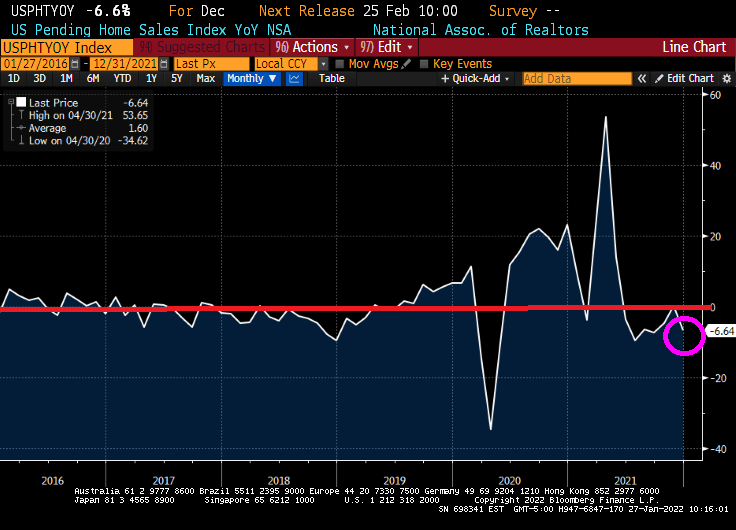

Pending home sales in the USA tanked 6.64% YoY. Yes, it was for December, but down 6.64% YoY means that pending home sales are lower than last December.

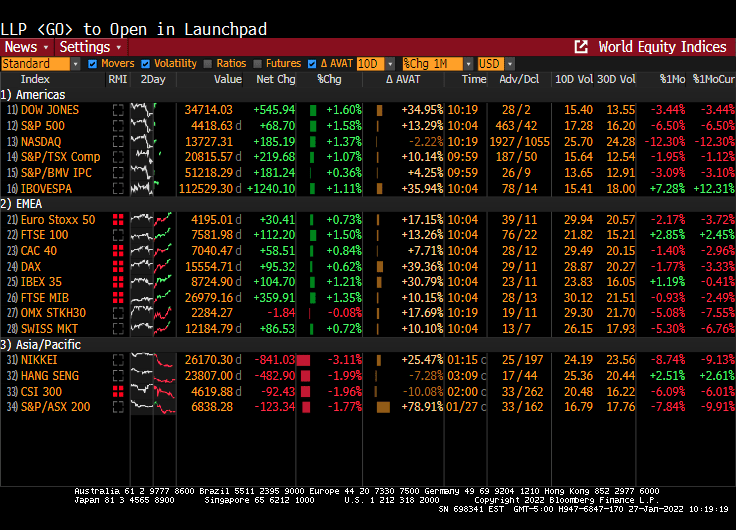

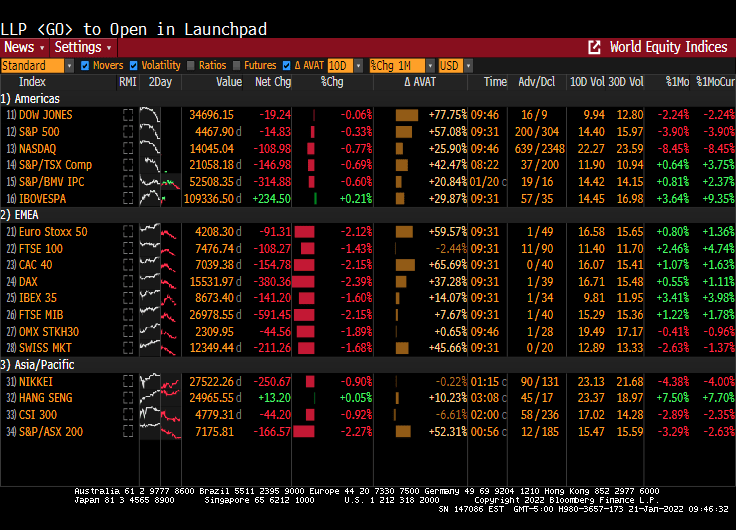

And the stock market was up across the board as Powell refused to take his foot off the monetary gas pedal.

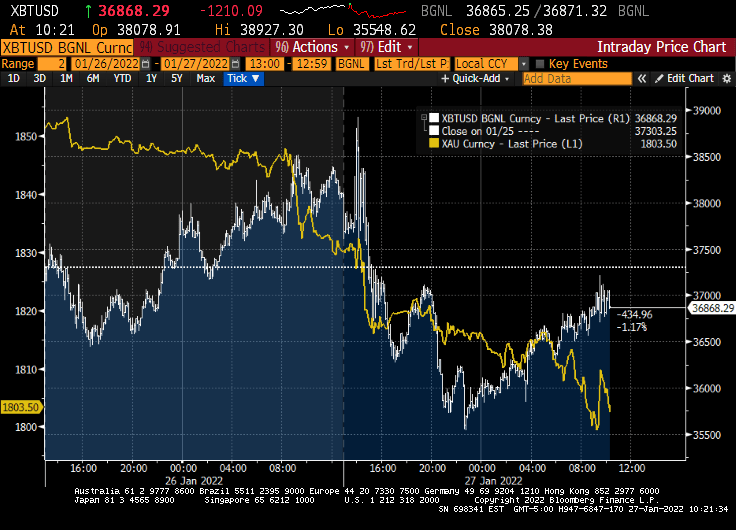

Gold is down along with Bitcoin for you ALT investment types.

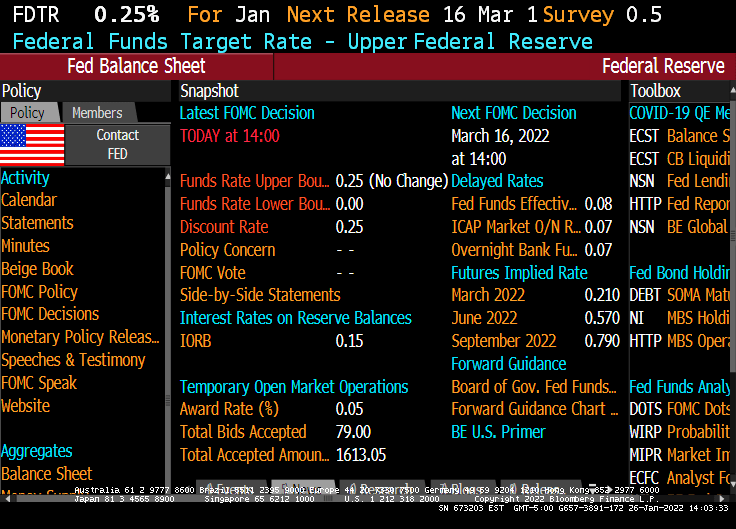

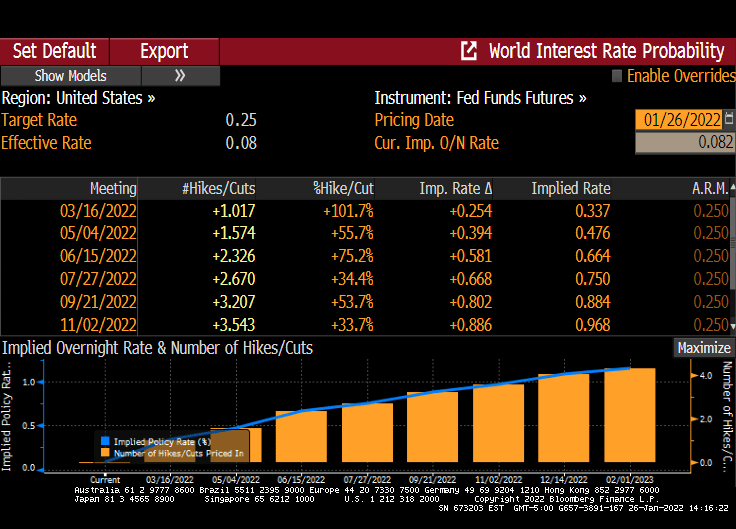

Yes, The Federal Reserve could have raised their target rate at their January meeting, but chose not to raise rates. Instead, Chairman Powell said that rate increases are a comin’!

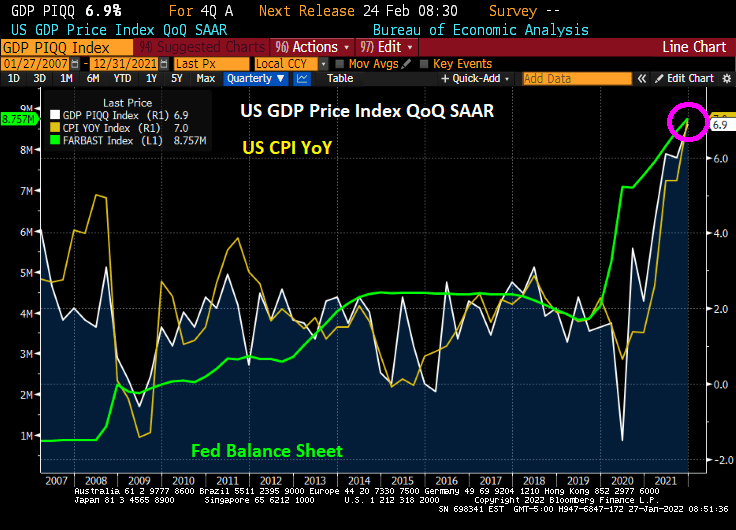

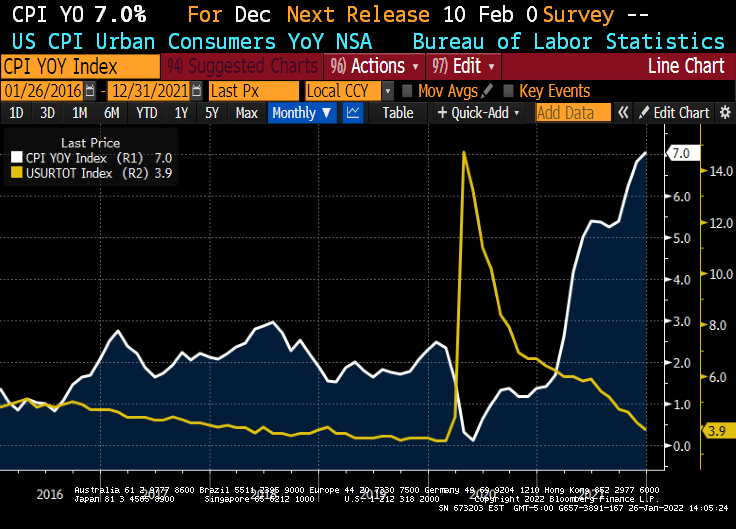

I hope Powell wasn’t hoping for a slowdown in inflation, because today’s Q4 GDP report showed a surge in GDP to 6.9% QoQ. But with that GDP surge we also got a surge in prices paid by consumers to 6.9% as well. Thanks to the continuing massive Federal stimulus being poured into markets.

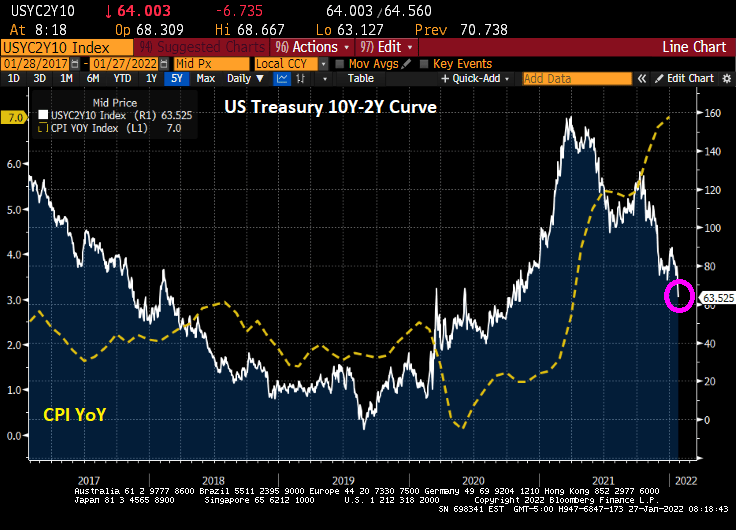

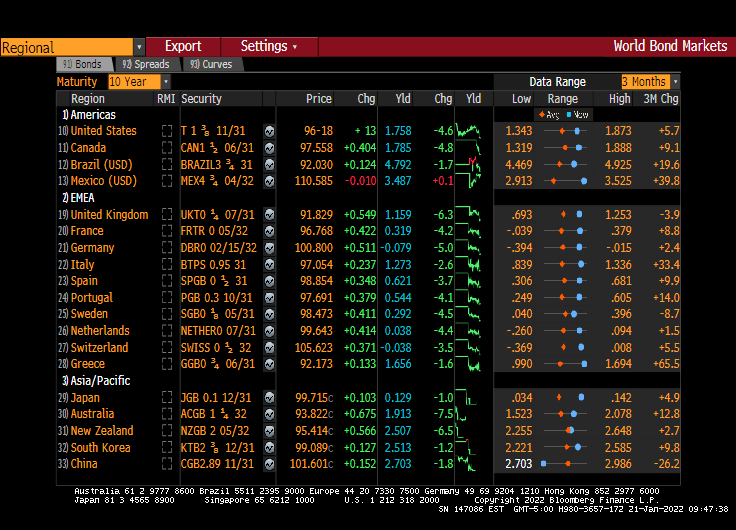

Despite the positive news on Q4 GDP, we are still seeing 7% inflation and a diving 10Y-2Y yield curve.

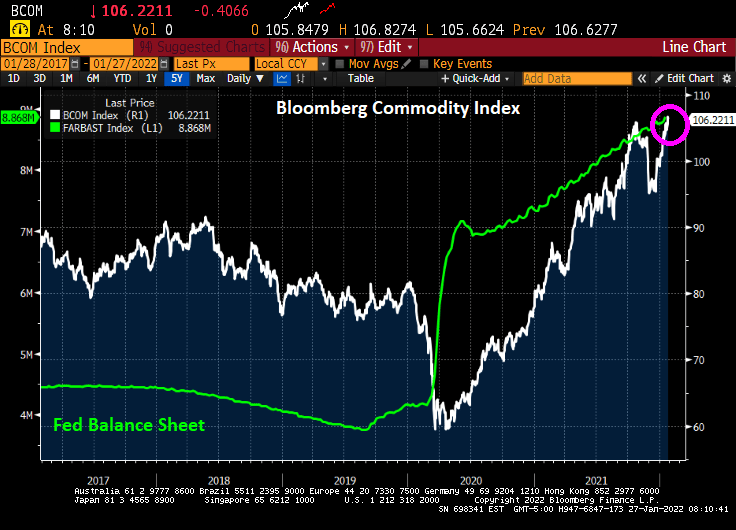

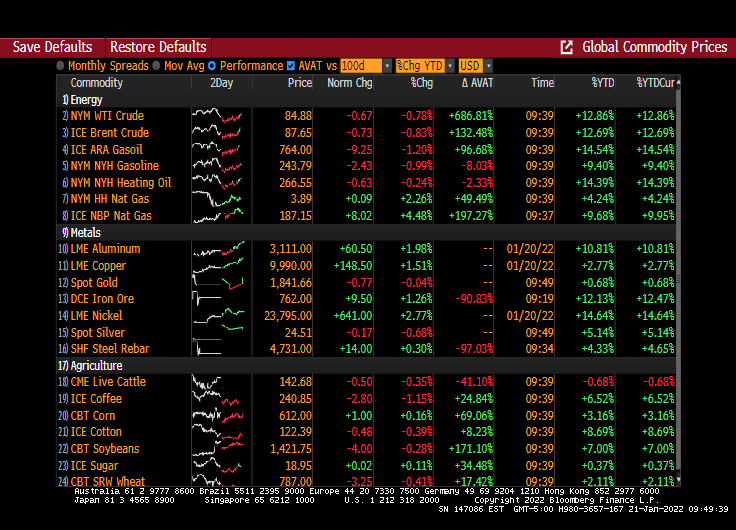

Along with that surprising GDP report, we are seeing the Bloomberg Commodity Index rising like a bat out of hell (RIP, Meatloaf).

Despite inflation growing at 7% (versus The Fed’s target rate of 2%) and U-3 unemployment being only 3.9%, one would have thought that Jay and The Gang would have started increasing rates at the January meeting.

But nooooo. The Fed actually sat on their hands and did nothing.

What did The Fed say?

“The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. In support of these goals, the Committee decided to keep the target range for the federal funds rate at 0 to 1/4 percent. With inflation well above 2 percent and a strong labor market, the Committee expects it will soon be appropriate to raise the target range for the federal funds rate. The Committee decided to continue to reduce the monthly pace of its net asset purchases, bringing them to an end in early March. Beginning in February, the Committee will increase its holdings of Treasury securities by at least $20 billion per month and of agency mortgage‑backed securities by at least $10 billion per month.“

According to The Fed Funds Futures data, the market is anticipating 1 rate increase at the March FOMC meeting. And another at the June FOMC meeting.

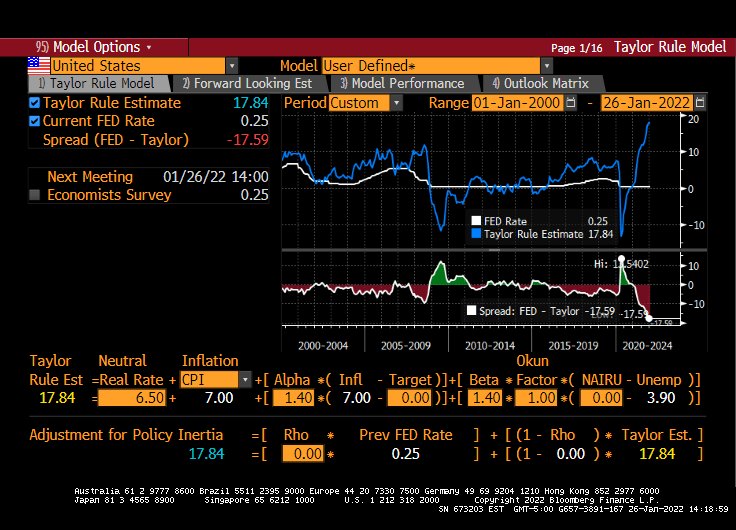

The Taylor Rule (not used by Jay and The Gang), suggests that The Fed should have their target rate at almost 18%! NOT 0.25%.

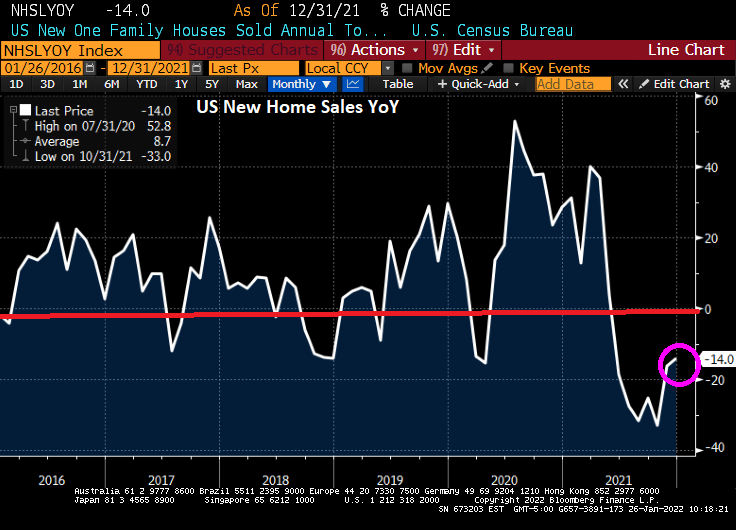

US new home sales spiked in December by 11.9% from November, but were down 14% year-over-year.

But the median price of new home sales (YoY) declined to 3.4%.

The Midwest saw a surge in new home sales (+56%).

The MBA’s mortgage applications index shows declining purchase applications (-1.83%) and declining refinancing applications (-12.60%) as mortgage rates increased from 3.64% to 3.72% for the week of 01/21.

Now, mortgage purchase applications rose for the week of 01/21 if we used non-seasonally adjusted data.

Interest rate hikes from the U.S. Federal Reserve and other central banks are likely to worsen a global debt crisis, particularly for developing countries, according to a new report from U.K. non-profit the Jubilee Debt Campaign.

In a report published Sunday, the Jubilee Debt Campaign highlighted that developing countries’ debt payments rose 120% between 2010 and 2021, and are currently at their highest since 2001. The average portion of government revenues channeled toward external debt payments increased from 6.8% in 2010 to 14.3% in 2021, with payments shooting up in 2020.

The sharp increase in debt payments is hindering countries’ economic recovery from the pandemic, the report suggested, and rising U.S. and global interest rates in 2022 could exacerbate the problem for many lower income countries.

Kristalina Georgieva, managing director of the International Monetary Fund, said last week that Fed rate hikes could “throw cold water” on already weak recoveries in certain countries. Higher U.S. interest rates, and thus a rise in the greenback, could make it more expensive for countries to meet their dollar-denominated debt obligations.

“The debt crisis continues to engulf lower income countries, with no end in sight unless there is urgent action on debt relief,” said Heidi Chow, executive director of the Jubilee Debt Campaign.

“The debt crisis has already stripped countries of the resources needed to tackle the climate emergency and the continued disruption from Covid, while rising interest rates threaten to sink countries in even more debt.”

Chow called on G-20 leaders to stop “burying their heads in the sand” and argued that the global economy urgently needs a “comprehensive debt cancellation scheme which compels private lenders to take part in debt relief.”

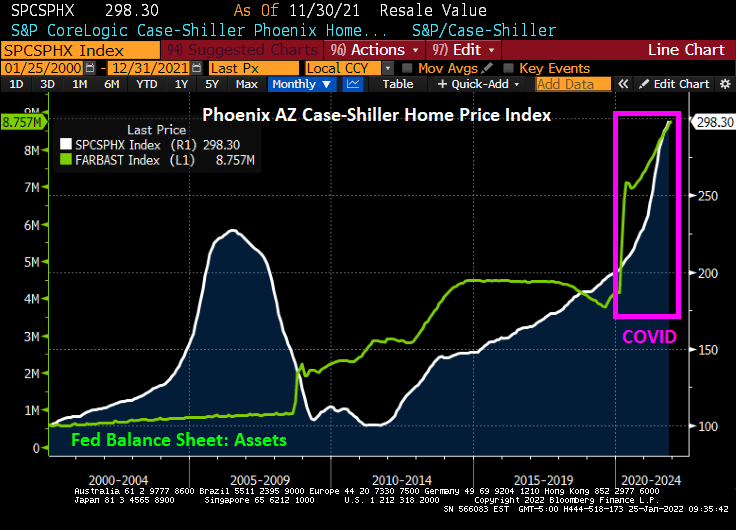

The Case-Shiller National home price index “slowed” to 18.81% YoY in November as The Fed continues its monetary stimulypto. Notice that The Fed is easing even when there is limited inventory available. Result? Hideous home price inflation.

Which metro area is growing the fastest, making housing even more unaffordable for renters? Phoenix AZ is growing at a 32.2% YoY clip while Washington DC is the slowest growing metro area at 11.1% YoY. The second faster growing metro area in Tampa FLA.

Phoenix AZ is growing at the fastest rate in the nation as The Fed still has its monetary stimulus at FULL SPEED AHEAD.

COVID and its omicron variant (as well as government reactions such as mask and vaccination mandates) are wreaking havoc on the global economy, but particularly in the USA where the Federal government dumped trillions of dollars in fiscal stimulus along with The Federal Reserve’s monetary stimulus into an economy not prepared for it. The result? INFLATION.

But global supply chains are nearing a turning point that’s set to help determine whether logistics headwinds abate soon or keep restraining the global economy and prop up inflation well into 2022, according to several new barometers of the strains.

Just a week before the start of Lunar New Year, the holiday celebrated in China and across Asia that coincides with a peak shipping season, economists from Wall Street to the U.S. central bank are unveiling a string of models in the hope of detecting the first signs of relief in global commerce.

From Europe to the U.S. and China, production and transportation have stayed bogged down in the early days of 2022 by labor and parts shortages, in part because of the fast-spreading omicron variant.

Among the big unknowns: whether solid demand from consumers and businesses will start to loosen up, allowing economies to finally see some easing in supply bottlenecks. Fresh indicators from the private and official sectors are in high demand because there’s still much uncertainty in industries overlooked by mainstream economics before the pandemic.

Once the realm of trade and industrial organization experts, supply chains “have shifted to center stage as a critical driver of sky-high inflation and a stumbling block to the recovery,” Bloomberg Chief Economist Tom Orlik said. “The profusion of new indices and trackers won’t unblock the arteries of the global economy any quicker. They should give policy makers and investors a better idea of how fast — or slowly — we are getting back to normal.”

The Bloomberg Economics Index

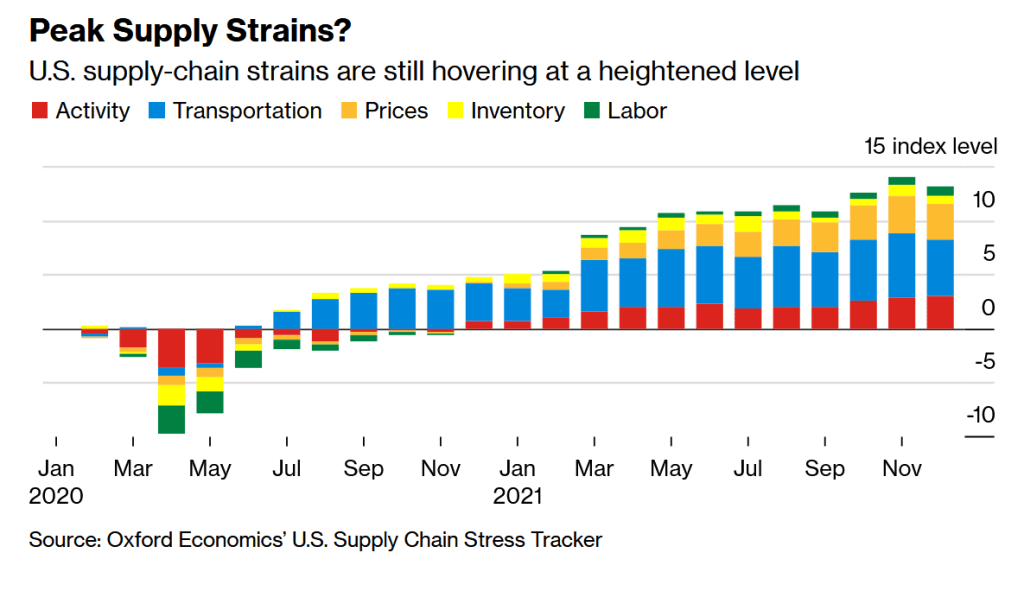

Bloomberg Economics’ latest supply constraint index for the U.S. shows that shortages have trended modestly lower for six months. Even so, strains remain elevated, and the wave of worker absenteeism is adding to the problems at the start of 2022.

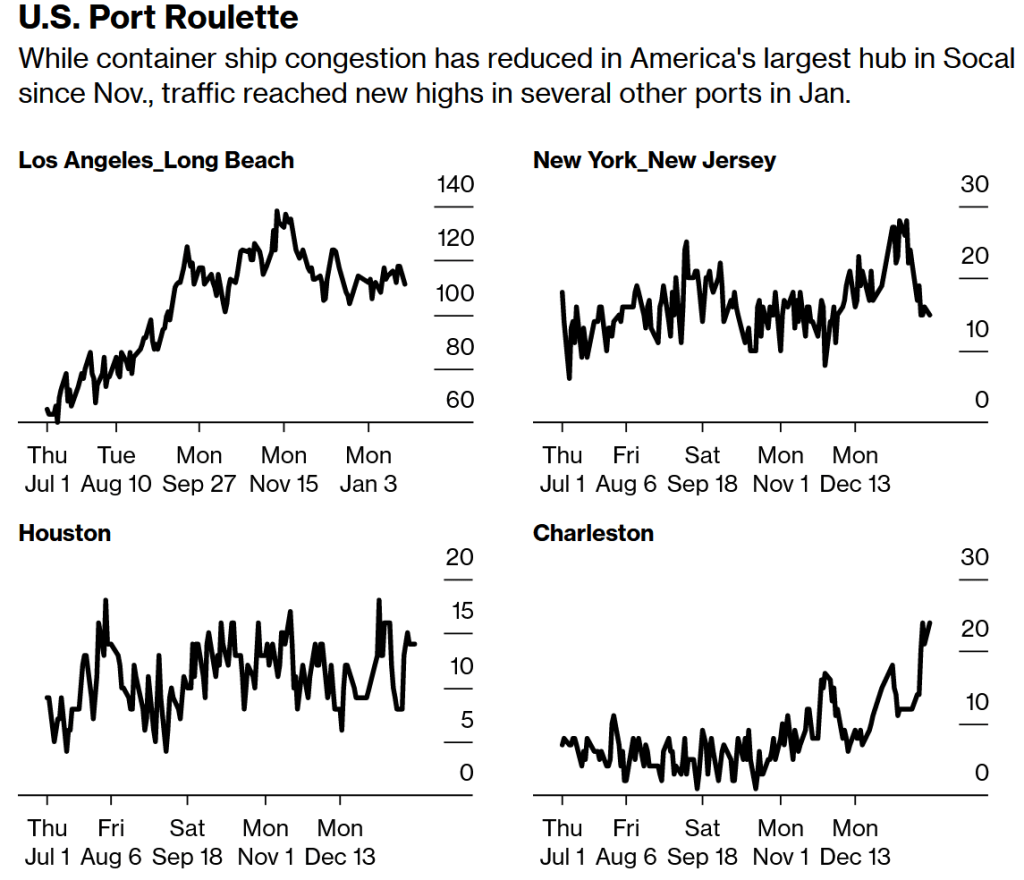

Port traffic tracked by Bloomberg shows container congestion continues to rankle the U.S. supply chain from Charleston, South Carolina, to the West Coast. The tally of ships queuing for the neighboring gateways of Los Angeles and Long Beach, California, continued to extend into Mexican waters, totaling 111 vessels late Sunday, nearly double the amount in July.

Source: Bloomberg, IHS Markit, Genscape

Note: Data counts the total number of container ships combined in port and in offshore anchorage area.

Kuehne+Nagel’s Disruption Indicator

Kuehne+Nagel International AG last week launched its Seaexplorer disruptionindicator, which the Swiss logistics company says aims to measure the efficiency of container shipping globally. It shows current disruptions at nine hot spots is hovering near “one of highest levels ever recorded,” with 80% of the problems happening at North American ports.

Flexport’s Guages

Another freight forwarder, San Francisco-based Flexport Inc., last year developed its Post-Covid Indicator to try to pinpoint the shift by American consumers back to purchasing more services and away from pandemic-fueled goods. The latest reading released Jan. 14 “indicates the preference for goods will likely remain elevated during the first quarter of 2022.”

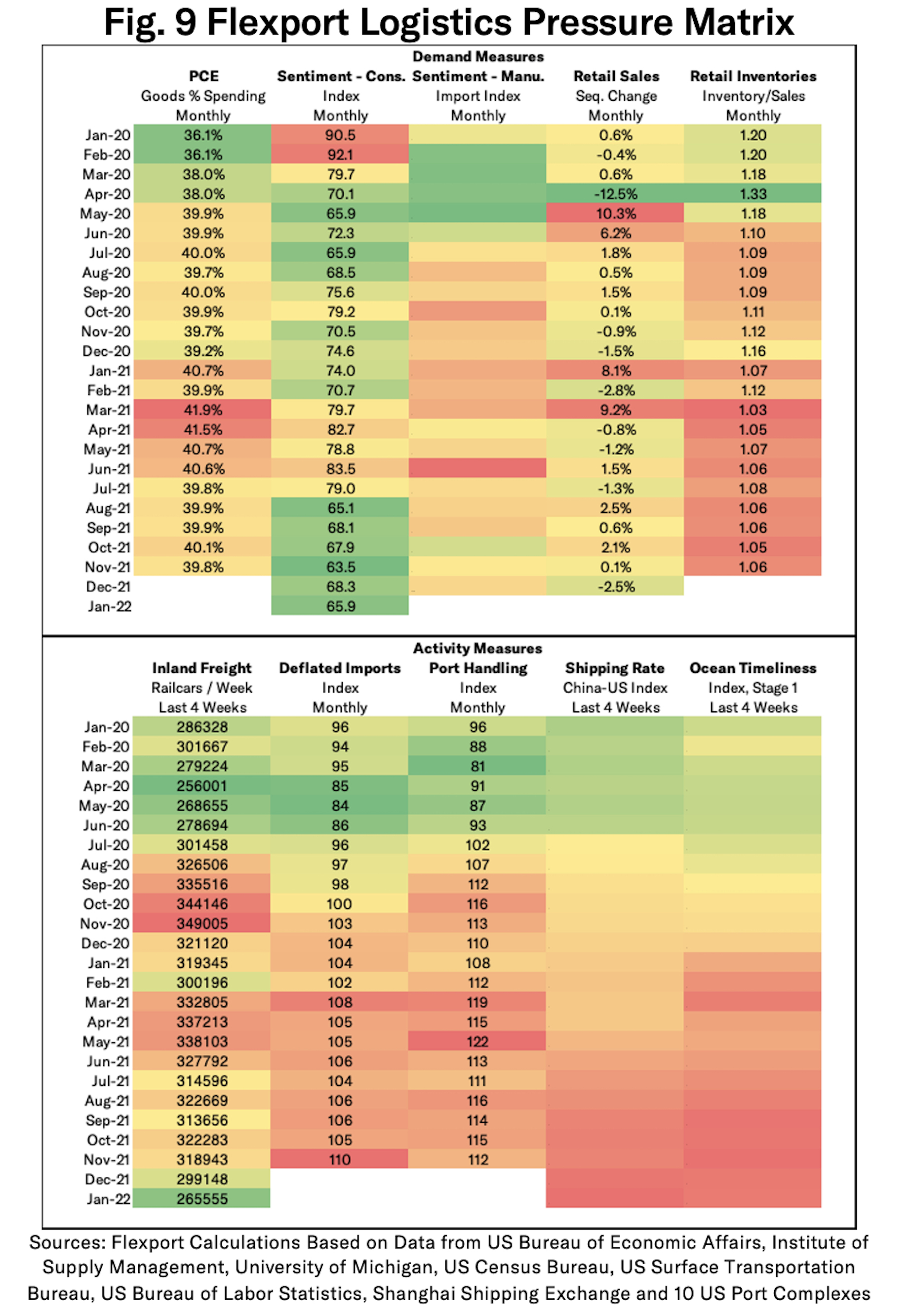

Flexport has a new Logistics Pressure Matrix with a heat map showing demand and logistics trends, and much of those numbers are still flashing yellow or red. Flexport supply chain economist Chris Rogers said in a recent online post that similar grids for Asia and European markets will be part of the research.

The Federal Reserve’s Stress Monitor

Adding their stamp to the burgeoning genre of supply stress indicators were three Ph.D. economists from the Federal Reserve Bank of New York, with the launch its Global Supply Chain Pressure Index. Rolled out earlier this month, it shows that the difficulties, “while still historically high, have peaked and might start to moderate somewhat going forward.” The New York Fed said it plans a follow-up report to quantify the impact of shocks on producer and consumer price inflation.

Morgan Stanley’s Index

Less than a week later came the Morgan Stanley Supply Chain Index. It lined up with the Fed’s view that frictions have probably peaked, though some of improvement ahead will come from a slowdown in the demand for goods.

“Supply disruptions remain a constraint to global trade recovery, but as firms continue to make capacity adjustments to address them, capacity expansion could mitigate these,” Morgan Stanley economists wrote in a report Jan. 12.

Citigroup’s Tool

Citigroup Inc. last week released research that was less optimistic yet complementary to the New York Fed’s work, which Citi said doesn’t factor the role of surging demand as a contributor to the supply disruptions. Sponsored Content The Collaboration Disconnect Atlassian

Co-written by Citi’s global chief economist Nathan Sheets, a former U.S. Treasury undersecretary for international affairs, the bank’s analysis “gives a more complete, and intuitive, picture of the current situation.” While strains may ease in coming months, Citi said, “these supply-chain pressures are likely to be present through the end of 2022 and, probably, into 2023 as well.”

The Keil Institute’s Flows Tracker

In Germany, the Kiel Institute for the World Economy updates twice a month its Trade Indicator, which looks at flows across the U.S., China and Europe. Its latest reading Jan. 20 shows that along the key trading route between Europe and Asia, there are 15% fewer goods moving than there would be under normal times. The last time the gap was that large was in mid-2020, when many economies were reeling from initial lockdowns, Kiel said.

More recently, “the omicron outbreak in China and the Chinese government’s containment attempts through hard lockdowns and plant closures are likely to have a negative impact on Europe in the spring,” says Vincent Stamer, head of the Kiel Trade Indicator, said in a post last week. “This is also supported by the fact that the amount of global goods stuck on container ships recently increased again.”

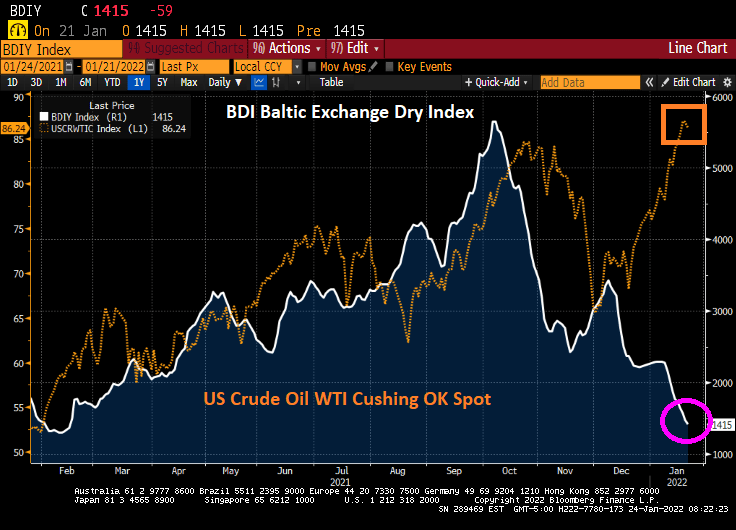

Baltic Dry Index

The Baltic Dry shipping cost index indicates that costs for shipping materials such as iron ore have decline to where it started under Biden, despite West Texas Crude Oil spot prices begin considerably higher thanks to Biden’s anti-fossil fuel policies.

So as the world comes out of Omicron (and whatever COVID variant rises to take its place), we should see a normalization in the supply chain. And with Intel building a new chip factory in New Albany Ohio (aka, outskirts of Columbus). the supply chain woes will eventually subside.

Then again, there is always the Russia-Ukraine tension that may erupt into a disaster. I suggest that President Biden sent Hunter Biden to Moscow to negotiate on behalf of The Ukraine.

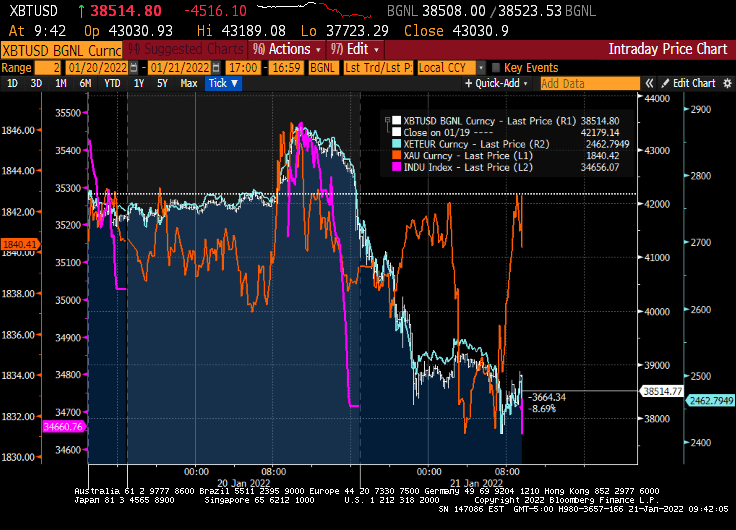

It has been a tough 7 days for Bitcoin, Ethereum and the NASDAQ composite index as The Fed is anticipated to raise their target rate AND engage in quantitative tightening.

While the NASDAQ composite index has been deflating over past 7 days, Bitcoin and Ethereum plunged in recent days. What is going on??

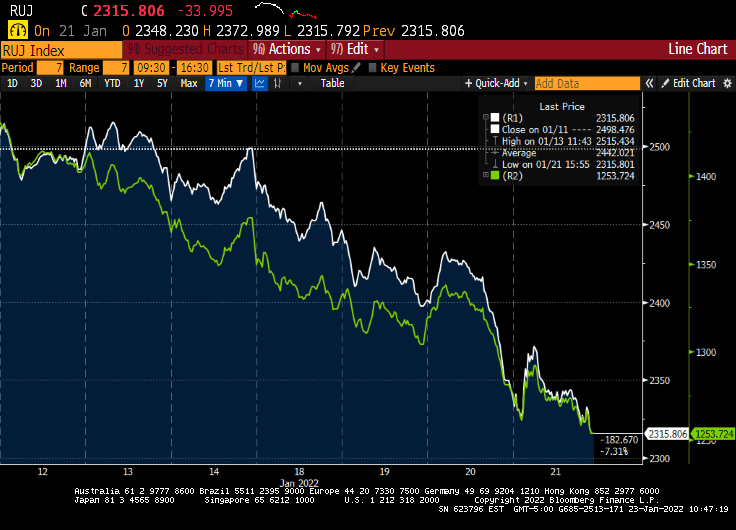

The Russell 2000 value (white) and growth (green) indices are both deflating.

With regards to anticipated Fed rate increases, Fed Funds Futures are signaling almost 4 rate hikes in 2022 and 4 by the February 2023 meeting.

Then we have the massive increase in The Fed’s balance sheet after COVID struck in early 2020. Now, with the S&P 500 skyrocketing (until 7 days ago), why is The Fed buying sooooo much Agency MBS??

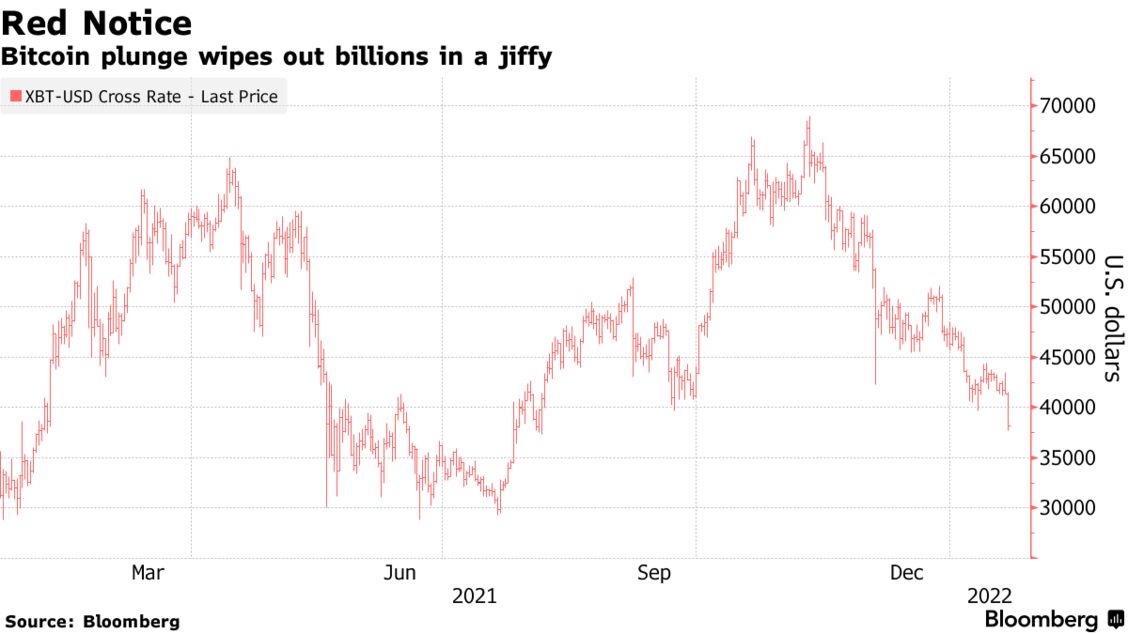

For Bitcoin, there’s only been one constant recently: decline after decline after decline. And the superlatives have piled up really quickly.

With the Federal Reserve intending to withdraw stimulus from the market, riskier assets the world over have suffered. Bitcoin, the largest digital asset, lost as much as 8.7% Friday and dropped below $38,000 to its lowest level in six months. Since its peak in November, it has lost 40% of its value. Other digital currencies have suffered just as much, if not more, with Ether and meme coins mired in similar drawdowns.

Bitcoin’s decline since that November high has wiped out more than $570 billion in market value, and roughly $1.17 trillion has been lost from the aggregate crypto market. While there have been much larger percentage drawdowns for both Bitcoin and the aggregate market, this marks the second-largest ever decline in dollar terms for both, according to Bespoke Investment Group.

“It gives an idea of the scale of value destruction that percentage declines can mask,” wrote Bespoke analysts in a note. “Crypto is, of course, vulnerable to these sorts of selloffs given its naturally higher volatility historically, but given how large market caps have gotten, the volatility is worth thinking about both in raw dollar terms as well as in percentage terms.”

Bloomberg

With the Fed’s intentions rocking both cryptocurrencies and stocks, a dominant theme has emerged in the digital-asset space: cryptos have twisted and turned in nearly exactly the same way as equities have.

You must be logged in to post a comment.