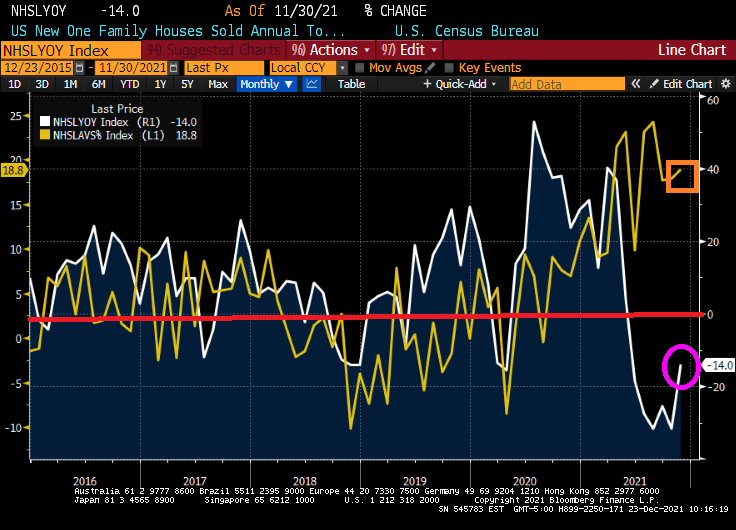

The Case-Shiller National home price index “slowed” to 18.81% YoY in November as The Fed continues its monetary stimulypto. Notice that The Fed is easing even when there is limited inventory available. Result? Hideous home price inflation.

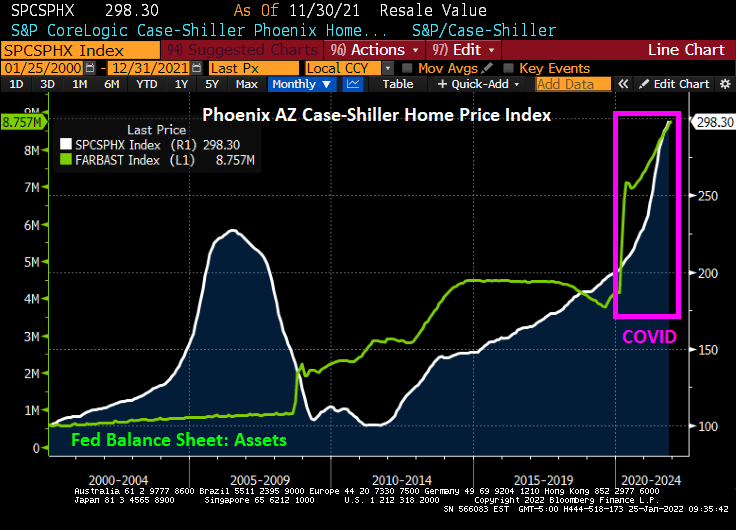

Which metro area is growing the fastest, making housing even more unaffordable for renters? Phoenix AZ is growing at a 32.2% YoY clip while Washington DC is the slowest growing metro area at 11.1% YoY. The second faster growing metro area in Tampa FLA.

Phoenix AZ is growing at the fastest rate in the nation as The Fed still has its monetary stimulus at FULL SPEED AHEAD.

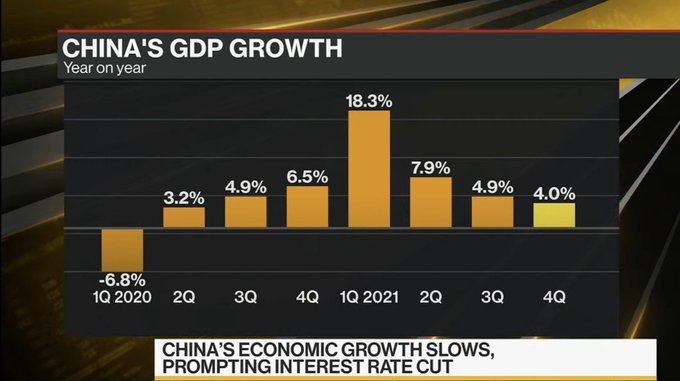

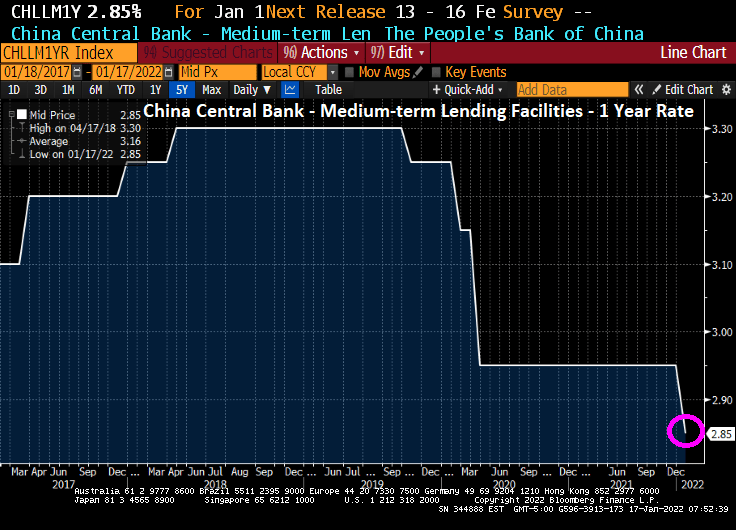

The Chinese Real Estate Developer Debacles continues to spread from Evergrande to other developers as China’s Central Bank cuts rates due to Omicron spread.

First, China’s Central Bank cut their 1 year medium-term lending rate to 2.85% from 2.95%. And the growing malaise in China’s real estate development continues.

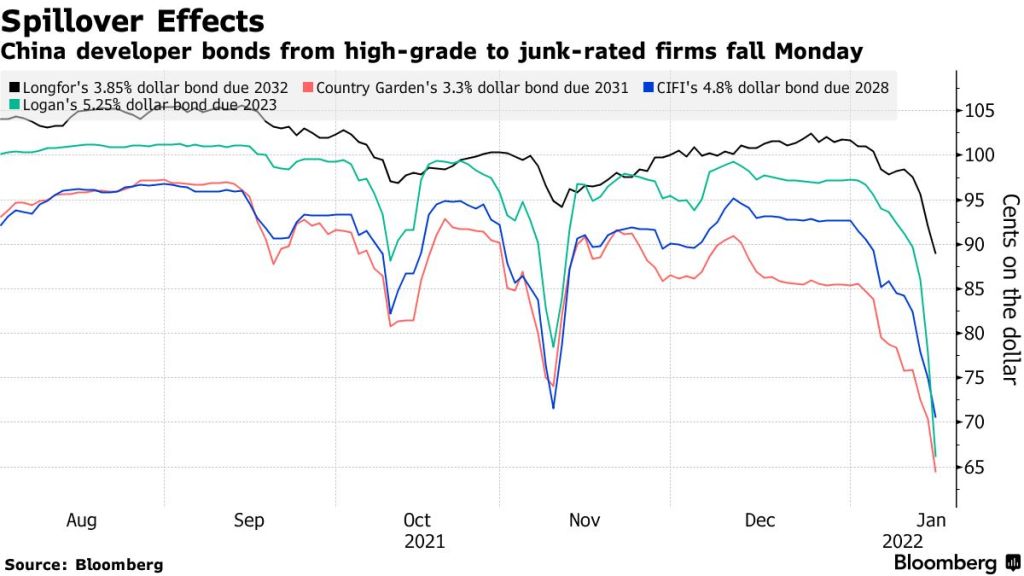

Fresh turmoil rocked Chinese property bonds on Monday on concern over the true scale of the industry’s hidden debts, deepening a selloff among higher-rated firms.

A Logan Group Co. note due 2023 sank 14.1 cents to a record low 62.9 cents after Debtwire reported the developer could be on the hook for $812 million of guarantees on outstanding obligations due through 2023. Country Garden Holdings Co.’s bond due 2024 tumbled 12.9 cents to 67.7 cents, extending last week’s selloff for the country’s biggest developer.

Let’s see if the US Federal Reserve follows through with it rates increases when China is cutting their rates.

If you look at the following chart, you can see multifamily (5+ unit) starts remain elevated (pink box) which is not surprising given that home prices at growing at 19.1% YoY nationally (orange circle) and REAL hourly earnings have declined (yellow triangle) thanks to reemergence of inflation after 40 years.

Then we have the humming dragon, rising mortgage rates, that will reduce housing affordability even further.

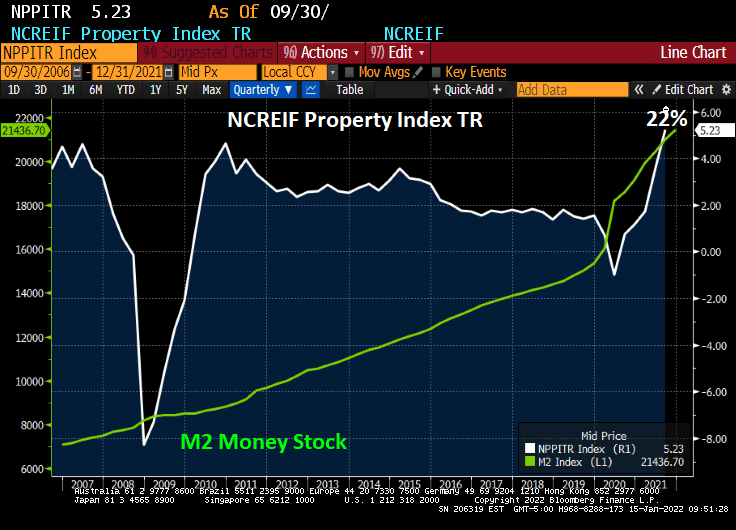

Inflation is burning out of control. While home price growth has been off the cherts (as Jean-Ralphio would say), commercial real estate has jumped incredibly at 22% YoY. The Bloomberg charting function hasn’t updated for the Q4 NCREIF report yet so I had to manually write-in 22% on the following chart.

So, what will happen IF The Fed follows through with its monetary stimulus reduction? JPMC’s Jaime Dimon warns that The Fed could hike 7 times in 2022 and not be ‘sweet and gentle’.

Inflation is the highest in 40 years. There used to be a lot of discussion about hedging against inflation in the 1970s and 1980s, but discussion subsided as inflation cooled in the US. But now it is roaring back as Fed monetary stimulus continues unabated and The Federal government continues to spends like crazy.

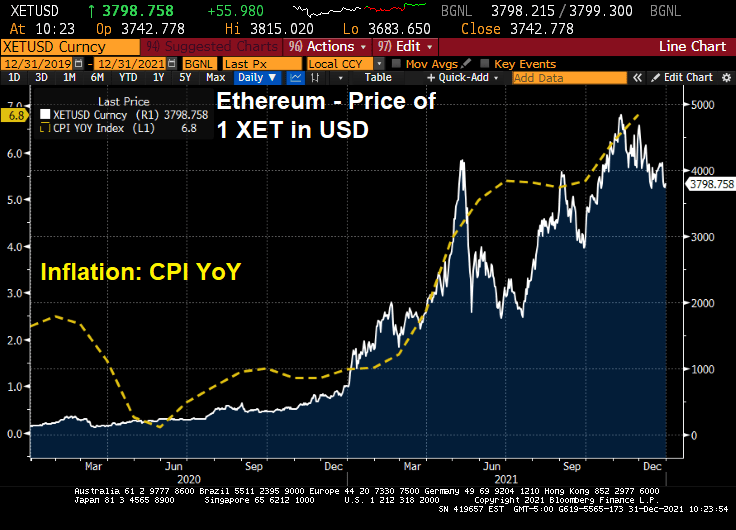

So, how do we protect ourselves against inflation caused by Federal government policies (or follicies)? How about cryptocurrencies like Ethereum?

Ethereum really started to take off as US inflation took off. Not a perfect fit (or hedge), but on average Ethereum has kept up with inflation.

If you believe in technical analysis, Ethereum is in the 3rd wave on the downside.

But if you believe the Ichimoku Cloud, Ethereum lies BELOW the cloud indicating that Ethereum is likely to rise.

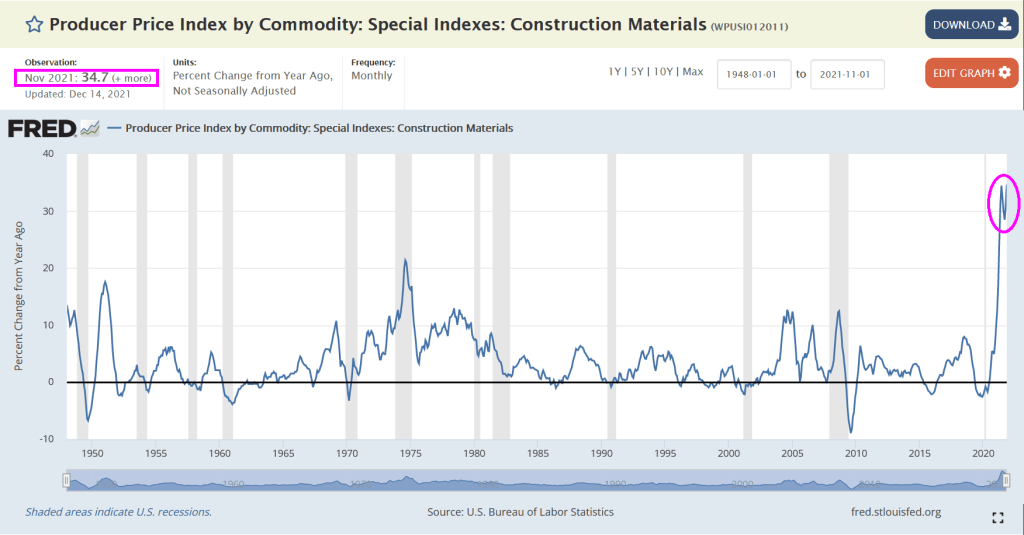

Bear in mind that Biden’s energy policies have created large increases in energy prices which lead to large increases in other products such as food prices. Again, not all inflation is due to Federal policies. Arabica coffee prices are driven by droughts and excessive rainfall, etc. But inflation causes a rise in agriculture prices due to transportation cost increases, increases in fertilizer prices (thank to natural gas price increases), and panic buying by consumers.

Despite what Federal officials jawbone about, inflation has momentum and is unlikely to swiftly subside, particularly if the Build Back (Inflation) Better Act passes in 2022.

Remember, consumer purchasing power of the US Dollar has declined dramatically since the creation of The Federal Reserve System in 1913. The Fed isn’t going away and neither is wasteful Federal spending, like BBB.

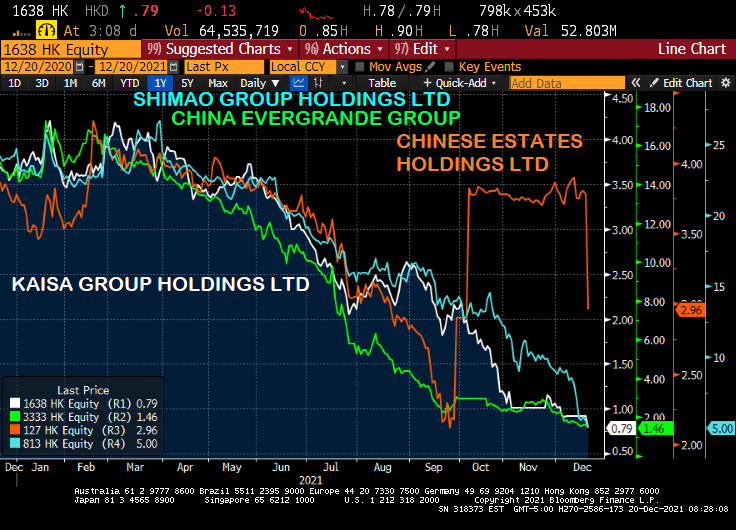

While the Chinese Wuhan virus (aka, the Fauci Flu) has plagued the world, another Chinese “export” is also suffering what is known as contagion: China’s real estate sector.

Real estate companies Evergrande, Kaisa, Shimao and Chinese Estates are falling like a rock today.

But it has been a steady decline since Q1 2021 except for Chinese Estates. But they have resumed their death dive.

On the debt side, Evergrande is down to 18.856 while Kaisa has lost less (but still quite a bit) and Shimao’s bond look almost like a good investment, relative to Kaisa and Evergrande. But they are all sucking wind. Maybe they all have the Fauci Flu?

Let’s see if this latest Chinese “export” washes ashore in the USA.

I love how The Federal Reserve talking heads, the media, economists like Paul Krugman, all refer to inflation as “transitory” and excessive liquidity as “temporary.”

Let’s look at a variety of alternative investments to the S&P 500, GameStop, Bitcoin, Ethereum and Gold after The Federal Reserve’s and Federal government massive (over)reaction to COVID in early 2020. Gold is the first asset to surge after M2 Money surged, but has declined since. Game Stop had a big surge (likely due to positive vibes on Reddit), but has been volatile and generally falling since “The Surge.” Bitcoin had a delayed surge as did Ethereum. Despite fear about government regulation, Ethereum in particular remains elevated.

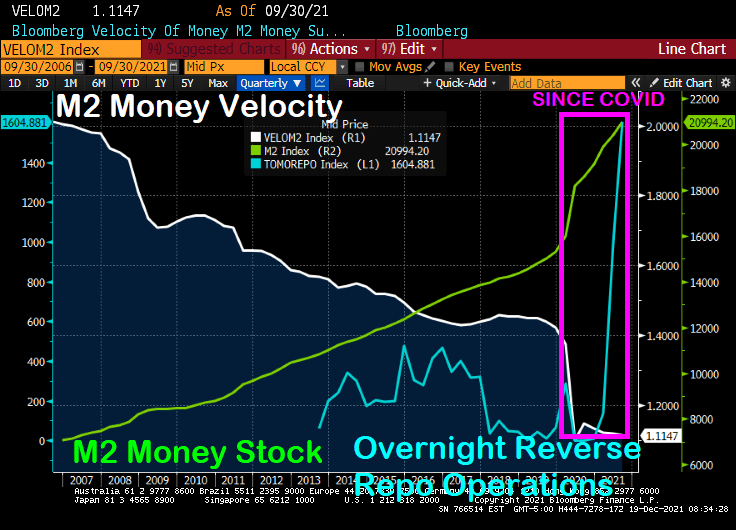

The “temporary” stimulus has resulted in the lowest M2 Money velocity in history. And we will have to see if the “temporary” excess liquidity in the financial system is truly temporary.

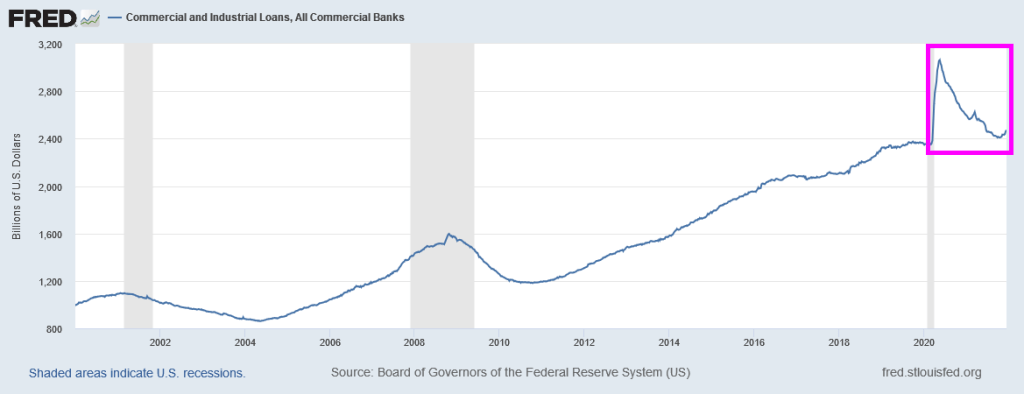

Here is a chart to show the “Stimulytpo” effect on commercial and industrial loans which surged (including PPP loans) but have simmered down to pre-COVID levels.

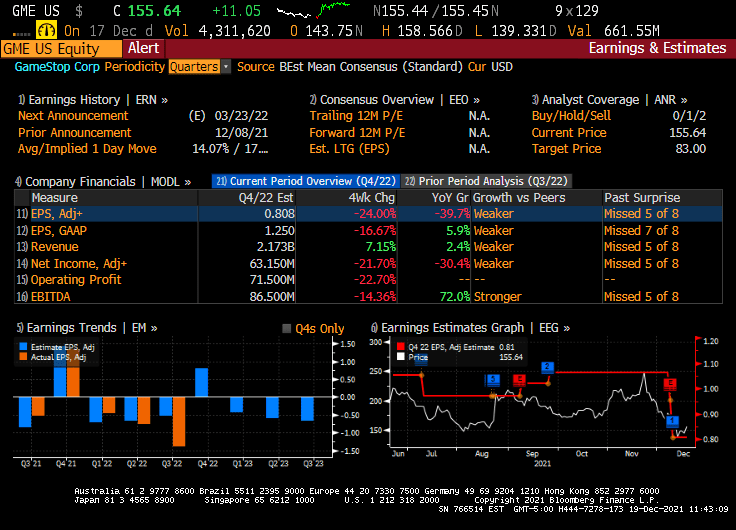

The earnings for GameStop were terrible (down 39.7% YoY). But at least Christmas season is upon us and maybe GameStop will surge with a good retail spending season.

But what happens to markets if the Federal government “stimulypto” is removed? If it ever is.

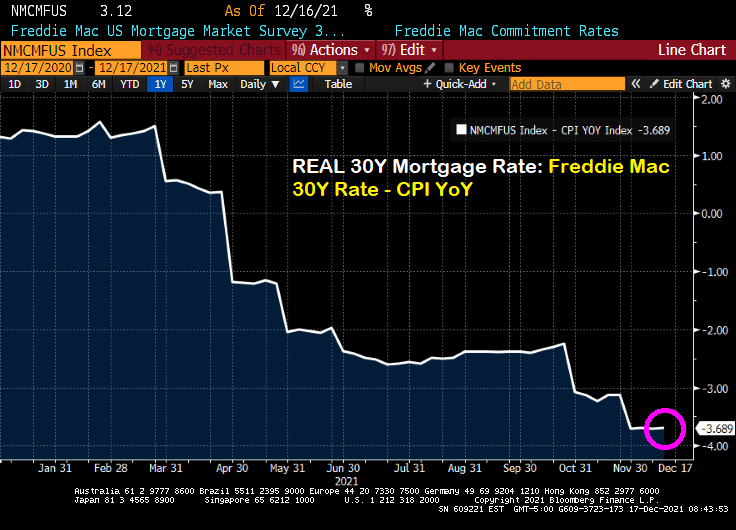

The Freddie Mac 30-year mortgage commitment rate rose to 3.12%. But once we subtract the gut-wrenching inflation rate, the REAL 30-year mortgage rate is -3.689%.

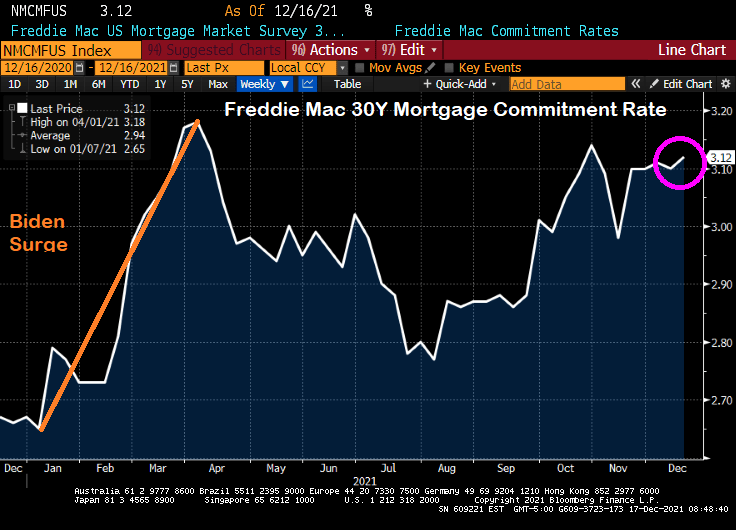

The nominal Freddie Mac 30-year commitment rate rose to 3.12% which is still lower than 3.18% back on April 1, 2021 after surge in rates following Biden’s taking the office of Presidency in January.

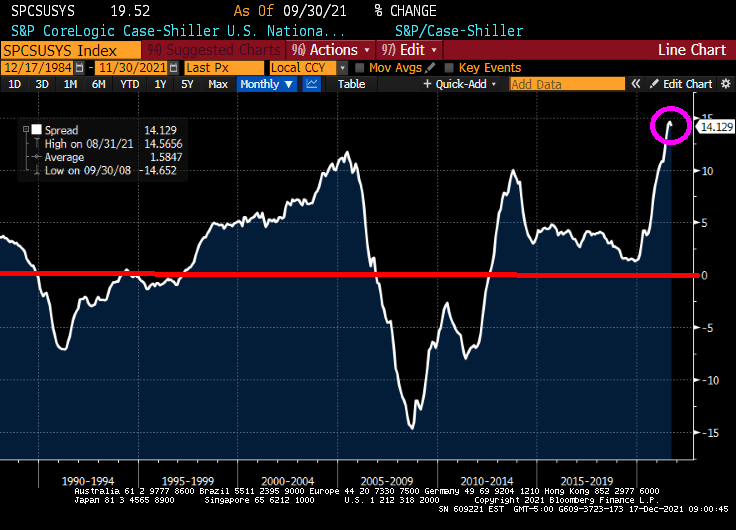

Meanwhile, the REAL Case-Shiller National home price index (CS National YoY – CPI YoY) is growing at the fastest rate in history. Great if you already own a home, but lethal if you are renting and want to move to homeownership.

Meanwhile, REAL wage growth is at -1.94% YoY.

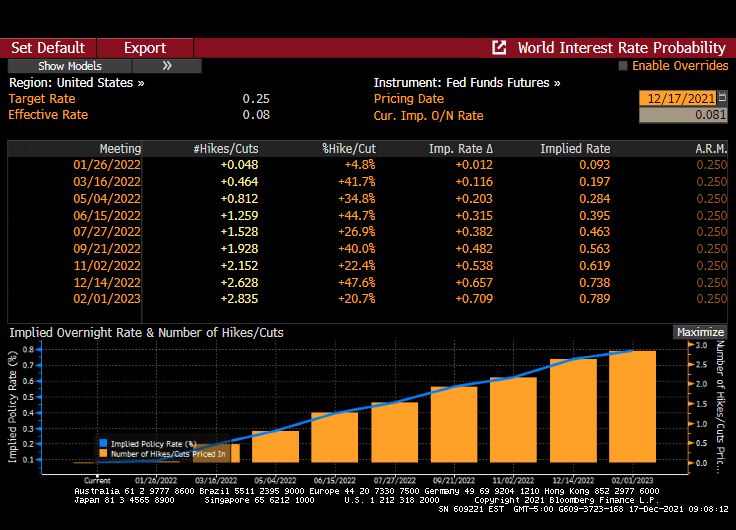

Well, Chairman Powell and The Gang failed to raise the Fed Funds Target Rate yet again, but let us know that they will tighten someday soon. The Fed Funds Futures are signalling a rate hike at the June 2022 meeting and another at the November meeting.

While The Fed couldn’t care less about the Taylor Rule, it is still interesting to note just how out of touch The Fed FOMC is with reality. The Taylor Rule indicates that their target rate should be 16.94% rather than the current target rate of 0.25%.

Keeping the target rate unchanged in the face of gut-wrenching inflation is a bold strategy, Cotton.

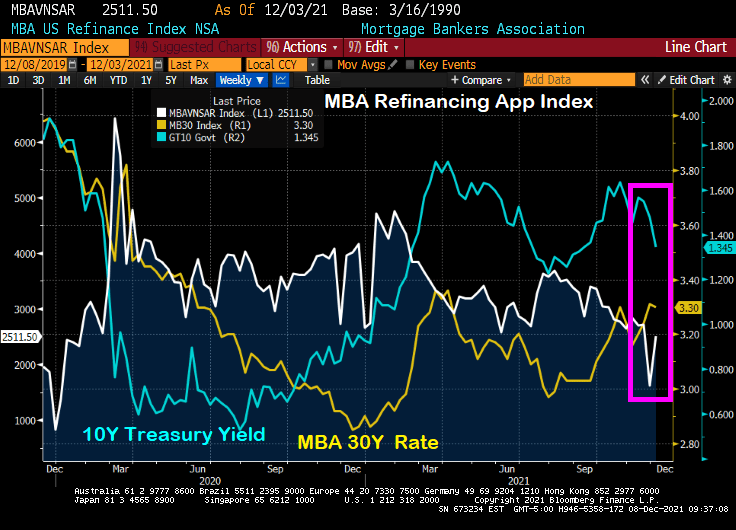

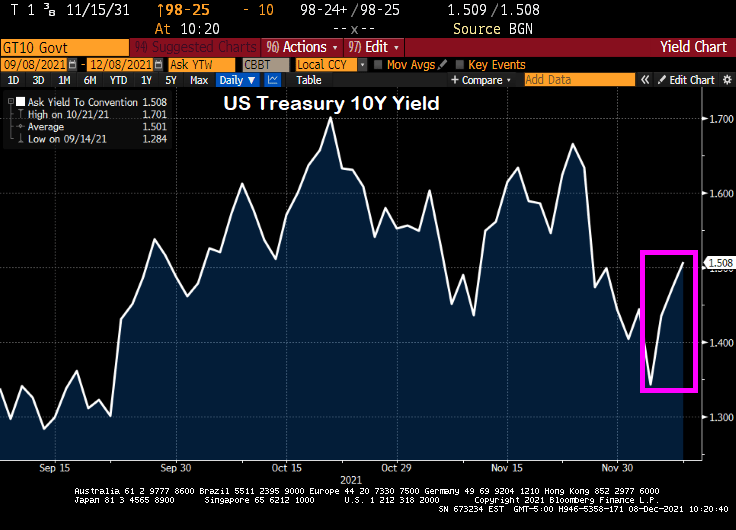

Despite the “Talk, Talk” from The Federal Reserve about balance sheet taper and rate “normalization,” we actually saw the 10-year Treasury yield fall from 1.6651% on 11/23/2021 to 1.343 on 12/3/2021. While the 30-year mortgage rate only fell from 3.31% to 3.3%, it is the SIGNAL that The Fed is sending that people should refinance their mortgages ASAP.

You can see the rise in mortgage refinancing applications of 56% week-over-week (WoW) (white line) with the drop in the 10-year Treasury yield (blue line) despite the relatively small drop in the Mortgage Bankers Association (MBA) tiny drop in their 30-year mortgage rate index.

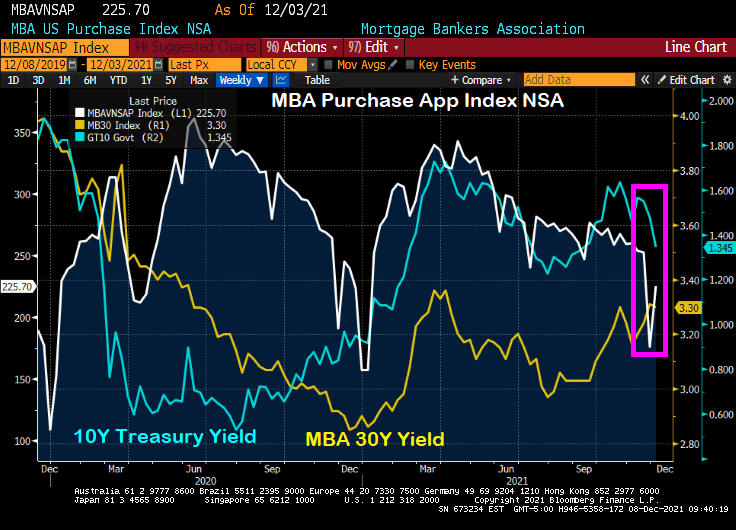

Ditto for the MBA mortgage purchase application index. The drop in the US Treasury yield (blue line) resulted in a 28% WoW increase in mortgage purchase applications.

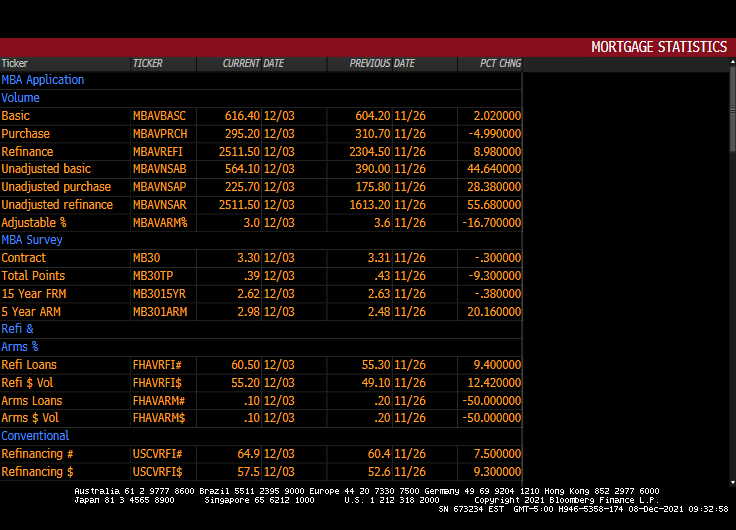

Here is the table of MBA data for the week of 12/03.

Please note that the 10-year Treasury yield have jumped since 12/03 indicating that mortgage application activity for the week of 12/10 will be lower.

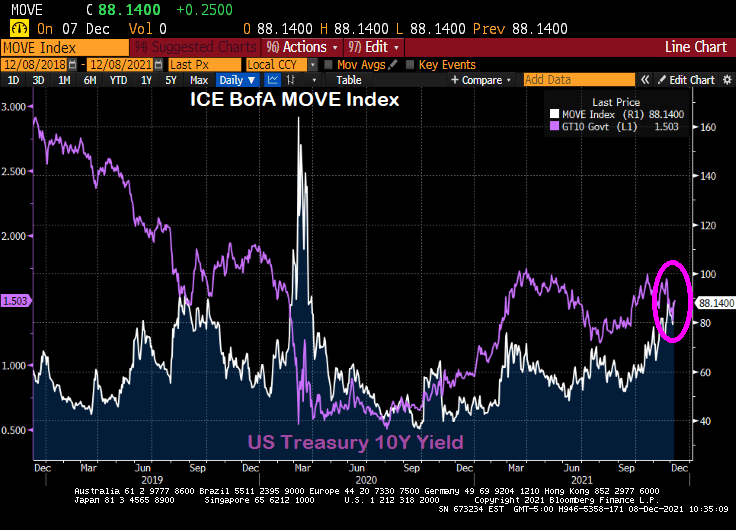

Here is the MOVE bond volatility index and the US Treasury 10-yield chart. Can you spot the COVID outbreak??

You must be logged in to post a comment.