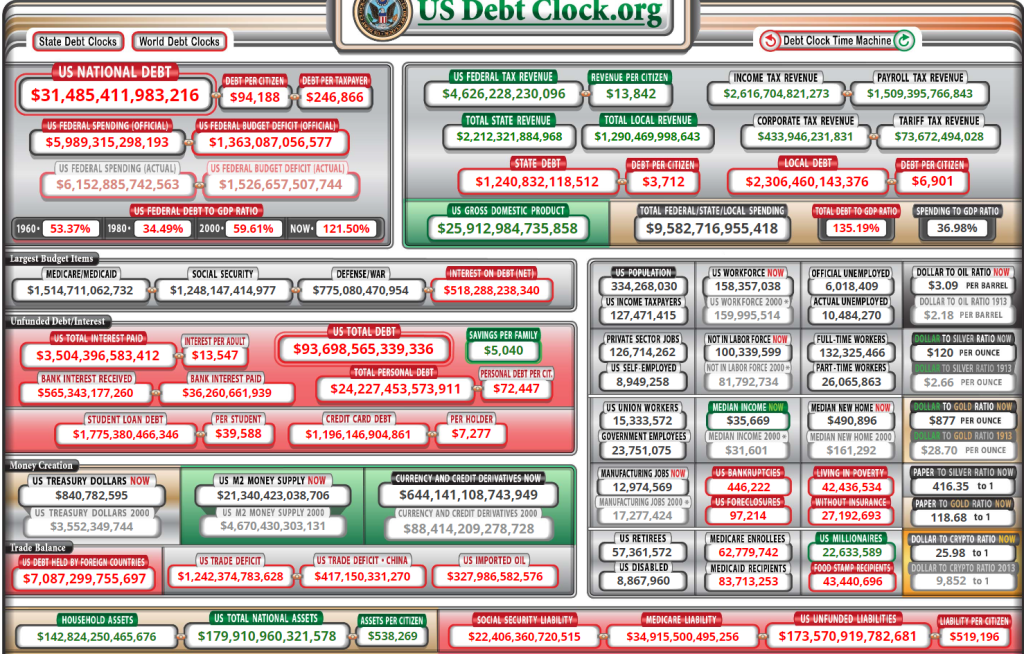

Its that time again when Congress does its Kabuki Theater drama about raising the US debt limit. Of course, everyone in Congress and the Biden Administration want to spend trillions of dollars so they will hike the debt limit.

With the US government facing the danger of a payments default later this year, Congress has a variety of paths to avert economic disaster and boost the debt ceiling.

All of them would likely involve going right up to the market-rattling brink, according to current and former lawmakers and aides.

The timeline kicks off within weeks, when Treasury Secretary Janet Yellen is expected to advise that the government will deploy extraordinary accounting measures to avoid running out of cash. Those steps are forecast to be exhausted after July.

Republicans now in control of the House are demanding deep spending cuts as the price for an increase in the ceiling, while President Joe Biden and congressional Democrats reject such an outcome.

Nothing has been the same since the financial crisis of 2008 and the ascension of all-time big spender Nancy Pelosi as House Speaker. Budget deficits have never been the same. The last budget surplus was under House Speaker Newt Gingrich. But since the financial crisis of 2008, Federal spending seems to have increased its trajectory.

Note that mandatory spending (Medicare, Social Security, etc) is growing like a wild fire while discretionary spending is seemingly flat. So, it mandatory spending that Congress will pretend to cut.

Yes, it is Medicare for our aging population that has blown out of control.

Then we have defense spending. The Ukraine spending should come from this pot, but forces decisions to make between Ukraine and taking care of our Navy (to compete with the growing Chinese navy).

Of course, as The Fed fights inflation, we are seeing the COST of Federal debt soaring since Covid.

Yes, Congress NEEDS to cut back the spending, particularly on Social Security and Medicare (not to mention Ukraine spending), but it is all Kabuki theater. Queue the screams of “Republicans will take away …”.

I wish everyone in Congress were like Kentucky U.S. Senator Rand Paul, not the other spendaholic Kentucky Senator.

2022 is one of the record books and not in a Tiger Woods way. Call it a year of pain.

First, the US enacted policies that drove up energy prices (goin’ green) that reverberated through the entire economy in the form of higher prices. Second, The Federal Reserve, in attempt to combat runaway inflation, started removing the excessive monetary stimulus that had been around since Fed Chair Bernanke initiated QE, the seemingly unlimited purchase of Treasury and Agency MBS securities. Janet Yellen continued the massive asset purchases and zero interest rate policies or ZIRP. Now that inflation has struck the American middle class hard, we are seeing Fed Chair Powell doing what Bernanke and Yellen wouldn’t do — remove the monetary punchbowl.

Using Robert Shiller’s on line data, US stocks and bonds have had an awful year, the worst combined year since 1871.

US equity returns have been demolished under the NEW dual mandate (goin’ green = rising prices = Fed tightening).

Let’s see how two of the most famous investment gurus did in 2022, Warren Buffet and Cathie Wood. Buffet’s Bershire Hathaway Class A equity was UP 4% in 2022, while Cathie Wood’s ARK Innovation ETF collapsed by -67% in 2022.

Here is the clinker. The US economy (as well as the global economy) seem dependent on “cheap money” from Central Banks like The Federal Reserve. So the question is … will The Fed pivot? Fed talking heads are saying no, but Fed Funds investors are saying yes to a pivot after June 2023.

Ulysses S Grant was the President the last time the combined stock and bond market was this bad.

Do I detect a trend in the US Leading Economic Indicator data?

The Conference Board’s US Leading Economic Indicator was released this morning and it wasn’t pleasant. The US Leading Index was down -1% MoM in November.

On a year-over-year basis, it is down -4.5% YoY as The Fed withdraws its massive monetary stimulus.

The good news … for military contractors … is that Biden and Congress have given Ukraine’s Zelenskyy ANOTHER $47 BILLION.

The Federal Reserve forecast for the US economy is a dismal 0.50% YoY. Do I detect a trend?

The FOMC forecast for 2023 and 2024. Core PCE YoY (inflation) is forecast to drop to 3.50%, still considerably higher than The Fed’s target rate of inflation of 2%. And unemployment is forecast to be 4.60%.

To cope with Bidenflation, US personal savings rate as of October is -67.9% YoY. The “good” news is that rents YoY are crashing. But food prices under Inflation Joe remain very high. But most everything is slowing down, not due to Biden’s policies, but a global and US economic slowdown.

With a big slowdown coming our way, you can understand why The Fed’s December Dot Plot is showing declining Fed Funds Target rate starts declining in 2024.

Even US mortgage rates are headed down.

Speaking of going down, cryptos are down across the board with Cardano leading the decline at -6.91%.

The numbers coming out today are not good. November numbers were 1) US Industrial Production was down -0.2% MoM, 2) manufacturing production is down -0.6%, 3) retail sales advanced down -0.6% (most in 11 months) and …

The Empire State Manufacturing outlook was down -11.2% and the Philadelphia Fed (or Phed) business outlook was down -13.8% in November.

And with all this bad news, global equity markets are dropping like a paralyzed falcon.

But at least Biden traded a dangerous international arms dealer for WBNA star Brittney Griner. Possilby the worst trade in history after the Chicago Cubs traded future Hall of Famer Lou Brock for sore-arm pitcher Ernie Broglio. Griner is Ernie Broglio.

Central bankers won’t ride to the rescue when growth slows in this new regime, contrary to what investors have come to expect. They are deliberately causing recessions by overtightening policy to try to rein in inflation. That makes recession foretold. We see central banks eventually backing off from rate hikes as the economic damage becomes reality. We expect inflation to cool but stay persistently higher than central bank targets of 2%.

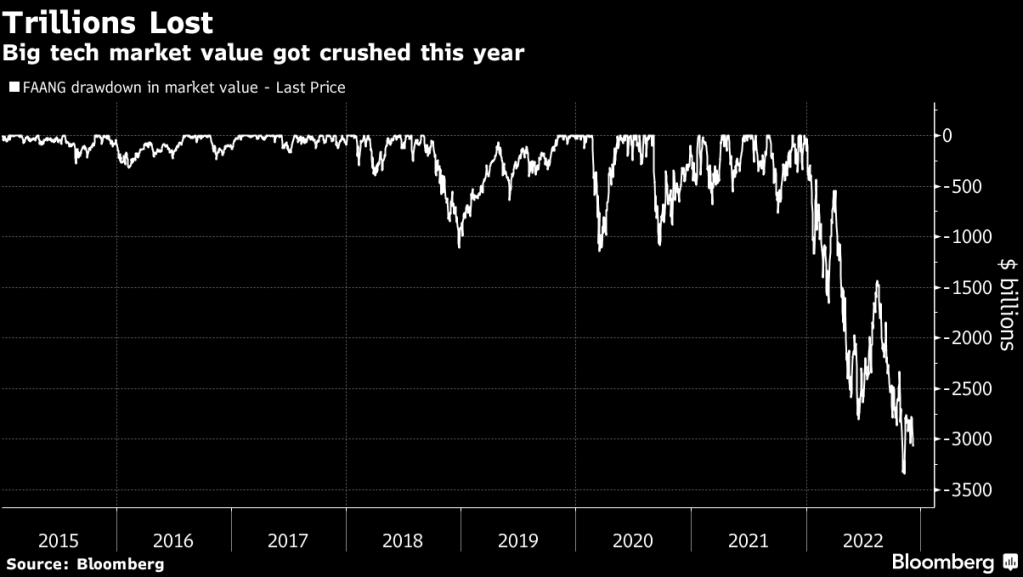

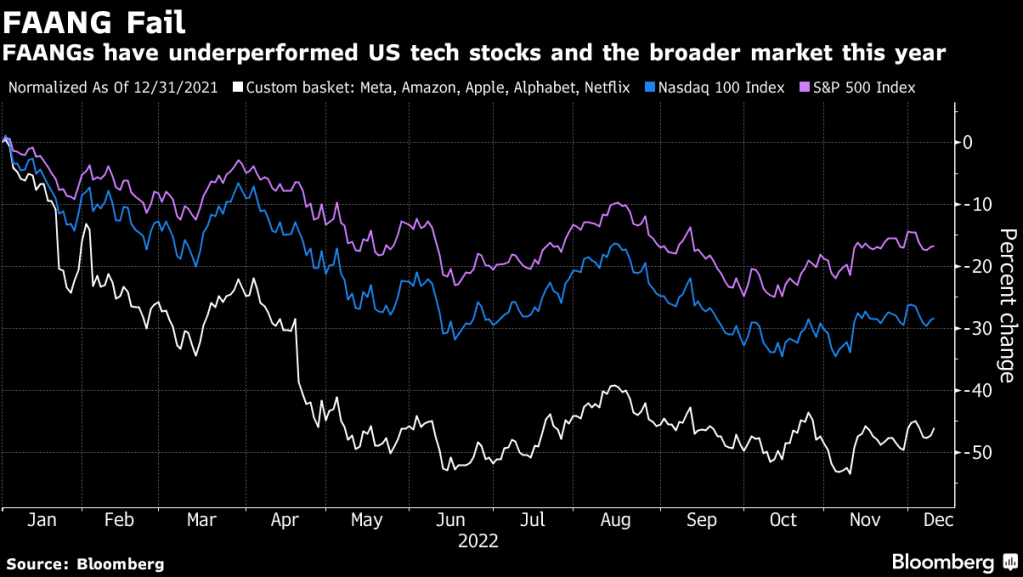

For some investors, this year’s rout in high-flying technology stocks is more than a bear market: It’s the end of an era for a handful of giant companies such as Facebook parent Meta Platforms Inc. and Amazon.com Inc.

Those companies — known along with Apple Inc., Netflix Inc. and Google parent Alphabet Inc. as the FAANGs — led the move to a digital world and helped power a 13-year bull run. And FAANG drawdown have reached over $3 trillion.

FAANGs (Meta, Amazon, Apple, Alphabet, Netflix) are getting clobbered in 2022.

Typically, when The Fed prints too much money, such as 10% or higher (red line), inflation follows. Particularly when The Fed prints at 25% YoY in Q4 2020, it was followed by the highest inflation rate in 40 years. But if M2 Money continues to slow, inflation will likely slow, but not to The Fed’s target of 2%.

Despite what Minneapolis Fed’s Neal Kashkari said about The Fed having infinite printing resourses, The Fed is going to fight inflation THAT THEY HELPED CAUSE. Biden’s energy policies (did you see that Elon Musk has a car that uses plentiful hydrogen?), and excessive Federal spending by Biden/Pelosi/Schumer, are culprits in creating the supply chain problems facing America. BUT after the 25% surge in M2 Money in 2020 and 2021, we saw M2 Money VELOCITY crash and burn to its lowest level in history. Which means the “bang for the buck” for printing more money is negligible.

Of course, big tech firms got caught influencing the 2020 Presidential election (see Musk’s release of Twitter files) and engaged in restriction of the 1st Amendment (Freedom of Speech). How much will that impact FAANG stocks going foward?

And yes, the US Treasury yield curve is inverted pointing to a recession in 2023.

And yes, apparently Biden was complicit in the Twitter fiasco.

US producer prices rose in November by more than forecast, driven by services and underscoring the stickiness of inflationary pressures that supports Federal Reserve interest-rate increases into 2023.

The producer price index for final demand climbed 0.3% for a third month and was up 7.4% from a year earlier, Labor Department data showed Friday. The monthly gains for October and September were revised higher.

At the same time, the annual increase was the smallest in 18 months, extending a months-long easing and suggesting the central bank still has scope to pause its rate hikes next year as expected. Cooler demand at home and abroad has taken some stress off supply chains.

The data come just days before the release of the closely watched consumer price index, which is forecast to show inflation, while much too high, continues to decelerate.

While PPI is declining, it is still far above The Fed’s inflation rate of 2% (red line).

Watch out for energy prices when the sleeping giant (China) opens up again and demand for energy skyrockets. Meanwhile, Clueless Joe is merrily draining the US Strategic Petroleun Reserve.

Lastly, congratulations to former Cleveland Brown QB Baker Mayfield for winning with the LA Rams against the Las Vegas Raiders with a stunning 99 yard drive for a TD at the end of the game.

The Fed has signaled the terminal rate will likely be around 5% — we think an upper bound of 5% — reached in early 2023. To get there, the central bank will likely raise rates by 50 basis points at its December 2022 meeting, followed by two more 25-bp hikes in 2023. We then see it holding at 5% throughout the year. Markets have priced in a similar amount of tightening.

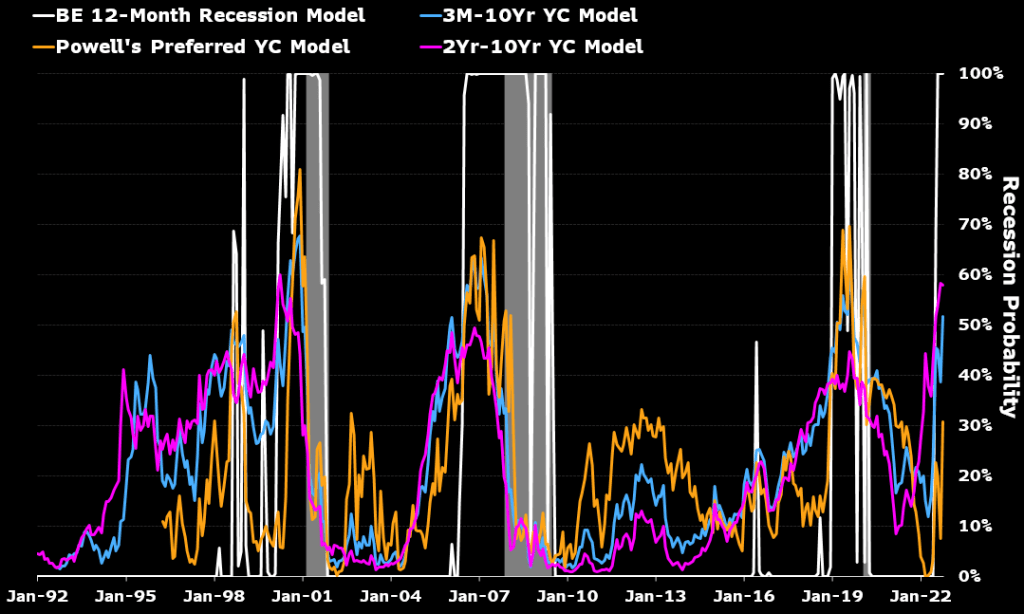

Controlling inflation comes at a cost to growth. Yield curves have inverted. A Bloomberg Economics model shows a 100% probability of recession starting by August 2023. Take that — like all model forecasts — with a grain of salt. But the basic view that aggressive Fed tightening will very likely tip the economy into a downturn is correct.

While various measures of impending US recession show a good chance of a 2023 recession, Powell’s preferred measure of the yield curve shows only a 30% chance.

What Might the Recession Look Like?

We project a 0.9% GDP contraction in 2H 2023, driven by an investment downturn as firms pare inventories amid a downshift in consumption. Residential investment will also contract with real interest rates likely to rise steadily throughout 2023 as nominal rates stay high and inflation moderates.

An Inventory-Led Downturn

Resilient consumption should help put a floor under demand.

Households have enough of a cash buffer — extra savings built up over the course of the pandemic, rising COLAs for Social Security recipients, ongoing state and local government stimulus and solid 2022 wage income growth — to sustain consumption during the recession. Our base case is for real spending to grow at a quarterly annualized pace of about 0.5% in 2023, with strength concentrated in services.

By one measure, households may still have $1.3 trillion in the coffers, based on flows within the personal income report through September. At the current rate of drawdown, that’s enough to last around 15 months, or through the end of 2023. Funds may dry up faster as job losses mount and the unemployed fall back on their savings.

$1.3 Trillion Extra Savings to Keep Spending Positive

The labor market remained exceptionally tight into the end of 2022. We expect it to soften significantly next year, with the unemployment rate rising to 4.5% by the end of 2023. The pace of hiring will slow markedly as support from catch-up hiring dissipates and the effects of restrictive monetary policy settle in. We estimate only 20%-30% of total employment is still in sectors experiencing labor shortages, implying demand for labor is falling fast.

Avoiding a Hard Landing Depends on Inflation, Fed

Extreme circumstances — the pandemic, Russia’s invasion of Ukraine — have made a recession more likely than not. Extreme circumstances can change, and so can policy makers’ response Whether the US can stick a soft landing depends substantially on how external conditions develop and how the Fed responds.

Not our base case, but we can envision a scenario in which the central bank opts to ease rates in 2023, boosting the chances of a soft landing.

One way that could happen is inflation falling faster than expected. Currently, our baseline is for headline CPI to drop to 3.5% and the core to 3.8% by the end of 2023. The most important assumption there is that energy prices remain flat next year from 2022.

In an alternative scenario, inflation fall faster as China maintains Covid controls and growth stumbles. A Bloomberg Economics model attributes the recent fall in oil prices entirely to a drop in demand — mainly from China. If China’s growth falls off the cliff, perhaps amid a sharp rise in Covid cases and resumed lockdowns, commodity prices could tumble sharply.

A warm winter in Europe and the US could also keep energy prices in check. Lower demand from Europe for US liquefied natural gas would help stem the increase in domestic electricity prices.

In that scenario, US energy prices could fall 20% in 2023 and headline inflation may drop to 2% by the end of the year. Lower gasoline prices would work to soften inflation expectations, easing pressure on the Fed to hold rates at higher level. A rate cut could then come in 2H 2023, raising the possibility of a soft landing.

Scenarios of CPI Inflation in 2023

The risk cuts both ways. A quick and successful pivot to reopening in China could boost oil and other commodities prices. A colder winter in Europe and the US would generate upward pressure for electricity and utility prices. Assuming China is fully open by mid-2023 — the base case for our China team — energy prices could increase by 20% in the year. In that case, headline US CPI would hit a bottom of 3.9% in midyear before surging to 5.7% by year-end.

In that scenario, the terminal fed funds rate would most likely top 5%, possibly closing 2023 near the upper end of St. Louis President James Bullard’s estimated restrictive range of 5%-7%.

Bloomberg Economics US Forecast Table

Thanks to Yellen’s legacy of too low interest rates for too long, The Fed is playing catch-up by finally raising rates.

We are truly living in Strange Days under Joe Biden. And with Elon Musk’s release of Twitter’s suppression of the Hunter Biden laptop scandal, they call Joe Biden the Sleaze.

As The Federal Reserve tries to crush Bidenflation, we are seeing Fed Remittances to the US Treasury soaring (white line). At the same time, we see the Biden Administration draining the Strategic Petroleum Reserve (orange dashed line). And as The Fed tightens, M2 Money growth crashes (green line).

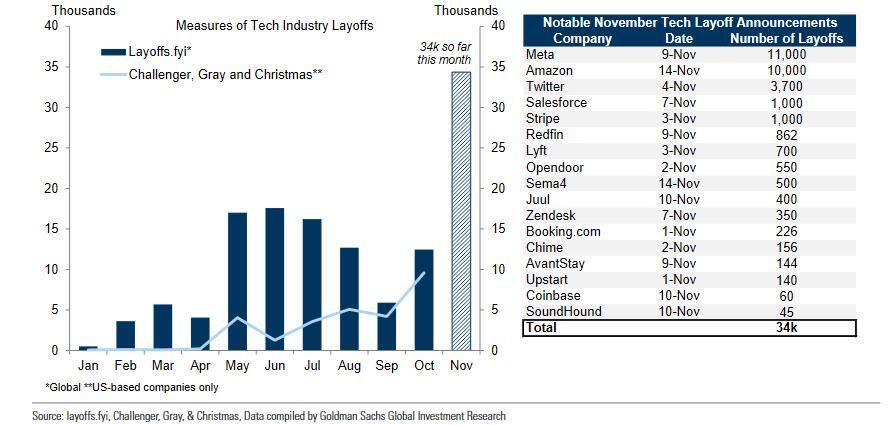

And with tech layoffs, I predict that 2023 job growth will be pretty bad.

As I have discussed before, I am a fan of ADP’s job reports and not a fan of the BLS NFP reports. As M2 Money growth slows, we can see declining ADP jobs added (yellow line), but BLS’s NFP report shows huge spikes.

Lastly, we have Sam Bankman-Fried and FTX. SBF should be in custody for being involved in one of the biggest fraud cases in history, but like Hunter Biden, is roaming free and trying to raise MORE funds. Why are these lapses in justice occuring with “10% for The Big Guy” Biden?

The hawkish drumbeat from central bankers is raising fears of a downturn, with global bonds joining US peers in signaling a recession, as a gauge measuring the worldwide yield curve inverted for the first time in at least two decades.

The US Treasury 10Y-2Y yield curve, on the other hand, has been inverted for 107 straight months.

And in Europe, 10-year sovereign yields are dropping like a paralyzed falcon.

The world and US yield curves are pointing to trouble. And drums along the Potomac (DC) and East River (NYC).

You must be logged in to post a comment.