People Get Ready! There’s a train a coming. Its called The Federal Reserve.

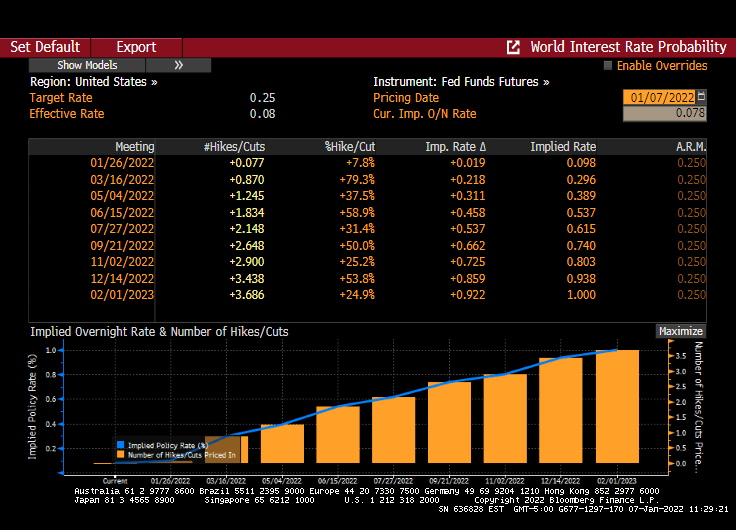

The market is pricing in 3 rate increases in 2022. And perhaps a faster than expected withdrawal of balance sheet stimulus.

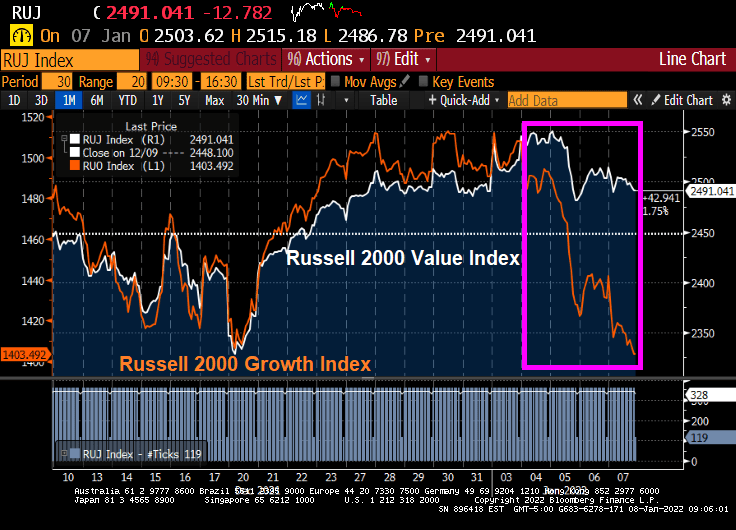

As a result, The Russell 2000 Growth index is plunging (orange line) relative to the Russell 2000 Value index (white line) which is down in 2021.

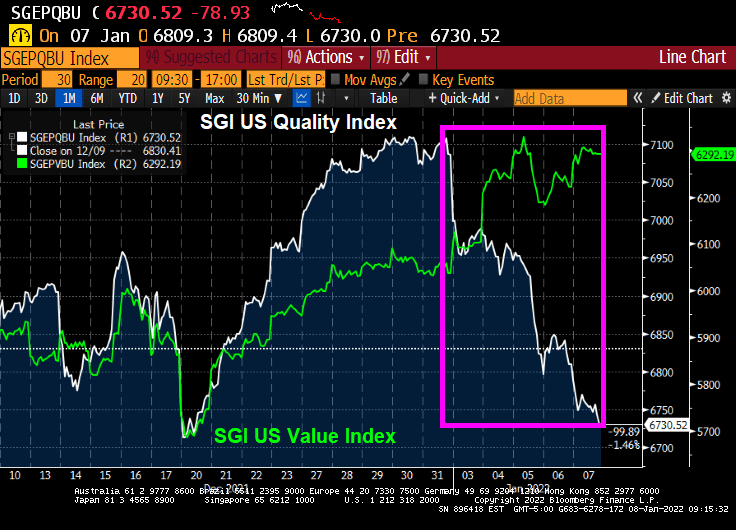

The Société Générale (SGI) US value and “quality” indices are telling the same story. The SGI US “Quality” index is falling like a paralyzed falcon while the SGI US Value index is up for 2022.

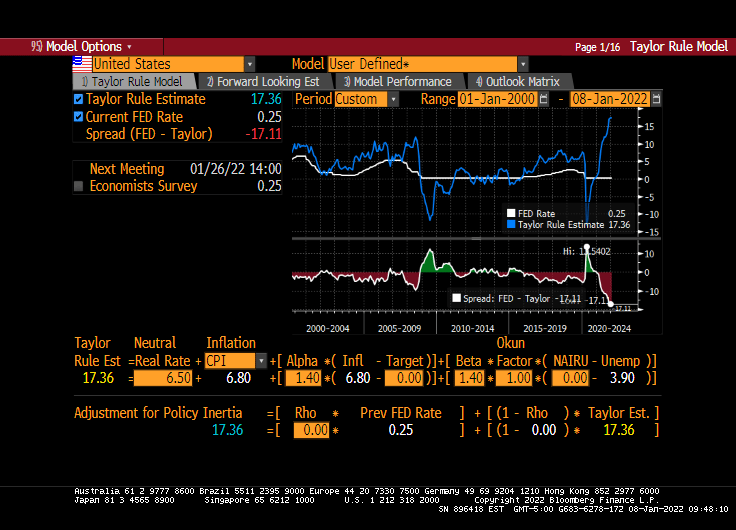

It is somewhat mystifying that markets would be soooooo sensitive to 3 rate increases from The Fed, particularly since the Taylor Rule suggests that The Fed’s target rate should be 17.36%. Even if you don’t like the Taylor Rule or disagree with its inputs, you must admit that the gap between where The Fed is (0.25%) and where they should be (17.36%) is … k-razy.

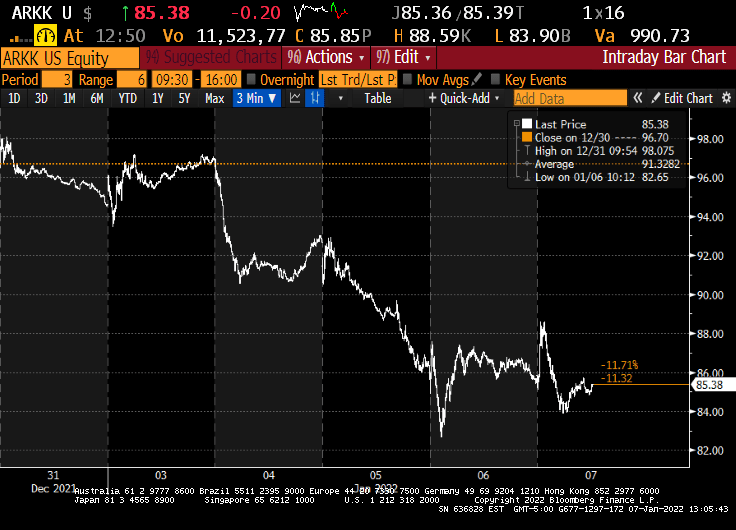

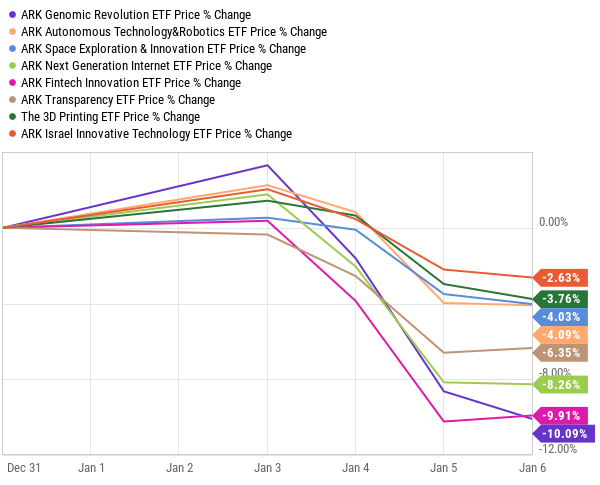

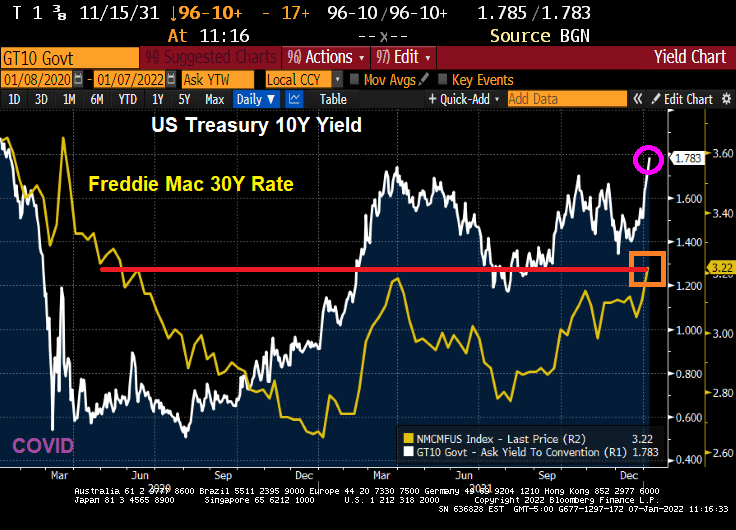

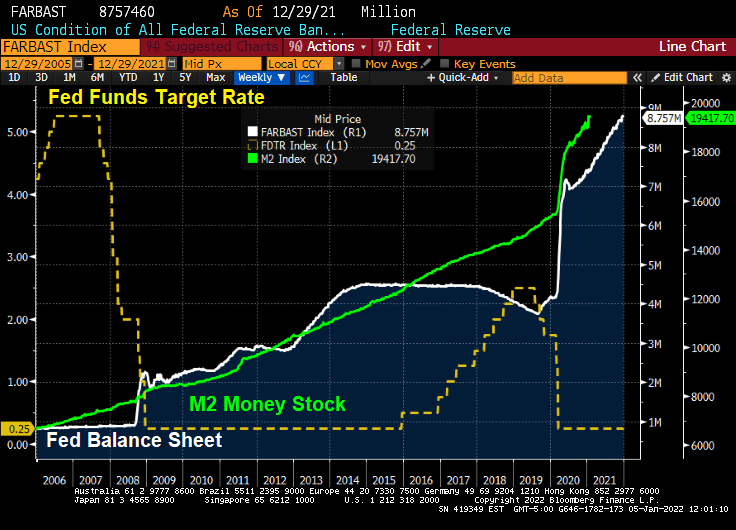

But here is where we sit.

You must be logged in to post a comment.