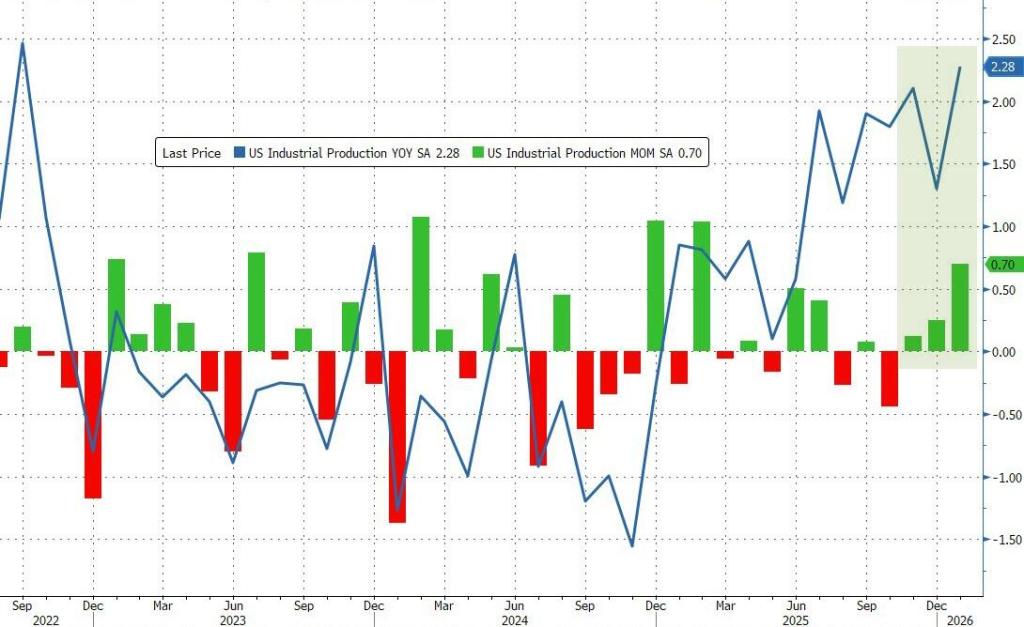

So much for the leftist fearmongers claiming that Trump Tariffs will kill US manufacturing, In January, US industrial production rose 0.7% MoM. And 2.28% YoY.

Capacity utililzation rose in January to 76.22%.

Pass the Save Act and don’t listen to leftist propaganda that women won’t be allowed to vote. Then get a passport and show that.

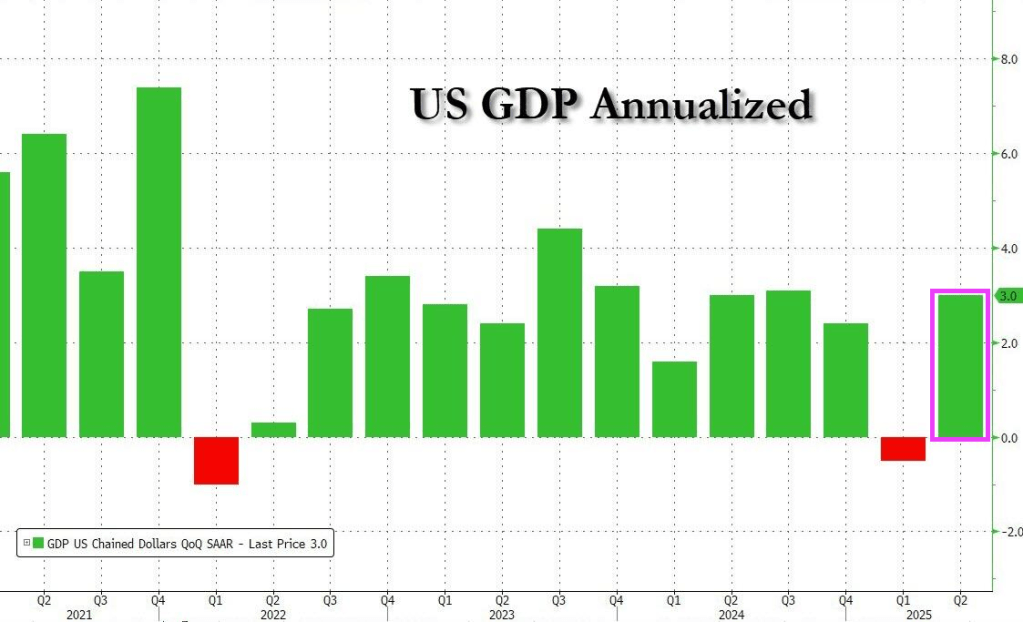

The Bureau of Econ Analysis reported that the first estimate of Q2 GDP came in at an unexpectedly brisk 3.0%, a complete reversal of the -0.5% decline in Q1.

Personal Consumption added 0.98% to the bottom line GDP, up from 0.31% in Q1.

Fixed Investment came at 0.08%, a big drop from the 1.31%, and perhaps the only concerning point in today’s report: was there really no major data center investments in the second quarter… and if so what are the hyperscalers doing?

The change in private inventories was a big drop, printing at -3.17% in the first estimate, up from 2.59% in the first quarter, and an expected reversal as retailers unloaded all that inventory they piled up ahead of tariffs.

Trade or net exports (exports less imports), came at a whopping 4.99% – the biggest addition to the bottom line GDP number – as imports collapsed and added 5.18% to GDP, a stark reversal to the -4.66% contraction in Q1.

Finally, government added just 0.08% to GDP, a reversal of the 0.10% subtraction in Q1.

So, the BEA reported 3.0% real GDP growth, `the Atlanta Fed’s GDP Now latest estimate was 2.9 percent. Pretty close!

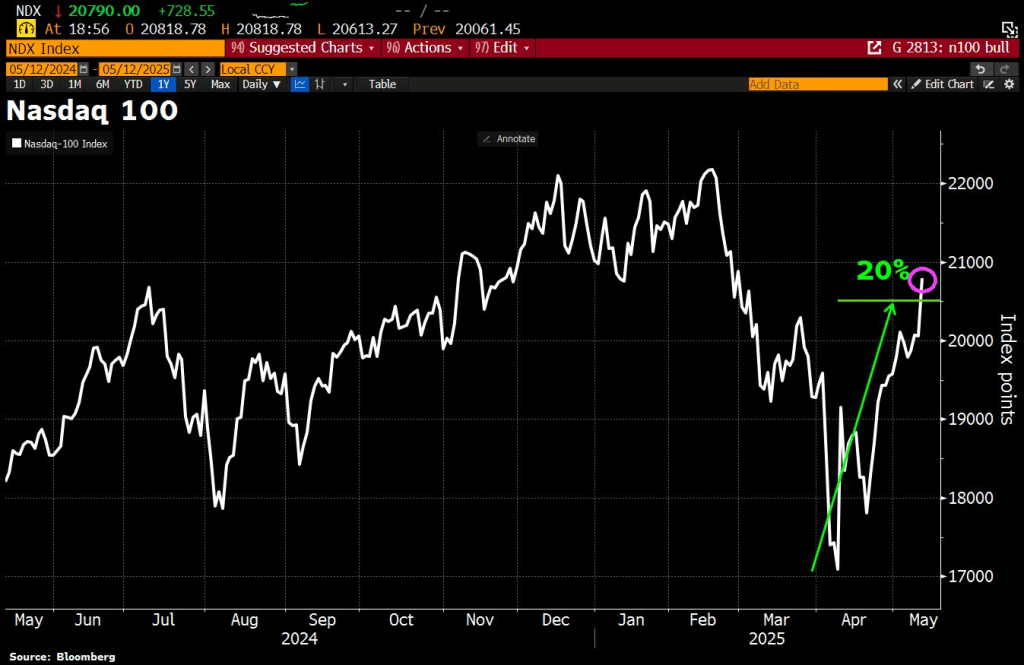

Well, U.S. and China reached an agreement to lower tariffs in a 90-day cool-off period. Despite China claiming they would NEVER agree to tariffs! The result? The NASDAQ 100 rose to its highest level since mid-February.

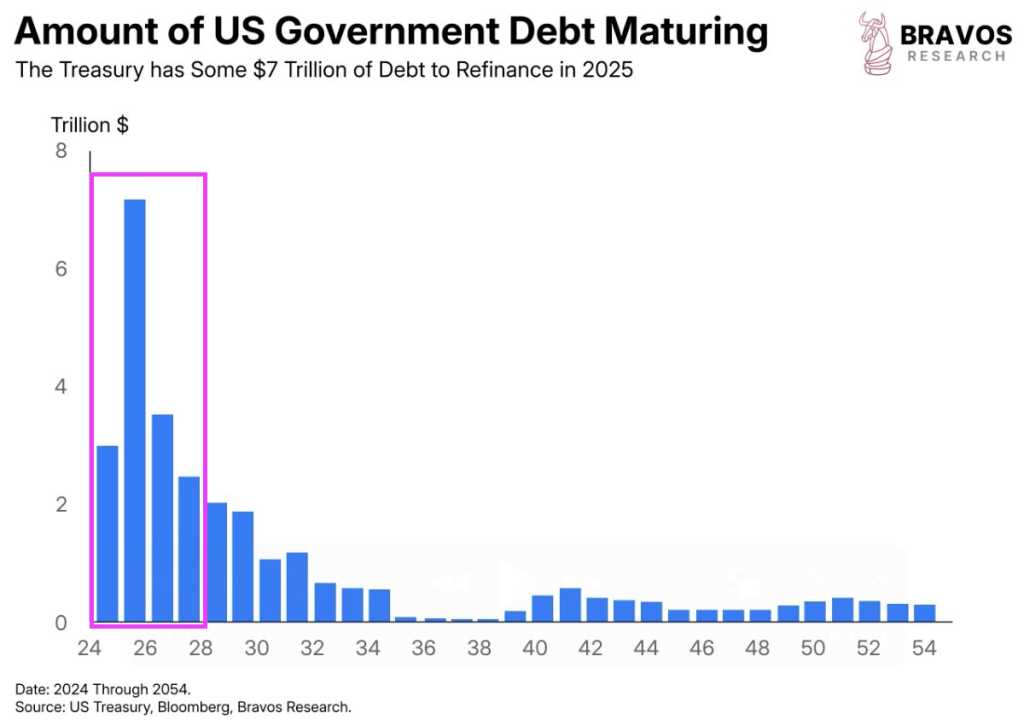

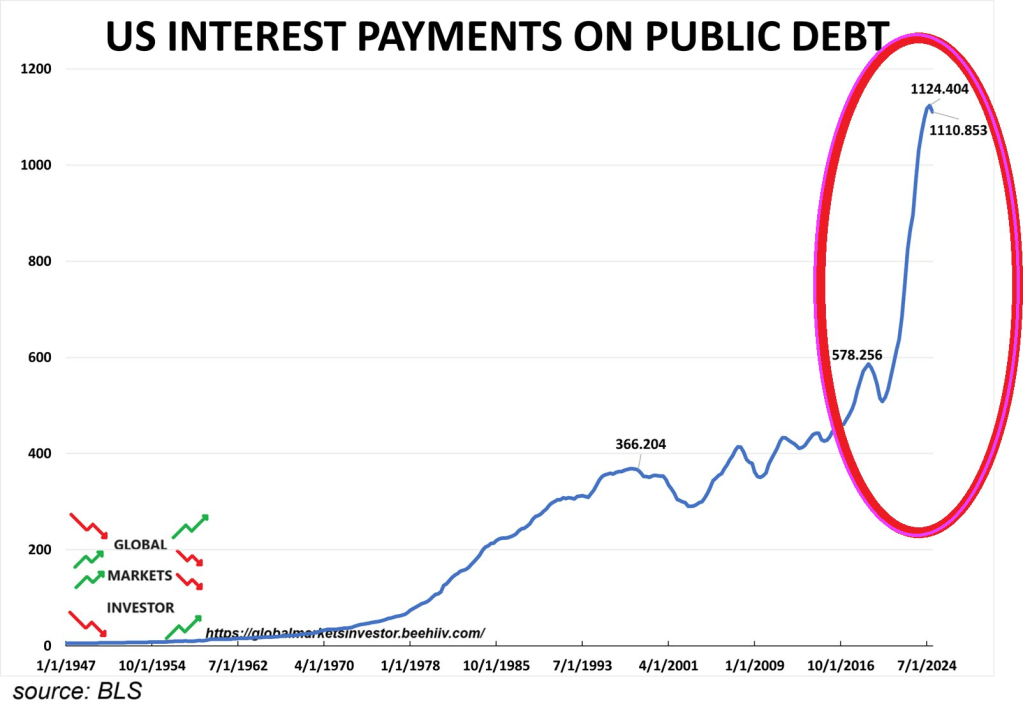

Doge is necessary to get close to closing the budget gap (tax receipts – spending). Biden left Trump and the US with an untenable fiscal situation (think Cloward/Piven). Extremely large debt load with debt maturing over the next couple of years. Thanks to former Treasury Secretary Janet “The Snake” Yellen government funding formula using ST government debt. And its time to pay the piper to pay for Biden’s overspending and Yellen’s Treasury mismanagement.

Most of the Treasury debt that Treasury Secretary Bessent must refinance is short-term.

And with interest rates higher under Trump/Bessent than Biden/Yellen, US Interest Payments on Public Debt is expected to keep rising.

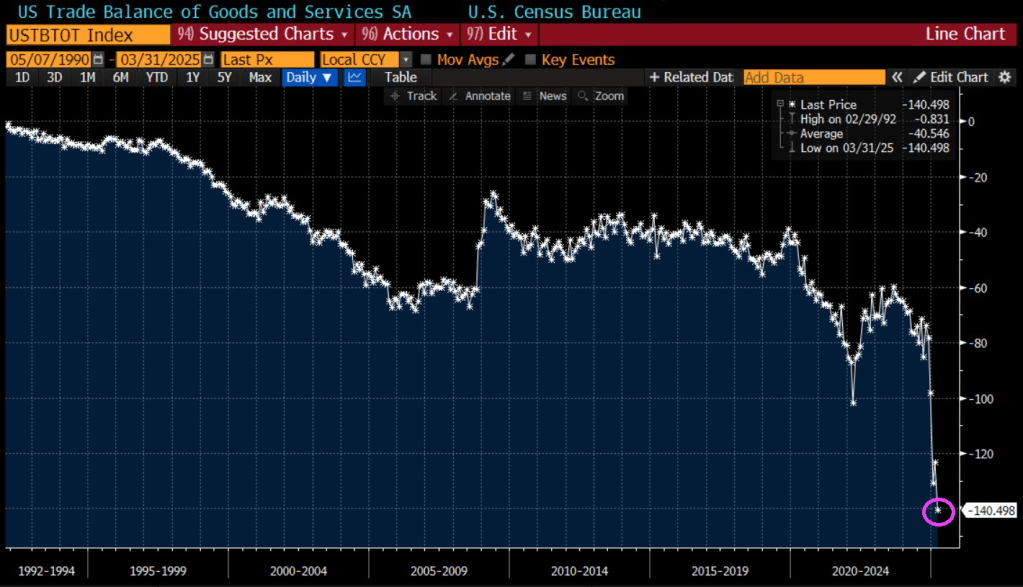

And US trade balance fell to -140.5.

So, were Biden’s economic policies (and Yellen’s Treasury mismanagement) an intentional Cloward-Piven strategy?

Here are Columbia sociologists Cloward and Piven attending a bill signing by President Bill Clinton.

Despite the slump in ‘soft’ survey data, analysts expected Empire Fed Manufacturing to bounce back from March’s tumble to one year lows and they were right with the headline index rising from -20.0 to -8.1 (considerably better than the -13.5), but still negative. However, while current conditions jumped, expectations plunged to the lowest since 9/11/.

Obama/Biden/Harris/Schumer/Pelosi have let the US be the punks for China. Trump is simply trying to level the playing field and China’s Xie doesn’t like the new equilibrium.

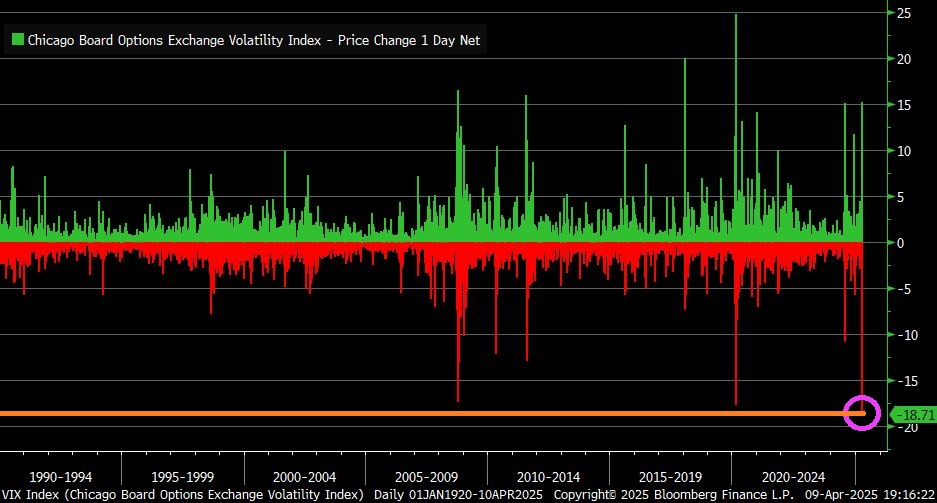

VIX Index fell by 18.7 points yesterday … largest one-day decline in history.

The correlation between stock prices and bond yields has returned to positive territory — hinting at a period of distress in equities and a regime shift in equity and bond markets where recession fears, rather than inflation, may be starting to drive direction of both. The correlation between the two asset classes was positive for the better part of 20 years prior to the pandemic, suggesting equities trended in the direction of yields as inflation mostly coincided with growth. Stocks held a negative correlation to yields throughout most of the 1980s and 1990s, when inflation hurt stocks — and that phenomenon returned for the 2022-24 bear market and recovery period.

Notably, major stock corrections occurred each time the correlation jumped out of its primary regime.

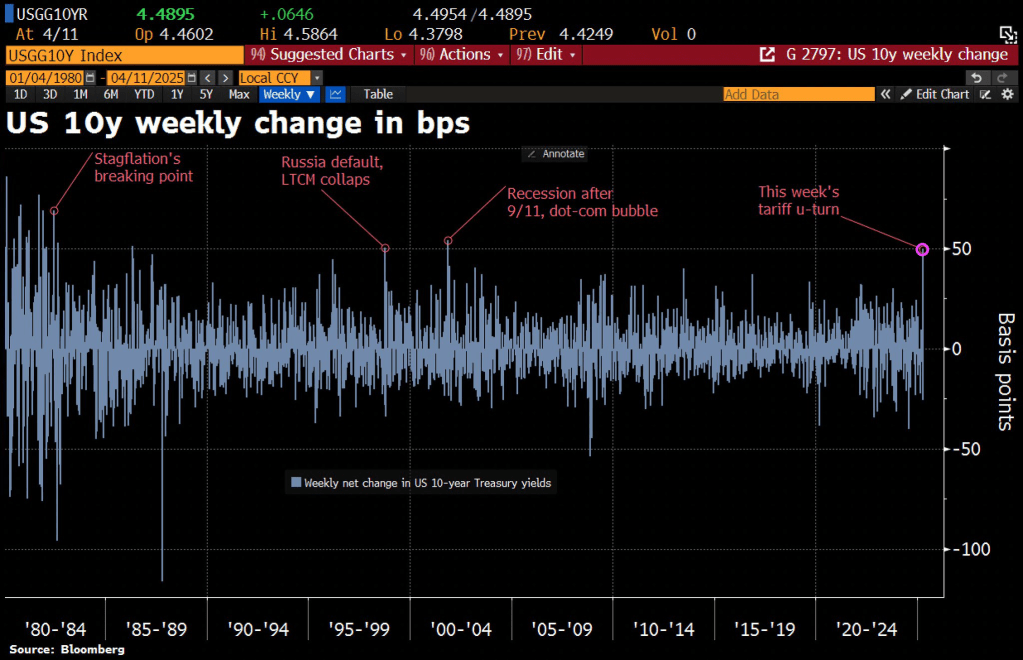

Thunderstruck! The tariff kerfuffle between the Trump Administration and China is causing turbulence in the Treasury market. The 10-year Treasury rate is soaring with China’s counterpunching.

MBS spreads are widening.

Along with volatility.

But corporate spreads are widening more than MBS spreads.

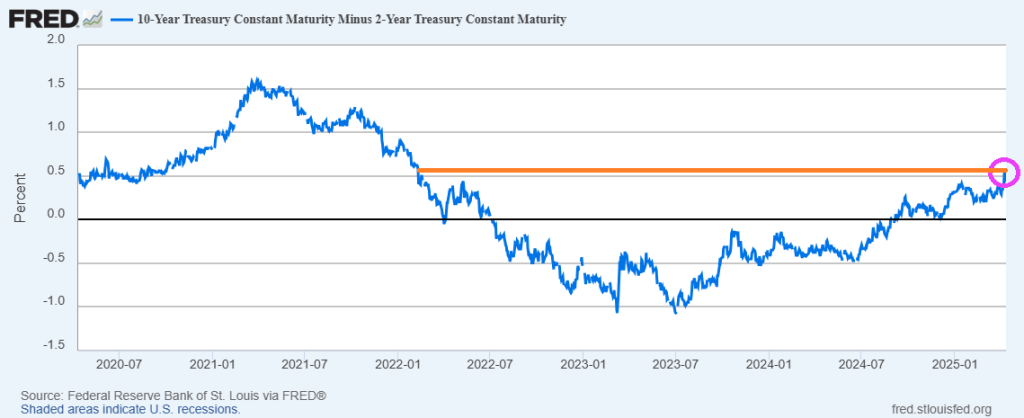

The 10Y-2Y yield curve has risen to the highest level since the early days of “China Joe” Biden.

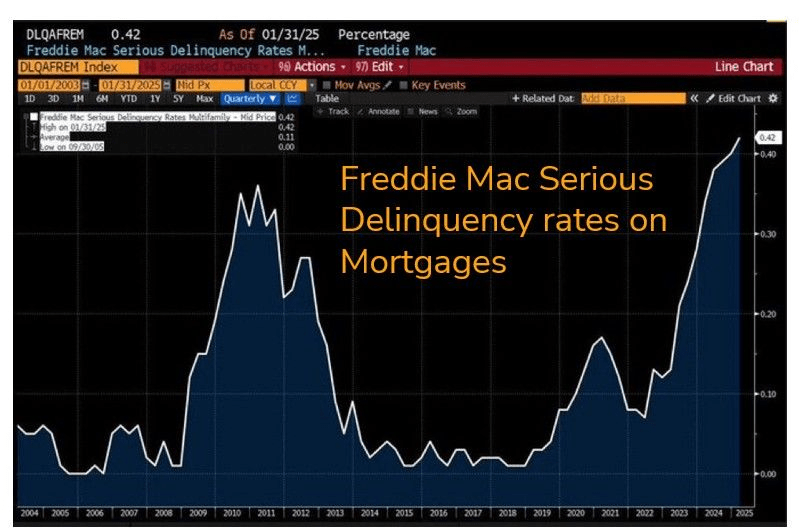

On a related note, Freddie Mac serious delinquency rates on mortgages is now the highest since the financial crisis.

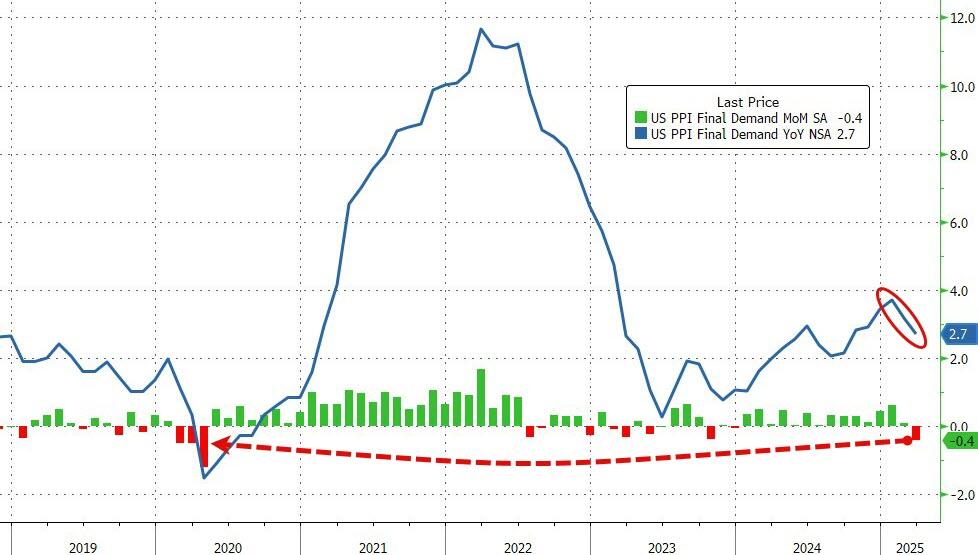

Headline PPI fell (yes fell) 0.4% MoM (dramatically cooler than the 0.2% MoM rise expected), dragging the headline index down to +2.7% YoY.

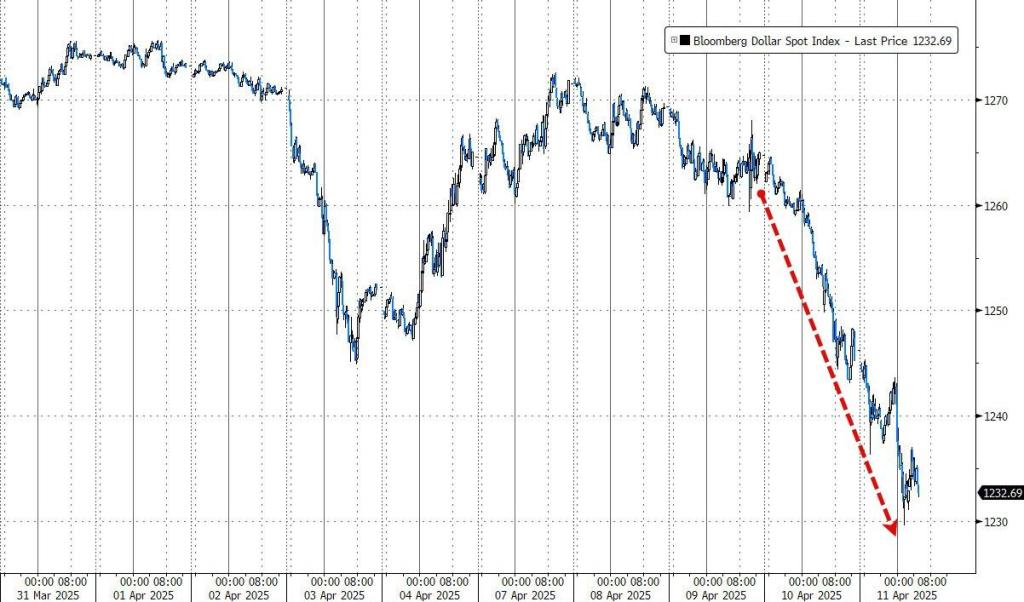

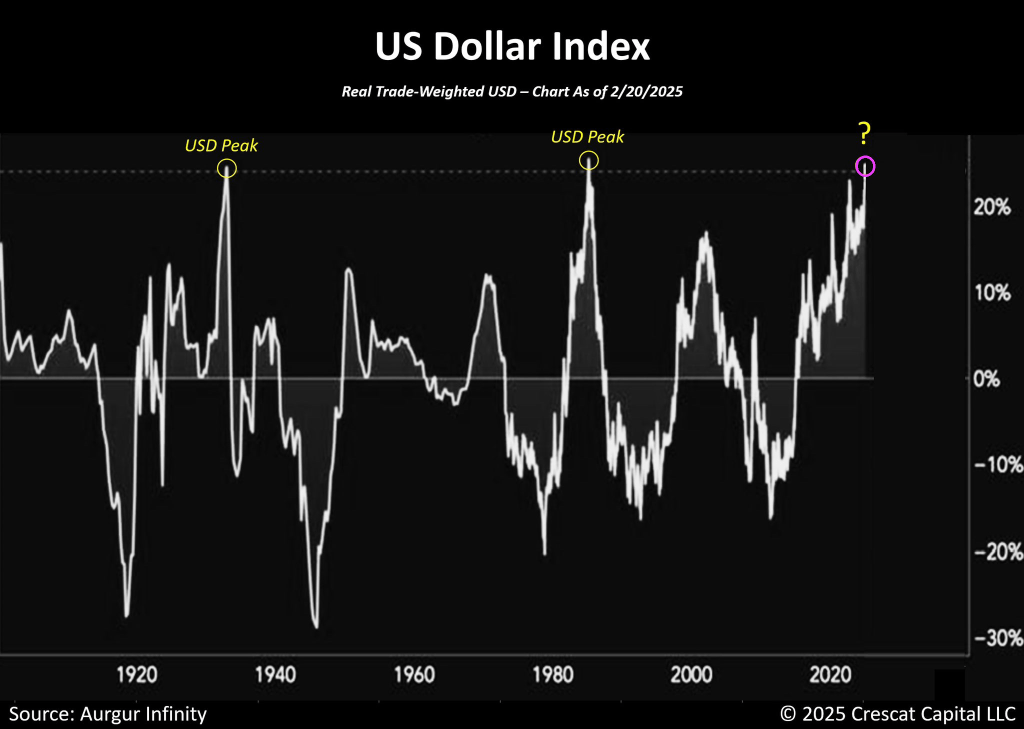

The market is re-assessing the structural attractiveness of the dollar as the world’s global reserve currency and is undergoing a process of rapid de-dollarization.

US tariff policies for the last 50 years represent a folly. Particularly since Presidents Obama and Biden (along with Chuck Schumer and Nancy Pelosi) did nothing to correct the enormous disparity in tariffs. Trump is trying to do something to right the ship before it sinks like The Titanic.

Victor Davis Hanson wrote in the Daily Signal, “China has prohibitive tariffs, so does Vietnam, so does South Korea, so does Japan, so does Mexico, and so does Europe. So do a lot of countries. So does India. But if tariffs are so destructive to their economies, why is China booming?

Why is Canada mad at us when it’s running a $63 billion surplus and it has tariffs on some American products at 250%. Doesn’t it seem like the people who started this asymmetrical—if I could use the word—trade war should be the culpable people, not the people who are reluctantly reacting to it?

Were tariffs leveled against countries that had no tariffs against us?

The US hasn’t run a trade surplus since 1975 or 50 years. So, it wasn’t suddenly we woke up and said, “It’s unfair. We want commercial justice.” No. We’ve been watching this happen. For 50 years it’s been going on. And no president, no administration, no Congress in the past has done anything about it.

In the postwar period, we were so affluent, so powerful—Europe, China, Russia were in shambles—that we had to take up the burdens of reviving the economy by taking great trade deficits. Fifty years later, we have been deindustrialized. And the countries who did this to us, by these unfair and asymmetrical tariffs, did not fall apart. They did not self-destruct. They apparently thought it was in their self-interest. And if anybody calibrates the recent gross domestic product growth of India or Taiwan or South Korea or Japan, they seem to have some logic to it.

There’s a final irony. The people who are warning us most vehemently about this tariff quote the Smoot-Hawley Act of 1930. But remember something, that came after the onset of the Depression—after. The stock market crashed in 1929. That law was not passed until 1930. It was not really amplified until ’31. And here’s the other thing that they were, conveniently, not reminded of: We were running a surplus. That was a preemptive punitive tariff, on our part, against other countries. We had a trade surplus. And it was not 10% or 20%. Some of the tariffs were 40% and 50%. And again, it happened after the collapse of the stock market.

In conclusion, don’t you find it very ironic that Wall Street is blaming the Trump tariffs for heading us into a recession, if not depression, when the only great depression we’ve ever had was not caused by tariffs but by Wall Street?”

Average reciprocal tariffs could rise to 35%!

The Mag 7 index has gotten crushed under Trump’s tariffs.

Corporate bond yield has soared with Trump’s tariffs.

The market correction thus far is -17.5%, not even close to the worst correction since 2009 (-35.4% in 2020).

Trump inherited a brittle economy from “The Fool” Joe Biden. And it is shown up.

The Trump Administration is fighting the remnants of Biden’s policies by cutting spending (DOGE) and deregulation.

All this has resulted in a soaring US Dollar.

Tarot cards have officially renamed “The Fool” card as “The Biden.” Although in Washington DC, there is no shortage of fools (see Maxine Waters (D-CA) and Rashida Talib (D-MI).

You must be logged in to post a comment.