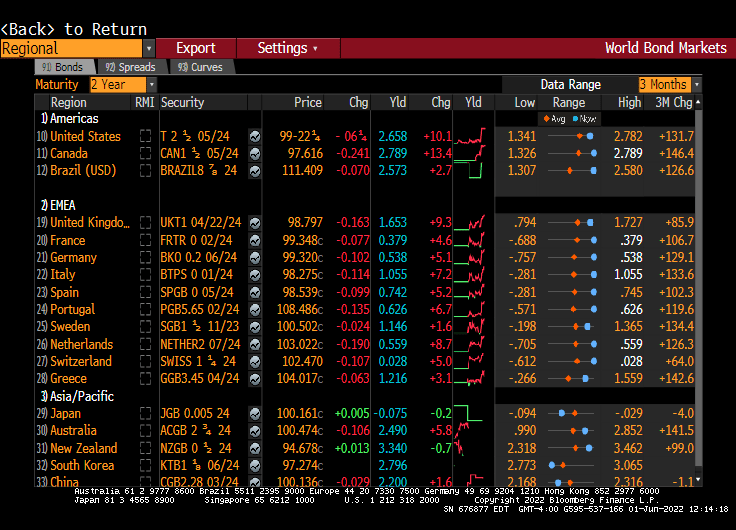

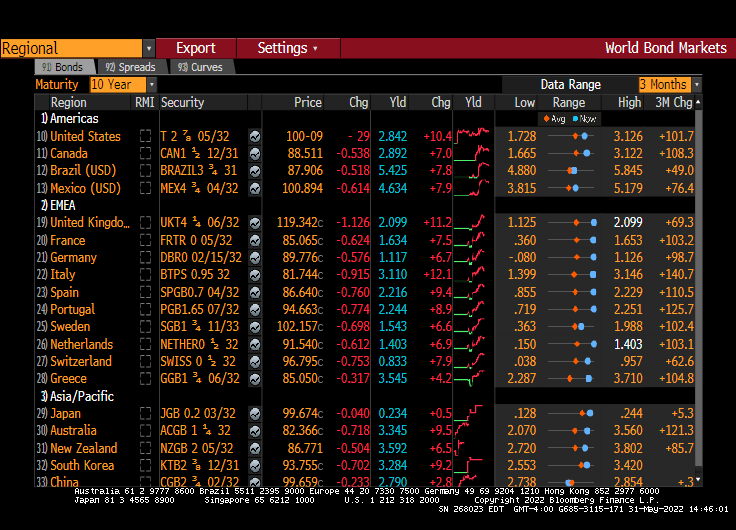

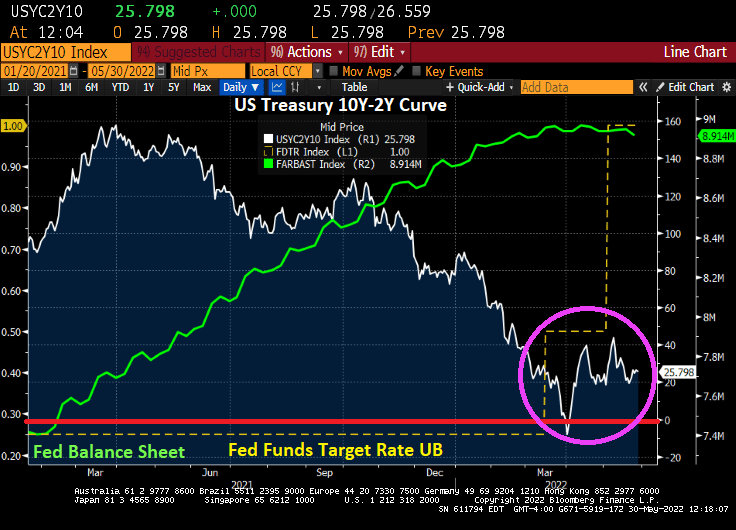

Another 10 basis point jumps in Treasury yields, this time at the 2-year Treasury Note.

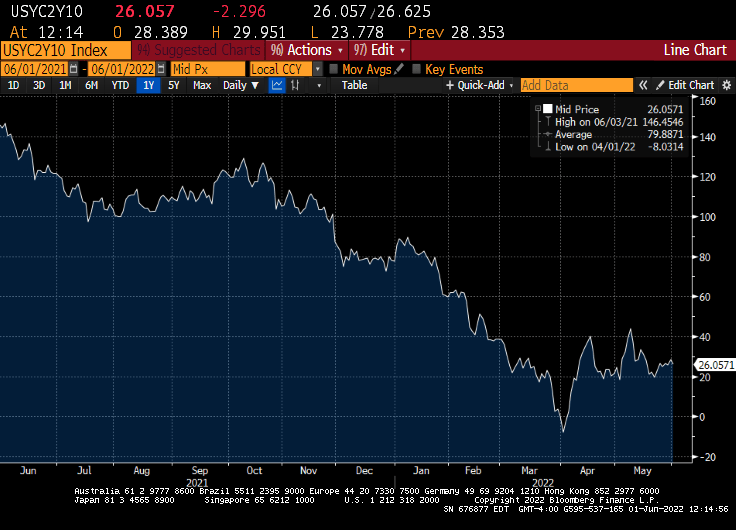

The 10Y-2Y Treasury slope just flattened to +26 BPS.

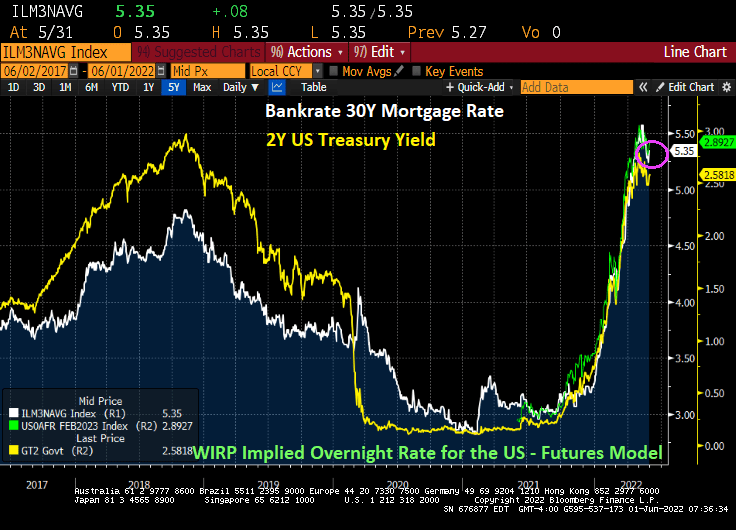

Another step in rising mortgage rates!

Confounded Interest – Anthony B. Sanders

Financial Markets And Real Estate

Another 10 basis point jumps in Treasury yields, this time at the 2-year Treasury Note.

The 10Y-2Y Treasury slope just flattened to +26 BPS.

Another step in rising mortgage rates!

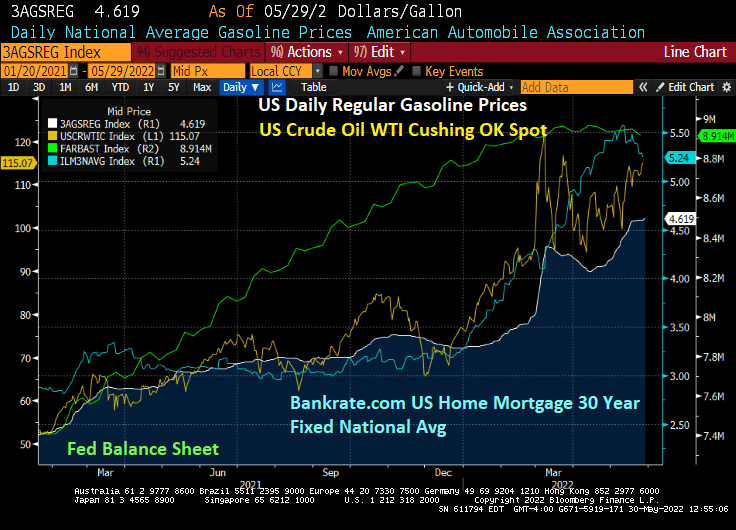

US gasoline prices just rose to an all-time high. Yes, even higher than the Dubya-era gasoline price surge of 2008.

Rising gasoline and diesel prices are helping drive up food prices to the highest level in history.

The proxy war the US is fighting in with Russia in Ukraine is helping drive up food prices. But at the core is Biden’s anti-fossil fuel drilling executive orders starting when Statist Joe (and The Fish) became President.

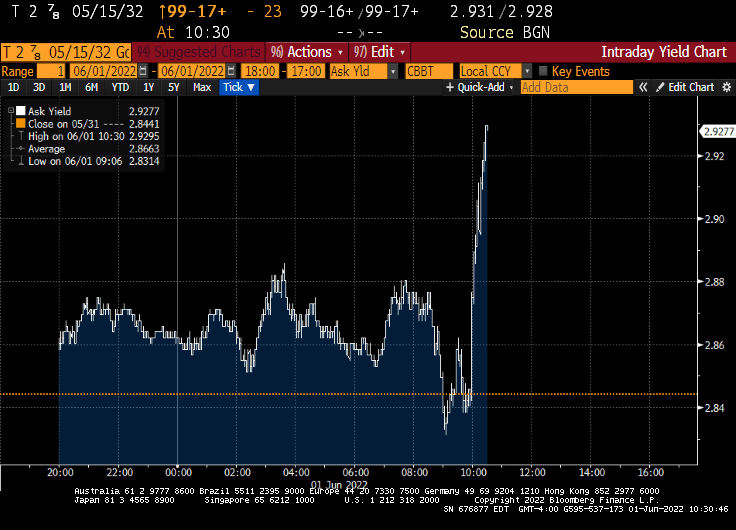

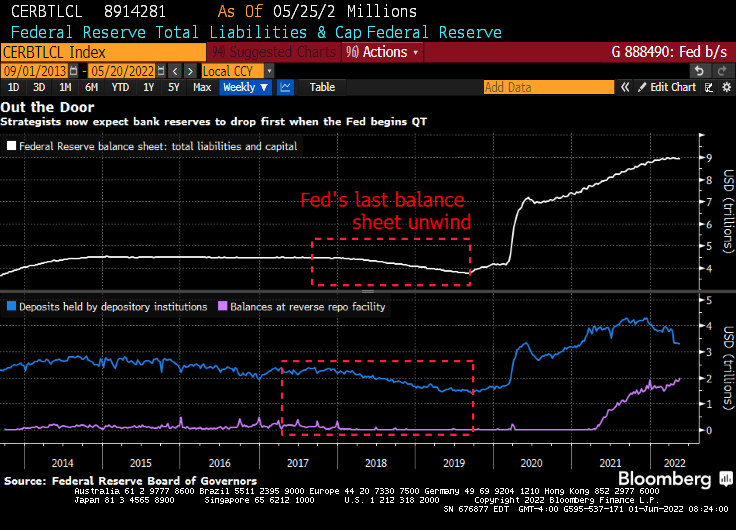

As The Fed begins unwinding their massive balance sheet, the 10-year US Treasury yield jumped 8.7 basis points.

Heartaches By The Number … for American households and mortgage lenders as The Federal Reserve begins FINALLY removing monetary stimulus.

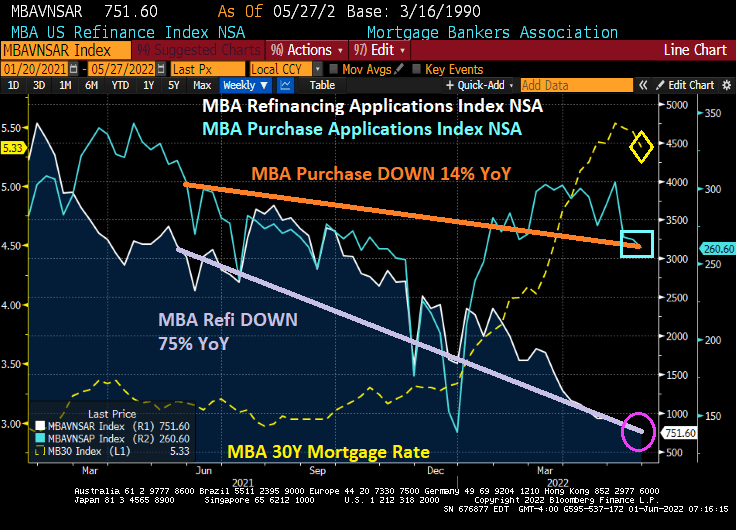

Mortgage applications decreased 2.3 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending May 27, 2022.

The Refinance Index decreased 5 percent from the previous week and was 75 percent lower than the same week one year ago.

The seasonally adjusted Purchase Index decreased 1 percent from one week earlier. The unadjusted Purchase Index decreased 2 percent compared with the previous week and was 14 percent lower than the same week one year ago.

Under Biden, mortgage refi applications are down -82.4%, purchase applications are down -7.5% and mortgage rates are up +80.7%.

Then we have this headline: “Fed Starts Experiment of Letting $8.9 Trillion Portfolio Shrink”

The Fed is capping monthly runoff at $47.5 billion — $30 billion for Treasuries and $17.5 billion for mortgage-backed securities — until September. Those thresholds will then double to a combined $95 billion. That compares to a peak of $50 billion a month when the Fed performed the exercise starting in 2017.

As expectation of Fed rate hikes increase, mortgage rates have soared like Tom Cruise’s Super Hornet aircraft from Top Gun: Maverick climbing over the steep mountain.

And mortgage rates are up a bit today.

Meanwhile, The Federal Reserve begins shrinking their balance sheet for the first time since Yellen and company started shrinking it under Trump.

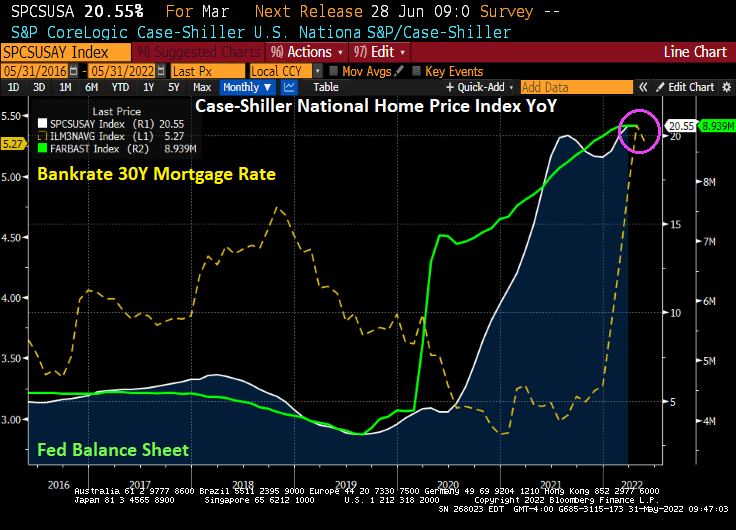

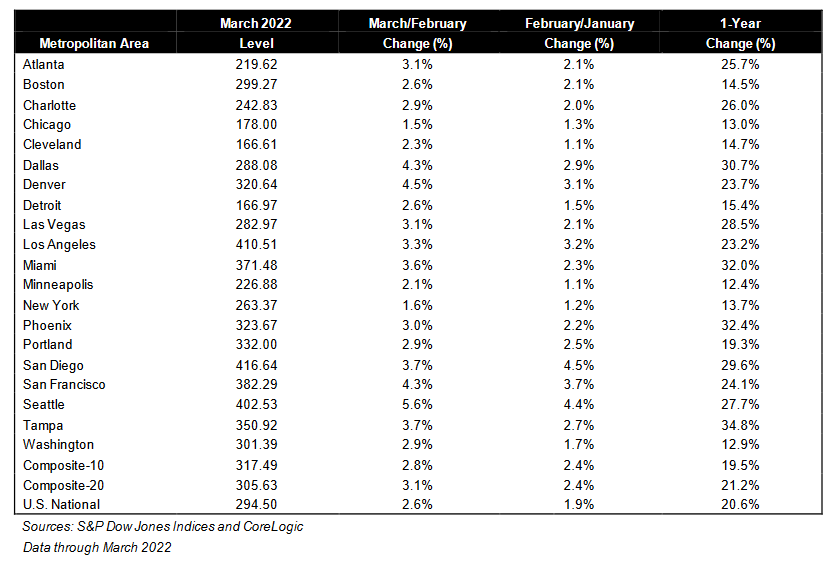

Earlier today, we saw that the Case-Shiller National home price index in March rose to its fastest rate in history.

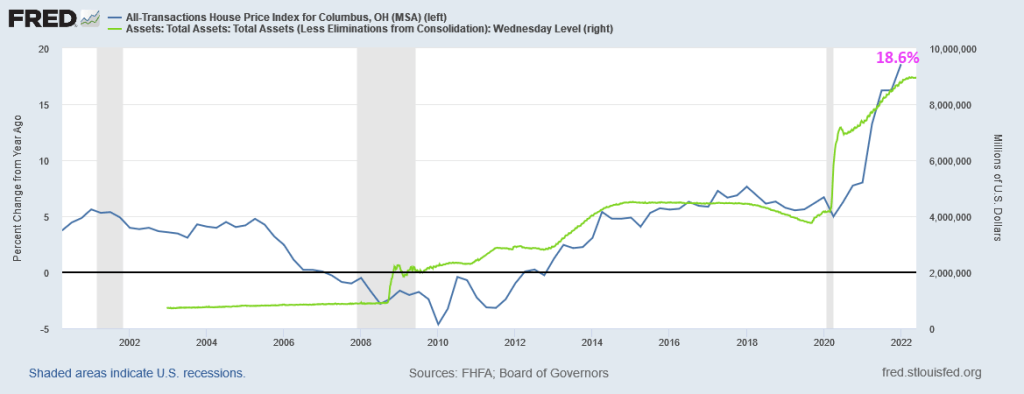

Columbus Ohio is not covered by Case-Shiller in their 20-city index, but the FHFA’s home price index does. And in Q1 2022, home prices grew at a 18.6% YoY clip.

Before Covid and the march of The Federal Reserve (and Biden’s anti-fossil fuel orders), home prices in Columbus Ohio were only growing at a 6.15% YoY rate. So, thanks to The Fed, home prices in Columbus are growing at nearly 3 times the pre-Covid rate.

Here is the CS national home price index.

Let’s see how Columbus home prices do with US Treasury yields starting to rise 10+ bps again.

Yes, its the housing market’s version of “March Madness!”

The Case-Shiller National Home Price Index for March was released this morning and it was a doozy. The Case-Shiller National home price index YoY accelerated to a whopping +20.55%.

And at +20.55%, it is the fastest price growth in history! Even the peak of the infamous 2000s housing bubble was only +14.51% in September 2005.

Why do we have historic highs in home price growth? The Federal Reserve’s monstrous Covid stimulus (green line) is still in place.

Washington DC is the slowest growing metro area in the US while Tampa FL, Phoenix AZ, Miami FL and Dallas TX are all above 30% YoY.

Let’s see what happens when The Fed FINALLY removes its Covid stimulus as mortgage rates rise.

Remember, Janet Yellen (who left monetary stimulus in place for too long under Obama) is now US Treasury Secretary.

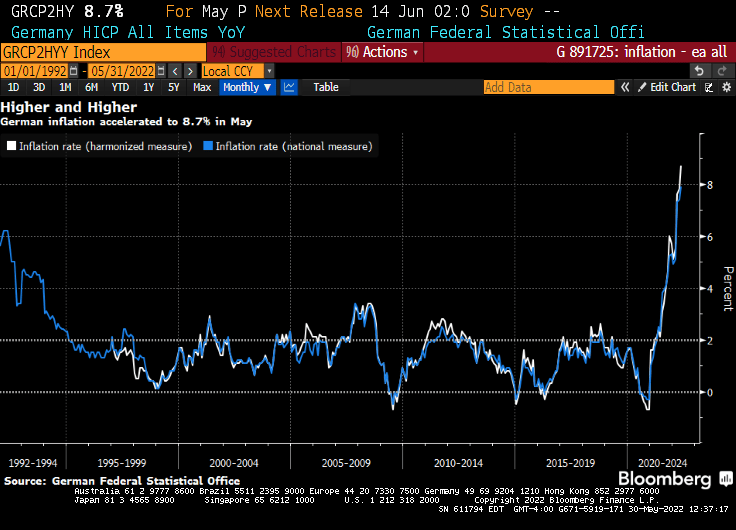

German inflation hit another post-World-War-II record high, piling pressure on The ECB’s need to exit from crisis-era stimulus after numbers from Spain also printed hotter than expected.

Driven by soaring energy and food costs, this morning’s data showed consumer prices in Europe’s largest economy surged 8.7% YoY – far hotter than the +8.1% expected (the highest since the start of the monthly statistics in 1963).

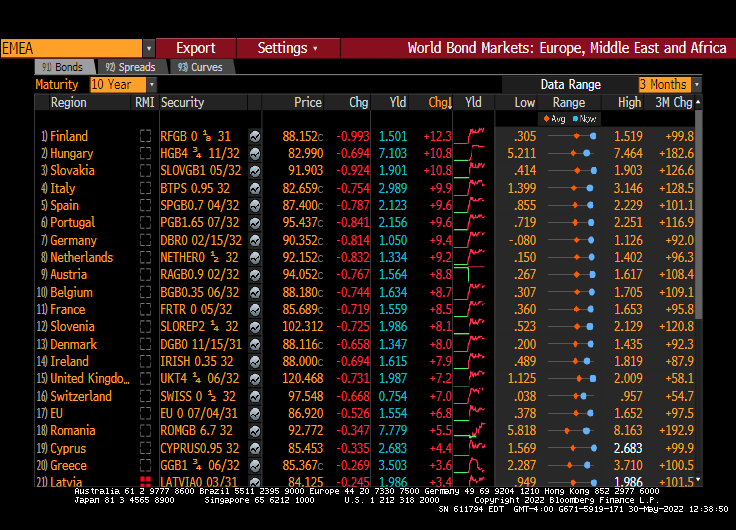

And top of that, the German 10-year Bund rate rose +9.4 BPS this morning, although Finland, Hungary and Slovakia all rose above +10 BPS.

While US markets are closed today in honor of Memorial Day, the US Treasury curve (10Y-2Y) has stabilized at 25.8 basis points after the initial shock of The Fed finally raising rates for the first time under Biden.

Then there is this headline: Biden to Meet Powell to Discuss Economy Amid Inflation Pain. So much for Fed independence. I wonder if Powell will say “Joe, have you ever considered canceling your executive orders on oil and natural gas exploration?”

Or perhaps Powell can bring Randy Newman to The White House to sing “Mr. President, have pity of the working man.”

OR maybe Biden can tell Powell to pause monetary tightening to avoid mortgage rates from rising to disastrous levels.

Memorial Day weekend is one where families often travel to meet relatives and friends, or travel to Washington DC to remember those who have died in the service of our country.

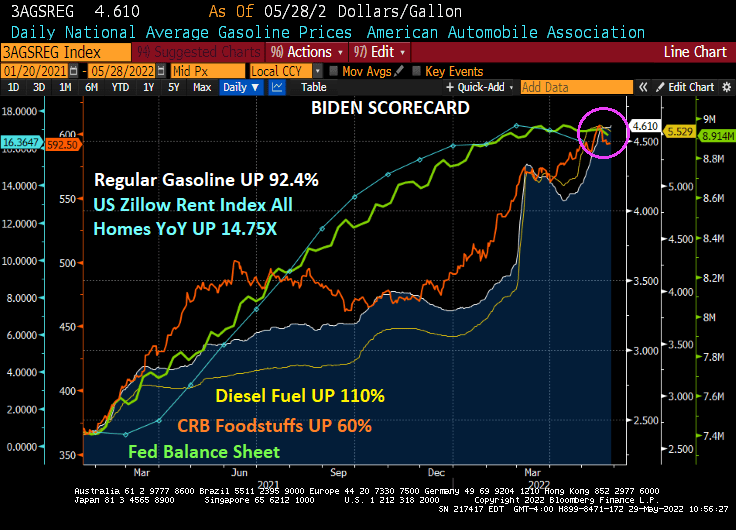

But traveling has gotten a lot more expensive under Biden. Gasoline prices are up 92.4% under Biden, while food prices are up 60%. Those hamburgers and hot dogs for grilling are being replaced by … pizza? Or maybe plant-based products.

Zillow’s Rent Index All Homes YoY was only 0.6234% in February 2021, and has soared to 16.36% YoY under Biden. That is an increase of 14.75x. So, not only is it much more expensive to travel on Memorial Day weekend, but it is far more expensive to stay home in your rental property.

On the currency front, we are seeing the US Dollar falling (greenback line), along with the Yuan/USD cross currency. West Texas Intermediate Crude Cushing OK spot is at $115.07.

At least Venezuela and Iran are benefiting greatly by Biden’s energy policies, even if Americans are suffering. Perhaps this is the new foreign policy of Wynken (US VP Harris), Blynken (US SecState), and Nod (Biden).

Remembering my Uncle Jack Sanders who served in the Battle of The Bulge during World War II, winning an individual Silver Star for bravery and two Purple Hearts. He rose from “buck” private to First Sergeant by the end of WWII.

Yikes! One of the unmentioned costs of Fed monetary tightening is the one to US taxpayers.

Fed carrying $330B in unrealized losses on its assets according to Q1 financial statement. Which US tax payers are on the hook.

Adjusting for the appreciation in its assets the Fed had seen through the end of last year, the unrealized losses were an even larger $458 billion.

This makes the Ukrainian relief bill of $30 billion look like chump change. Although it is about the same amount as Biden’s student loan forgiveness plan which would about to $321 billion.

Nobody spends other peoples’ money like politicians and now The Federal Reserve. Who are also DC-based politicians.

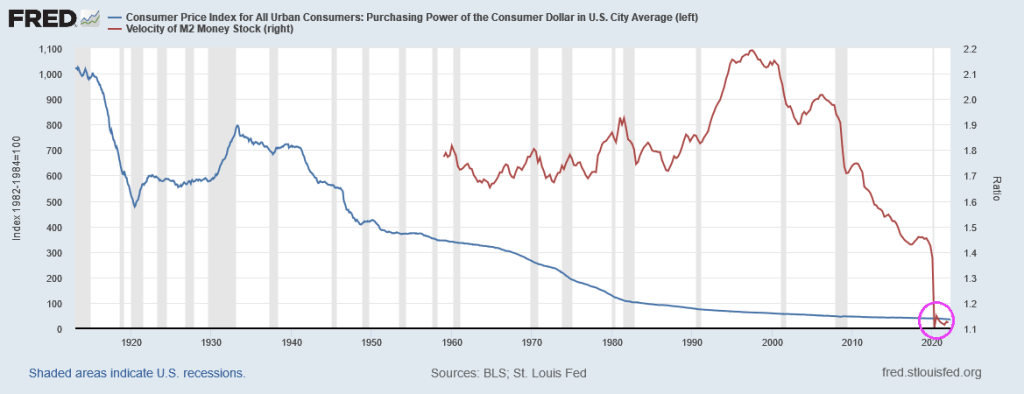

And yes, the purchasing power of the US Dollar and M2 Money Velocity (GDP/M2) appear to be collapsing like a dying star.

The Federal Reserve has been signaling a tightening of its loose monetary policy (essentially loose since the housing bubble burst of 2008 and the ensuing financial crisis). It is still loose as The Fed hasn’t really trimmed its massive balance sheet yet and has just raised it target rate to 1%.

So, potential home owners have to pay 5.10% for a 30-year fixed-rate mortgage while the effective Fed Funds rate, the rate at which banks lend to each other, is a measly 0.83%. This puts consumers at a relative disadvantage to large Wall Street firms that are gobbling up houses at an accelerated rate.

RealtyTrac has a Attom-sourced table of investor purchases of housing from Q3 2021, before The Fed started helping to crank-up mortgage rates for consumers.

With the US housing market slowing (thanks to The Fed’s signaling of monetary tightening), the question now is how far will The Fed go in its “War on Inflation!”?

You can see a major cause of inflation in the US since 2000: Federal spending and Federal (public) debt. During The Great Recession of 2008-2009, we saw inflation (CPI YoY) collapse into negative territory as Federal spending and debt soared. But the mini-recession of 2020 caused by the Covid governments shutdowns led to TWO surges in Federal spending and debt: Covid relief followed by the infrastructure spending bill. Combined with Biden’s anti-fossil fuel executive orders and massive splash of Federal spending in to the economy, we have inflation soaring.

If surges in Federal spending (requiring surges in Federal debt) have gone away (except for $40 billion in Ukrainian relief and Biden’s possible student loan cancellation of $10,000 that will cost an estimated $321 billion … and help drive up college tuitions even further), we may be over the “twin gorgings” of the Covid spending spree. This alone may result is a decline in the inflation rate.

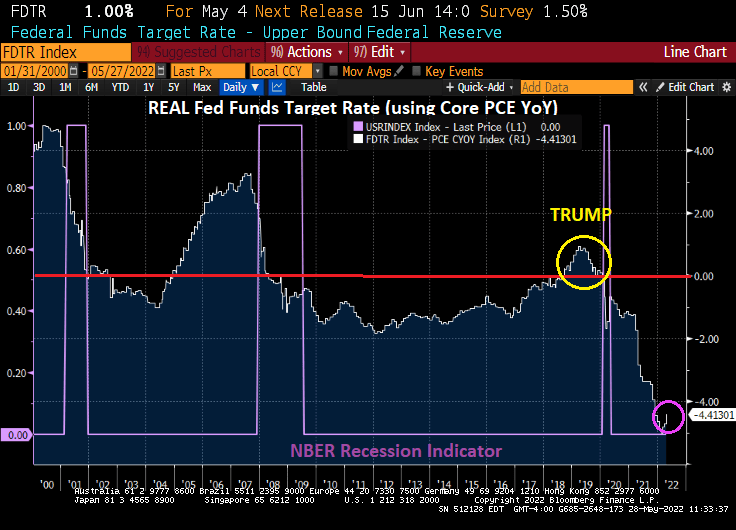

Where do we sit today with the REAL neutral rate? The REAL Fed Funds Target Rate (upper bound) is -4.41%. It was in positive territory during the Trump years. But then Covid struck.

So, we sit here today with Fed Monetary policy “loose as a goose.” And Wall Street investors “drunk as a skunk” on Fed Stimulus.

No wonder Wall Streeters like to go “Down To The Nightclub!” The Fed still has not taken the monetary stimulypto away, but have taken it away for consumers buying housing.

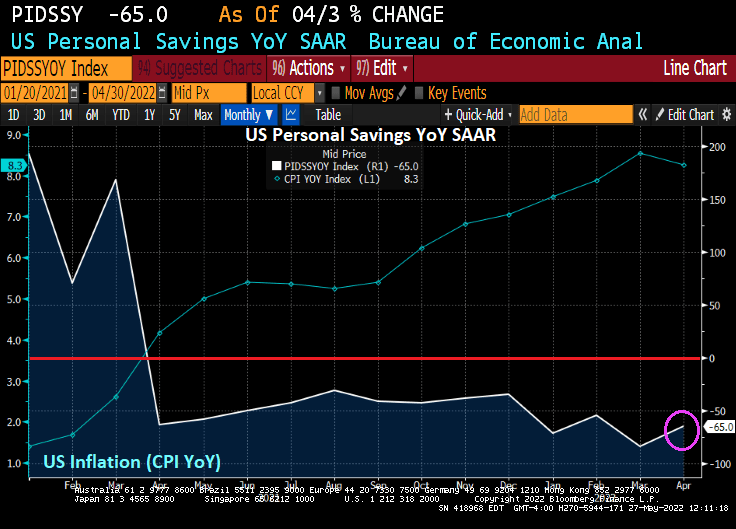

Americans’ Savings Rate Drops to Lowest Since 2008 as Inflation Bites.

Yes, inflation really bites. In fact, as US inflation is near the 40-year high, US personal savings declined -65% YoY as consumers try to cope with rising prices.

Its not only that personal savings is crashing in the face of inflation, revolving debt has soared as consumers try to cope with rising prices. I call this chart “The Biden Bowl.” Soaring consumer credit card debt with crashing personal savings.

You must be logged in to post a comment.