Harry Truman once uttered the phrase “The buck stops here.” Joe Biden’s catchphrase should be “It’s Russia’s fault!”

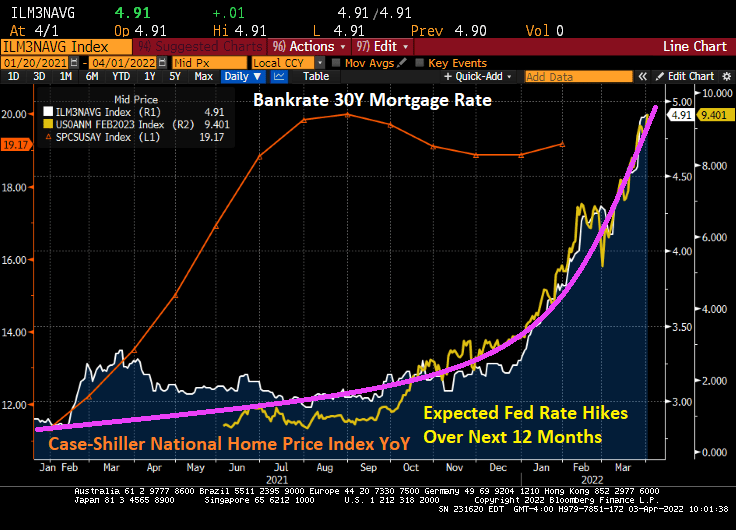

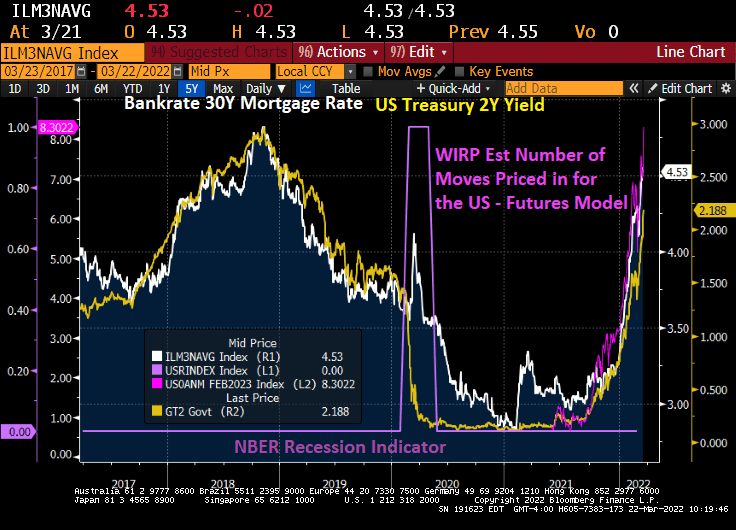

Well, all roads led to Joe and Jay. Here is a chart of Producer Price Index (Final Goods) prices YoY, now the highest in history. At least, gasoline prices are declining to $4.083 (they were $2.40 when Biden was installed as President). But inflation is out of control and the 30-year mortgage rate is now 5.14% (mortgage rates were 2.82% in February 2021 just after Biden took control).

Just in case you wonder why I follow Fed Funds Futures data so closely.

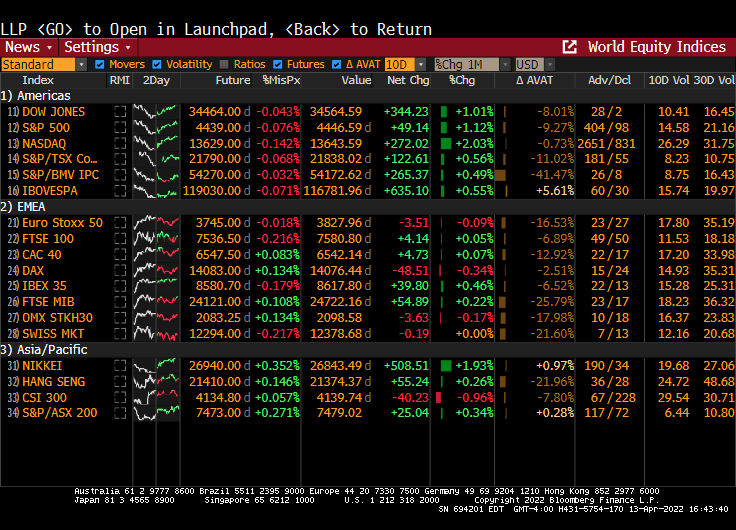

Equity markets are up strongly today as markets sense a weakening in resolve by The Federal Reserve (number of expected rate hikes dropped at 10AM EST).

It appears that we have a “Powell in the headlights” problem.

As we are painfully aware, The Fed’s exaggerated monetary flood combined with Federal stimulus spending has led to horrible inflation.

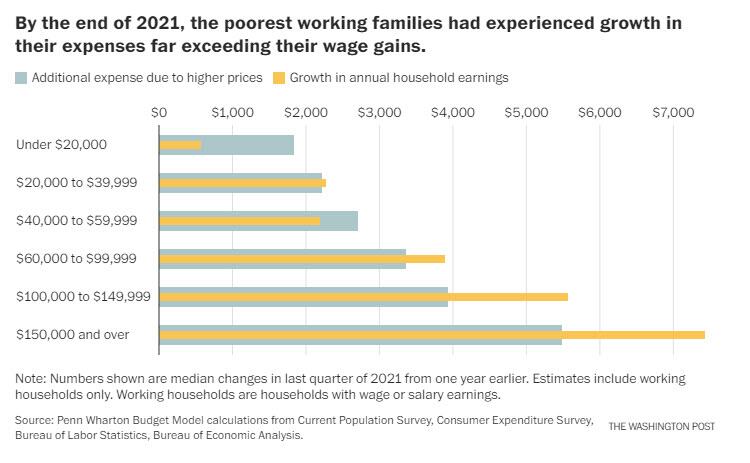

Yes, despite what government talking heads say, Federal stimulus increases demand for goods, the supply is generally slow to respond resulting in rising prices. Then government policies driving up energy prices also leads to highers prices. Throw in Federal Reserve monetary stimulypto and we have this chart from hell from Penn-Wharton. The chart shows that households earning less that $60,000 experience higher expenses due to rising prices than their gain in earnings.

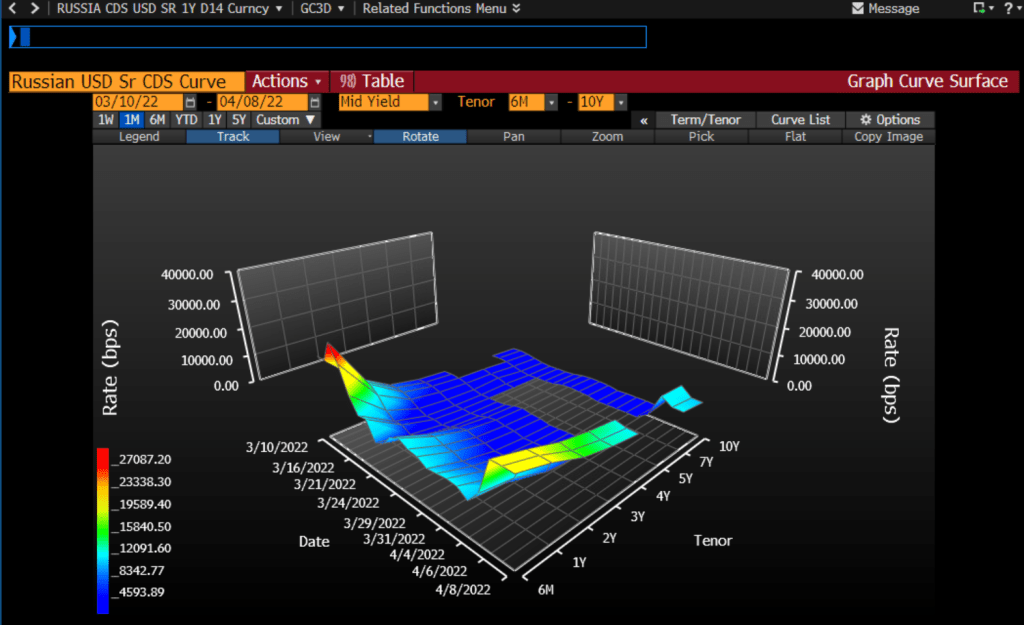

Another chart from hell is the Russian USD Credit Default Swap (CDS) curve. It is spiking at over 20,000.

The one-year Russian CDS is currently at a whopping 20,336 indicating that there is about a 99% of a Russian default over the coming year. As someone who lived through the 1998 Russian credit default scare on Wall Street, this will send a shock wave through credit and Treasury markets.

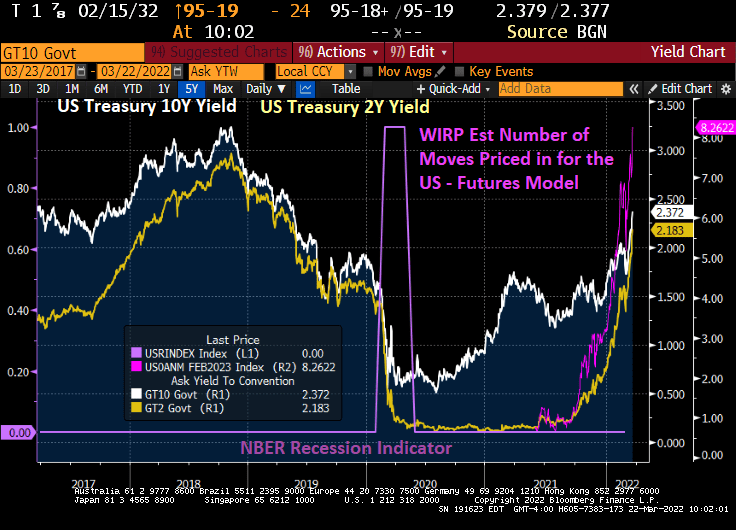

On the US Treasury front, this chart shows how steeply sloped the US Treasury actives curve has become. Steep until 3 years, then flat. I call this chart “T-Dazzle!” T-Dazzle because I can’t believe how badly the Biden Administration and The Federal Reserve are screwing up the country.

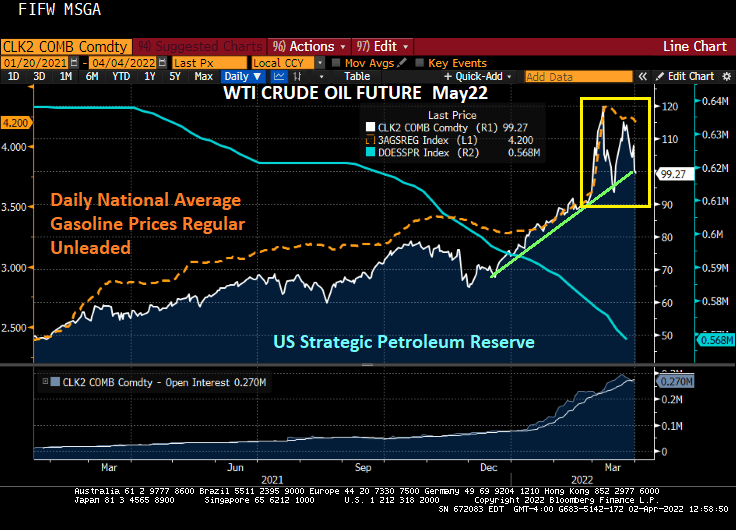

Crude oil? WTI Crude is back to almost $100 per barrel while Brent Crude is at $102.78 per barrel. Wheat is up 3.22% thanks largely to problems related to Russia invading Ukraine (Europe’s bread basket) and a dismal Chinese wheat harvest.

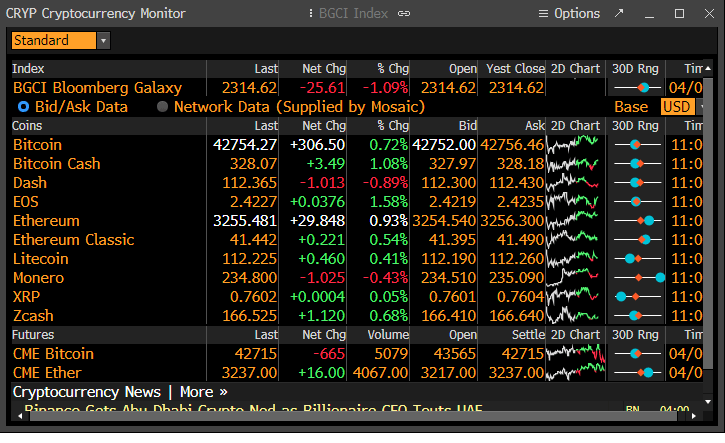

Cryptocurrencies, the alternatives to the US fiat dollar, are rising (in particular, Bitcoin and Ethereum).

Of course, I have to finish up with the soaring 30-year mortgage rate.

Its official! I submitted my resignation from George Mason University effective June 1, 2022. I will miss teaching the students, past and present.

But back to the US Treasury yield curve. It remains in reversion (meaning shorter-term Treasuries have higher yields than longer-term Treasuries, usually a sign of impending recession. The Fed has actually started quantitative tightening (QT) and the growth rate of Treasury note and bond purchases has slowed to a crawl.

Meanwhile, Bankrate’s 30-year mortgage rate rose slightly to 4.91%.

Meanwhile, President Joe “The Big Guy” Biden has ordered carmakers to increase their average fuel economy to about 49 miles (78.8 kilometers) per gallon by 2026. Of course, this is intended to kill-off gasoline-powered autos and make all cars electric or hybrid like the Toyota Prius.

This can be the Democrat’s midterm election slogan: “Making living in the USA unaffordable!”

The middle-class unaffordable Ford F-150 Lightning at nearly $100,000. Thanks Joe!

Alternatively, you can buy a Buick Envision (made only in Shanghai China) with up to 24 city / 31 highway MPG. Well, kiss that baby goodbye under Biden’s new MPG mandate.

Consider what has happened since President Biden was elected. The S&P 500 total return index (green index) has risen thanks to The Federal Reserve’s balance sheet expansion (orange line) with COVID. Until 2022 when the expectation of Fed rate hikes surged from 3 in late December 2021 to 9.4 expected rate hikes over the next 12 months (yellow line).

The US Treasury total return index (white line) has gotten crushed with The Fed’s signals of rate hikes and quantitative tightening (QT). Call it “White Line Fever.” The commodity total return index (blue line) has surged as The Fed’s expected rate hikes have risen from 3 to 9.4 in 2022.

Is The Fed causing a Great Reset in housing? In 2022, we see the surge in Fed rate hike expectations leading the 30-year mortgage rate to be nearly 5%. The last Case-Shiller home price index was for January and it was still raging at 19.17% YoY growth. Let’s see if The Fed’s QT will slow down home price growth. But home prices are growing at 4x 30-year mortgage rates.

(Forbes) – Credit Suisse’s Zoltan Pozsar argues Bretton Woods II crumbled when the G7 countries seized Russia’s foreign exchange reserves. Keeping money inside financial institutions like the IMF was considered risk free. That is clearly no longer the case. Similarly, Bretton Woods I collapsed when Nixon took the US of the gold standard back in 1971 when dollars were convertible to gold at a fixed exchange rate of $35 an ounce. This led to Bretton Woods II, backed by “inside money” or the dollar, which itself is not linked to gold or any other commodity.

Now the basis of this system, which has operated for the past 50 years, is being called into question. The sanctions on Russia, which showed that reserves accumulated by central banks can simply be taken away, raised the question of “what is money?”

That question may explain why Pozsar believes a huge shift in the way the world organizes money and reserves is now underway, “creating a “Bretton Woods III backed by outside money,” (gold and other commodities). Including crude oil and bitcoin.

At least crude oil has fallen below $100 as Biden merrily drains the Strategic Petroleum Reserve (SPR). Gasoline prices have fallen slightly as this is being done before the midterm elections with political, not economic, intent. Once the midterms pass, will Biden continue draining the SPR until there is little left forcing the US to convert to “green energy”?

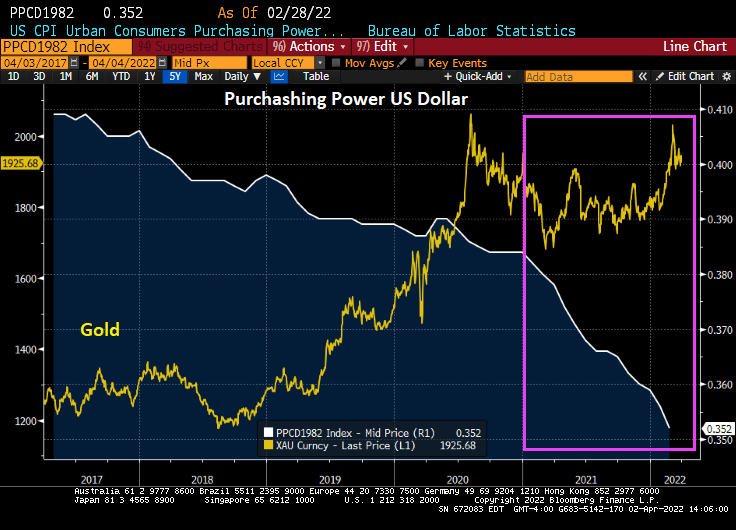

The purchasing power of the consumer dollar took a plunge under Biden as other commodities such as Bitcoin and crude oil soared.

An alternative asset, gold, have generally risen under Biden’s Reign of Error, but particularly after the Russian invasion of Ukraine.

Wasting away again in Biden/Pelosiville, looking for my lost inexpensive gasoline and food. Some people say that Putin is to blame, but we know its Biden/Pelosi’s fault.

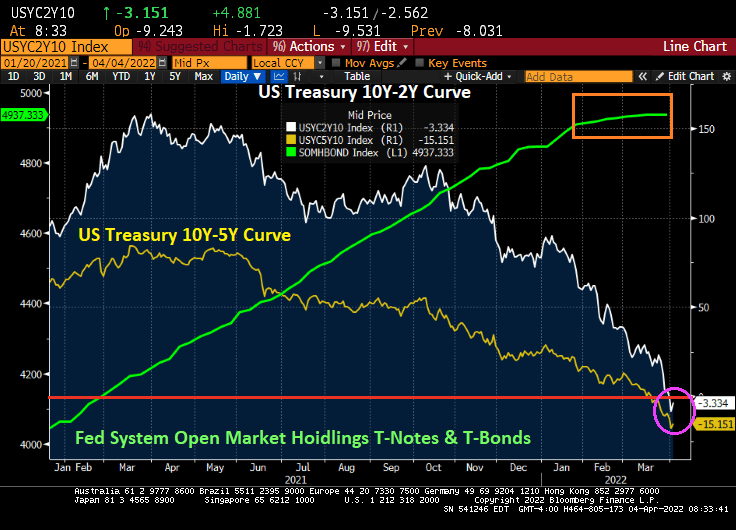

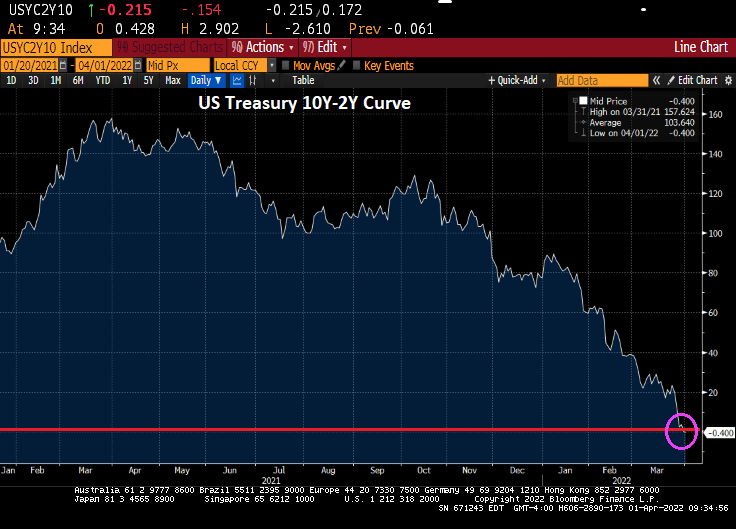

The US Treasury 10Y-2Y yield curve just inverted, generally a precursor to a recession. Called it, nothing but net!

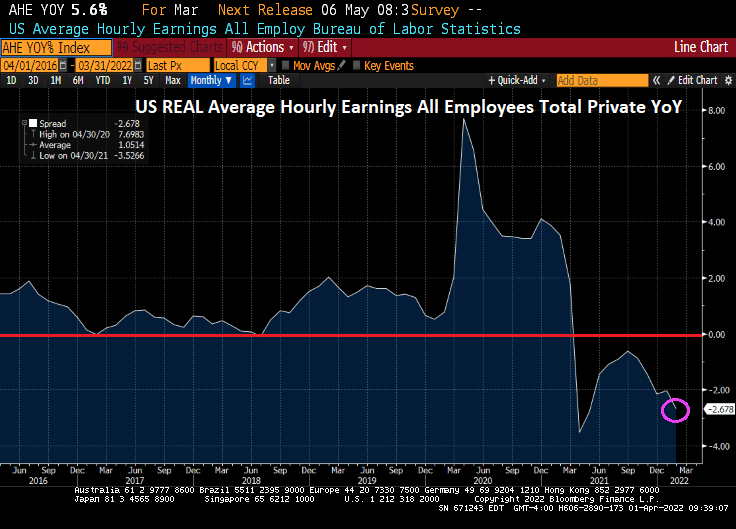

Meanwhile, today’s jobs report shows that Bidenflation is crushing America’s wage growth. While average hourly earnings grew to 5.6% YoY, we are still seeing inflation growing at 7.9% YoY meaning that inflation is reeling hurting the middle class and lower-income households.

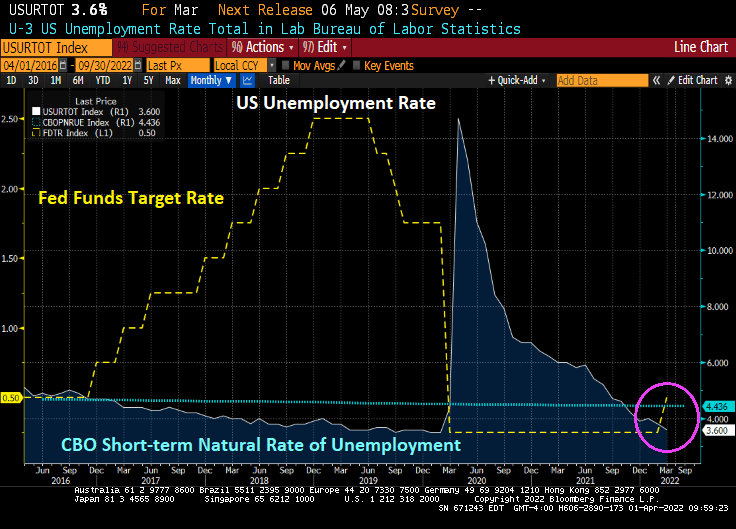

The good news is that the U-3 unemployment rate fell to 3.6%, almost back to the Trump-era unemployment rate of 3.5% prior to the Covid outbreak. And the unemployment rate remains below the CBO’s short-term natural rate of unemployment indicating that the labor market is OVERHEATED.

Today’s jobs report was pretty good, as we would expect from a recovery caused by governments shutting down economies, then reopening them. 431k jobs were added, but less than last month’s jobs added of 678k and less than the forecast 490k.

The number of people NOT in the labor force fell slightly, but it still around 100 million. The number of people holding multiple jobs to overcome Bidenflation rose to 7.5 million.

On the mortgage front, Bankrate’s 30-year mortgage rate rose to 4.90% as the 2-year Treasury rate (yellow) rises and the number of expected Fed rate hikes over the coming year is 9.26%.

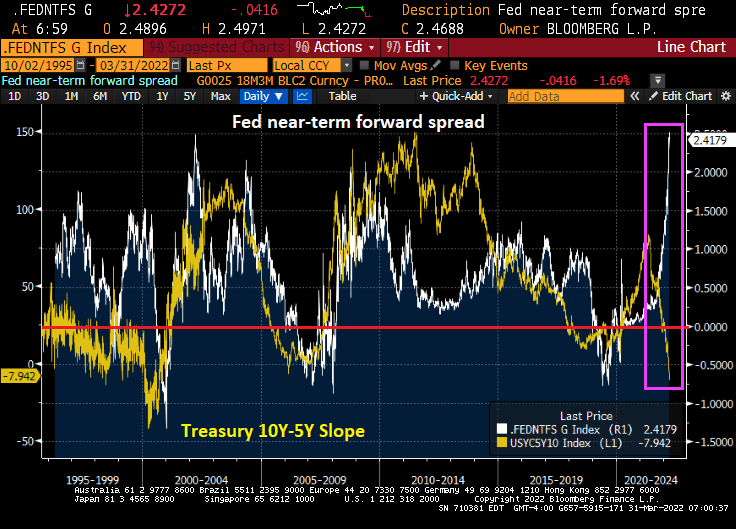

There is a massive divergence between the collapsing US Treasury 10Y-2Y yield curve and the near-term forward spread. The near-term forward spread is the difference between the implied interest rate expected on a three-month Treasury bill six quarters ahead and the current yield on a three-month Treasury bill.

As we already know, the 10Y-5Y yield curve has inverted signaling a coming recession.

This divergence between the Treasury yield curves and the near-term forward spread is occurring as US inflation hits the highest rate in 40 years.

As of today, Jerome “Nero” Powell and The Gang at The Federal Reserve have not trimmed the Fed’s balance sheet and have only raised their target rate once under President Biden.

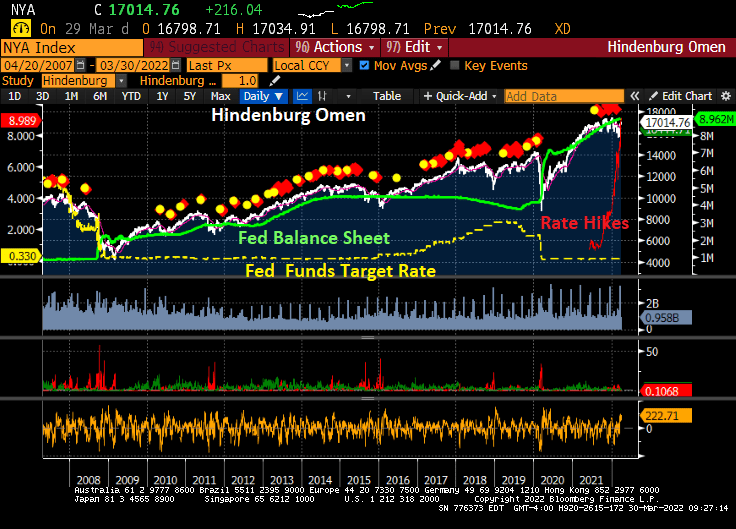

Here is the Hindenburg Omen, named for the catastrophic explosion on May 6, 1937 at Lakehurst Naval Air Station in New Jersey. The Hindenburg Omen was flashing red before the stock market correction of late 2007-2009. But, the Hindenburg Omen has flashed red repeatedly since the financial crisis, yet the S&P 500 index has kept rising. The reason? Repeated policy errors by The Fed leaving monetary stimulus in place for too long leading to a bubble forming in the stock market.

The Shiller CAPE (Cyclically-adjust price-earnings) ratio is at the second highest level since the 1800s. The highest point was the infamous Dot.com bubble and bust in 2000/2001.

Since The Fed continues to say “We have a plan!” to slow/shrink The Fed’s balance sheet and raise their target rate … it has not done anything yet (other than a 25 basis point bump at the March meeting).

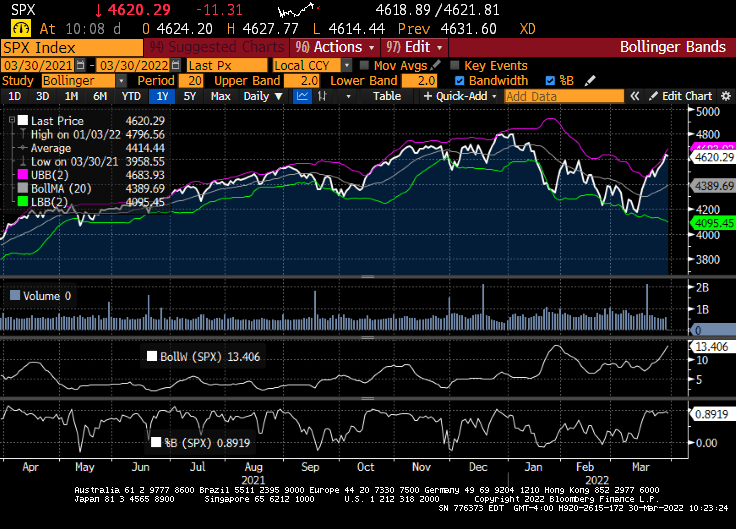

I am not advocating technical analysis for stocks, but the Bollinger Band analysis for the S&P500 index is showing the S&P 500 index near the top band indicating that a decline in likely.

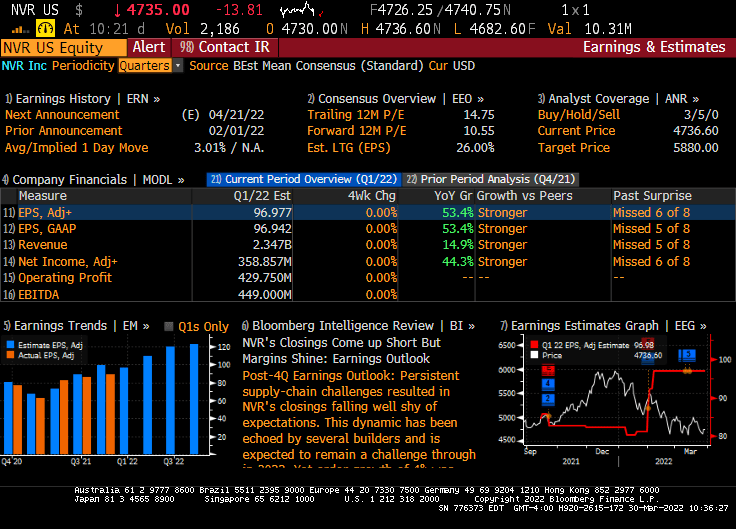

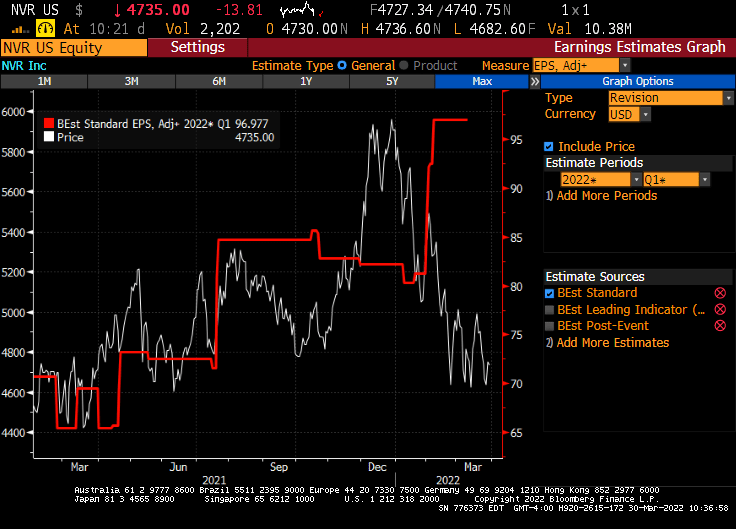

Today, the US equity market in essentially flat given the massive uncertainty about the Russia/Ukraine situation and whether the US economy is slipping into darkness. But this morning, Federal government blessed companies (healthcare, solar energy and Blackrock) are doing quite well, while homebuider NVR is taking it on the chin thanks to hints that The Fed will raising rates.

Now, NVR (Northern Virginia Homes, Ryan Homes) had explosive earnings growth in their February 1, 2022 report.

But the market is pricing in the crushing Fed rate hikes that are expected.

So, will Foul Powell pull a Volcker and raise rates and crush the economy (and stocks)? Or will Foul Powell And The Fed gang let inflation burn out of control, but preserve the massive asset bubbles?

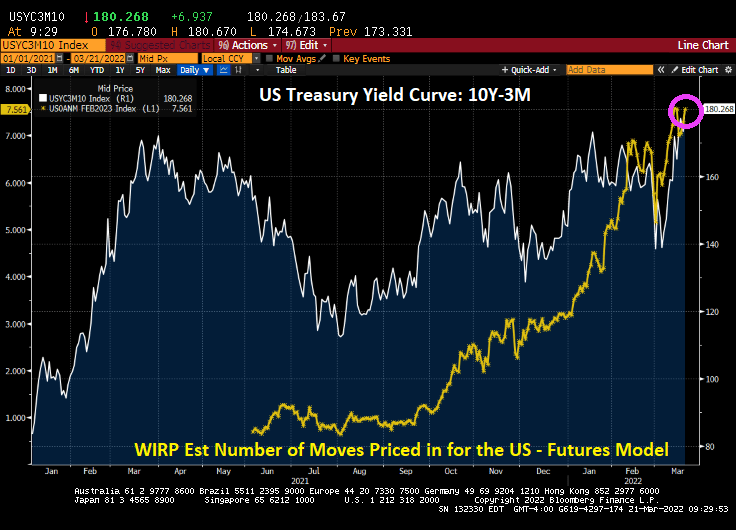

Oil prices are soaring as US President Biden pleads like a homeless person to foreign countries for oil rather than let the US produce more oil to drive down prices. Meanwhile, the US Treasury yield curve 10Y-3M is at its steepest (rising 10Y yields while The Fed keeps short rates at near zero).

But if we look at the belly of the beast, so to speak, the 10Y-5Y slope, we can see that the Treasury curve has declined to a mere 0.278 basis points as inflation rages.

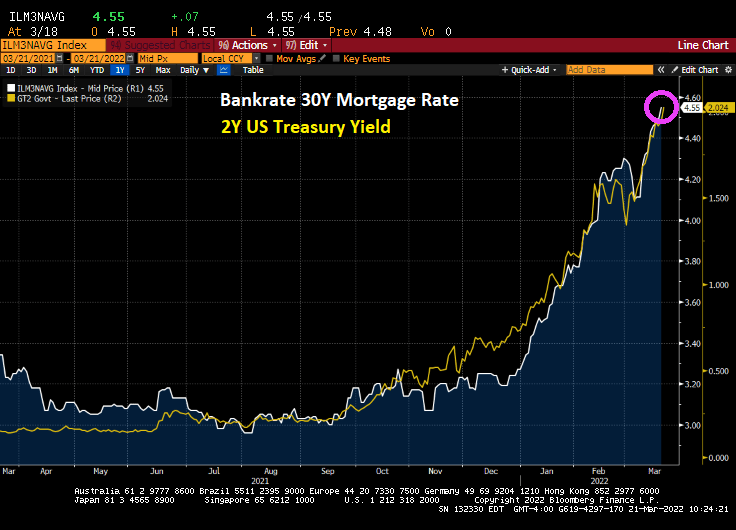

Bankrate’s 30-year mortgage rate keeps on climbing and has hit 4.55% as the 2-year Treasury yield rises rapidly.

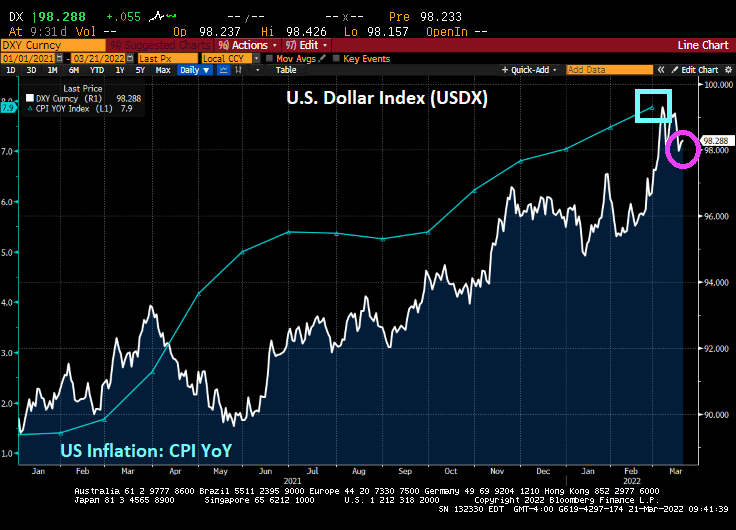

The US Dollar Index has risen dramatically as US inflation has increased dramatically.

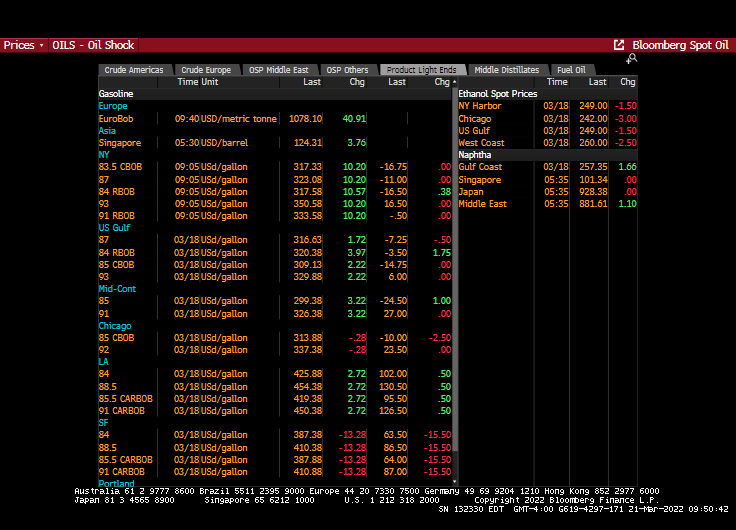

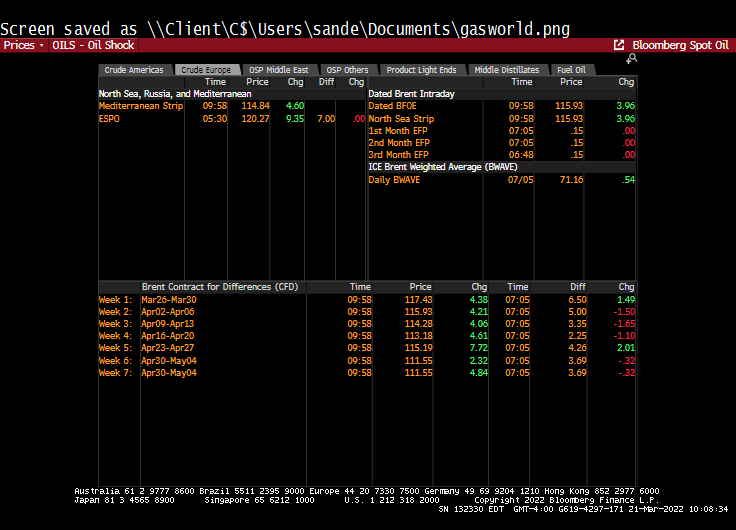

Oil? Oil is up over 4% in the US. Mexican Mix (not a #3 meal at Chuy’s) is up 7.32%.

Gasoline? NY prices are up over 10%.

Russian oil is up 9.35%.

Ah, for the good old days of 30 cents a gallon gasoline, although I always wondered about Gulf’s marketing campaign. “Good Gulf” seems to imply that the other Gulf gasolines aren’t good. And Gulf’s “No-nox” seems to imply that the other Gulf gasolines knock like Biden’s knees as he pleads for foreign oil.

You must be logged in to post a comment.