Mortgage applications increased 3.2 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending December 9, 2022.

The Refinance Index increased 3 percent from the previous week and was 85 percent lower than the same week one year ago. The unadjusted Purchase Index decreased 1 percent compared with the previous week and was 38 percent lower than the same week one year ago.

You can see the impact of seasonalilty on mortgage purchase applications (white line). They peaked in the week of May 6, 2022 and have been generally declining since. While refi applications (orange line) increased over the past week, they have been pummelled by The Fed tightening.

It is quiet today as investors wait for The Fed to announce a 50 basis point rate increase. Fed Funds Futures point to almost another 100 basis point hike by May 5, 2023, then a slow decline in The Fed Funds target rate (upper bound).

And here is Sam Bankman-Fried and his high-powered legal defense.

Central bankers won’t ride to the rescue when growth slows in this new regime, contrary to what investors have come to expect. They are deliberately causing recessions by overtightening policy to try to rein in inflation. That makes recession foretold. We see central banks eventually backing off from rate hikes as the economic damage becomes reality. We expect inflation to cool but stay persistently higher than central bank targets of 2%.

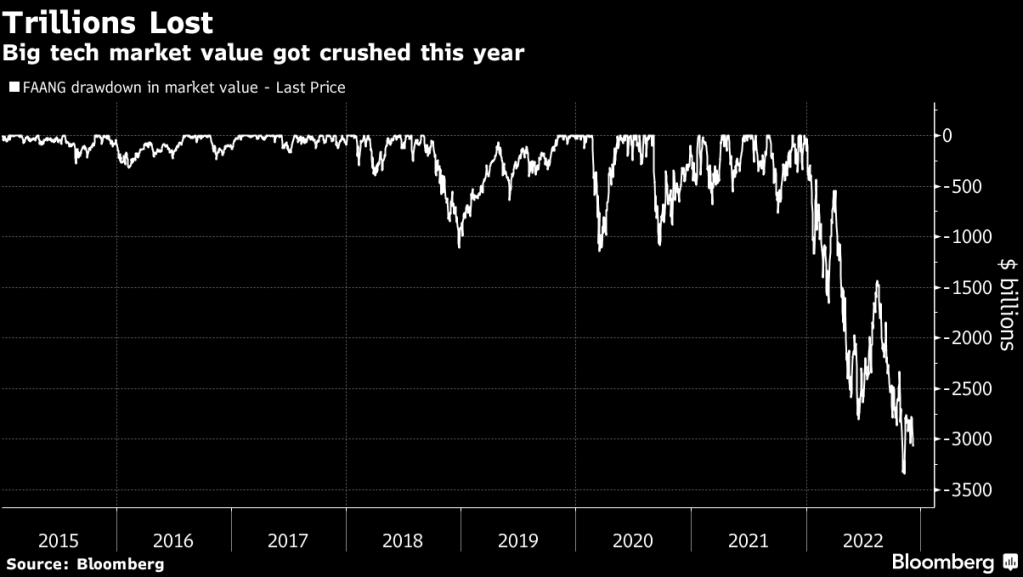

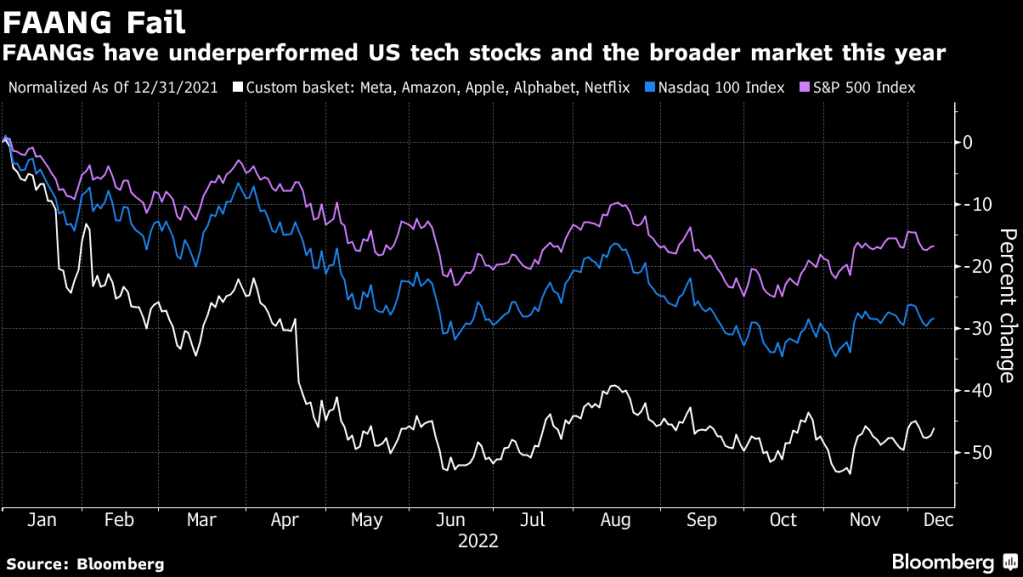

For some investors, this year’s rout in high-flying technology stocks is more than a bear market: It’s the end of an era for a handful of giant companies such as Facebook parent Meta Platforms Inc. and Amazon.com Inc.

Those companies — known along with Apple Inc., Netflix Inc. and Google parent Alphabet Inc. as the FAANGs — led the move to a digital world and helped power a 13-year bull run. And FAANG drawdown have reached over $3 trillion.

FAANGs (Meta, Amazon, Apple, Alphabet, Netflix) are getting clobbered in 2022.

Typically, when The Fed prints too much money, such as 10% or higher (red line), inflation follows. Particularly when The Fed prints at 25% YoY in Q4 2020, it was followed by the highest inflation rate in 40 years. But if M2 Money continues to slow, inflation will likely slow, but not to The Fed’s target of 2%.

Despite what Minneapolis Fed’s Neal Kashkari said about The Fed having infinite printing resourses, The Fed is going to fight inflation THAT THEY HELPED CAUSE. Biden’s energy policies (did you see that Elon Musk has a car that uses plentiful hydrogen?), and excessive Federal spending by Biden/Pelosi/Schumer, are culprits in creating the supply chain problems facing America. BUT after the 25% surge in M2 Money in 2020 and 2021, we saw M2 Money VELOCITY crash and burn to its lowest level in history. Which means the “bang for the buck” for printing more money is negligible.

Of course, big tech firms got caught influencing the 2020 Presidential election (see Musk’s release of Twitter files) and engaged in restriction of the 1st Amendment (Freedom of Speech). How much will that impact FAANG stocks going foward?

And yes, the US Treasury yield curve is inverted pointing to a recession in 2023.

And yes, apparently Biden was complicit in the Twitter fiasco.

The Fed has signaled the terminal rate will likely be around 5% — we think an upper bound of 5% — reached in early 2023. To get there, the central bank will likely raise rates by 50 basis points at its December 2022 meeting, followed by two more 25-bp hikes in 2023. We then see it holding at 5% throughout the year. Markets have priced in a similar amount of tightening.

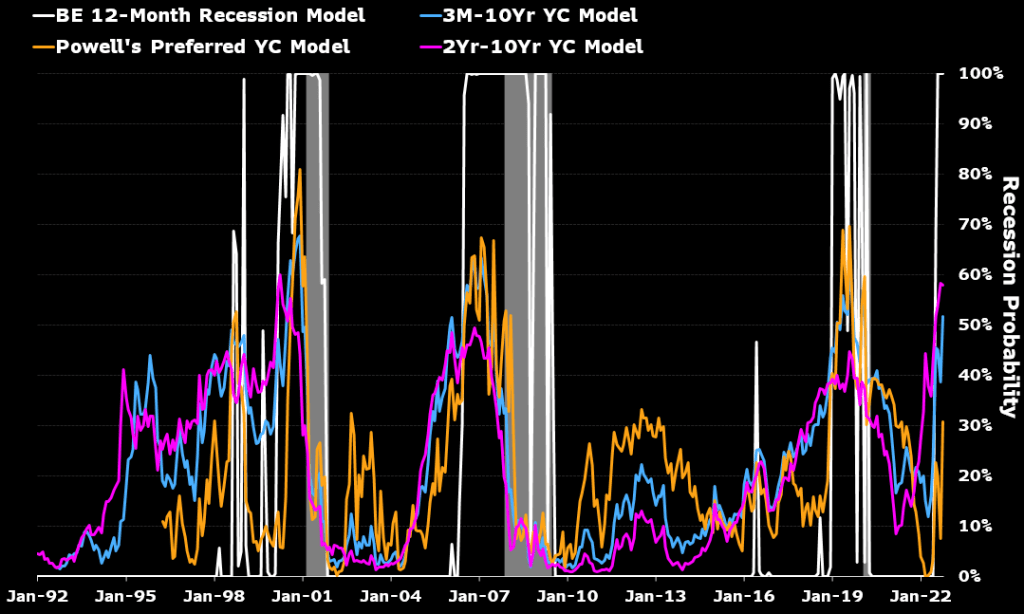

Controlling inflation comes at a cost to growth. Yield curves have inverted. A Bloomberg Economics model shows a 100% probability of recession starting by August 2023. Take that — like all model forecasts — with a grain of salt. But the basic view that aggressive Fed tightening will very likely tip the economy into a downturn is correct.

While various measures of impending US recession show a good chance of a 2023 recession, Powell’s preferred measure of the yield curve shows only a 30% chance.

What Might the Recession Look Like?

We project a 0.9% GDP contraction in 2H 2023, driven by an investment downturn as firms pare inventories amid a downshift in consumption. Residential investment will also contract with real interest rates likely to rise steadily throughout 2023 as nominal rates stay high and inflation moderates.

An Inventory-Led Downturn

Resilient consumption should help put a floor under demand.

Households have enough of a cash buffer — extra savings built up over the course of the pandemic, rising COLAs for Social Security recipients, ongoing state and local government stimulus and solid 2022 wage income growth — to sustain consumption during the recession. Our base case is for real spending to grow at a quarterly annualized pace of about 0.5% in 2023, with strength concentrated in services.

By one measure, households may still have $1.3 trillion in the coffers, based on flows within the personal income report through September. At the current rate of drawdown, that’s enough to last around 15 months, or through the end of 2023. Funds may dry up faster as job losses mount and the unemployed fall back on their savings.

$1.3 Trillion Extra Savings to Keep Spending Positive

The labor market remained exceptionally tight into the end of 2022. We expect it to soften significantly next year, with the unemployment rate rising to 4.5% by the end of 2023. The pace of hiring will slow markedly as support from catch-up hiring dissipates and the effects of restrictive monetary policy settle in. We estimate only 20%-30% of total employment is still in sectors experiencing labor shortages, implying demand for labor is falling fast.

Avoiding a Hard Landing Depends on Inflation, Fed

Extreme circumstances — the pandemic, Russia’s invasion of Ukraine — have made a recession more likely than not. Extreme circumstances can change, and so can policy makers’ response Whether the US can stick a soft landing depends substantially on how external conditions develop and how the Fed responds.

Not our base case, but we can envision a scenario in which the central bank opts to ease rates in 2023, boosting the chances of a soft landing.

One way that could happen is inflation falling faster than expected. Currently, our baseline is for headline CPI to drop to 3.5% and the core to 3.8% by the end of 2023. The most important assumption there is that energy prices remain flat next year from 2022.

In an alternative scenario, inflation fall faster as China maintains Covid controls and growth stumbles. A Bloomberg Economics model attributes the recent fall in oil prices entirely to a drop in demand — mainly from China. If China’s growth falls off the cliff, perhaps amid a sharp rise in Covid cases and resumed lockdowns, commodity prices could tumble sharply.

A warm winter in Europe and the US could also keep energy prices in check. Lower demand from Europe for US liquefied natural gas would help stem the increase in domestic electricity prices.

In that scenario, US energy prices could fall 20% in 2023 and headline inflation may drop to 2% by the end of the year. Lower gasoline prices would work to soften inflation expectations, easing pressure on the Fed to hold rates at higher level. A rate cut could then come in 2H 2023, raising the possibility of a soft landing.

Scenarios of CPI Inflation in 2023

The risk cuts both ways. A quick and successful pivot to reopening in China could boost oil and other commodities prices. A colder winter in Europe and the US would generate upward pressure for electricity and utility prices. Assuming China is fully open by mid-2023 — the base case for our China team — energy prices could increase by 20% in the year. In that case, headline US CPI would hit a bottom of 3.9% in midyear before surging to 5.7% by year-end.

In that scenario, the terminal fed funds rate would most likely top 5%, possibly closing 2023 near the upper end of St. Louis President James Bullard’s estimated restrictive range of 5%-7%.

Bloomberg Economics US Forecast Table

Thanks to Yellen’s legacy of too low interest rates for too long, The Fed is playing catch-up by finally raising rates.

Always behind the curve, US Senators (Warren, Marshall, Kennedy) want to get to the bottom of Silvergate’s decline and its relationship with Sam Bankman-Fried and FTX. This reminds me of the 2008 financial crisis when The Federal Reserve claimed they never saw it coming. Despite the data.

But back to crypto bank Silvergate.

Crypto bank Silvergate Capital Corp. was asked by three US Senators to release all records about transfers of funds for the collapsed FTX empire of Sam Bankman-Fried.

“Your bank’s involvement in the transfer of FTX customer funds to Alameda reveals what appears to be an egregious failure of your bank’s responsibility to monitor for and report suspicious financial activity carried out by its clients,” Senators Elizabeth Warren, Roger Marshall and John Kennedy wrote in a letter released Tuesday. “The public is owed a full accounting of the financial activities that may have led to the loss of billions in customer assets, and any role that Silvergate may have played in these losses.”

Shares of the La Jolla, California-based bank fell as much as 8%. The slide extends Silvergate’s losses on the year to more than 84% and has it trading at a fresh 52-week low. Not surprisingly, Silvergates’ stock price is closely linked to cryptocurrency Bitcoin.

The letter cite concerns about the banking services that Silvergate provided to both FTX as well as Bankman-Fried’s trading firm, Alameda Research. It says the arrangement between FTX and Alameda depended on Silvergate’s depository services and puts the bank “at the center of the improper transmission of FTX customer funds.”

“Silvergate’s failure to take adequate notice of this scheme suggests that it may have failed to implement or maintain an effective anti-money laundering program, as required under the Bank Secrecy Act,” the Senators said.

Perhaps Silvergate should be renamed Silverfish. But seriously, no US Senator or DC regulator saw the following chart?? Bitcoin and other cryptos have been clobbered in 2022 as The Fed tightens monetary policy to combat inflation.

Here is our regulator, SEC’s Gary Genslar, keeping an eye on cryto exchanges like FTX.

Maybe US Senators and DC regulators thought Silvergate is a silverfish.

The Covid outbreak of early 2020 begat a massive surge in monetary stimulus which has dissipated. Notice that home price growth is dissipating as well.

Also causing problems for housing is NEGATIVE REAL WAGE GROWTH. While the US is suffering from inflation and decling real wage growth, trading partner Germany has even a worse REAL WAGE GROWTH problem.

Deutsche Bank, my former employer, said that The Fed will slash rates by 200 basis points by mid-2024 after staying hawkish in the short term.

Deutsche Bank increased its view on the terminal rate and now sees it hitting 5.1% in May.

The Federal Reserve will remain hawkish in the short term but will cut benchmark rates sharply after that, according to a Monday note from Deutsche Bank.

The central bank has hiked rates by 375 basis points so far this year, with another half-point increase widely expected next month. Even more tightening will come, with analysts at Deutsche Bank increasing their view on the terminal rate, which they now see hitting 5.1% in May.

“Risks remain skewed to the upside, and we caution that the transition to pausing and eventual cuts may not be entirely linear,” the note said. “If elevated inflation and labor market imbalances persist, or financial conditions fail to tighten, a higher terminal rate could be needed.”

Meanwhile, the economy will slow down amid the aggressive tightening, and Deutsche Bank sees an 80% probability of a recession in the next year.

Analysts anticipate a moderate recession beginning mid-2023, with real GDP falling about 1.25 percentage points over three quarters and the unemployment rate reaching a peak of 5.5%.

“With a sharp rise in the unemployment rate and inflation showing clearer signs of progress, the Fed should cut rates by 200bps by mid-2024 when it approaches a neutral level around 3%,” analysts said. “QT should cease when the Fed cuts rates, to ensure both tools are not working in competing directions. Balance sheet drawdown could be modified or halted earlier if reserves continue to fall faster than expected.”

The first rate cut will be 50 basis points in December 2023, followed by 150 basis points of cuts into 2024, the note said.

The last Fed Dots Plot shows the next leg of The Fed Rollercoaster.

In the short term, Fed Funds Futures are pointing at another 106 basis point increase by June 2023.

Why is this terrifying? Blockchain technology is a fantastic innovation for processing payments given its ledger capabiliities. But that means that The Federal Reserve might be able to look at your complete history of expenditures. Or worse, perhaps even shut down your ability to make payments, This may lead to a China-style “social credit score” where the Fed and the Federal government punish people for driving “too much” increasing your carbon footprint or eating non-Federal government approved foods and lowering your social credit score.

Will there be safeguards? Allegedly, but remember the FBI hid Hunter Biden’s laptop prior to the Presidential election of late 2020. And HOW did our nation’s regulators completely drop the ball on Sam Bankman-Fried (or Spam Bankfraud)?

The US economy is in “The Deep.” Deep into yield curve inversion, that is.

The US Treasury 10Y-2Y yield curve swam deeper into inversion at -75 basis points. The deepest inversion since just before The Great Recession and housing market crash.

During the Covid crisis of 2020 (red box). consumer credit declined and households were saving. But following the end of US Covid economic shutdowns, we saw inflation soaring to 40-year highs as Biden declared war on fossil fuels and a Pelsoi-led Congress went on an epic spending spree. But with soaring inflation, came a decline in personal savings and soaring consumer credit outstanding in an attempt to cope with Bidenflation.

Meanwhile, in the crypto universe, CNBC’s Jim Cramer and ARK’s Cathie Wood are going big for cryptos. With Wood buying Bitcoin and Cramer touting Coinbase.

Hmmm.

But at least Litecoin and the others are up today. Likely because Cramer and Wood are touting cryptos with “buy the dip!” strategy.

And on the Sam Bankman-Fried fiasco front, I am watching the deflection of wrongdoing from SBF to his girlfriend and now the co-CEO of Alameda Research, Sam Trabucco.

Bloomberg: He has a degree from MIT and cut his teeth as a trader at Susquehanna International Group. Yet the former co-head of Alameda Research made it clear that poker and black-jack tables were where he honed the gambler’s instincts he applied to cryptocurrency trading.

“I may or may not be banned from 3 casinos for this,” Sam Trabucco once tweeted about counting cards at black jack tables.

As of today, the US Treasury 10yr-2yr yield curve is the most inverted since 1981 at -70 basis points.

Meanwhile, equity put/call ratio from CBOE spiked yesterday to highest since 1997.

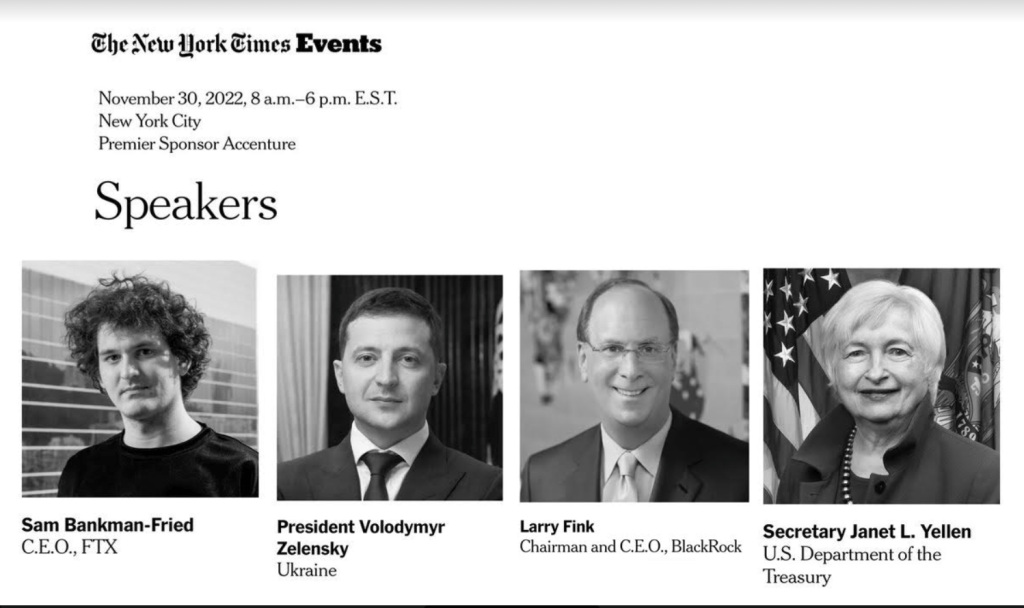

I am disappointed that The New York Times cancelled their $2,400 event to listen to Sam The Sham Bankman-Fried, Vlad “Show my your money!” Zelensky, Larry “The Big Fink” Fink and Janet “We never saw it coming” Yellen. I would have loved to do the New York Times job for them and ask hard questions to Sam The Sham and Zelensky about money laundering.

You must be logged in to post a comment.