies that Powell is following into the world’s largest economy (or gorilla).

Only Igor and The Federal Reserve would pick such abnormal policies that ultimately lead to massive misallocations and inflation.

On a side note, do Biden and Transportation Secretary Pete Buttigieg really believe that they can fix the backed-up ports that are flooded with cargo thanks to Stimulypto? By Christmas??

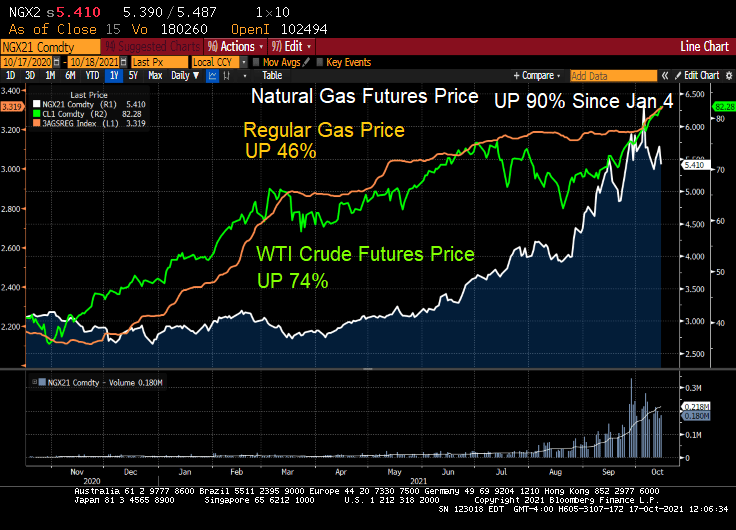

Not with natural gas prices up 90% since January 4th!

Since Joe Biden took office in January 2021, we have seen several actions from The White House. First, was the cancellation of the Keystone Pipeline (making the US more energy dependent on others). Second, Biden waived US sanctions on Russian pipeline to Germany. Big winner? Russia. Big loser? US consumers trying to heat their homes.

Here is a chart of natural gas prices since Biden took office in January.

Biden reminds me of Dwight Schrute from the TV show “The Office” as he loves to punish people. In this case, families trying to heat their home. And have his own currency, Schrute Bucks.

Perhaps The Federal Reserve should rename the US Dollar as “Biden Bucks.”

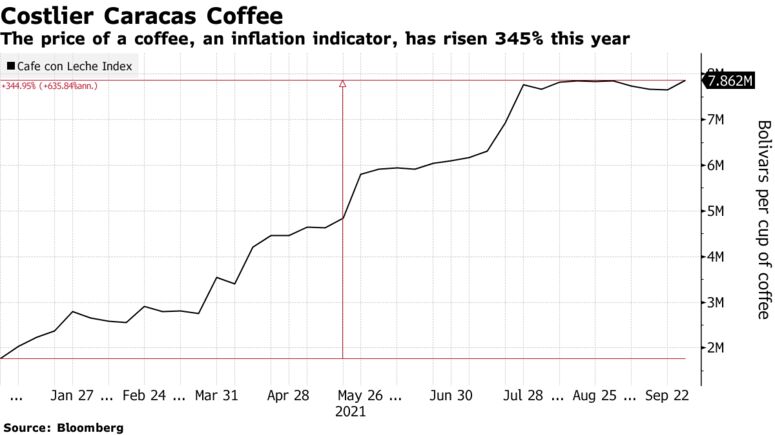

Here they go again! A cautionary tale of a government gone wild resulting in gut-wrenching inflation and 76.7% of the population living in extreme poverty.

Venezuelais launching a new version of the bolivar in the latest attempt to salvage a currency so beaten down by years of hyperinflation that residents have adopted the U.S. dollar.

The so-called digital bolivar, which is being introduced Friday, effectively removes six zeroes from the “sovereign bolivar,” which started circulating just three years ago.

New banknotes and coins will be put into use. Bank accounts will be adjusted to reflect the redenomination. And debit and credit card purchases will become easier: there were so many digits involved in some transactions that merchants were forced to split the transaction into multiple card swipes.

It’s another maneuver aimed at propping-up the national currency, even though President Nicolas Maduro’s government is permitting the use of the U.S. dollar as a way to cope with runaway inflation and shortages. The government has implemented two other currency changessince 2008, dropping eight zeroes. Hyperinflation, among the highest in the world, has slowed to 2,146% per year from more than 300,000% in 2019, according to Bloomberg’s Cafe Con Leche index.

Under Friday’s change, the largest former banknote, for 1 million bolivars — worth about $0.23 –will be replaced by a 1-bolivar coin. One dollar will fetch around 4.2 bolivars instead of 4.2 million bolivars at the official exchange rate.

“This is useless. Prices will continue to rise and, in a few months, the new bills will be useless,” said Leida Leon, a 37-year-old cleaning worker at a Caracas school.

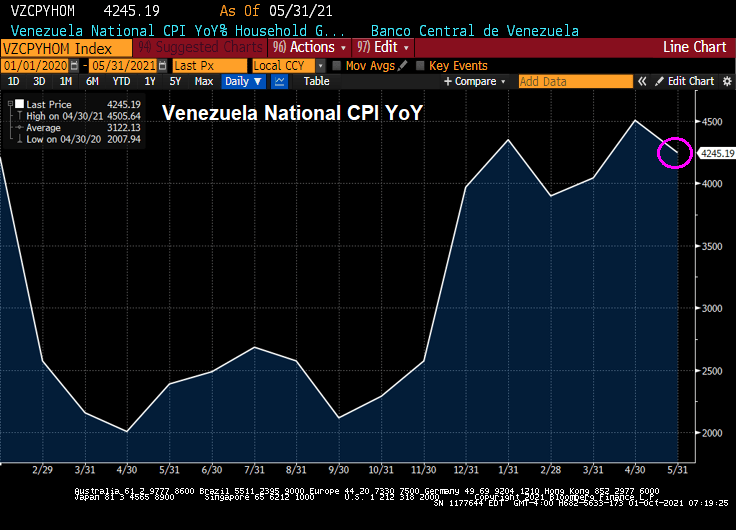

And Venezuela’s official inflation rate for household goods is a blood-curdling 4,245% YoY.

On Thursday, demand for dollars rose as people feared a prolonged suspension of banking services as the redenomination is rolled out, said Luis Arturo Barcenas, senior economist at Caracas-based financial analysis firm Ecoanalitica.

Two-thirds of retail transactions involve the U.S. dollar, according to Ecoanalitica. Yet, many Venezuelans need bolivars for everyday transactions, like bus fares and to buy gas subsidized by the government. While the government is attempting to boost the use of digital payments, many regions are beset by regular electrical blackouts that affect communications.

Venezuelans have faced disastrous government policies and pressure from U.S. sanctions that have put the country on the brink of its eighth-straight year of economic contraction. More than 5 million people have fled the country, once one of Latin America’s wealthiest.

An estimated 76.6% of Venezuelans are living in extreme poverty, up from 67.7% last year, according to a university survey on living conditions known as Encovi.

As least Venezuela’s Treasury Department could produce a likeness of Simón Bolívar (aka, Simón José Antonio de la Santísima Trinidad Bolívar y Ponte Palacios y Blanco) that doesn’t look like a bad cartoon character.

Building materials copper and PVC (pipes) both surged with The Fed’s Cat 5 hurricane approach to liquidity. Then copper backed-off, but PVC rose when Hurricane IDA struck the gulf coast.

The Fed will announcing their plans (maybe) at 2pm today.

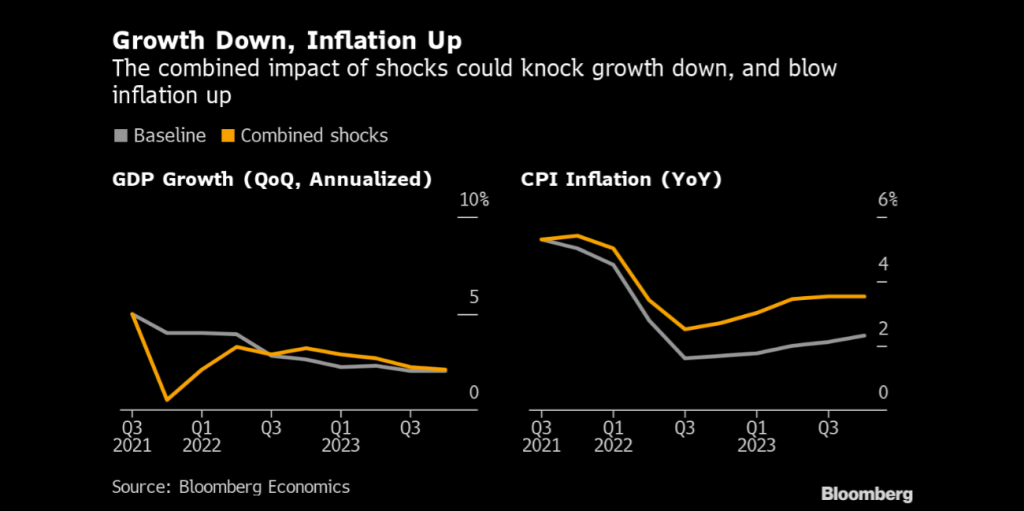

What would it take to knock the U.S. recovery off course and send Federal Reserve policy makers back to the drawing board? Not much — and there are plenty of candidates to deliver the blow.

From one direction: U.S. debt-ceiling deadlock, China property slump or simply an extension of Covid caution could hit growth and jobs — taking the Fed’s proposed taper of bond purchases off autopilot, and pushing its first interest-rate increase back to 2024 or later. From the other: Sustained supply-chain snarl-ups could keep inflation stubbornly high and unmoor inflation expectations — forcing an acceleration of the taper, and an early rate liftoff in 2022.

And if shocks arrive from both directions at once, the upshot could be a combination of weak growth and rapidly rising prices — not as severe as the stagflation of the 1970s — but still leaving Fed Chair Jerome Powell and his colleagues with no easy answers.

In the following, we use Bloomberg Economics’ new modeling tool SHOK to explore these scenarios. None of them represents our base case. At a moment of elevated uncertainty, it makes sense to pay more attention to the risks.

Is the U.S. Economy Headed for a Slowdown? Signs of a slowdown in the U.S. economy aren’t hard to find.

August payrolls — just 235,000 new jobs, one-third of the expected number — were a red flag. The delta variant has made consumers cautious again. The University of Michigan’s index of sentiment plunged in August; only six declines since the modern index was launched in 1978 have been bigger.

Add all these pieces together, and a recovery that looked unstoppable just a few weeks ago now appears to be losing steam. At Bloomberg Economics, we have cut our prediction for annualized third-quarter growth to 5%, from above 7% at the start of the quarter. Others have gone lower, with forecasters at some of the big banks anticipating growth closer to 3%. Even if delta subsides, it’s not hard to imagine scenarios where the slide continues.

One of them involves the partisan impasse over raising the U.S. debt ceiling. The U.S. government is expected to reach the limits of its debt-servicing capacity in October. Default, a potentially catastrophic event for the global financial system, still appears an outside possibility. But even without one, recent history shows that dancing around the possibility — triggering a persistent risk-off period in the markets — can have serious consequences. Separately, a government shutdown starting Oct. 1 would hardly be helpful when the recovery is already struggling to find its footing.

In the three weeks around the 2011 debt-ceiling standoff, the S&P 500 index plummeted more than 15% and corporate borrowing costs spiked. Using SHOK we estimate that a repeat performance would shave about 1.5 percentage points off annualized fourth-quarter growth — and ensure a rocky start to 2022.

Global Risks to the Fed’s Plan Not all the risks originate so close to home.

Fears of a China housing crash have long haunted global markets. Now, President Xi Jinping’s “common prosperity” agenda has turned that into a real possibility.

Regulators are cracking down on abuses that inflated property values, and tight controls on lending have helped push prices and new construction sharply down. That’s left Evergrande, one of the nation’s biggest developers, on the cusp of a default. The consequences of a wider slump could be severe, because real estate drives demand for everything from steel and concrete to furniture and home electronics — contributing as much as 29% of China’s GDP, all told.

It wouldn’t take a sub-prime style meltdown to send shockwaves around the world and move the dial for the U.S. China’s economy is currently forecast to enter 2022 with growth at around 5%. A property slump could take that down to 3%, triggering a blow to trade partners, a drop in oil and metal prices, and a risk-off moment in global markets. In that scenario, the U.S. would limp into 2022 with the recovery marked down and inflation back below the 2% target.

When Is Jerome Powell Likely to Raise Rates? Powell has set out the FOMC’s criteria for rates liftoff: maximum employment, and inflation that hits and is set to exceed the 2% target for some time. A blow to employment and demand from a debt-ceiling standoff or China shock might mean those criteria are not met. Rate hikes could be kicked into the long grass, with expectations moving from 2023 out to 2024 or beyond. The test for tapering is less stringent, and a start at the end of this year appears close to baked in. Even so, if the recovery stumbles the Fed might have to make a course correction, introducing discretion into a process that markets expect to run on autopilot.

In 2015, the stock-market and currency slump in China — and the sustained shift to global risk-off sentiment that triggered — was enough to delay the start and slow the pace of the U.S. tightening cycle. In 2021, the Fed might not have that luxury.

China’s residential property slowdown deepened last month, signaling that regulatory tightening and an escalating crisis at the country’s most indebted developer are hurting buyer sentiment.

Supply-chain breakdowns — from port closures to shortages of semiconductors and lumber — have been one of the main factors pushing U.S. inflation above 5% this summer. That’s enabled Powell to label the price jumps as “transitory” and soothe fears of an upward spiral. The lower CPI reading for August provides some support for that thesis.

It wouldn’t take much, though, for further supply shocks to keep inflation uncomfortably high. From home electronics to textiles, American consumers load their shopping carts with goods that are made in Asia and delivered via supply chains that crisscross the continent. When the inflation rate for used cars in the U.S. hit 45% this year, driven by semiconductor shortages that threw assembly lines into disarray, it illustrated what can happen when those fragile linkages break down.

All of this adds to the risk of further “transitory” shocks to inflation. One early-warning signal: according to press reports, semiconductor giant TSMC has announced plans for price hikes of as much as 20% next year.

The effects of pandemic-induced supply-chain disruptions are still rippling through businesses and households, reflected in higher prices for goods, delays in receiving them and flat-out shortages.

For the Fed, inflation running hot into 2022 would be troubling on its own, and worse if it triggers a shift in inflationary psychology. If businesses start to feel comfortable setting prices higher, and workers start demanding higher wages to compensate, the risk is a situation reminiscent of the wage-price spirals of the 1970s — when it took a recession engineered by the Volcker Fed to squeeze inflation expectations out of the system.

Unmoored inflation expectations would very likely trigger an early and aggressive response from the Fed: an accelerated taper, and a rate hike in 2022.

A no-win scenario would be if the two blows — to output and jobs, and to supply chains and prices — landed at the same time, leaving Fed officials in a quandary. Ease policy to support growth and they would add fuel to the inflationary fire. Tighten to bring prices under control, and they would exacerbate the drag on the recovery, throwing more Americans out of work.

Agreement in Congress, or decision by the Democrats to go it alone, could remove the default risk. China has in the past proved skillful at shifting gears to avoid a housing crash. Vaccination rates in Asia are rising. The latest U.S. data — inflation slowed and retail sales rose — have been encouraging.

You must be logged in to post a comment.