So much for the defeatist mentality in the main stream media, Congress and economists!

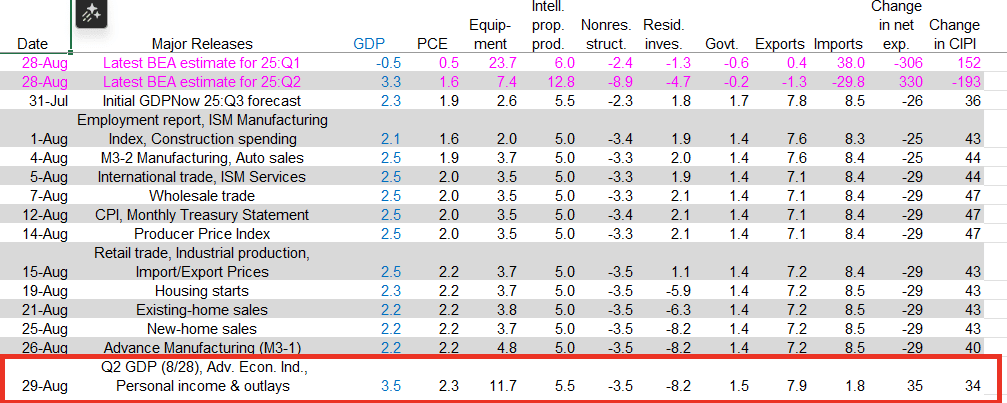

The GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the third quarter of 2025 is 3.5 percent on August 29, up from 2.2 percent on August 26. After recent releases from the US Census Bureau and the US Bureau of Economic Analysis, the nowcasts of third-quarter real personal consumption expenditures growth and second-quarter real gross private domestic investment growth increased from 2.2 percent and 4.4 percent, respectively, to 2.3 percent and 6.1 percent, while the nowcast of the contribution of net exports to third-quarter real GDP growth increased from -0.36 percentage points to 0.59 percentage points.

The breakdown? Equipment growth at 11.7 was the standout along with exports at 7.9%.

Residential investment is down -8.2. This isn’t helping!

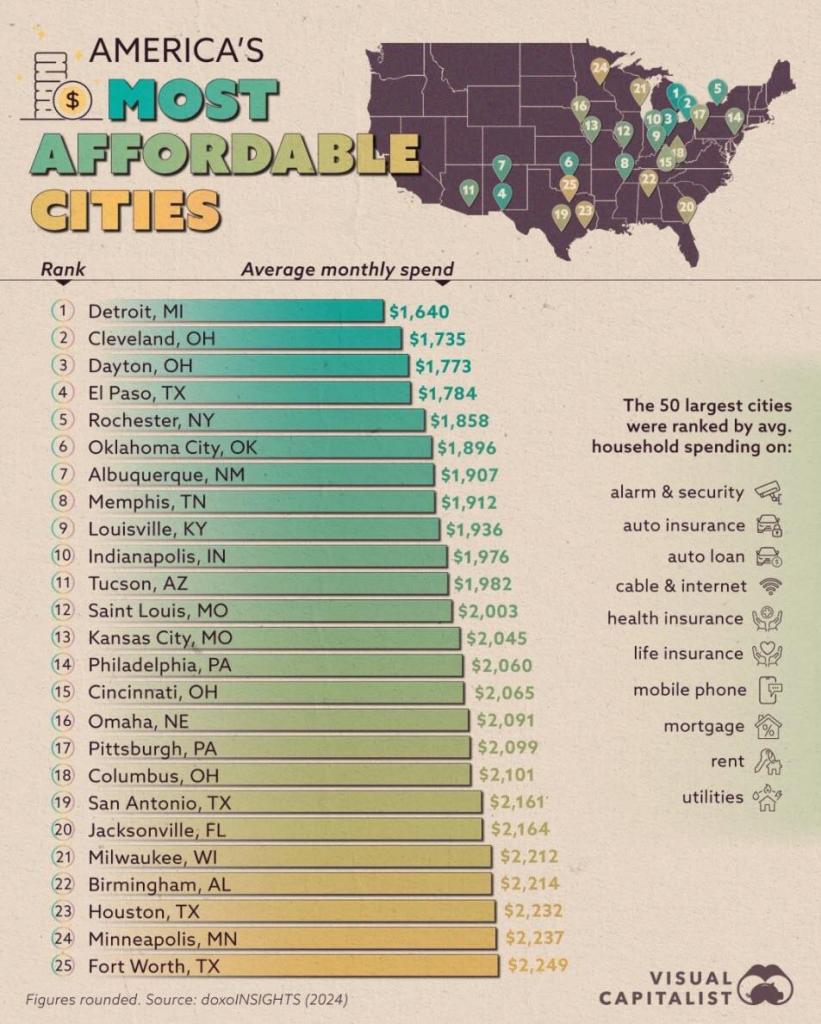

The Visual Capitalist calls most unaffordable cities as least affordable. San Jose California and New York City are the two most unaffordable cities in the USA. According to household spending.

Fortunately, I live in Columbus Ohio. the 18th most affordable city in the USA.

Much of the difference amongst cities is land use and construction restraints. And booming/dying local economies.

As a sad reminder about the last four years, Pete Buttigieg will leave his post as Transportation Secretary having spent $7.5 BILLION to build 8 EV charging stations.

October STICKY core inflation is still up 4% YoY (year-over-year)

Core CPI rose 0.3% MoM (as expected) which pushed it up 3.3% YoY (not even close to the 2% mandate)…

Source: Bloomberg

There has not been a single monthly decrease in core consumer prices since Biden too office.

dddd

Between The Fed’s insane monetary policy and Biden/Harris insane fiscal policies, we are living in a world where Ray Bradbury’s novel Fahrenheit 451 becomes a reality. Instead of books burning, it is the US Dollar burning.

I just watched Dennis Quaid in “Reagan”. Excellent film. But it reminded me of how Reagan sank the Soviet Union: by outspending the Soviet Union on the arms race. It worked! The Soviet Union, hamstrung by grossly inefficent central planning, couldn’t keep up and collapsed under President George H.W.Bush.

Fast forward to today. Starting with Barack Obama and Joe Biden in 2009, following the financial crisis in 2008. The Federal government ramped up Federal spending, and Federal debt. While The Federal Reserve, the hand maiden to the Federal government, ramped up M2 Money supply.

“You never want a serious crisis to go to waste. And what I mean by that is an opportunity to do things that you think you could not do before.” – Rahm Emmanuel

Then came Biden/Harris who drove Federal debt and spending to absurb level (orange box). Like the financial crisis, fans of big government and big government spending will utter the word “Covid.” But that is gross misleading. Covid was the excused for wild spending and debt issurance. And MORE Fed money printing. It’s almost as if Obama/Biden/Harris were replicating Reagan’s bankrupcy strategy in reverse! That is, collapsing the US from within.

As we are all painfully aware, the US Debt now stands at $36 TRILLION with $220.3 TRILLION in unfunded liabilities. Too bad total US Assets are only $217 TRILLON.

Do I believe that Obama/Biden/Harris want a “Great Reset”? Absolutley. Just look at our fiscally unsustable open borders and our politiicians blatanly lying to us. :Like Ohio’s Senator Sherrod Brown who brags about his helping write the border bill that would reverse Trump’s deportations and fund the speeding up of immigration.

Tennessee Ernie Ford sang it best. $36 tons of debt. Another day older and deeper in debt. Notice virually no political candidate will acknowledge or discuss.

The federal government spent $1.8 trillion more than it collected in tax revenue in fiscal year 2024, according to figures released Friday by U.S. Treasury Department.

Congress has run a deficit every year since 2001. In the past 50 years, the federal government has ended with a fiscal year-end budget surplus four times, most recently in 2001.

The deficit for fiscal 2024 was $1.8 trillion, or $138 billion higher than the prior year’s deficit. As a percentage of GDP, the deficit was 6.4%, an increase from 6.2% in fiscal 2023. The 2024 deficit is $196 billion lower than in 2023, excluding the effect of the Supreme Court’s 2023 decision in Biden v. Nebraska regarding student loan programs, according to year-end data from the September 2024 Monthly Treasury Statement of Receipts and Outlays of the United States Government.

And then we have the REAL disaster in the form of unfunded liabilities of $220 TRIILLION (or $651,000 per citizen). For a family of 5 citizens (like my household), that amounts to $3.26 MILLION per household of 5.

Imagine Kamala’s filibustering a response to a question about the national debt and unfunded liabilities. Other than “Donald Trump.”

I read “The Arms of Krupp” by William Manchester. A great book about the rise of ThyssenKrupp during World War II. It is one of the world’s largest steel producers, but it now has NEGATIVE ENTERPRISE VALUE.

The cause? Germany is up the creek without an economic paddle after years of gross mismanagement by Angela Merkel and her party. Mass immigration in Germany and a slowdown in the global economy aren’t helping.

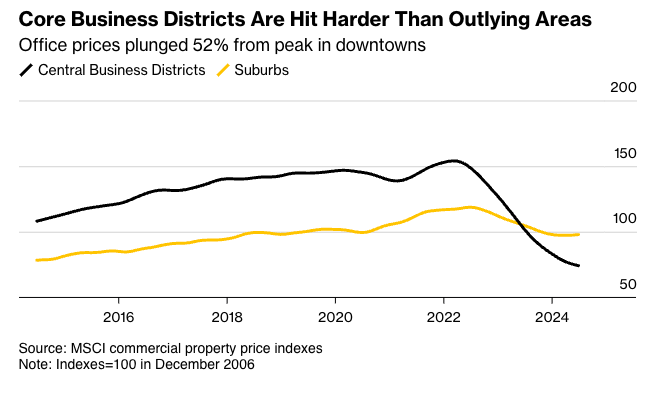

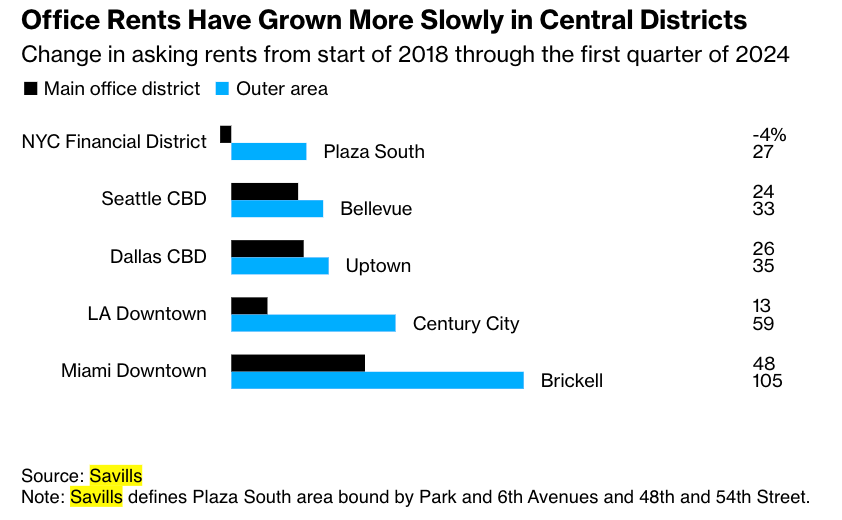

Commercial real estate market challenges are more severe for older office towers in downtown metro areas than those outside city centers. The mismatch between funding needs and available credit in a high-interest-rate environment has also intensified the strain on building owners, as elevated tower vacancy rates persist across many markets due to the ongoing trend of remote work becoming the norm.

Aging business districts from Los Angeles to Chicago to Boston of zombie towers with high vacancy rates that have no use in today’s economy.

Big landlords, including Brookfield, Blackstone, and Starwood Capital Group, have walked away from older downtown towers in recent quarters.

The latest data from MSCI shows office values in metro areas have crashed 52% from their highs. Some of the worst declines have occurred in San Francisco, Manhattan, Washington, and Boston.

Source: Bloomberg

Between 2019 and 2023, about $557 billion of value evaporated from US offices due to a multi-year slide in demand, with older towers quickly falling out of favor with companies, according to an estimate by economists at Columbia and New York universities. CBRE Group noted that only 2% of towers in the US are considered top-tier, with rents 84% higher than the rest of the market.

Data from brokerage Savills shows office rents in business districts have grown slower than rents for similar buildings outside metro areas.

Source: Bloomberg

The move to new towers highlights how, for decades, the bubbles in legacy downtown districts, fueling economies, have ended for now, and older towers will have to be torn down.

To be very frank. It’s a crisis. Democrats running the crime-ridden metro area are delusional and blinded by their woke religion as the city’s population recently crashed to a 100-year low, and violent crime remains a major issue.

We’ve had conversations with multiple folks at wealth management and investment banking firm Stifel Financial about the latest shift of operations outside the dying business district to a new tower in a much safer and newer district. At first, Stifel contemplated leaving the city for the suburbs because far-left Democrats in City Hall could not enforce law and order.

CRE foreclosures are on the rise.

Don’t forget about Soros-funded district attorneys not enforcing the law in large cities. Expect more of the same if Harris/Walz win the election.

The scary thing about the BLS overstating job gains by Biden/Harris by almost 1 million jobs is that US Commerce Secretary Gina “The Goofball” Raimondo didn’t even know about the Philly Fed report.

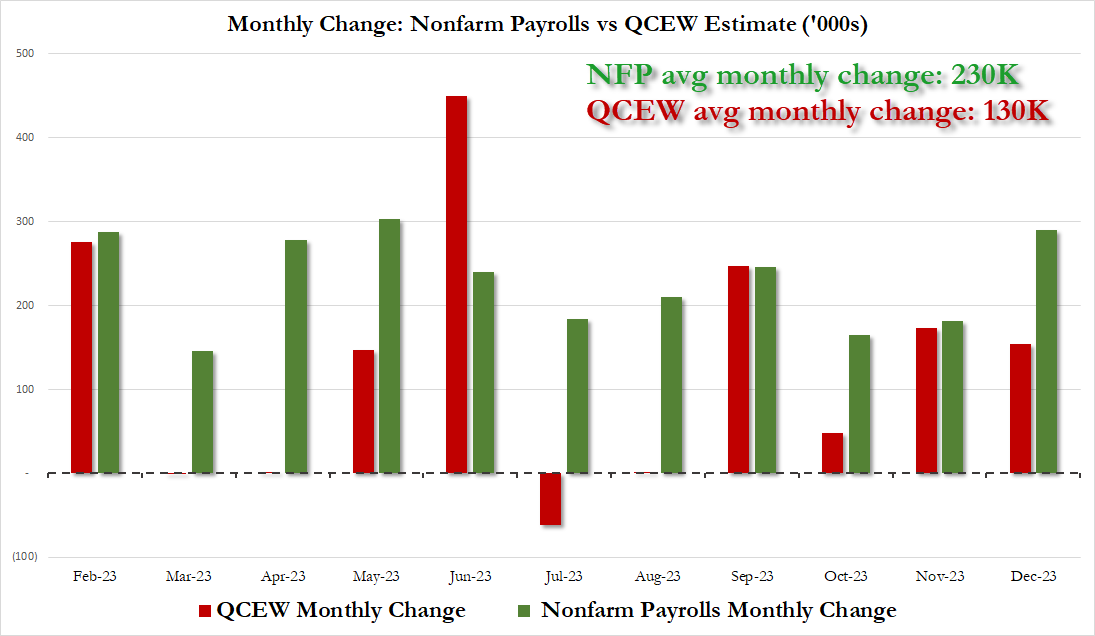

Back in March, when most of Wall Street and economists still believed the lies spewed forth by the Biden Bureau of Labor Statistics, which intentionally uses inaccurate, rushed “data” from the Establishment survey which is meant to pad sentiment and make the economy appear far stronger than it is for propaganda purposes (as one can see by the constant monthly downward revisions), we did an in-depth analysis looking at the actual, “uncooked” numbers published by the Philadelphia Fed preview of the annual Quarterly Census of Employment and Wages employment revision, and warned our readers that actual US payrolls are overstated by at least 800,000.

Specifically, we concluded that “the BLS had overstated payrolls by 800,000 through Dec 2023 (and more if one were to extend the data series into 2024)” and added that “it’s truly statistically remarkable how every time the data error is in favor of a stronger, if fake, economy.”

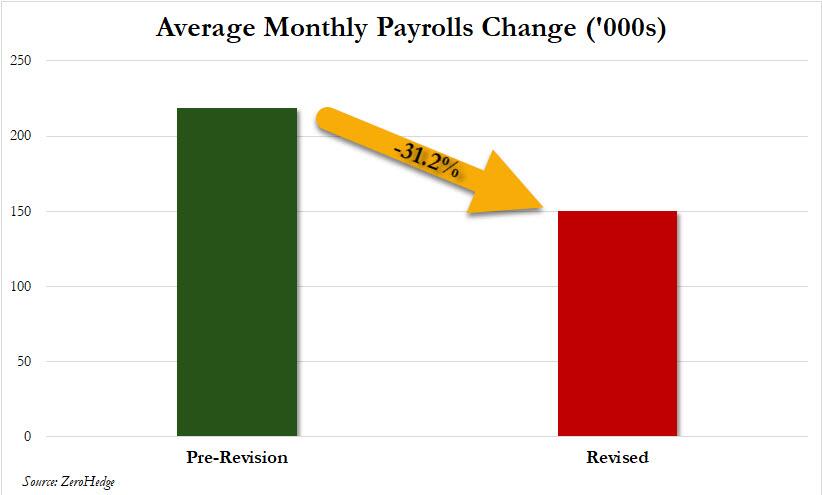

Furthermore, we also noted that the revision “also means that far from the stellar 230K average monthly increase in payrolls in 2023, which the White House would spin time and again as direct evidence of the benefits of Bidenomics, the true average monthly payroll increase in 2023 was only 130K! The full monthly change in payrolls as originally reported by the BLS (in green) and the actual monthly number, as per the QCEW (in red) is shown below.”

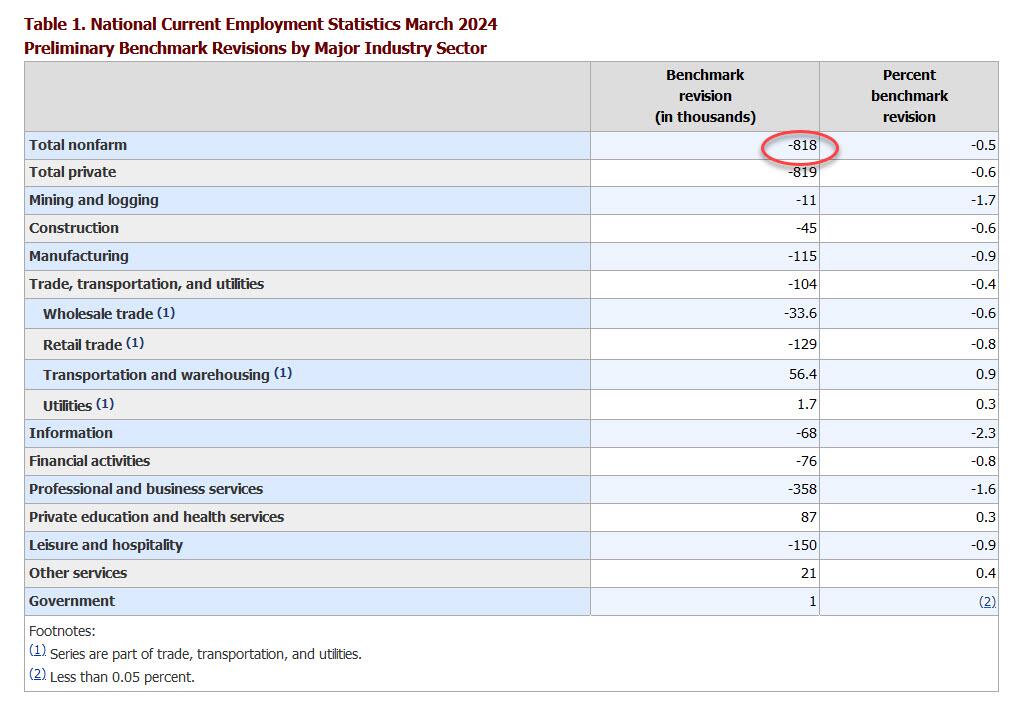

This matters because as we reminded our followers this weekend, today at 10am, the BLS would publish its annual nonfarm payrolls benchmark revision where it would unveil as , which it did (with the usual 35 minute delay because that’s the kind of service $35 trillion in debt buys you), and it confirmed that we were right almost to the dot, because as the BLS unveiled in its CES Preliminary Benchmark Announcement, “the preliminary estimate of the benchmark revision indicates an adjustment to March 2024 total nonfarm employment of -818,000 (-0.5 percent)” or just above the 800,000 was said to expect back in March.

The revision is mainly due to the highest-paying sectors: i.e., professional services -358k, leisure -150k, and manufacturing -115k. Not at all surprising: government was revised +1,000.

As an aside, while the data were scheduled to be released at 10 a.m. in Washington but didn’t appear on the BLS’s website for more than a half hour later. A spokesperson for the agency didn’t answer Bloomberg’s questions as to why the figures were delayed, but we have some pretty good guesses about the panic that gripped the BLS as they realized they needed a green lights from the propaganda ministry before going live with this number.

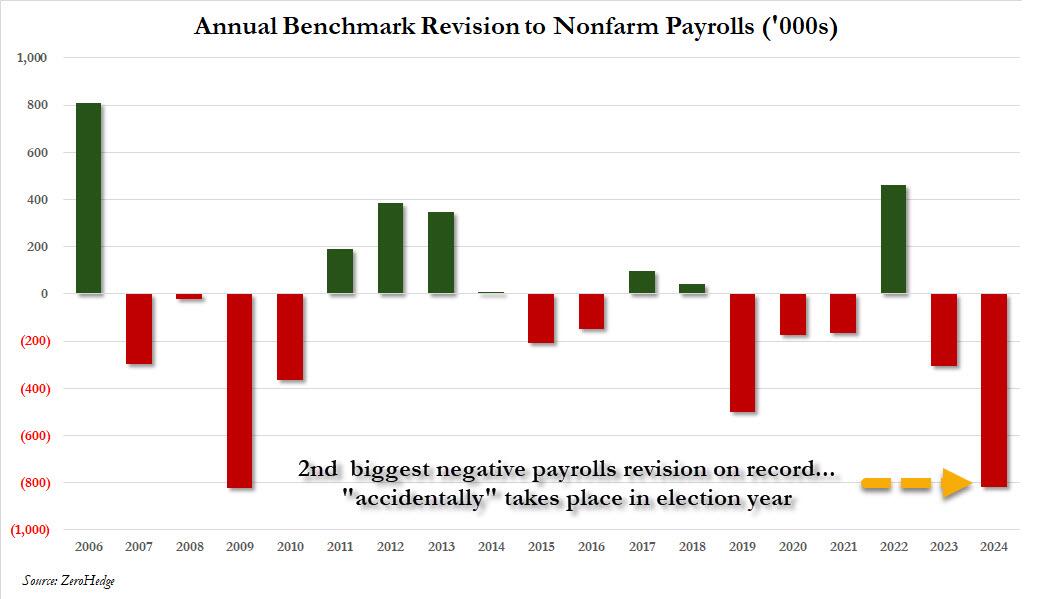

How big is the 818,000 revision in context? As the chart below shows, the 2024 revision was the biggest in the past decade, and the second biggest on record, with just the 824K downward revision in 2009 just (barely) greater.

The revisions confirm that – as we had been warning for much of the past year – the labor market started moderating much sooner than flawed conventional wisdom thought. It wasn’t until earlier this month that markets and economists grew concerned with the release of the July jobs report. That set off alarm bells with a weak pace of hiring and a fourth month of rising unemployment, but other metrics like jobless claims and vacancies have suggested a more moderate slowdown.

Putting it all together, we now know – as we reported first back in March – that the labor market is, and was, far weaker than conventionally believed. In fact, no less than 800,000 payrolls would end up “missing” when one uses the far more accurate Quarterly Census of Employment and Wages data rather than the BLS’ woefully inaccurate and politically mandated payrolls “data”, and if one looks back the the monthly gains across most of 2023, one gets not 218K jobs added on average every month but rather 150K, a 31% decline. Needless to say, the market would look very different if it had known that effectively all the payroll “beats” of the past year would be deleted!

Of course, none of that paints Bidenomics, or Kamalanomics, or whatever it is now, in a flattering picture, because while one can at least pretend that issuing $1 trillion in debt every 100 days to add 3 million jos per year is somewhat acceptable, learning that that ridiculous amount buys 800,000 jobs less is hardly the endorsement that the White House needs. On the flip side, pretending that the US had added an additional 800,000 jobs in the past year is precisely what Biden, and now, Kamala would have wanted to generate the kind of buzz and momentum that somehow translates into the “greatest economy ever”… at least until it is all revised away as the admin’s lies finally wash away.

What is the implication for the market? Well, as UBS trader Leo He correctly notes, “the Fed is well aware of nonfarm payrolls (establishment survey) overstating the job market, but unemployment rate (household survey) underestimating the job market” and he goes on to quote Governor Bowman’s speech on Tuesday:

“There are also risks that the labor market has not been as strong as the payroll data have been indicating, and it appears that the recent rise in unemployment may be exaggerating the degree of cooling in labor markets. The Q4 Quarterly Census of Employment and Wages (QCEW) report suggests that job gains have been consistently overstated in the establishment survey since March of last year, while the household survey unemployment data have become less accurate as response rates have appreciably declined since the pandemic. The rise in the unemployment rate this year largely reflects weaker hiring, as job searchers entering the labor force are taking longer to find work, and layoffs remain low. It is also likely that some temporary factors contributed to the soft July employment report. The rise in the unemployment rate in July was largely accounted for by workers who are experiencing a temporary layoff and are more likely to be rehired in coming months. Hurricane Beryl also likely contributed to weaker job gains, as the number of workers not working due to bad weather increased significantly last month.”

At the end of the day, all this does is cement the Fed’s 25bps rate cut next month.

As for broader socio-political implications, the reactions are already pouring in with those on the blue side of the spectrum pretending nothing happened, while those on the other side of the aisle raging at what has now become clear propaganda by the highly politicized Department of Labor. To wit, here is RFK, Jr., proposed VP candidate Nicole Shanahan slamming the BLS, and using our data to do so:

The Bureau of Labor Statistics (BLS) has long been used as a tool of propaganda by the executive branch. Here’s how: they distort definitions, manipulate data, exclude discouraged workers, and revise past reports to create narratives that fit the agenda of whichever administration is in power. This skews the actual economic picture and misleads citizens about the true state of our economy. It’s like a game of musical chairs, and neither side wants to be caught standing when the music stops. The Constitution doesn’t grant the government the authority to track unemployment statistics, so why do we even have this agency? Perhaps it’s time to get rid of it. Their $750M budget could surely be put to better use, and private companies already track U.S. unemployment for free. Win-win.

We agree: back in March we concluded our article, which predicted today’s revision with near 100% accuracy, by warning that the staggering size of the revised data “is also why nobody in the mainstream media – which is now nothing more than the PR smokescreen for the Biden puppetmasters, the government and the deep state – will ever mention this report.”

Today it will be more difficult for the propaganda press to ignore it.

At least she should speak in front of a Communist Chinese flag! Her true master.

On Tuesday, it was announced that Presidential candidate Kamala Harris would be supporting President Joe Biden’s tax proposals for 2025, which include a 44.6% capital gains rate and a 25% tax on unrealized gains.

Having used up all of the rest of the batshit, insane, counterintuitive economic dirty tricks left in the “we’ll literally do anything but cut spending” bag, the Biden administration began pushing this tax idea in April 2024 when I first wrote about it. Unrealized gains taxation could be the most destructive idea for our country since prohibition, I joked at the time.

As part of its budget proposal for the 2025 fiscal year, the Biden administration was trying to raise an addition $4.3 trillion over 10 years in the worst way possible: imposing a minimum tax equal to 25 percent of a taxpayer’s taxable income and unrealized capital gains less the sum of their regular tax, for taxpayers with wealth over $100 million.

Biden/Harris pushes taxes way beyond the revenue maximing point, down to the point of deminishing revenues and economic growth. Here is the Laffer Curve.

Putting aside the fact that this high-risk idea only amounts to a pittance, $430 billion per year, the introduction of taxing unrealized gains could be one of the worst slippery slopes we ever dare to roll our country’s economy down.

We could save $1 trillion just by not sending $100 billion a year to other nations for starters.

A tax on unrealized capital gains means that individuals are penalized for owning appreciating assets, regardless of whether they have realized any actual income from selling them.

If you purchased a stock for $100 this year, for example, and it increased to $110 next year, you would pay the assigned tax rate on the $10 capital gain. You didn’t sell the asset, so you don’t realize the $10 appreciation, but must pay the tax regardless.

Taxing unrealized capital gains contradicts the basic principles of fairness and property rights essential for a free and prosperous society. Taxation, if we’re going to have it on income, should be based on actual income earned, not on paper gains that may never materialize.

mplementing such a tax not only deeply infringes upon personal liberty and private property rights — but I can’t help but think about how it also sets a destructive wrecking ball rolling down a slippery slope for the first time in our nation’s history.

And, given the precarious state of our nation’s finances, it doesn’t seem like the best time to start spitballing about new risky ideas that may or may not catch on only because they sound like they are addressing the problem of a widening wealth gap that Federal Reserve policies created and continue to exacerbate to begin with.

If the administration really wanted to address the problem of wealth inequality, it would be setting its sights on the central bank that sacrificed price stability so it could spray trillions of dollars in “stimulus” toward financial assets, while cutting American families paltry checks of just $600, during COVID. When I did the math during COVID, the total amount spent to bail out the country.

Why do we trust any Democrat politiician? I certainly don’t!

Taxing unrealized gains would risk mass sale of US assets and therRich fleeing.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.