Well, the Fed’s talking heads have been saying a 50 basis point hike was coming in May … and it appeared!

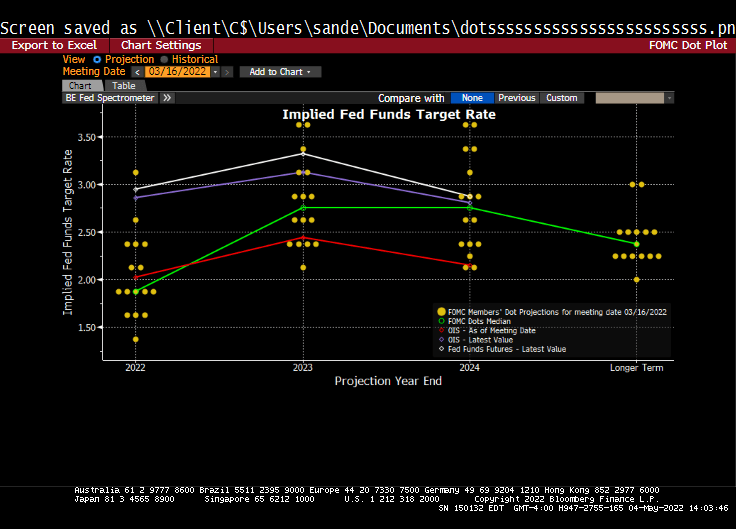

And it looks like 9 rate hikes are a comin’ by February 2023.

The Fed’s Dot Plots shows a cooling of Fed rate hikes by 2024 and beyond.

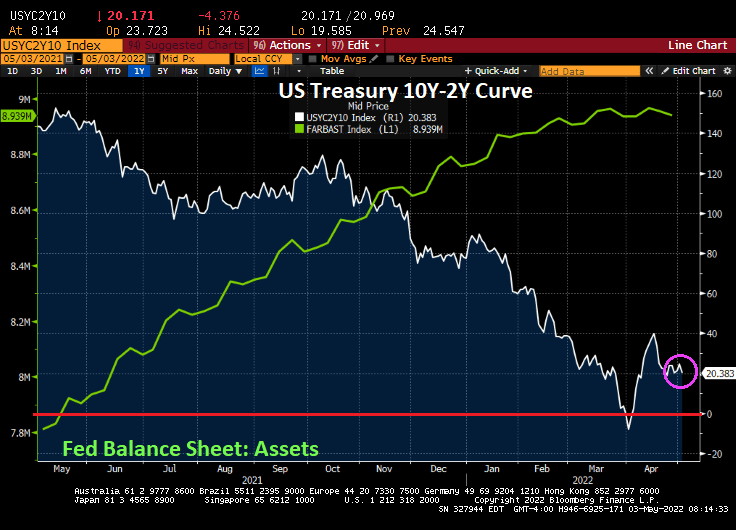

Here is the path of Balance Sheet peel-off.

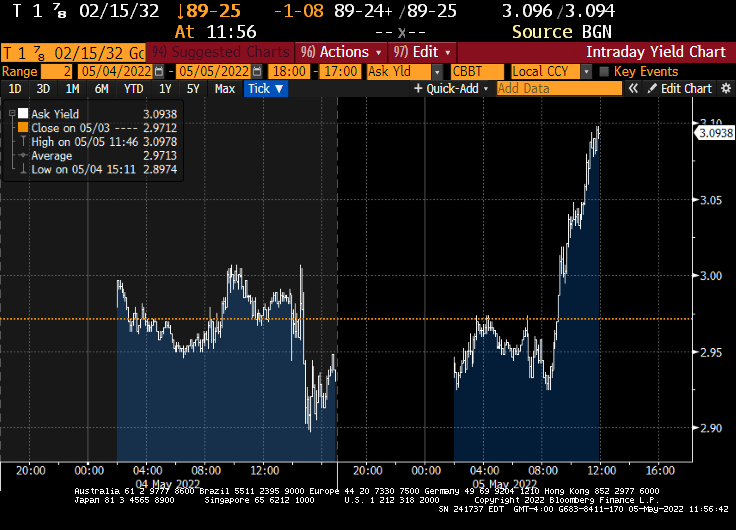

The US Treasury actives curve is up by 14 bps at the 10-year tenor and up 17 bps at the 2-year tenor.

The plan will see $30 billion of Treasuries and $17.5 billion on mortgage-backed securities roll off. After three months, the cap for Treasuries will increase to $60 billion and $35 billion for mortgages.

I could read the Fed’s speech on their decision, but since The Fed has been so highly politicized, I don’t really care what they say. Only what they do.

The U.S. Treasury market is showing signs of stress that may have implications for whether the curve keeps steepening.

Over the past month the curve has retraced from an inversion to a steepening driven by a surge in yields on benchmark 10-year bonds. That has led to interesting outlier indications, as traders weigh the outlook for Federal Reserve interest rate increases and inflation.

The US Treasury yield curve has settled-in at 20.383 bps (effectively zero) as The Fed continues its war on inflation.

On the SOFR front, we see SOFR Coupons being slow to benefits from Fed rate hikes. So, SOFR Coupons are behaving like Stouffer’s lasagna, frozen and tasteless.

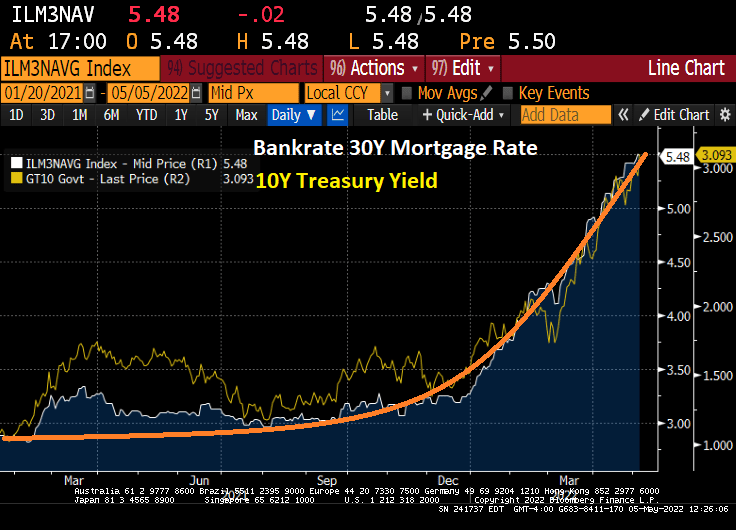

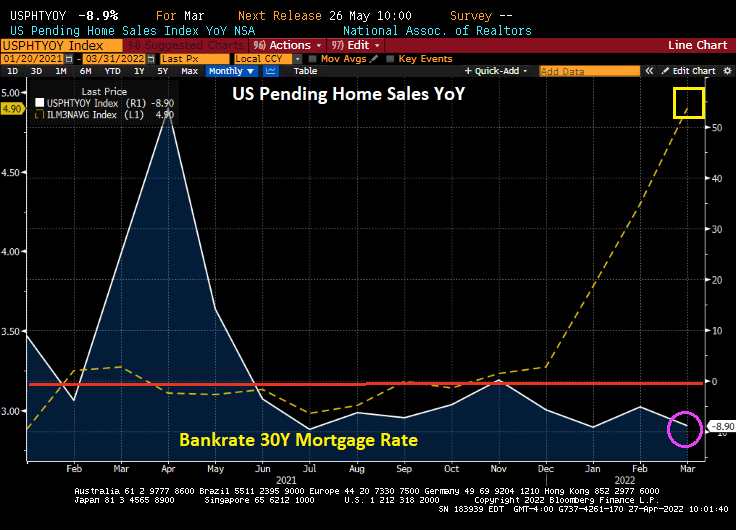

On the other hand, mortgage rates continue to soar on EXPECTATIONS of Fed rate hikes.

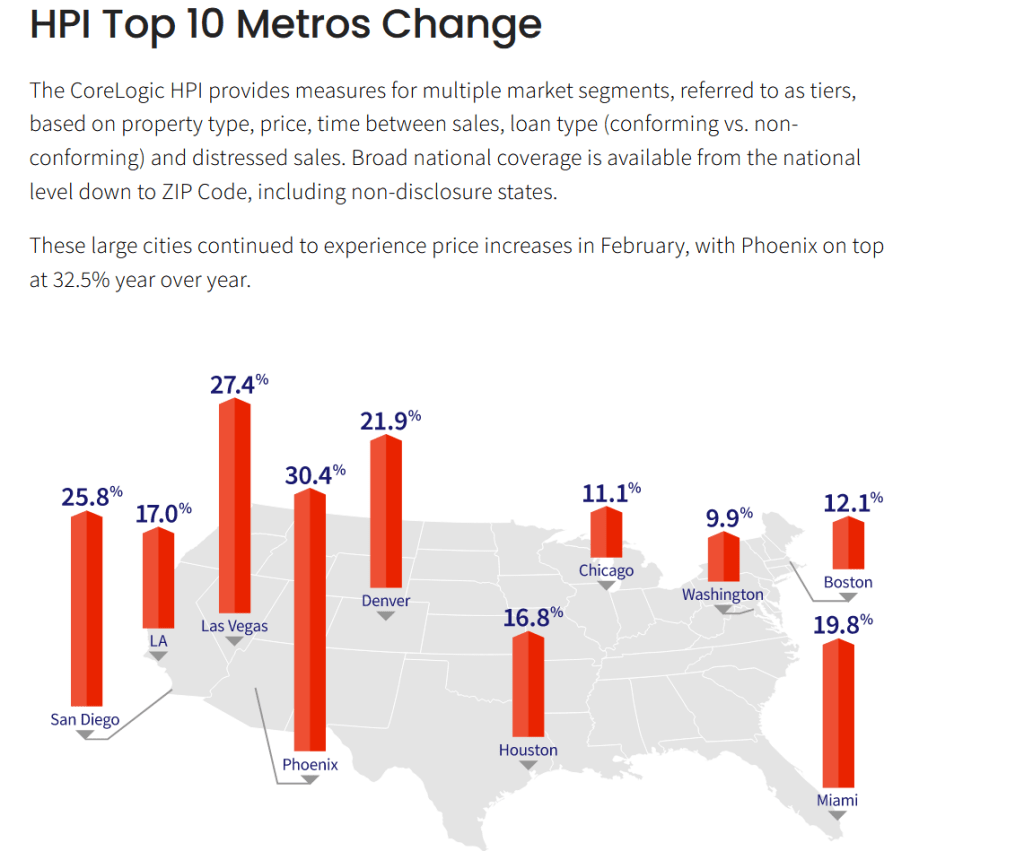

Phoenix AZ leads the top ten at 30.4% with Washington DC lagging at 9.9%.

So, its official. The Federal Reserve is best exemplified by former Yankee/Mets first baseman “Marvelous” Marv Throneberry. When players presented Mets’ manager Casey Stengel with a birthday cake but neglected to give piece of cake to Throneberry, Stengel replied to Throneberry when asked why no cake, “Because I was afraid your were going to drop it.”

Just like The Federal Reserve, the honorary Marv Throneberry of the the global economy.

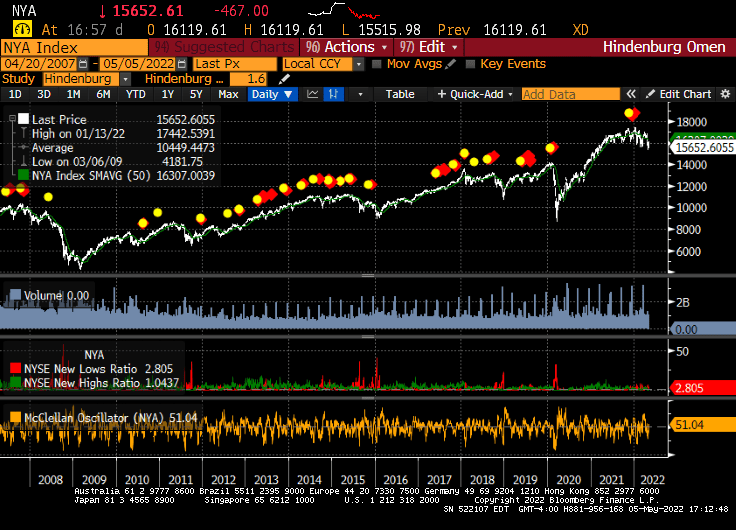

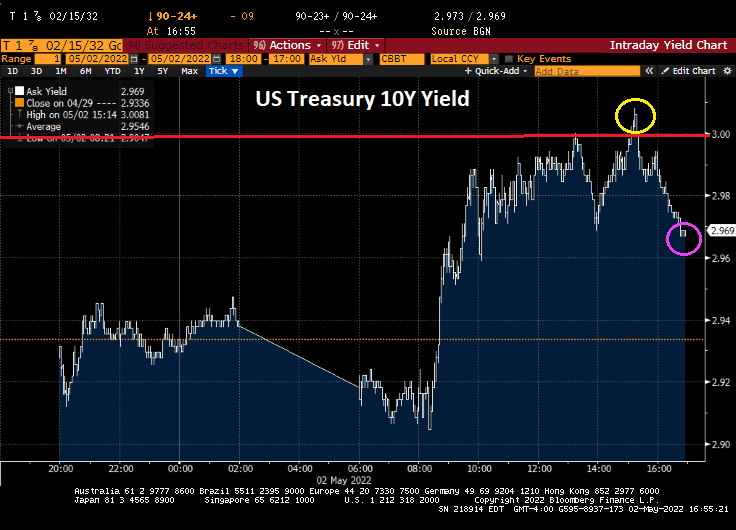

Today we saw the 10-year Treasury Note yield break through the 3% barrier, then retreat as is there was a reflecting barrier at 3%.

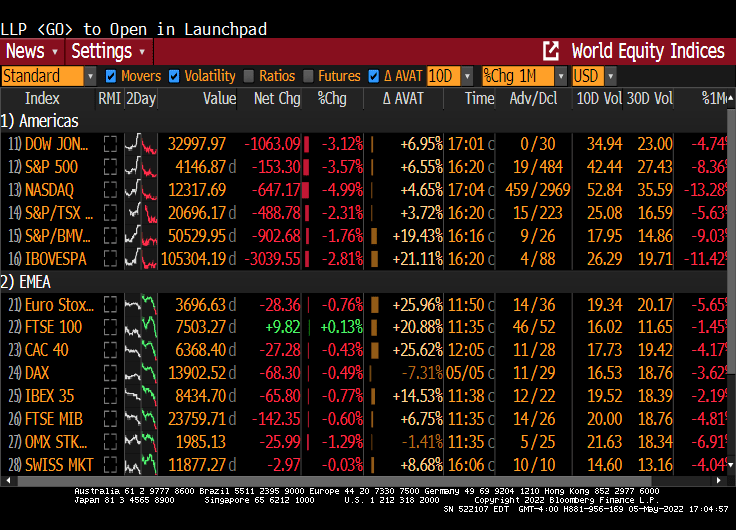

And in Europe, we saw a flash crash allegedly caused by Citi’s trading desk.

The selloff was triggered by a large erroneous transaction made by the U.S. bank’s London trading desk, according to people with knowledge of the matter who asked not to be identified discussing private information. A knee-jerk selloff in OMX Stockholm 30 Index in five minutes wreaked havoc in bourses stretching from Paris to Warsaw toppling the main European index by as much as 3% and wiping out 300 billion euros ($315 billion) at one point.

The US Dollar rose again as expectations of Fed monetary tightening due to inflation become a reality.

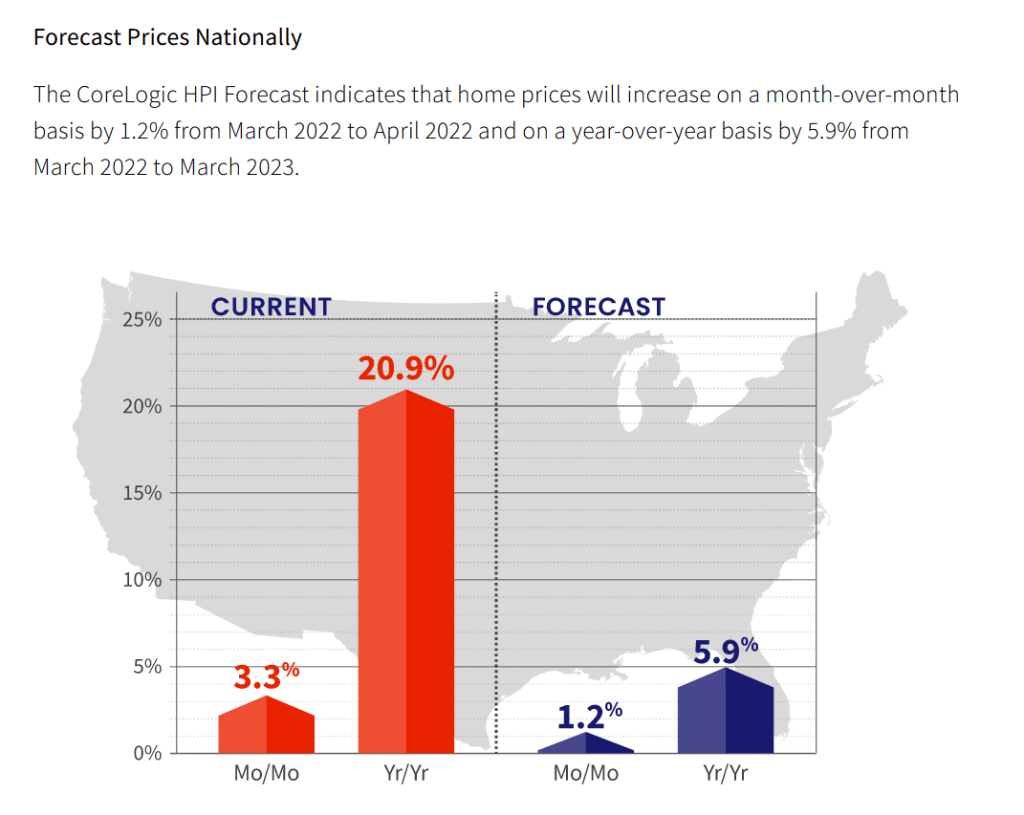

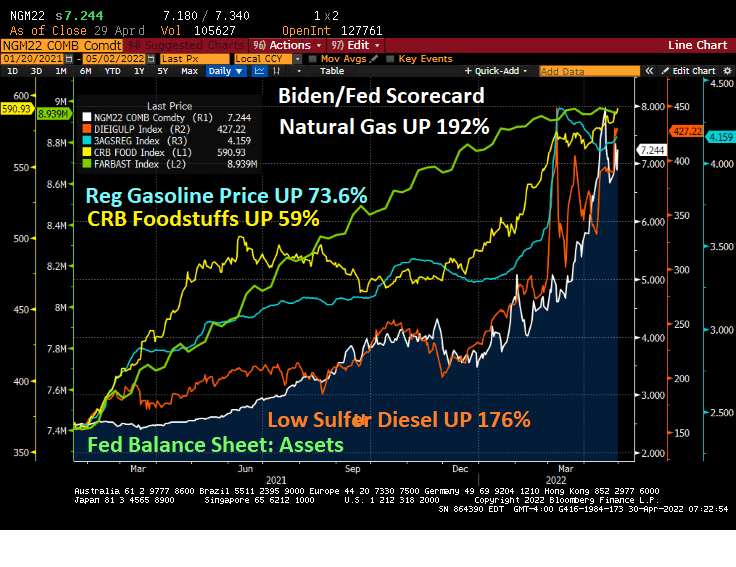

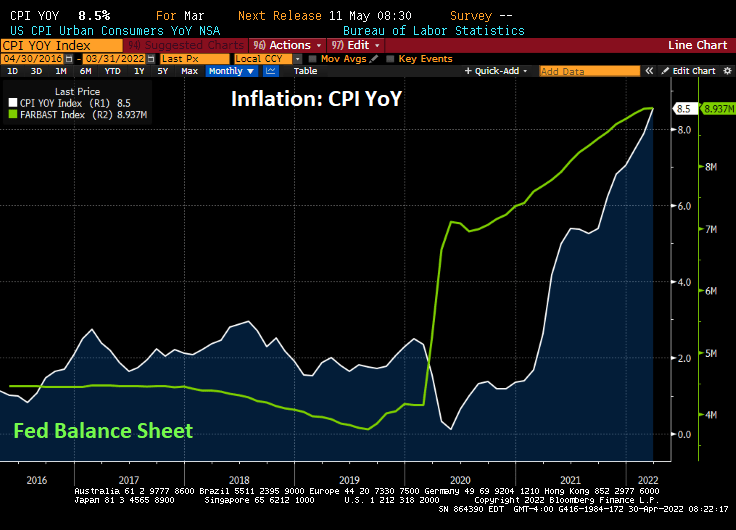

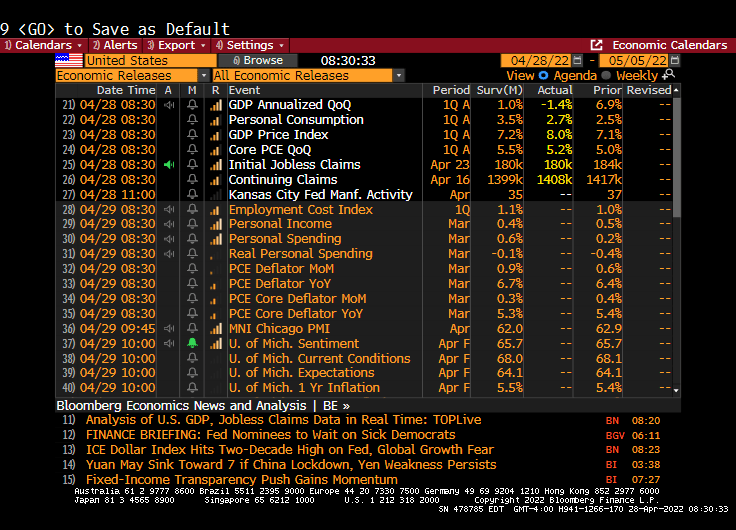

We all know (except for Biden apparently) that inflation is up 8.5% YoY as measured by the change in the Consumer Price Index (CPI). However, the CPI change doesn’t fully capture what is crushing Americans’ pocketbooks. Here is a brief update on where we stand prior to the upcoming Federal Reserve Open Market Committee meeting on May 4th.

Since Biden was installed as President on January 20, 2021, prices for key commodities have soared. Natural gas futures UP 192%, Regular Gasoline prices UP 73.6%, Commodity Research Bureau Foodstuffs UP 59%, Low sulfur Diesel futures UP 176%.

Since we now have the Biden’s Orwellian Ministry of Truth (actually The Department of Homeland Security’s “Disinformation Board”) which will start censoring free speech. And this post is what could fall under their reign of terror. Or in Biden’s case, reign of error.

Jen Psaki, the President’s talking head, has said that it is Russia and Putin’s fault. So, here are the same prices up to Russia’s invasion of Ukraine since Biden was installed as President: Natural gas futures UP 82.3%, Regular Gasoline prices UP 80.2%, Commodity Research Bureau Foodstuffs UP 50.1% ,Low sulfur Diesel futures UP 47.7%.

Yikes! So, even before Russia invaded Ukraine, the lethal combination of Biden’s green energy executive orders and The Fed’s continuing monetary stimulypto was deadly for American households.

On a sad note, The Biden Administration is considering cancelling student loan debt as a way to control inflation (?). Of course, cancelling student debt will lead to a surge in consumer spending and even MORE soaring inflation. Biden is suffering from The Medusa Touch. Everything he touches turns to stone.

While The Fed is expected to remove monetary stimulus, don’t expect inflation to return to pre-Biden levels. The anti-fossil fuels edicts from Biden are still in effect. Even if the bottlenecks clear up, Biden and Congress may unleash more Federal spending (although much of Federal spending benefits “Friends and Family” of Biden and Congress, not the American middle class or lower-wage workers).

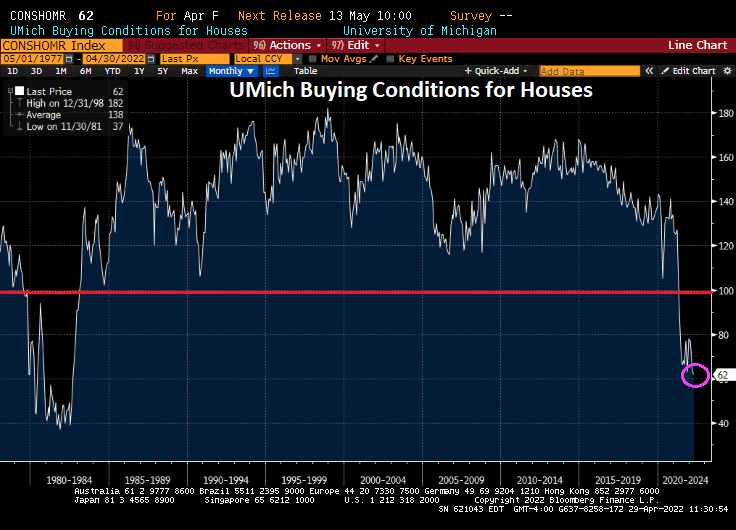

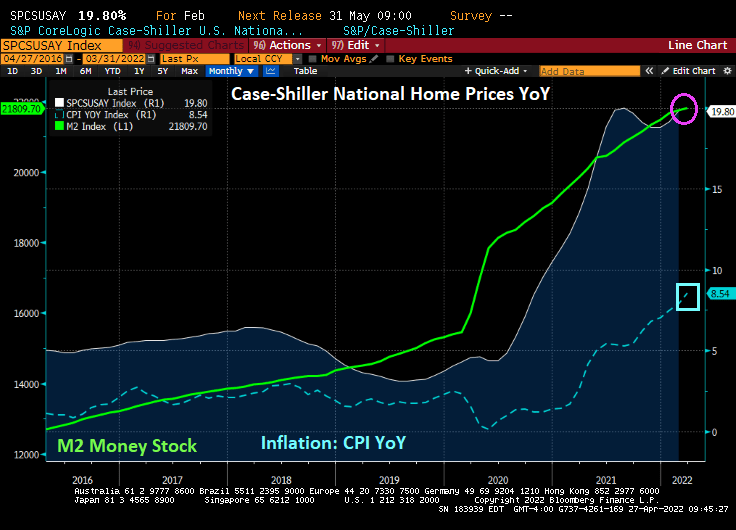

Rising home prices and The Fed signaling an end to the perpetual punch bowl have resulted in the University of Michigan buying conditions for houses to hit the lowest level since 1982.

While bearish sentiment in markets highest since 2009 in the stock market.

I don’t get why Biden created a “Disinformation Control Board” led by Nina Jankowicz – a disinformation spewer. We already have disinformation media outlets like CNN, MSNBC, ABC, CBS, NBC, New York Times, Washington Post, etc., so why create a Federal control board? All in time for the midyear elections!!

If this move by Biden doesn’t terrify you, then you didn’t study history.

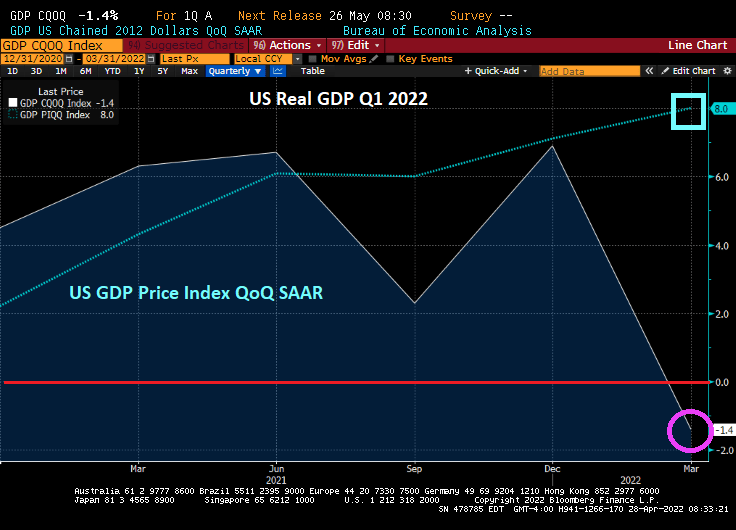

Heartaches in heartaches. US GDP growth for Q2 has stumbled to 0.446% as The Fed is launching quantitative tightening (QT) to fight the inflation that they caused in the first place.

According to the Atlanta Fed’s GDPNow real-time GDP tracker, US GDP growth has stumbled to a meager 0.446%. Despite the massive stimulus from The Federal Reserve and Washington DC’s massive fiscal stimulus.

Here is Dvorak’s New World Symphony, an appropriate piece the global turmoil that has taken place after Russia’s invasion of Ukraine.

Here is the ratio of the S&P 500 index against the Bloomberg Commodity Price Index. This ratio is plotted against The Federal Reserve’s balance sheet of assets. Notice the decline in the Commodity Ratio in 2022, even ahead of the Russian invasion of Ukraine.

Global currencies, on the other hand, have been really crushed since the Russian invasion of Ukraine. The Japanese Yen, China’s Renminbi and Europe’s Euro relative to the US Dollar are falling due to a variety of reasons. Covid lockdown in China, Japan’s insistence on monetary easing while other Central Banks are tightening and the Euro with Russia threatening nuclear war.

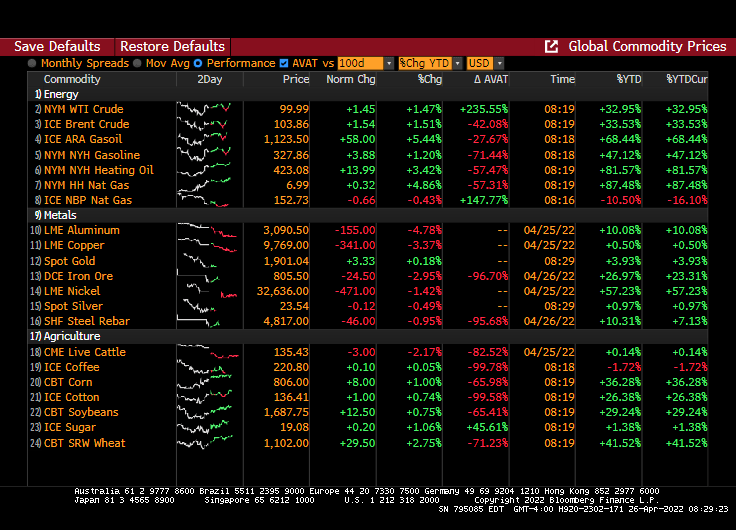

WTI Crude is back to $100 a barrel. Critical metals are down today related to a slowing global economy and wheat is up 2.75%.

Could it be that US Dollar hegemony is nearly over and commodity-backed currencies are the way of the future?

You must be logged in to post a comment.