The National Association of Home Builders market index fell more than expected in September to 46, the lowest reading since 2012 (if I exclude the Covid economic shutdown).

Note that the NAHB market index is declining along with at the increase in the 30yr mortgage rate.

Inflation is stubborn because “goin’ green!” by 1) restricting US fossil fuel production and exploration and 2) Biden/Congress endless spending splurge since Covid. So, The Federal Reserve has a tough problem: cooling inflation while US energy prices are up 54% under Biden. And those higher energy prices have percolated through the entire economy in terms of food prices and heating prices.

Where do we sit? The US Treasury 10yr-2yr yield curve remains inverted (a sign of impending recession). Mortgage rates are the highest in 14 years as The Fed tightens.

If we look at Fed Funds Futures data, we can see that traders expect The Fed’s target rate to rise to 4.395% by March 2023’s FOMC meeting. Then traders expect The Fed to take their enormous foot off the tightening pedal.

Yes, inflation is crushing the middle class and low-wage workers. Average hourly earnings YoY after we subtract inflation are negative.

Taylor Rule? Currently, the Taylor Rule based on Core inflation of 4.56% YoY suggests a Fed target rate of 9.14%. Since traders anticipate the target rate to peak at 4.395%, The Fed will almost be halfway towards cooling inflation.

The problem is … Fed Chair Powell and Treasury Secretary Yellen don’t like rules limiting their “power.” Powell and Yellen think the Taylor Rule is a New Jersey ham product.

US mortgage applications dropped to the lowest level since 1997. I wonder if President Biden will invite boring crooner James Taylor back to the White House to sing about the collapsing mortgage market? Perhaps he can sing “Shower The People” and change the lyrics to “Shower ON The People.”

Mortgage applications decreased 1.2 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending September 9, 2022. This week’s results include an adjustment for the observance of Labor Day. The Refinance Index decreased 4 percent from the previous week and was 83 percent lower than the same week one year ago. The seasonally adjusted Purchase Index increased 0.2 percent from one week earlier. The unadjusted Purchase Index decreased 12 percent compared with the previous week and was 29 percent lower than the same week one year ago.

The Bankrate 30-year mortgage rate is now at the highest level since 2008 at the advent of Fed’s QE.

REAL average hourly earnings growth remain in the toilet at -3.06% YoY.

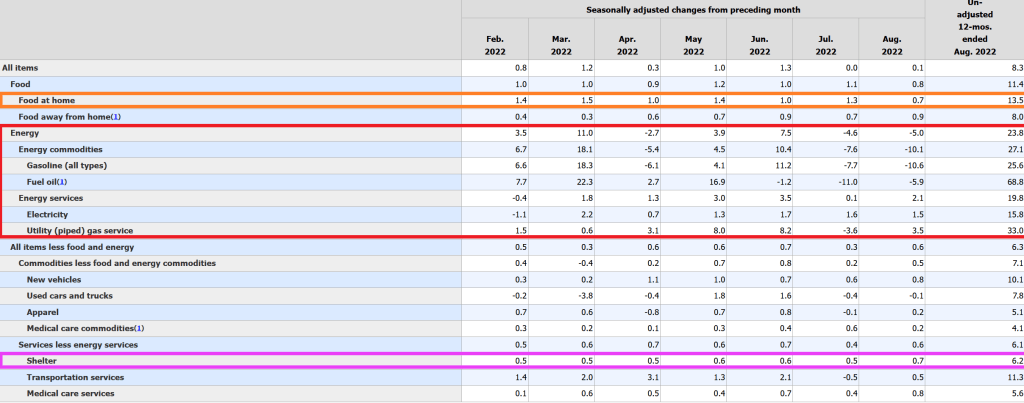

Fuel oil used to heat homes rose 68.8% YoY. Food at home rose 13.5% YoY while rent (shelter) rose “only” 6.2% YoY. Wow, renters are REALLY getting the short-end of the stick from The Fed and the Biden Administration!!

New vehicles are UP 10.1% YoY. Good luck buying those “cheap” electric cars that Mayor Pete Buttigieg trumpets! And wait for the bill when the battery needs to be replaced!!!

Freddie Mac’s 30-year mortgage commitment rate just rose to its highest level since … The Fed initiated Quantitative Easing (aka, fanatical money printing) during the financial crisis.

The good news? The US inflation report is likely to show a slowing of the inflation rate to around 8% YoY and -0.1% MoM. Why? Gasoline prices are cooling thanks to the global economic slowdown.

While gasoline and food prices are falling, CORE US inflation, the inflation rate excluding food and energy, is expected to rise to around 6.1% YoY and +0.30% for August.

The Federal government reaction to the Covid outbreak in early 2020 included massive monetary stimulus, Federal government spendathons and Biden’s green energy policies have resulted in a sizzling 8.5% inflation rate (update on Monday morning).

The problem is that The Federal Reserve is far behind the inflation curve with their target rate at only 2.5%. And The Fed’s balance sheet remains near $9 TRILLION in assets held.

In Euroland, we are seeing a similar problem (Frankfurt, we have a problem!). The Eurozone inflation rate is at 9.1% while their version of The Fed Funds Target rate is only 0.75%, a large catch-up gap.

If we look at the Taylor Rule for the US using headline inflation, we see that The Fed needs to raise their target rate to … 21.72% to crush inflation.

In Euroland, the problem is similar. At 9.10% inflation, the ECB will have to raise their version of The Fed’s target rate to 16.80% to combat inflation. As if that will happen in either the US or Euroland.

On a different note, is it my imagination or does US Democrat Senate candidate from Pennsylvania John Fetterman look like the alien from the flick “Battleship”?

The monetary noose tightens on the housing and mortgage markets.

Mortgage applications decreased 0.8 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending September 2, 2022. They are now the lowest since 1999.

The Refinance Index decreased 1 percent from the previous week and was 83 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 1 percent from one week earlier. The unadjusted Purchase Index decreased 3 percent compared with the previous week and was23 percent lower than the same week one year ago.

At least the percentage of adjustable rate mortgages (ARMs) remained the same at 8.5%.

For the sake of the housing and mortgage market, somebody stop Powell and The Gang from tightening!

(Bloomberg)Investors who might be looking for the world’s biggest bond market to rally back soon from its worst losses in decades appear doomed to disappointment.

The US employment report on Friday illustrated the momentum of the economy in face of the Federal Reserve’s escalating effort to cool it down, with businesses rapidly adding jobs, pay rising and more Americans entering the workforce. While Treasury yields slipped as the figures showed a slight easing of wage pressures and an uptick in the jobless rate, the overall picture reinforced speculation the Fed is poised to keep raising interest rates — and hold them there — until the inflation surge recedes.

Swaps traders are pricing in a slightly better-than-even chance that the central bank will continue lifting its benchmark rate by three-quarters of a percentage point on Sept. 21 and tighten policy until it hits about 3.8%. That suggests more downside potential for bond prices because the 10-year Treasury yield has topped out at or above the Fed’s peak rate during previous monetary-policy tightening cycles. That yield is at about 3.19% now.

Then we have Bankrate’s 30-year mortgage rate soaring on Fed intervention expectations.

Inflation? US inflation is near its highest in 40 years and the USDollar Plain Vanilla Swap was at 0.50 when Biden first took office as President and is now 3.371 (quite an increase!).

Here is an interesting chart of FNCL 2% Agency MBS.

You must be logged in to post a comment.