Bidenomics is where the Attorney General Garland gives Hunter Biden blanket amnesty and arrests Biden’s Presidential opponent. Welcome to the United Venezuelan States of America!e

But while Fitch cited “the expected fiscal deterioration over the next three years, a high and growing general government debt burden, and the erosion of governance relative to ‘AA’ and ‘AAA’ rated peers” as reasons for the downgrade, the Biden administration is of course blaming Donald Trump and his supporters due to one portion of Fitch’s explanation: “a steady deterioration in standards of governance over the last 20 years,” and that “repeated debt-limit political standoffs and last-minute resolutions have eroded confidence in fiscal management.”

Then on Wednesday, Fitch’s Richard Francis told Reuters that the downgrade was ‘due to fiscal concerns and a deterioration in U.S governance as well as polarization which was reflected in part by the Jan. 6 insurrection.’

“It was something that we highlighted because it just is a reflection of the deterioration in governance, it’s one of many,” he said, adding “You have the debt ceiling, you have Jan. 6. Clearly, if you look at polarization with both parties … the Democrats have gone further left and Republicans further right, so the middle is kind of falling apart basically.”

And so of course, the Biden administration is blaming Trump.

“This Trump downgrade is a direct result of an extreme MAGA Republican agenda defined by chaos, callousness, and recklessness that Americans continue to reject,” said Biden re-election campaign spokesman Kevin Munoz. “Donald Trump oversaw the loss of millions of American jobs, and ballooned the deficit with the disastrous tax cuts for the wealthy and big corporations.”

Ah, so now it’s the Trump downgrade™

Meanwhile, White House spox Karine Jean-Pierre also blamed Trump on Tuesday, saying that the White House “strongly” disagrees with the decision, adding “it’s clear that extremism by Republican officials — from cheerleading default, to undermining governance and democracy, to seeking to extend deficit-busting tax giveaways for the wealthy and corporations — is a continued threat to our economy.”

Former Clinton Treasury Secretary Larry Summers called the decision “bizarre and inept,” while former Obama economic advisor Jason Furman called the move “completely absurd.”

On Wednesday, CNBC wheeled out Jared Bernstein, chair of Biden’s Council of Economic Advisers and former Obama official, who similarly blamed Trump.

“I think again the timing issue is is Jermaine here. The deficit went up every year under President Trump. The debt to GDP ratio rocketed under President trump. It has stabilized admittedly at a higher level under this president but we’re doing all we can to try to ameliorate those tensions,” he said.

Bernstein reflected on the “cognitive dissonance” he felt at the downgrade amid the success of ‘Bidenomics’ commenting that “creditworthiness deteriorated significantly under President Trump for good reasons… and under President Biden, it started to track back up…”

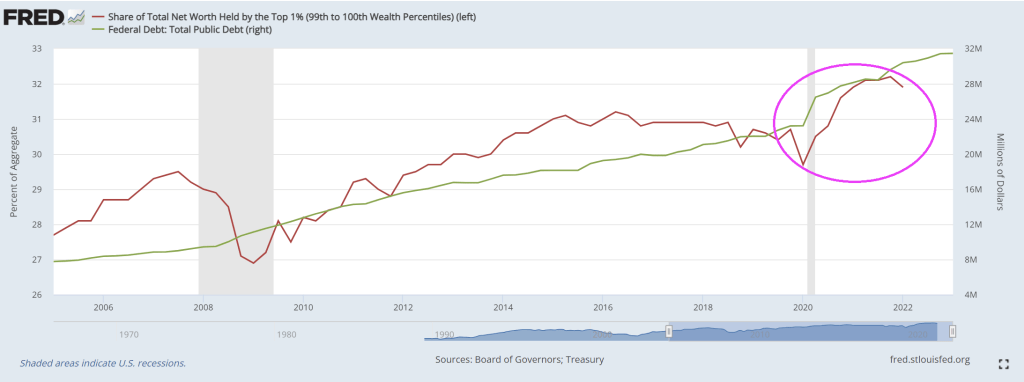

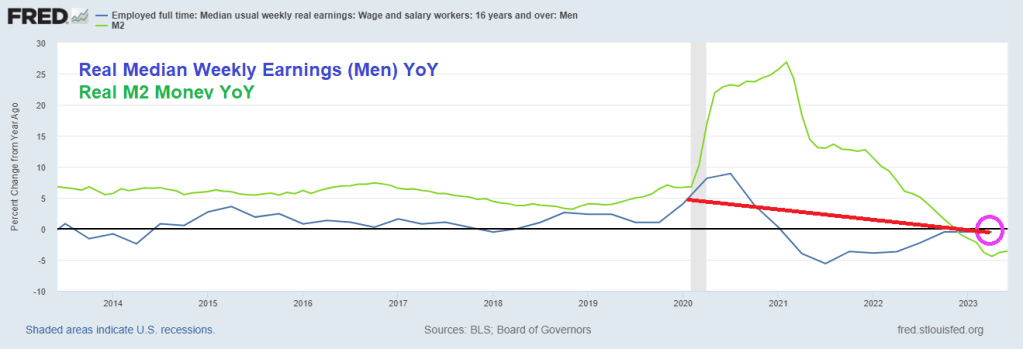

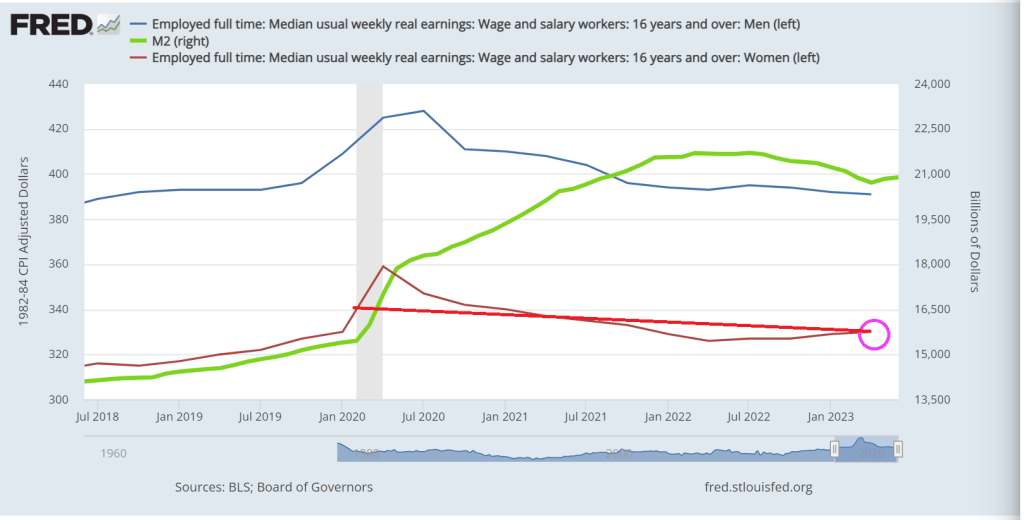

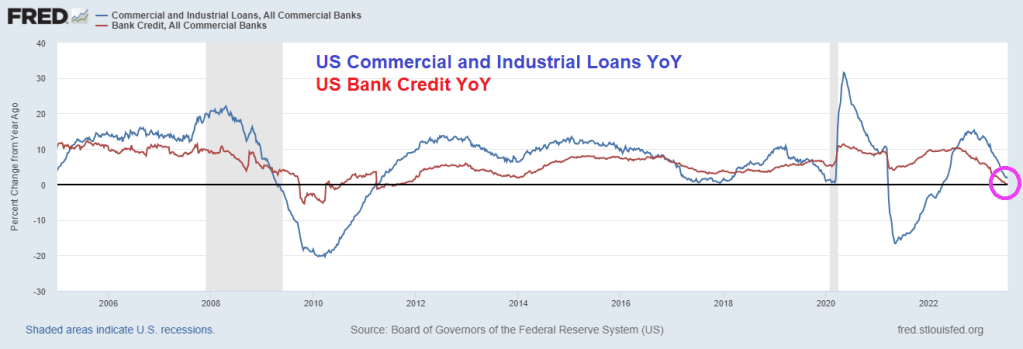

Except that’s the exact opposite of what happened. According to the 100% non-partisan “market”, the creditworthiness of US Treasury debt improved almost constantly under President Trump and worsened dramatically almost immediately upon President Biden’s inauguration:

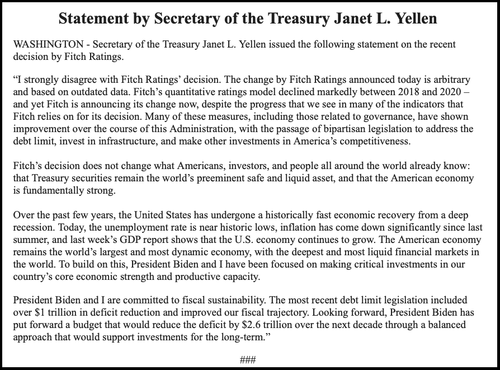

Treasury Secretary Janet Yellen said that the downgrade was “arbitrary and based on outdated data,” adding “Today, the unemployment rate is near historic lows, inflation has come down significantly since last summer, and last week’s GDP report shows that the U.S. economy continues to grow.”

CNN also blamed Trump, penning the headline: Fitch downgrades US debt on debt ceiling drama and Jan. 6 insurrection.”

The stupidity on CNN and Jared Bernstein are appalling. True, the media and Biden Administration are terrified of losing the 2024 Presidential election, but outright lies and misrepresenation are wrong no matter what.

But the claims that the US was downgraded because Trump’s economy lost miilions of jobs is ridiculous.

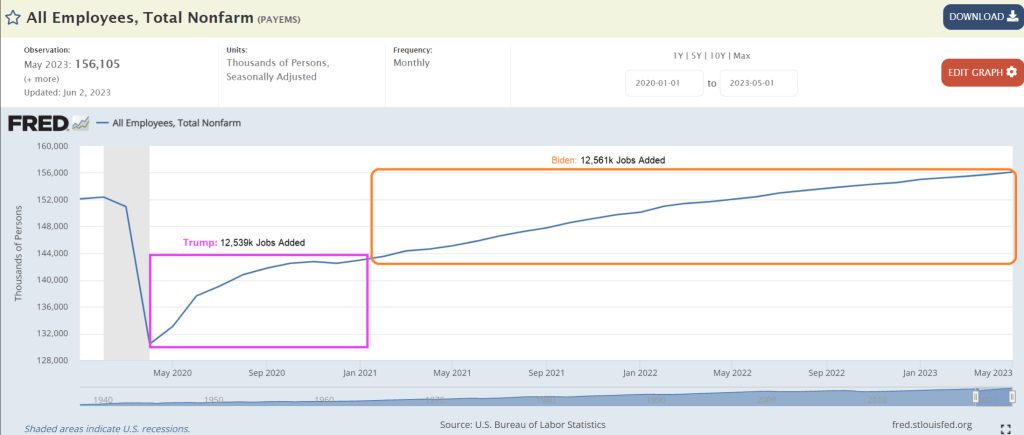

Actually, the US economy added 12.53 million jobs after April 2020 (Trump) while Bidenomics created took 2 1/2 years to add 12.56 million jobs. So, Biden took over twice as long to create jobs after Covid than it did under Trump. Simply opening the economy and schools produced that magical claim by Biden. And the National Teacher’s Union and Randi Weingarten worked with Fauci to orchestrate shutting down schools. Blaming Trump for local governments shutting down the economy is pure bunk.

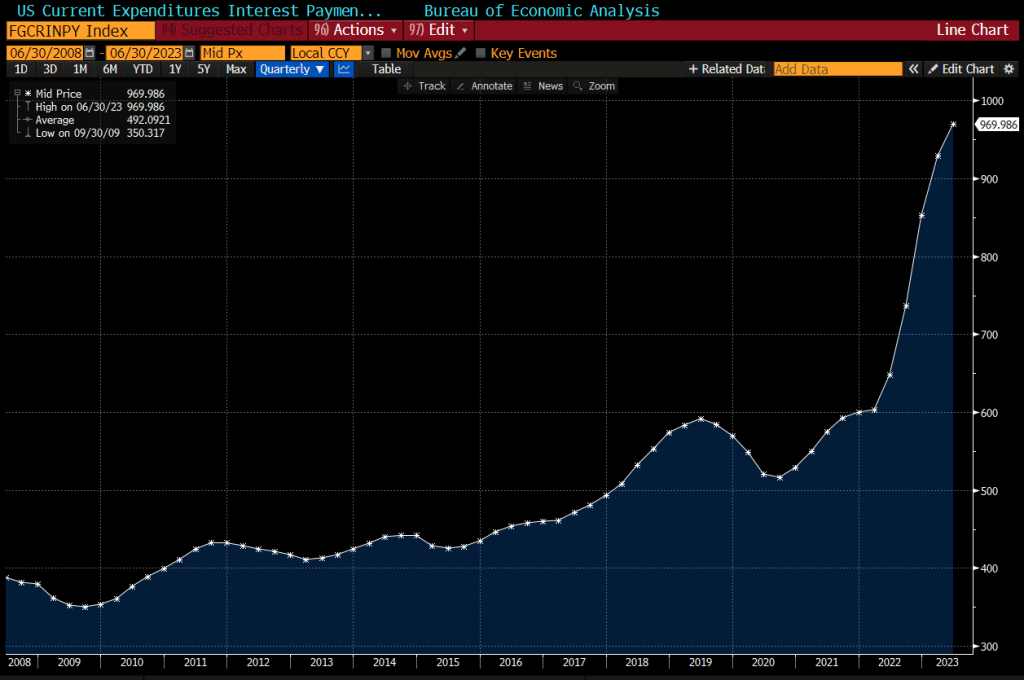

Bidenomics and massive Federal spending is the cause for the downgrade. Not Trump.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.