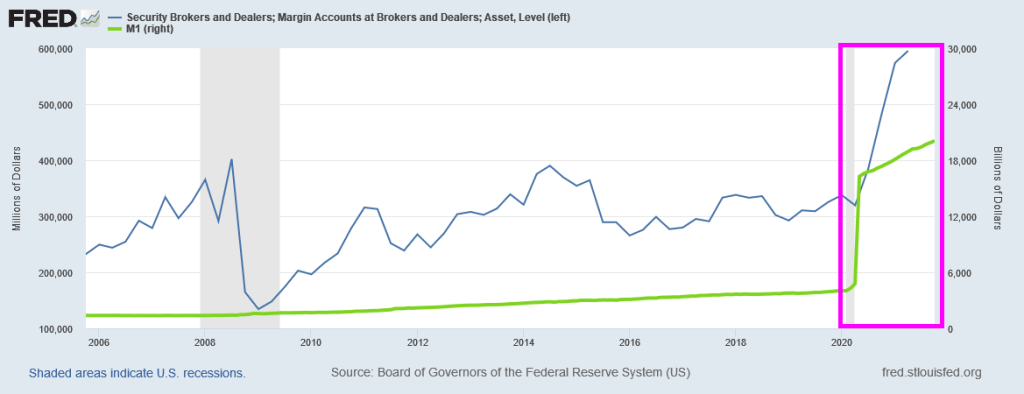

As we are all painfully aware, The Federal Reserve went on a 2nd money printing spree to allegedly stave-off the economic impacts of the COVID outbreak in March 2020. The first money printing spree took place in late 2008 as The Fed tried to stave-off the economic impacts of the housing bubble burst of 2008 and the ensuing financial crisis.

But for now, we have this horrifying chart showing the exploding margin accounts at security brokers and dealers (not, not the Walter White-type dealers, but Wall Street dealers). Notice the 400% surge in M1 Money stock after COVID struck.

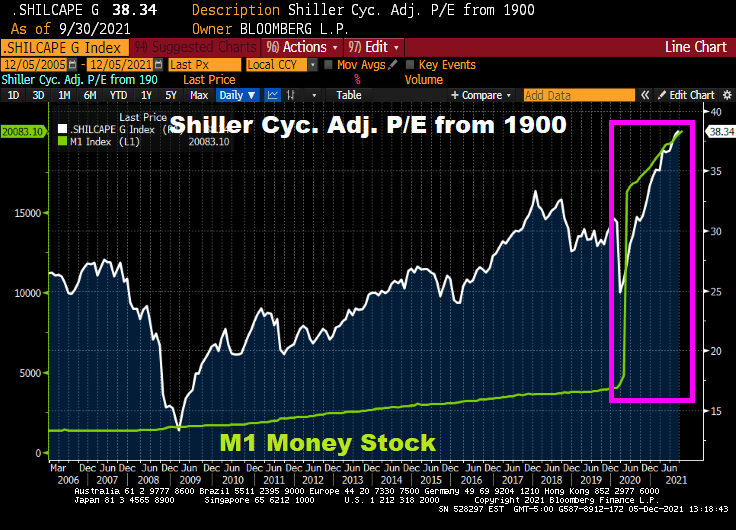

Of course, the soaring stock market is feeding the margin loop, encouraged by The Fed. Check out the Shiller Cyclically Adjusted Price Earnings (CAPE) ratio after The Fed’s M1 printing storm.

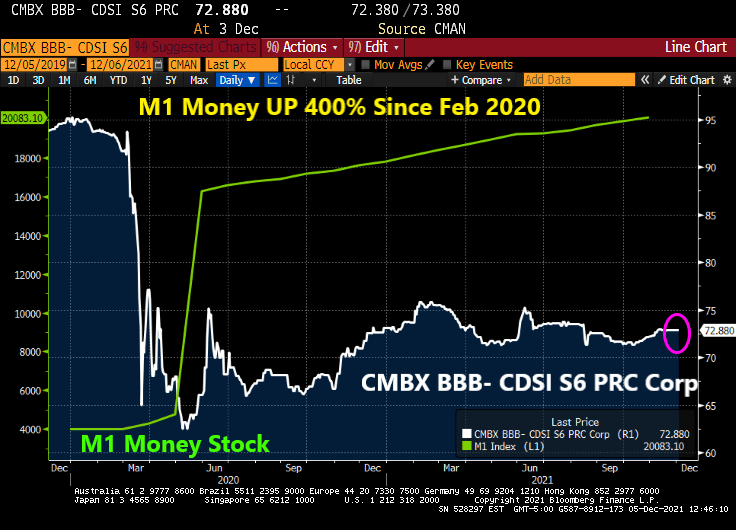

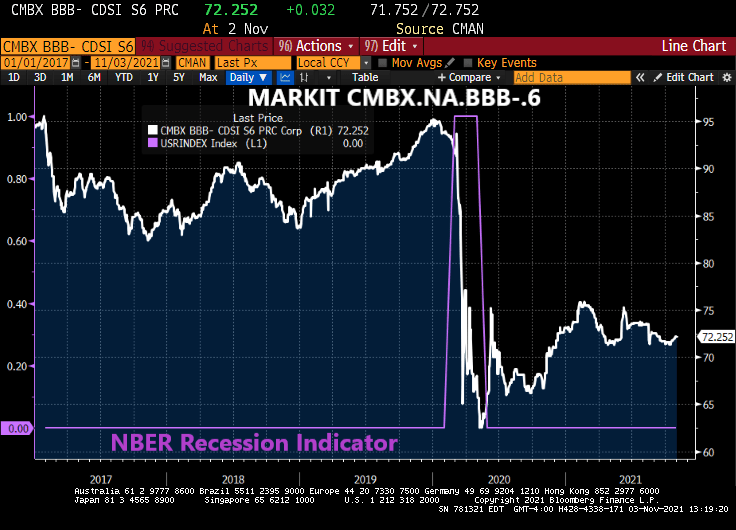

What can’t money printing fix? How about CMBS prices (or CMBX BBB- S6 prices … down 30.5% since just before COVID struck.

Let’s see if The Fed sucks the 400% growth back to zero.

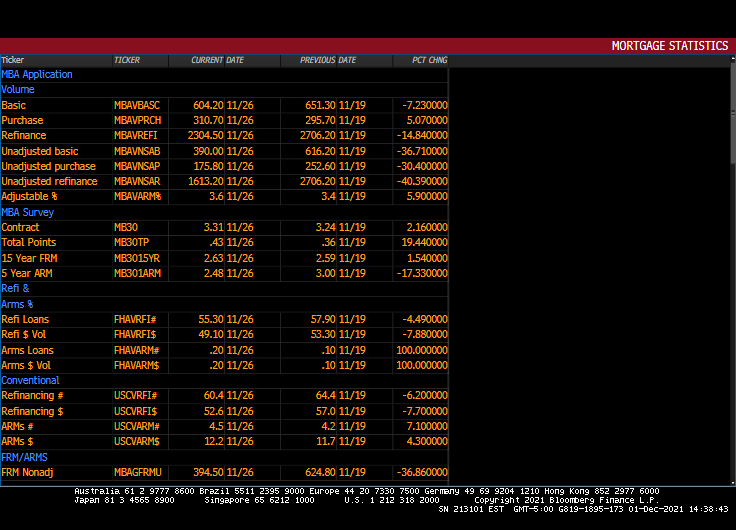

Its that time of year for mortgage purchases applications! Purchase applications usually decline during December and start to rise after the beginning of the year.

Mortgage purchase applications (white line) dropped -30.4% from the previous week, not usual for December. But what is surprising is the drop in REFINANCING applications: down -40.3% from the previous week.

30-year mortgage rates rose 2.16% from the previous week.

But between Omicron (or as the French say, “Oh! Macron!”) and The Federal Reserve, there is a good chance that mortgage rates will fall this week putting a quick end to refi application plunge.

Purchase applications? Nope, it is that time of the season when purchase applications drop like a rock.

I have written numerous times about nothing has been the same since the housing bubble burst and ensuing financial crisis of 2008. The crisis led to bank bailouts (TARP) and banking legislation (Dodd-Frank) giving The Federal Reserve even more power. And then the COVID lockdowns led to even MORE power for The Fed. And a horrid decline in money velocity (the ability of printing money to increase economic growth … or GDP).

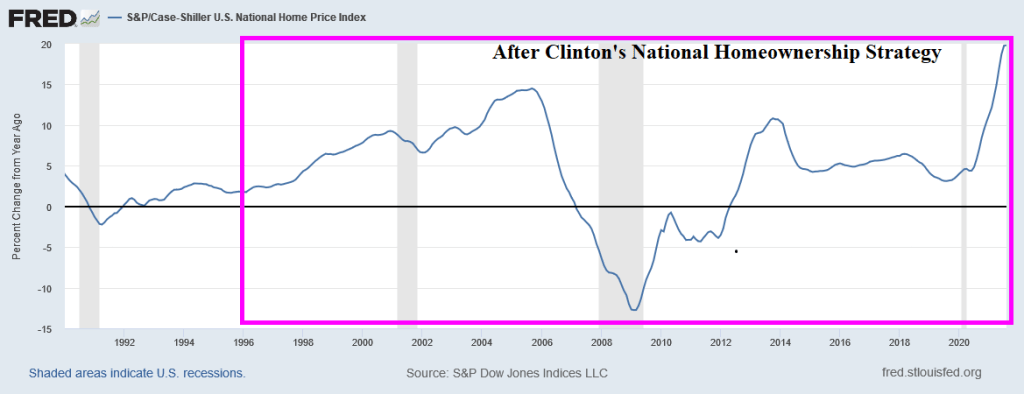

But let’s take one step backwards. One the causes of the housing bubble that burst was President Clinton’s infamous National Homeownership Strategy that encouraged “partners” with the Federal government to soften underwriting standards for mortgage lending, particularly for minority households. The intent was to increase the homeownership rate in the US and it worked! Too well. Along with increasing the homeownership rate came rising home prices, culminating with home price growth reaching 14.5% YoY in September 2005. Only to start slowing to a crash.

Of course, the housing bubble was associated with no/low documentation and subprime mortgage lending. But the relaxing of underwriting standards by the National Homeownership Strategy helped fuel the no/low doc and subprime lending crisis. But weakening underwriting standards to increase homeownership rates is a dangerous strategy.

Note the surge in M1 Money Velocity (GDP/M1) starting in 1994. M1 Velocity grew until Q4 2007, then crashed along with home prices. The second and more sudden crash in M1 Velocity occurred with the COVID outbreak in March 2020 and the ensuing economic lockdowns and the intervention of The Federal Reserve in terms of money printing. M1 Money surged 173% from October 2008 to February 2020 and then another 369% from March 2020 to today. THAT is a Fed Storm Surge!!

M2, the broader definition of money, has not grown as rapidly as M1, but it still grew at an alarming rate. Atlanta Fed President Raphael Bostic blamed inflation on COVID but not The Fed’s insane money printing or government lockdowns. C’mon man!

Finally, the banking crisis (and TARP bailouts) along with COVID have made consumer purchasing power of King Dollar even worse.

Be careful of government strategies to make housing more “affordable” because they seem to make housing more expensive and can help crash the financial system.

Renters in the US are getting clobbered by inflation.

The US Zillow Rent Index All Homes YoY + CPI YoY is one measure of renter misery.

The classic misery index (CPI YoY + U-3 unemployment rate) is 10.80%.

Then there is inflation in food prices, gasoline, heating oil, natural gas, etc.

While Biden is releasing the Strategic Petroleum Reserves (SPR) in order to mitigate the problem that he created by terminating the energy pipelines and oil/natural gas drilling permits in the name of “Going Green!” But on the announcement of tapping the SPR, crude oil futures actually rose.

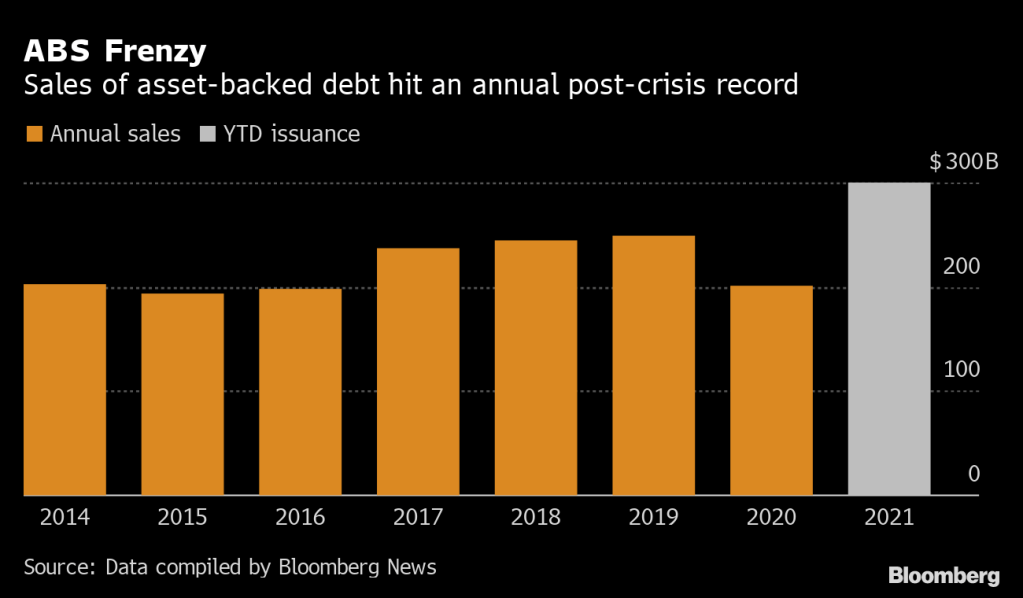

I remember the surge in securitization of loans, receivables, etc during the housing bubble of the mid-to-late 2000s. Today seems like 2007 all over again.

(Bloomberg) — Bankers are repackaging everything from fast food franchises to fitness-center fees into bonds at the fastest clip since the global financial crisis as investors chase yield and inflation protection.

This year’s sales of U.S. asset-backed securities have already surpassed $300 billion, according to data compiled by Bloomberg — and more is expected by year-end. Post-crisis issuance records have also been set in private-label commercial mortgage bonds and collateralized loan obligations, which are also seen accelerating.

“Solar, consumer loans, container lease and whole business transactions to some degree all offer attractive yields and spreads,” said Dave Goodson, head of securitized credit at Voya Investment Management. “These so-called esoteric sectors remain well supported with plenty of money to invest.”

On Monday, Self Esteem Brands, a franchiser of businesses including its flagship gyms Anytime Fitness, priced a $505 million ABS that was backed by franchise agreements, royalties and fees. In whole business securitizations like these, companies mortgage virtually all their assets.

Last month, fried chicken restaurant chain Church’s Chicken sold a $250 million securitization backed by franchise and royalty collateral. Golden Pear Funding recently securitized litigation fees related to financial settlements on everything from personal injury cases to wrongful convictions. And Oasis Financial priced a similar deal linked to payments on medical liens.

Then we have this headline that will send chills through the CMBS market for retail space, particularly at a time when commercial real estate (particularly RETAIL) are trying to recover from COVID lockdowns and the growth of online shopping.

“Retailers Sound Alarm on Organized Theft as States Warn of Rise”

Retailers say shoplifting is getting more brazen in the U.S.: A California Nordstrom store was recently hit by a flash mob of more than 80 people who made off with designer goods, while more than a dozen people pilfered from a Louis Vuitton location in a suburb of Chicago.

On Tuesday, the impact of shoplifting reached Wall Street, with Best Buy Co. shares plunging after the electronics retailer said widespread theft contributed to a decrease in one gauge of profitability. Last month, Walgreens said it would close five San Francisco stores after theft rates there spiked.

Seemingly, no one learns from history. Or as the zen master Yogi Berra once said “It’s like déjà vu all over again.”

Or “You better cut the pizza in four pieces because I’m not hungry enough to eat six.”

President Biden has decided to nominate Fed Chair Jerome Powell for a second term in an effort not to rock the boat. Lael Brainard is nominated for Deputy Chair.

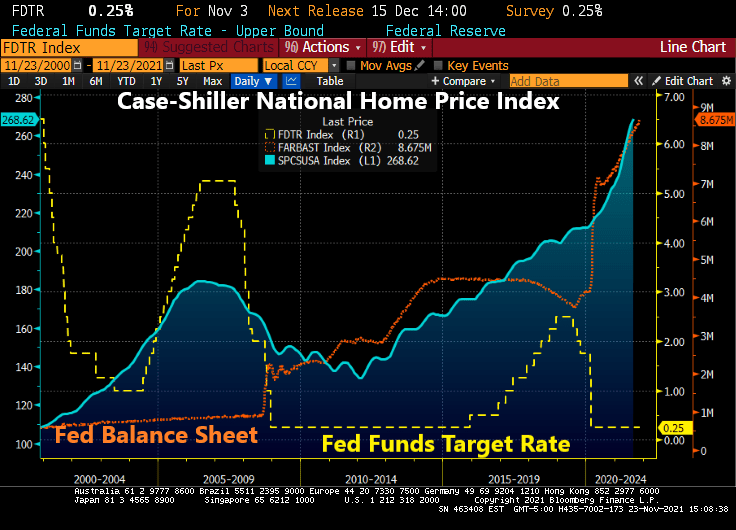

Welcome to The Fed’s Gilded Age … for housing! The gilded age refers to the thin-veneer of gold covering up problems in the late 1800s.

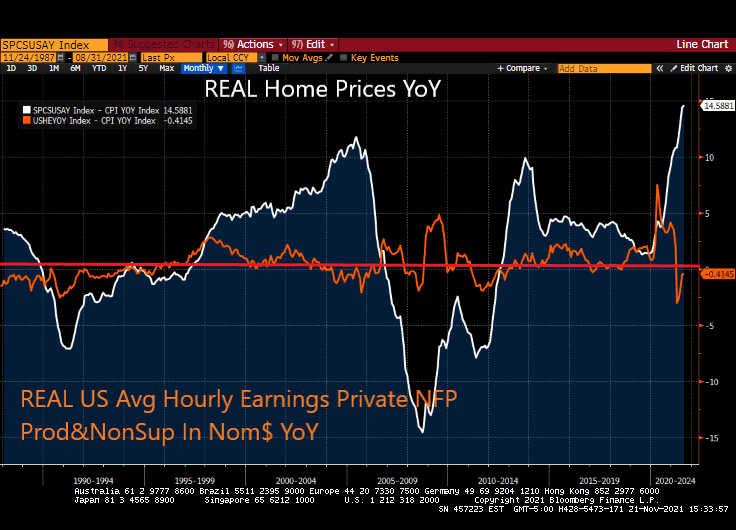

Today’s gilded age is largely fueled by The Federal Reserve’s uber-easy monetary policies combined with absurd Federal government policies. The result? Thanks to inflation, REAL home prices are growing at 14.6% YoY while REAL hourly earnings are declining (-0.41% YoY).

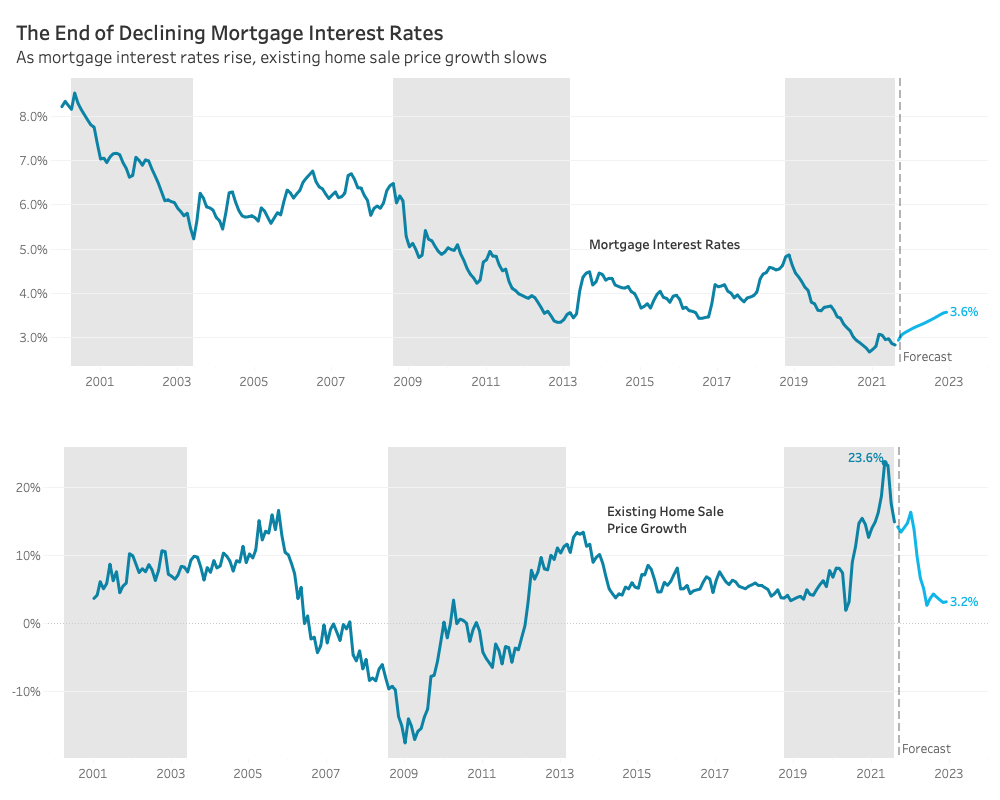

Redfin predicts a more balanced housing market in 2022. Part of their rationale is that they predict mortgage rates will rise to 3.6%. This growth in the mortgage rate is predicted to slow home price growth to 3.2% from double digit growth currently.

While this scenario is plausible, it will require a change in direction of the 10-year Treasury yield which has been declining since 1981. 5.39% YoY inflation may encourage The Fed to raise rates.

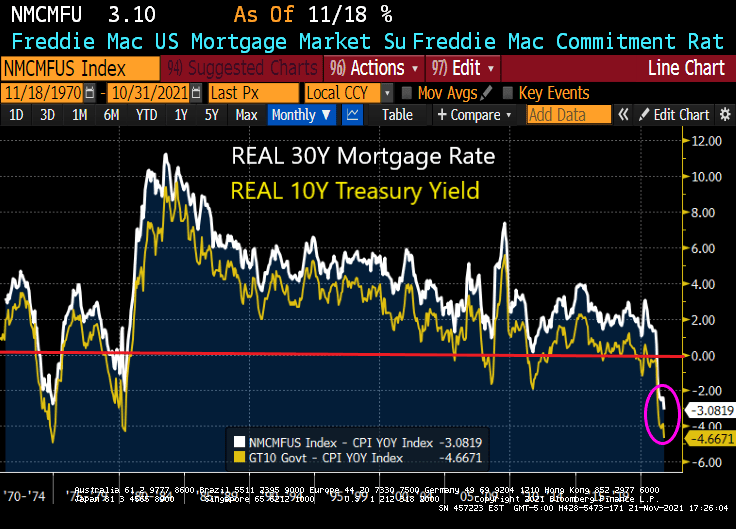

Today’s REAL 30-year mortgage rate is -3.08% while the REAL 10-year Treasury yield is -4.67%. It will require a reduction in inflation AND an increase in the nominal rate to get to 3.6%.

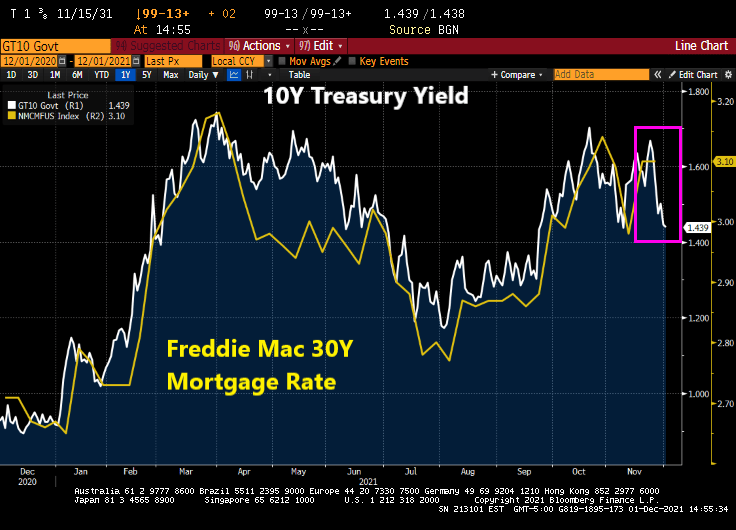

With the Freddie Mac 30-year survey rate at 3.10, will a 50 basis point increase in mortgage rates send the market crashing? Not likely.

After all, the US economy is under the thumb of The Federal Reserve.

US housing starts for October were less than expected. A 1.5% increase MoM was expected, but housing starts actually fell -0.7% MoM.

5+ unit (multifamily) starts were up 6.82% MoM. 1-unit single family detached units were down -3.89% MoM. Permits to build were up 4% MoM.

On a YoY basis, 1-unit start declined -10.6% as M2 Money growth continues to fall.

And 1-unit housing starts have fallen with the rapid decline in home buying sentiment.

1-unit starts have slowed to pre-COVID levels, thanks in part to The Federal Reserve’s money printing bonanza which may never end.

As housing sentiment crashes (due to rapid home price growth), we are seeing the demand for multi-family housing rise. 5+ unit (multifamily) starts were up 6.82% MoM in October.

Nothing has been the same since Covid struck in early 2020.

CMBX BBB-, the reference basket for CMBS 6, was climbing to around $95 prior to the Covid outbreak and resulting recession. The CMBX reference basket is now at $72.25.

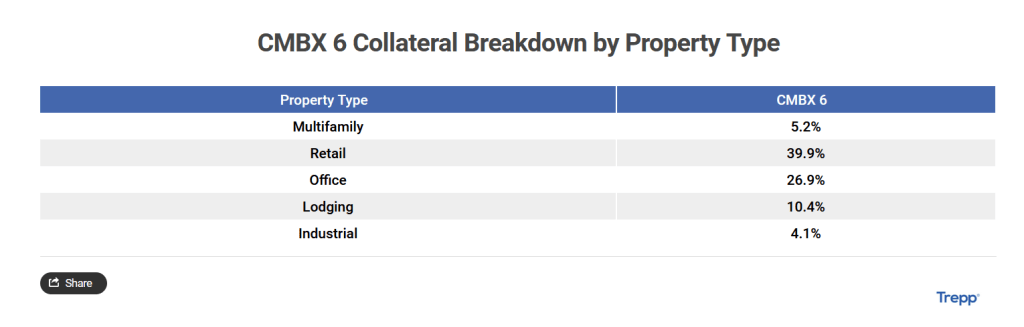

CMBX 6 is largely composed of retail and office, both hit hard by Covid and the ensuing lockdowns and fearmongering by the Federal government and main street media.

You must be logged in to post a comment.