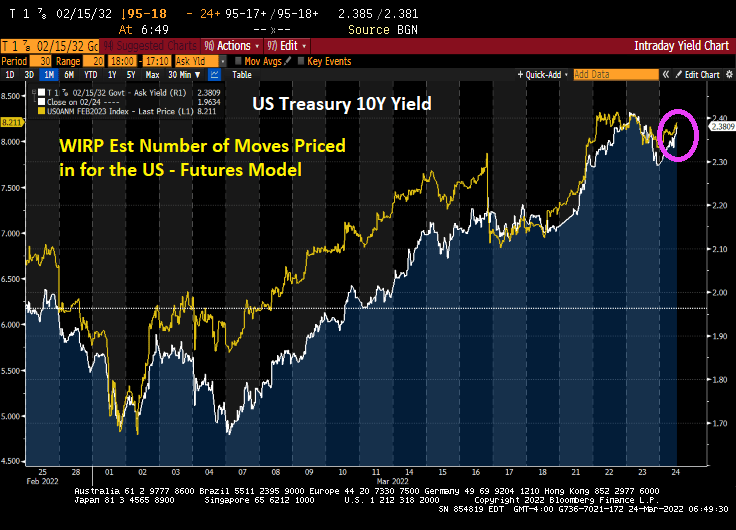

Overnight, the US Treasury yield rose to 2.38% as the number of forecast Fed rate hikes rose to 8.211. So, enjoy “low” rates while you can.

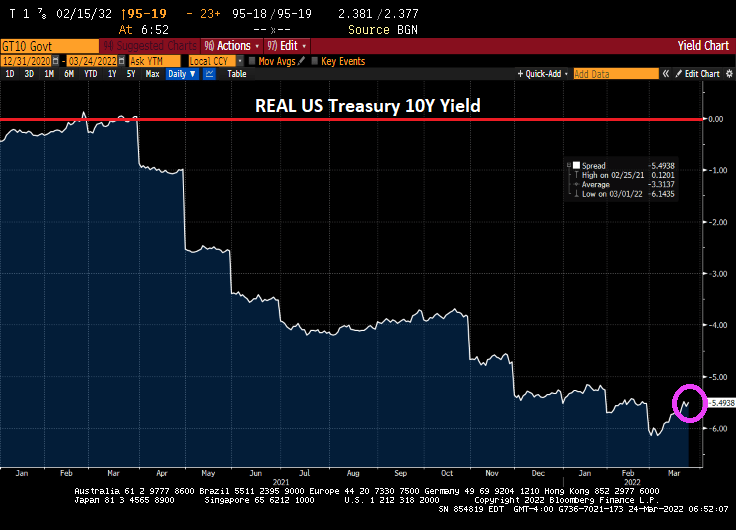

If we back out the highest inflation rate in 40 years, the REAL 10Y Treasury yield is -5.50%.

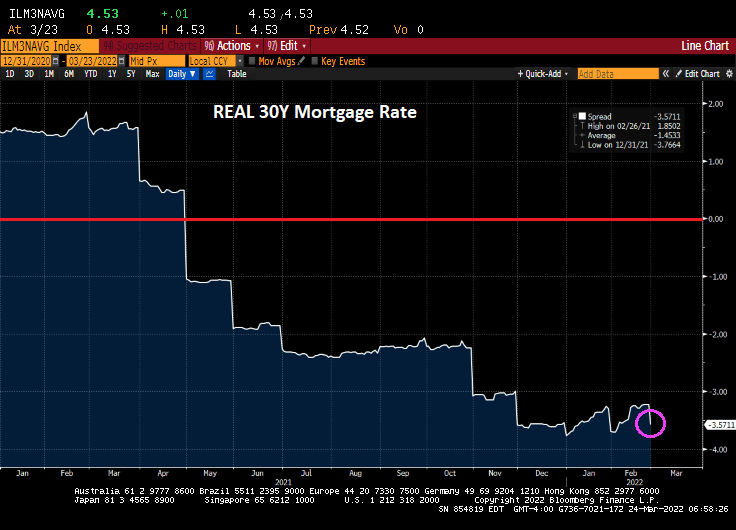

And the REAL 30Y mortgage rate is -3.57%.

Of course, the meteoric rise in inflation is due largely to Biden’s attack on the fossil fuel industry (until Russia’s invasion of Ukraine distracted from Biden’s inflation fiasco). Remember, Russia didn’t invade Ukraine until February 2022.

Wait. I thought the purpose of Biden’s executive orders was to reduce dependence on fossil fuels by driving up gasoline and natural gas prices producing a shift to “green energy.” Won’t these “gas rebates” simply continue the consumption of gasoline and natural gas? And increase inflation??

As Winston Churchill once said, “Never let a crisis go to waste.”

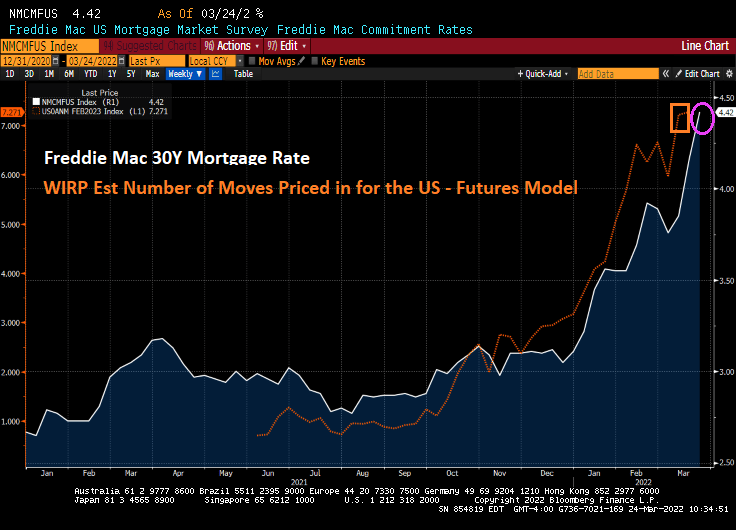

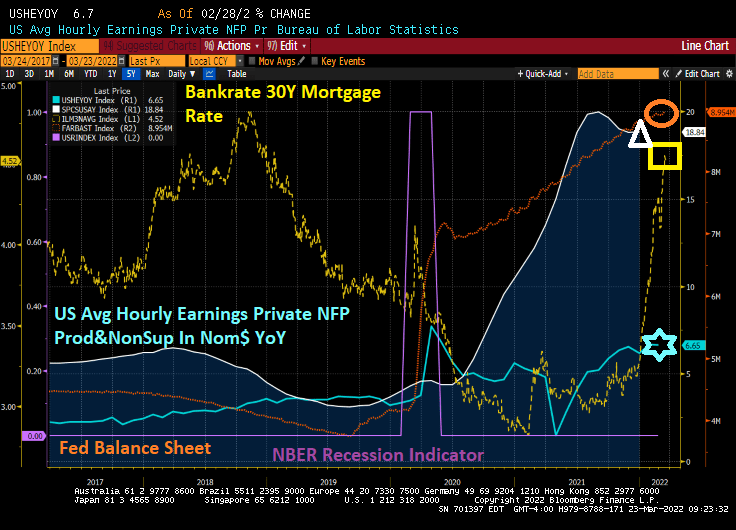

US mortgage rates are soaring, US home prices are soaring, The Fed’s balance sheet is still growing, and US average hourly earnings are growing at a fraction of home price growth.

The unafforable nature of US housing prices is similar to that of 2005-2007 when home price growth greatly exceeded wage growth.

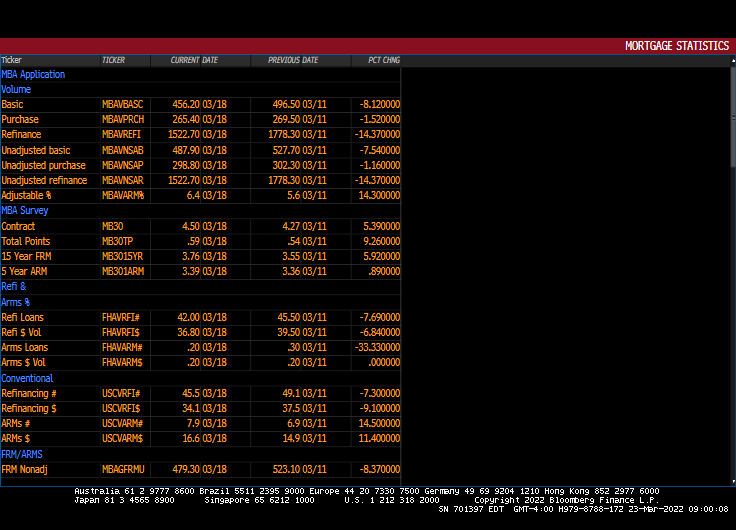

Another side effect of soaring mortgage rates: MBA refinancing applications plunged 14.37% from the preceding week.

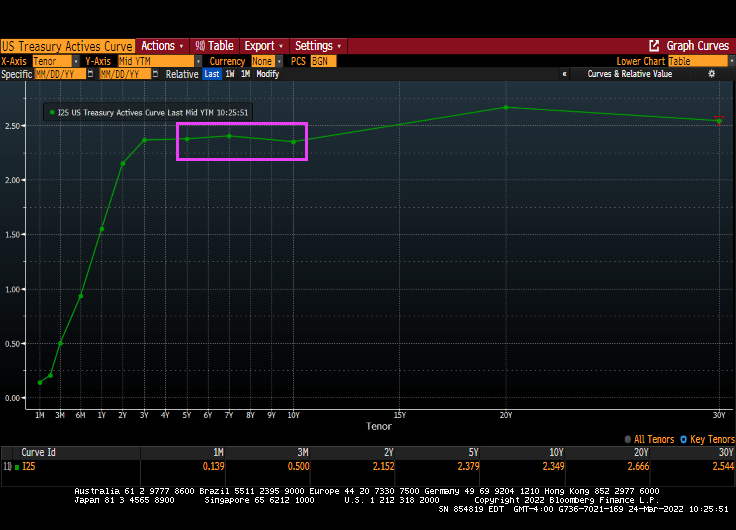

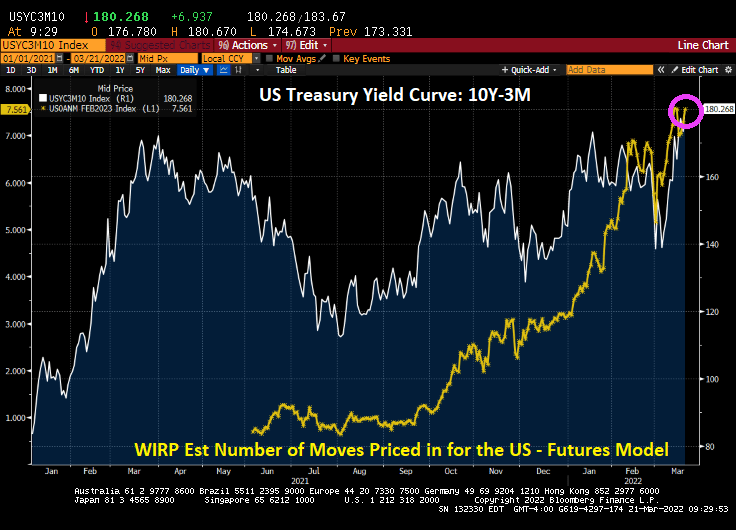

Oil prices are soaring as US President Biden pleads like a homeless person to foreign countries for oil rather than let the US produce more oil to drive down prices. Meanwhile, the US Treasury yield curve 10Y-3M is at its steepest (rising 10Y yields while The Fed keeps short rates at near zero).

But if we look at the belly of the beast, so to speak, the 10Y-5Y slope, we can see that the Treasury curve has declined to a mere 0.278 basis points as inflation rages.

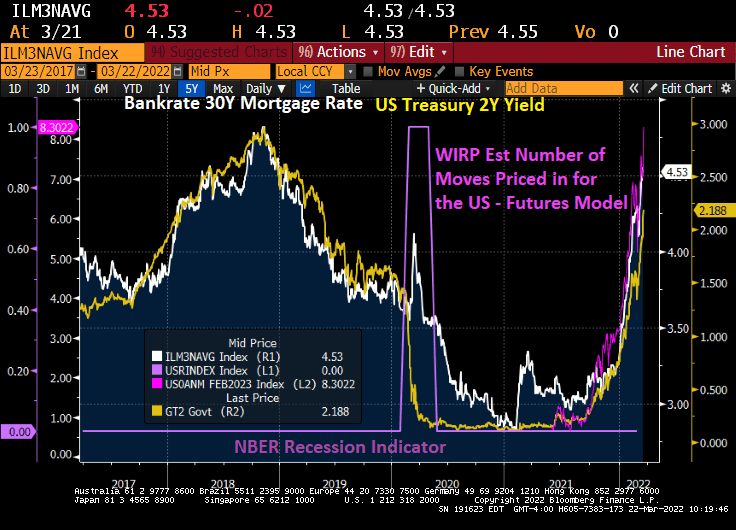

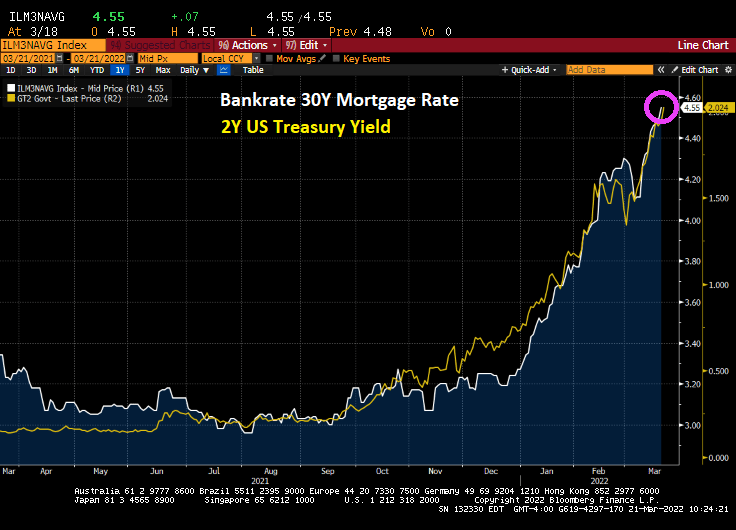

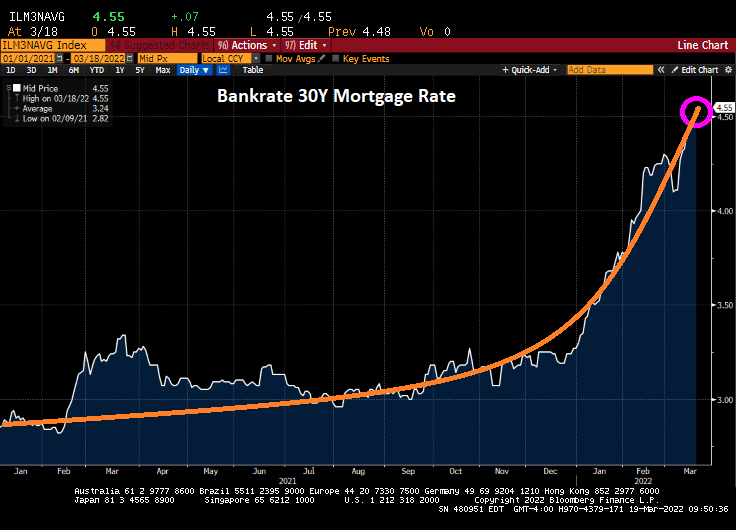

Bankrate’s 30-year mortgage rate keeps on climbing and has hit 4.55% as the 2-year Treasury yield rises rapidly.

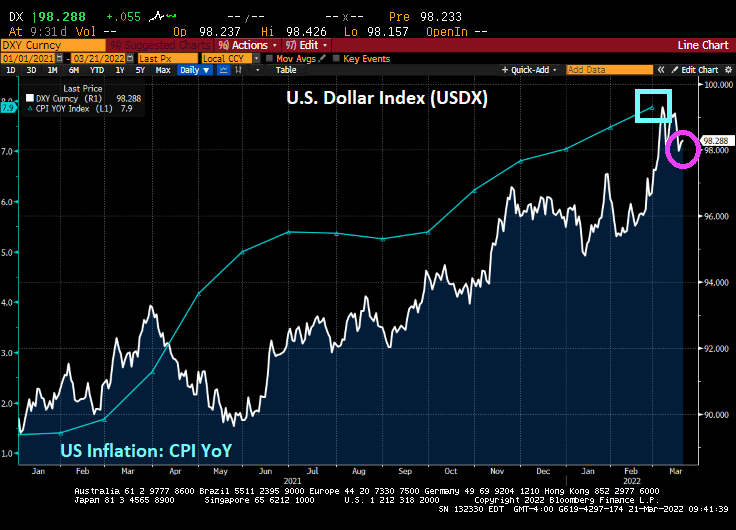

The US Dollar Index has risen dramatically as US inflation has increased dramatically.

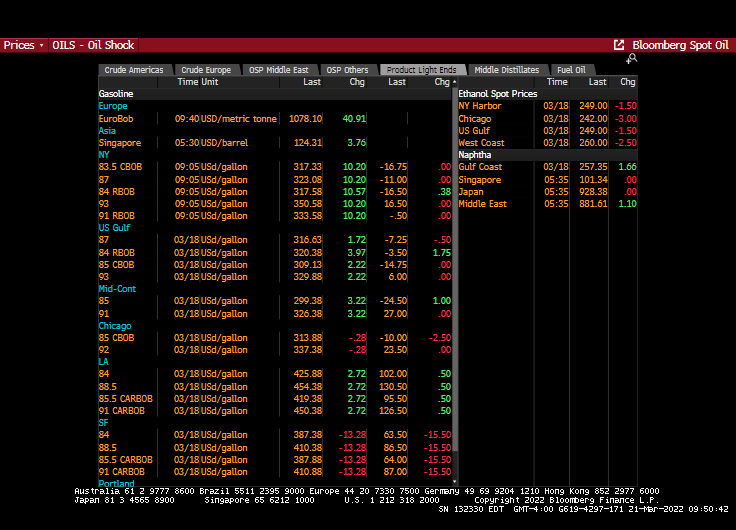

Oil? Oil is up over 4% in the US. Mexican Mix (not a #3 meal at Chuy’s) is up 7.32%.

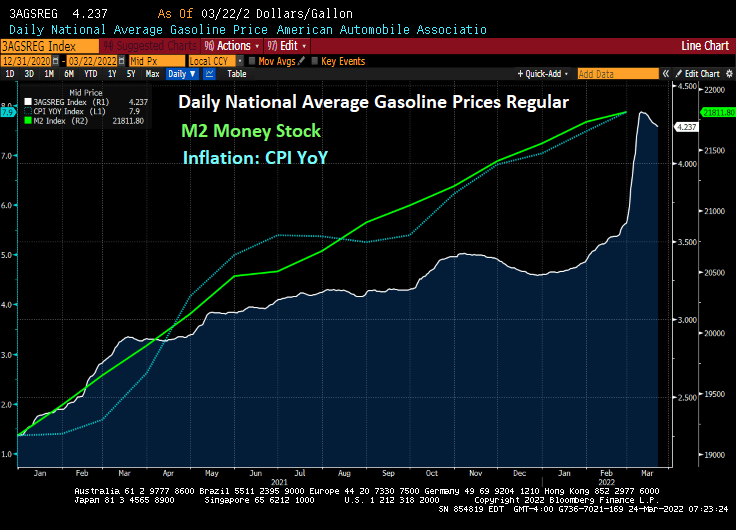

Gasoline? NY prices are up over 10%.

Russian oil is up 9.35%.

Ah, for the good old days of 30 cents a gallon gasoline, although I always wondered about Gulf’s marketing campaign. “Good Gulf” seems to imply that the other Gulf gasolines aren’t good. And Gulf’s “No-nox” seems to imply that the other Gulf gasolines knock like Biden’s knees as he pleads for foreign oil.

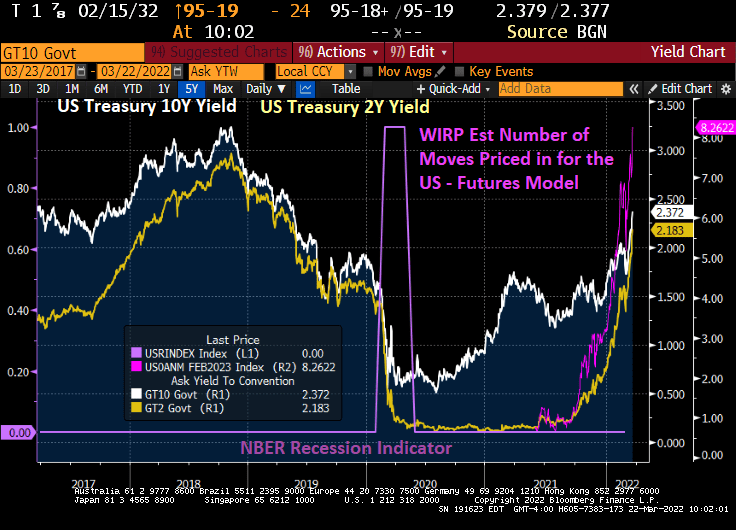

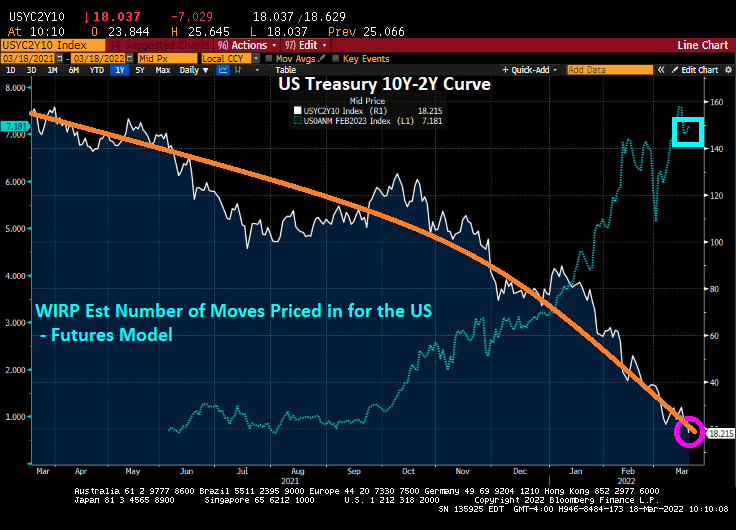

The US Treasury yield curve (10Y-2Y) is rapidly approaching inversion at 20.5 bps (where the 10-year yield is lower than the 2-year yield). But the 10Y-3M curve is generally steepening at 173.33 bps.

Of course, the driving force behind the flattening of the 10Y-2Y curve is the rapidly rising 2-year Treasury yield (orange line). The last time the 10Y-2Y curve inverted was in 2019, prior to the COVID outbreak in early 2020.

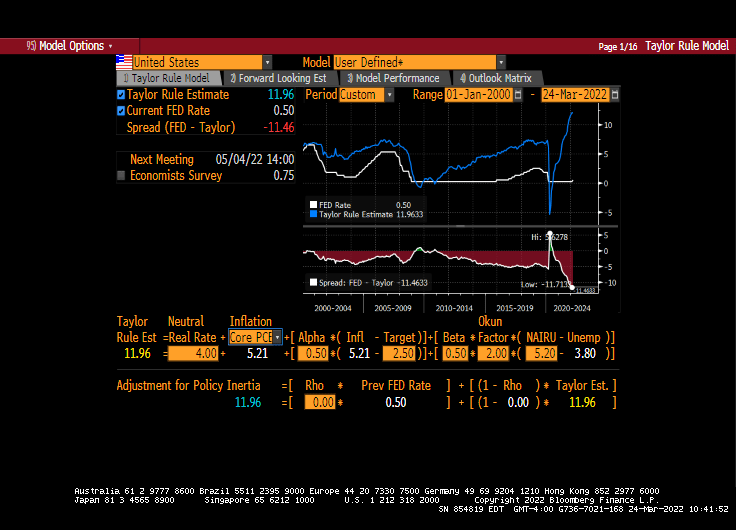

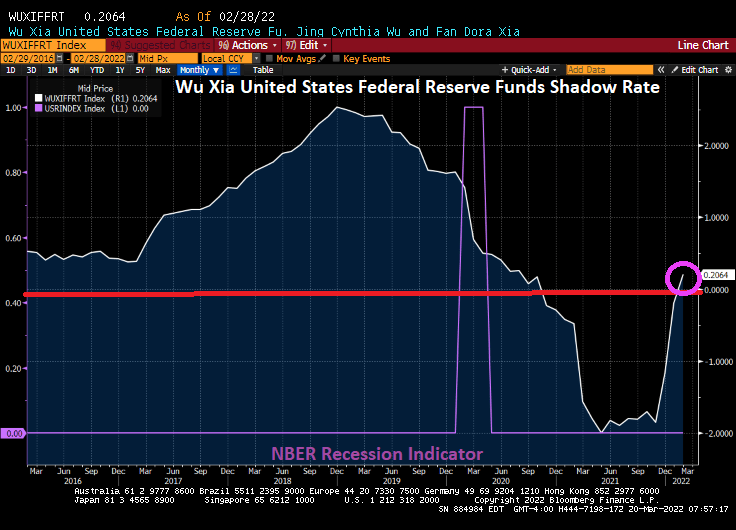

The Wu Xia United States Federal Reserve Funds Shadow Rate has finally climbed back into positive territory.

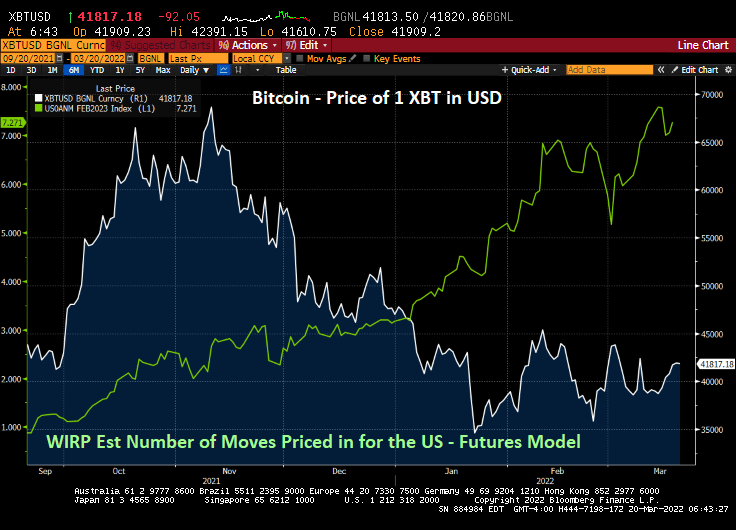

At last look, The Federal Reserve is forecast to raise their target rate 7 times over the coming year. And with the increasing forecast of rate hikes, we are seeing the cryptocurrency Bitcoin fall from near $70,000 to $41,817.

President Biden announced that he will be issuing an executive order to combat rising energy prices (the rising energy prices that he caused in the first place with … executive orders). Let’s see what happens next.

The news just keeps getting worse and worse. Russia is still assaulting Ukraine, WTI Crude prices are above $100 a barrel and climbing, the Cleveland Browns signed Deshaun Watson to replace Baker Mayfield at quarterback, etc.

But back to energy prices. Since Biden was sworn-in as President, WTI Crude Oil futures are up 125%, regular gasoline prices are up 89%, and diesel fuel prices are up 155%. Diesel is important since America uses diesel-powered trucks to transport goods to market.

Globally? The world inflation rate has grown from 2% in January 2021 to 6.82%. Global food prices are up 24%.

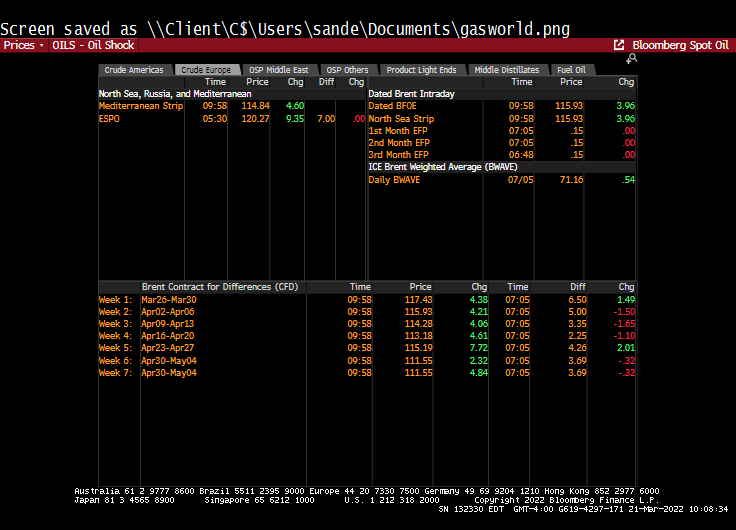

Yes, WTI Crude and Brent Crude are above $100 per barrel.

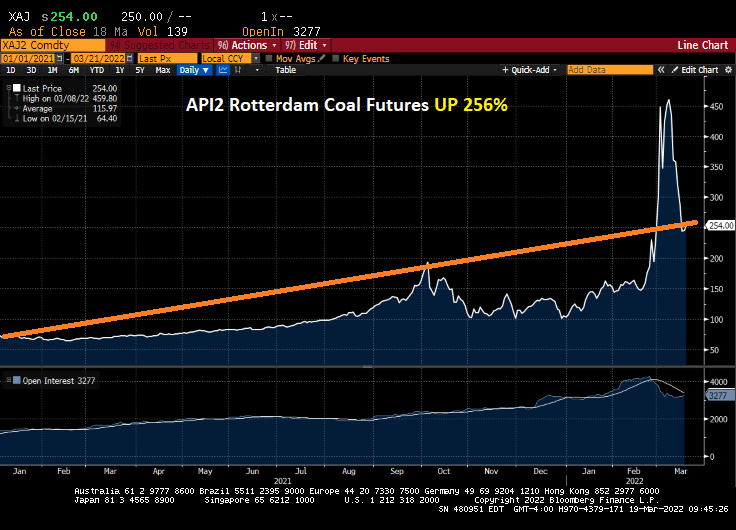

And coal prices are up 256% under Shoeless Brainless Joe.

Mortgage rates? Bankrate’s 30-year mortgage rate is now above 4.50%.

Let’s see if Dr. StrangeFedpolicy raises rates as aggressively as signaled.

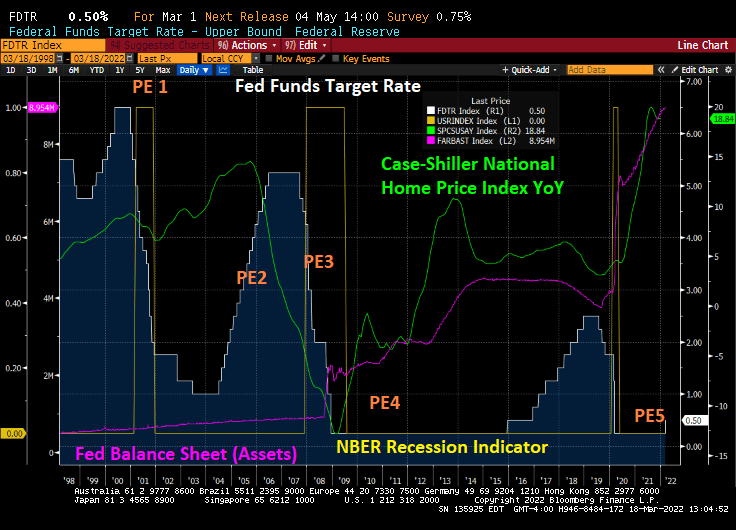

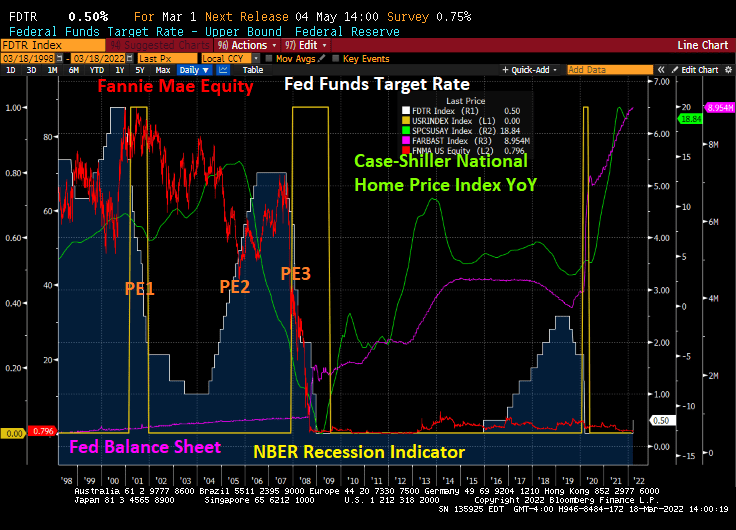

The Federal Reserve is not mentioned in the movies “The Big Short” or “Margin Call”, but The Fed’s policy errors played a big role in the demise of Fannie Mae’s and Freddie Mac’s equity prices.

Here is a chart of The Fed’s many policies errors. Let’s start with The Fed lowering rates too fast around the 2001 recession. They pushed their target rate from 6.5% in December 2000 down to 1.75% after one year and then down to 1% (PE1). As home price growth accelerated, The Fed engaged in their second policy error — raising rates too fast resulting in a dramatic cooling of home price growth. Then came Policy Error 3: the dropping of The Fed Funds Target rate from 5.25% in September 2007 to an eventual 0.25% in December 2008.

With the election of President Obama, The Fed engaged in Policy Error 4: keeping The Fed Funds Target rate too low for too long, combined with their massive asset purchase programs (QE).

Finally, The Fed (under Yellen) finally raised The Fed’s target rate ONCE under Obama, but started raising rates once Trump was elected. The Fed also slowed their QE under Trump which as called “Fed policy NORMALIZATION.” Then COVID struck and The Fed engaged in Policy Error 5: keeping rates too low for too long … again while massively expanding their balance sheet.

Fannie Mae and Freddie Mac, the DC mortgage giants were done in by The Fed’s whipsaw Policy Error machine.

Now we are embarking on PE 5: Powell and The Fed Gang not raising rates but signalling that they will. Like the play “Waiting for Godot.”

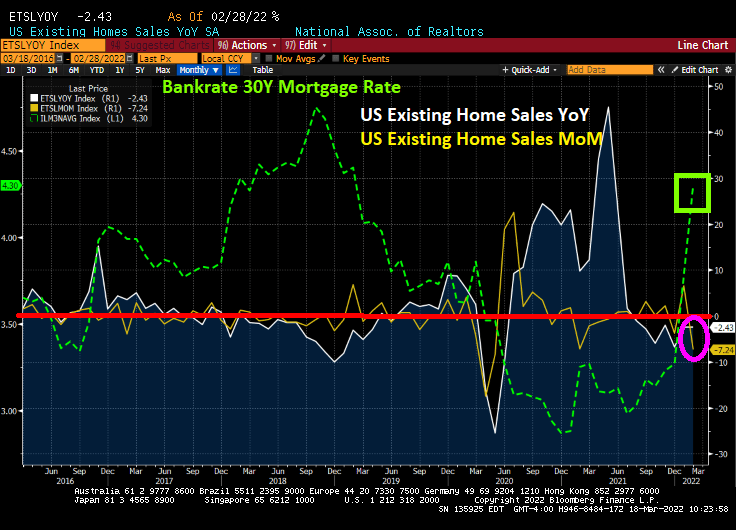

US existing home sales fell -7.24% from January as mortgage rates soar. On a YoY basis, existing home sales declined by -2.43%.

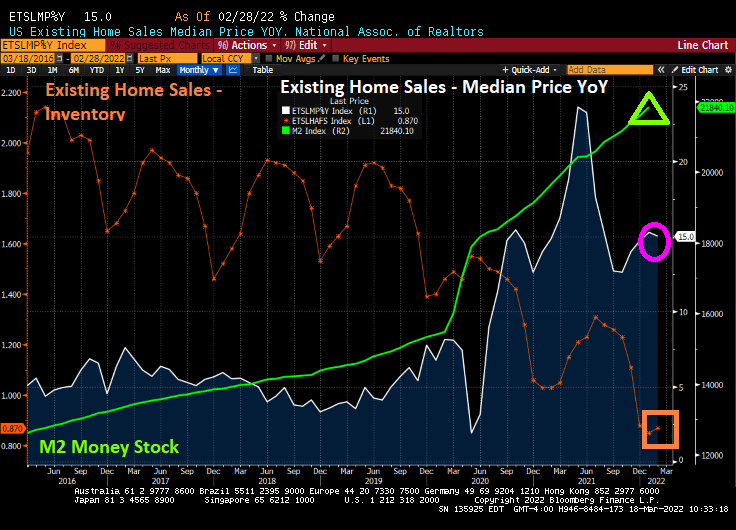

The median price of existing home sales “slowed” to 15% YoY in February as inventory picked-up slightly. And yes, Fed Stimulypto is still around and hasn’t helped increase inventory for sale.

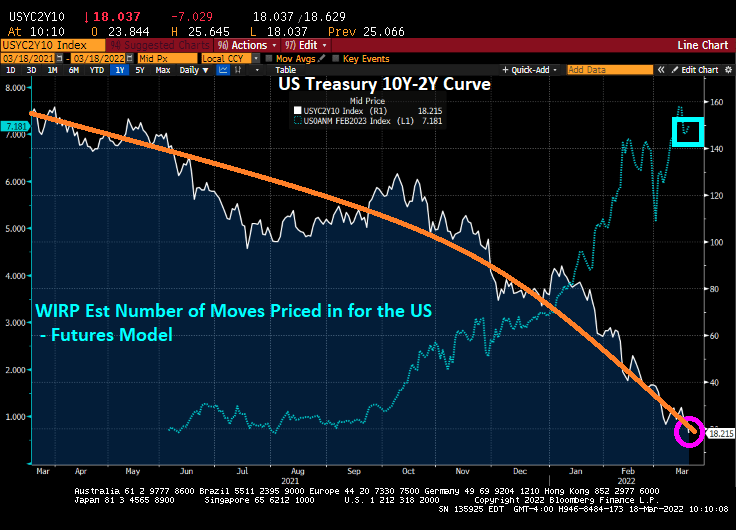

As I said earlier, we are seeing the Treasury yield curve plunging towards recession.

“The data is basically screaming at us to go 50 but the geopolitical events were telling you to go forward with caution. So those two factors combined pushed me” to support the 25 basis points increase, he said. “Going forward that will be an issue whether to think about going 50 in the next couple of meetings or not. But the data certainly seem to suggest that we move in that direction.”

WIRP is pricing in over 7 rate increases by February 2023 as the Treasury yield curve (10Y-2Y)

You must be logged in to post a comment.