Face it. No one in Washington DC wants to close the border. Republicans supporting big agriculture support open borders and cheap labor, Democrats love open borders for political gains, despite open borders meaning a flood of migrants and depressing job prospects for native born Americans.

Case in point. Under the leadership of Biden (more like a followship because Biden clearly isn’t in charge of anything), the native born labor force (blue line) grew by 3.6%. However, the foreign born labor force (red line) grew by 14.6%.

The media focused on 1 million jobs lost for native-born and a gain of 697k jobs for foreign-born. But this claim is misleading. Look at the month to month changes in the labor force since 2020 (pink box). In several past months, we witnessed the same thing … native born job losses when foreign born gained jobs. But several months had the exact opposite. It is the overall trend that is alarming: native born jobs only grew 3.6% under Vacation Joe Biden while foreign born jobs grew 14.6%.

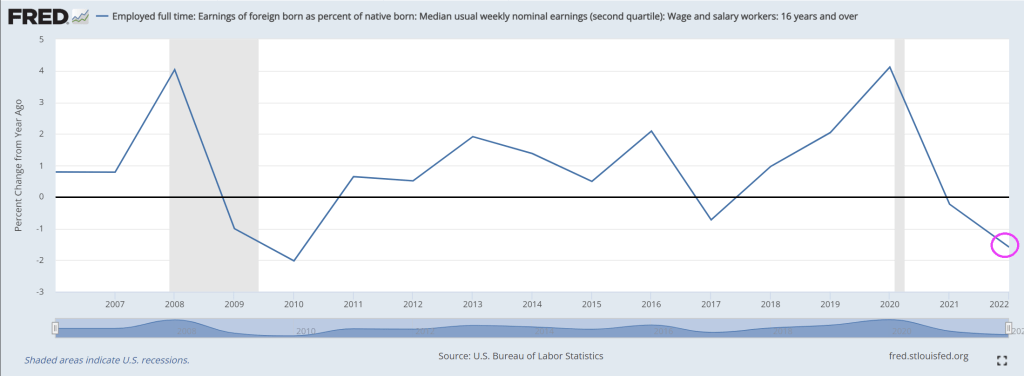

If we look at Employed full time: Earnings of foreign born as percent of native born: Median usual weekly nominal earnings (second quartile): Wage and salary workers: 16 years and over, we see that the YoY growth rate of earnings for foreign born declining. I attribute this to open borders and the influx of unskilled, largely uneducated immigrants pouring over the southern border.

Biden’s biographer claims that Biden is worried that he will be remembered as “Stupid.” Well, Biden IS stupid. But he is also the most corrupt President in history.

Simple Joe is what he will be remembered as.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.