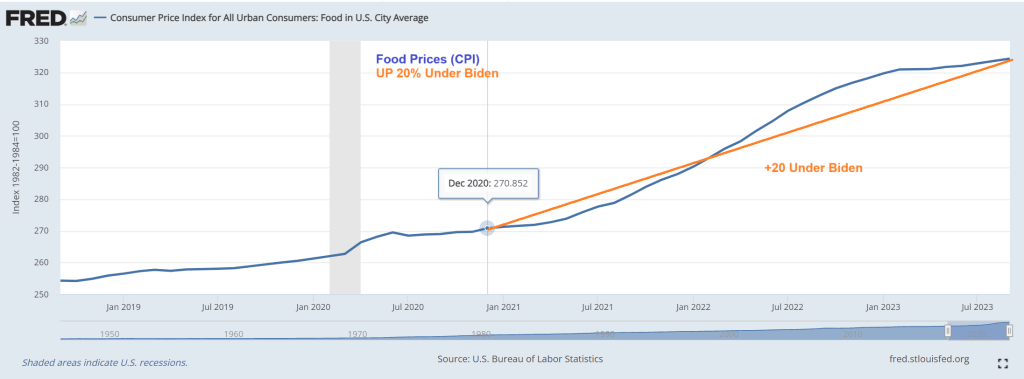

First, food prices are up 20% since December 2020. Talk about destruction of middle class wealth!

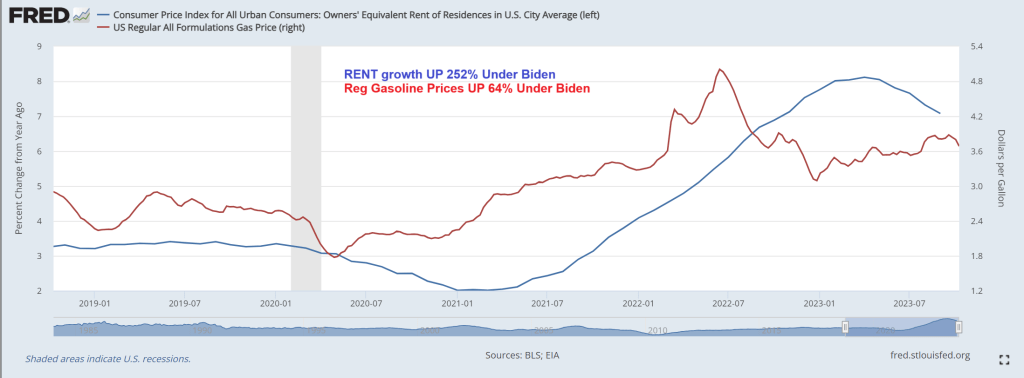

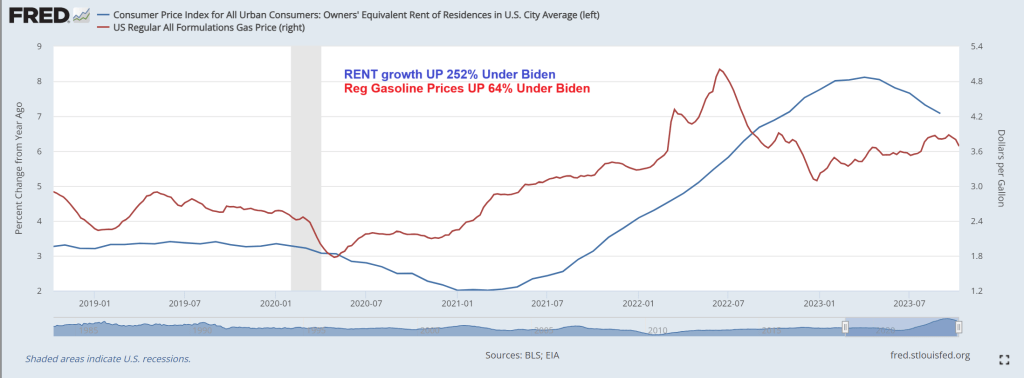

That is in addition to gasoline prices are up 64% under Biden while rent growth is up 252%. Well, Biden waived through millions of illegal immigrants and rent had to rise. Biden and Washington DC’s broken borders is Livin’ La Vida Loco.

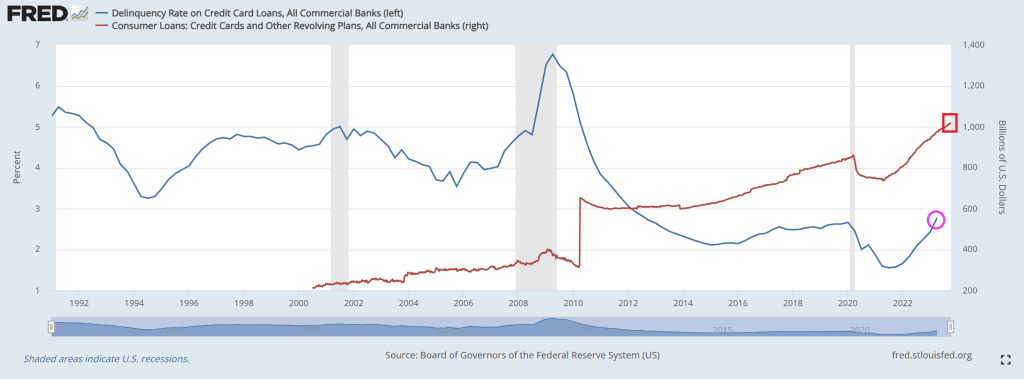

To cope with inflation (that Paul Krugman claims is over but the last inflation report showed that the tinders of inflation are hard to extinguish), consumers have turned to credit cards to survive. In fact, credit cards have expanded 38% since April 2021 despite rapidly rising interest rates. And credit card delinquency rates are rising and are now above Covid-era economic shutdown levels.

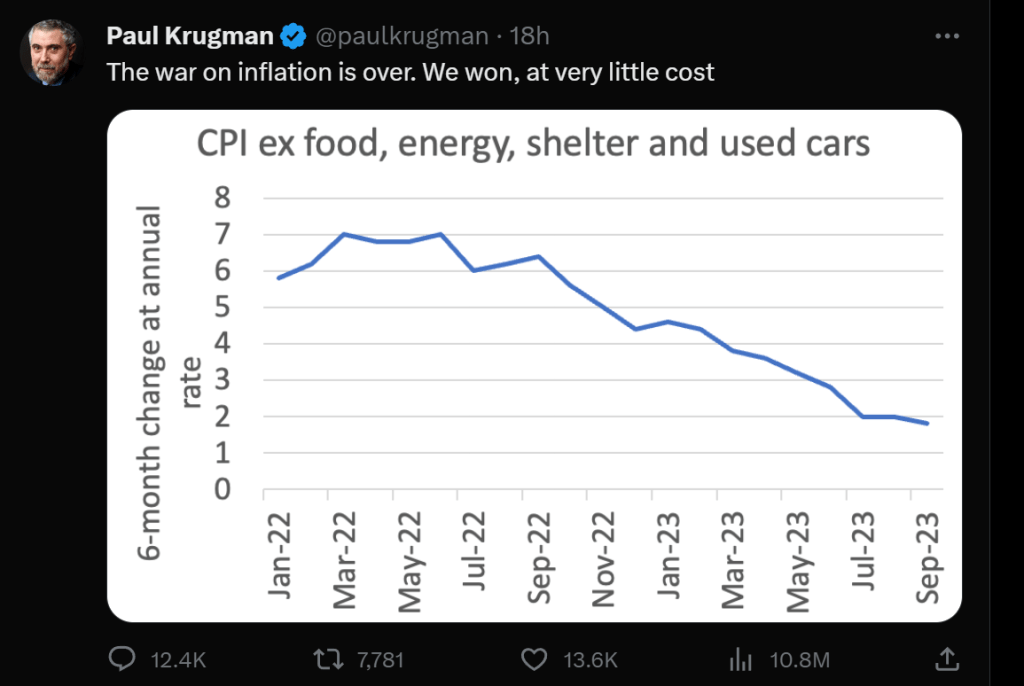

Paul Krugman, Nobel Laureate in economics and media celebrity, made a terrible claim yesterday when he pronounced that “The war on inflation is over. We won, at very little cost.” Krugman’s proclamation was trumpeted by The View’s Joy Behar Joy who claimed that everything is going great in the country! The economy is “booming” and people are having an “easier time” putting bread on the table. Huh? Easier than a month ago maybe, but not easier since 2021 under Bidenomics.

Hmm. Suppose that during World War II the Germans had stopped after they invaded and captured Paris on June 14, 1940. The war could have been over, but France was lost to Germany amidst thousands of dead and loss of property. That is not a victory, but a crushing defeat.

Just like my Paris example, Krugman’s claim the war on inflation is over and we won AT VERY LITTLE COST was grossly misleading and a big kerplunk (thud). Why? For one, the average American family is $7,400 POOR than in January 2021 when Biden became President. So, it looks like we know the cost of inflation and it was steep, not “very little cost.” Well, very little cost to elitist millionaires like Krugman.

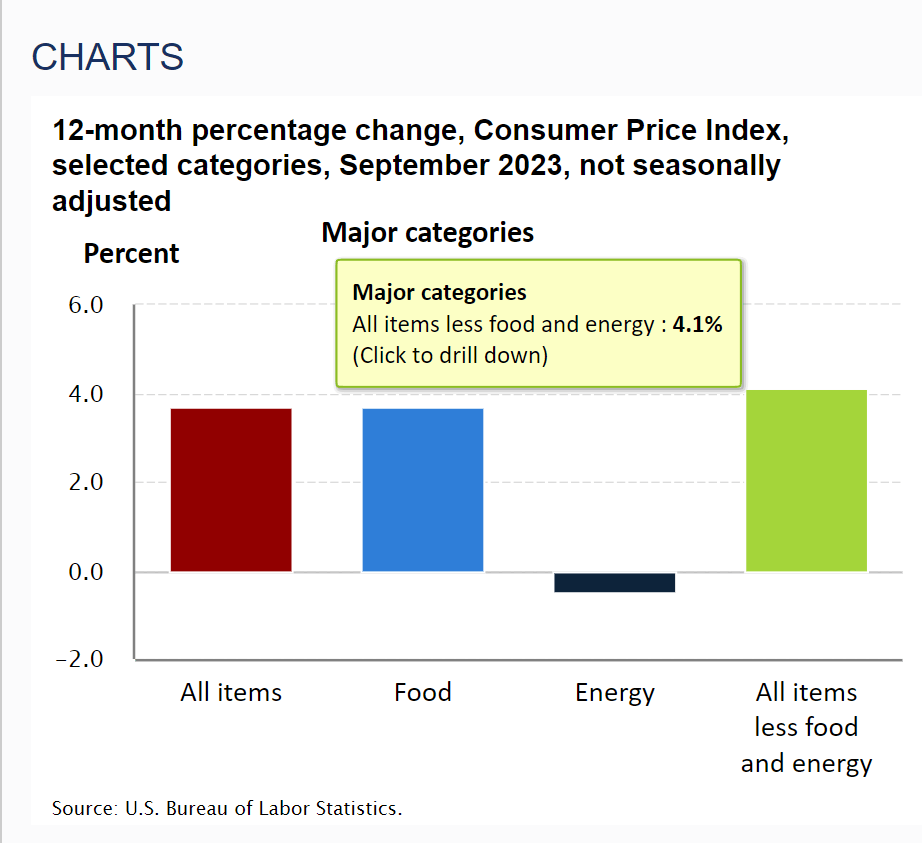

Krugman loves the recent inflation report from the BLS. Specifically, the 12-month change in the Consumer Price Index Less Food And Energy for September was 4.1%. Krugman focuses on the recent 6-month change being less than 2%. In Krugman’s mind, this is victory … core inflation has been tamed and inflation is at The Fed’s target rate of 2%.

But before Krugman pops the champagne cap on the 1959 Dom Perignon for $42,350 (while the rest of us are drinking E&J Gallo’s Thunderbird), bear in mind that he is referring to the RATE OF GROWTH in prices, not the highly elevated levels of prices. Victory against inflation would be if prices returned to December 2020 levels.

I pointed out yesterday that “real” wages contracted 0.1% YoY (after 3 months positive) in September. It is important to note that real wage growth was negative from 2021 until 3 months ago, but has gone negative yet again. Victory??

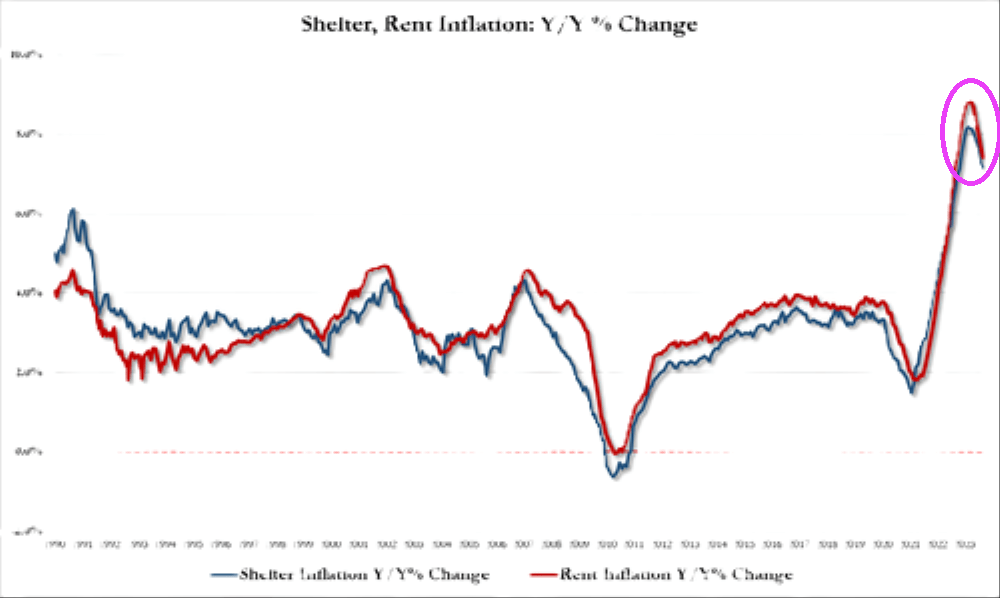

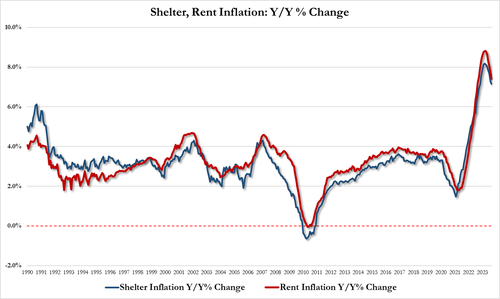

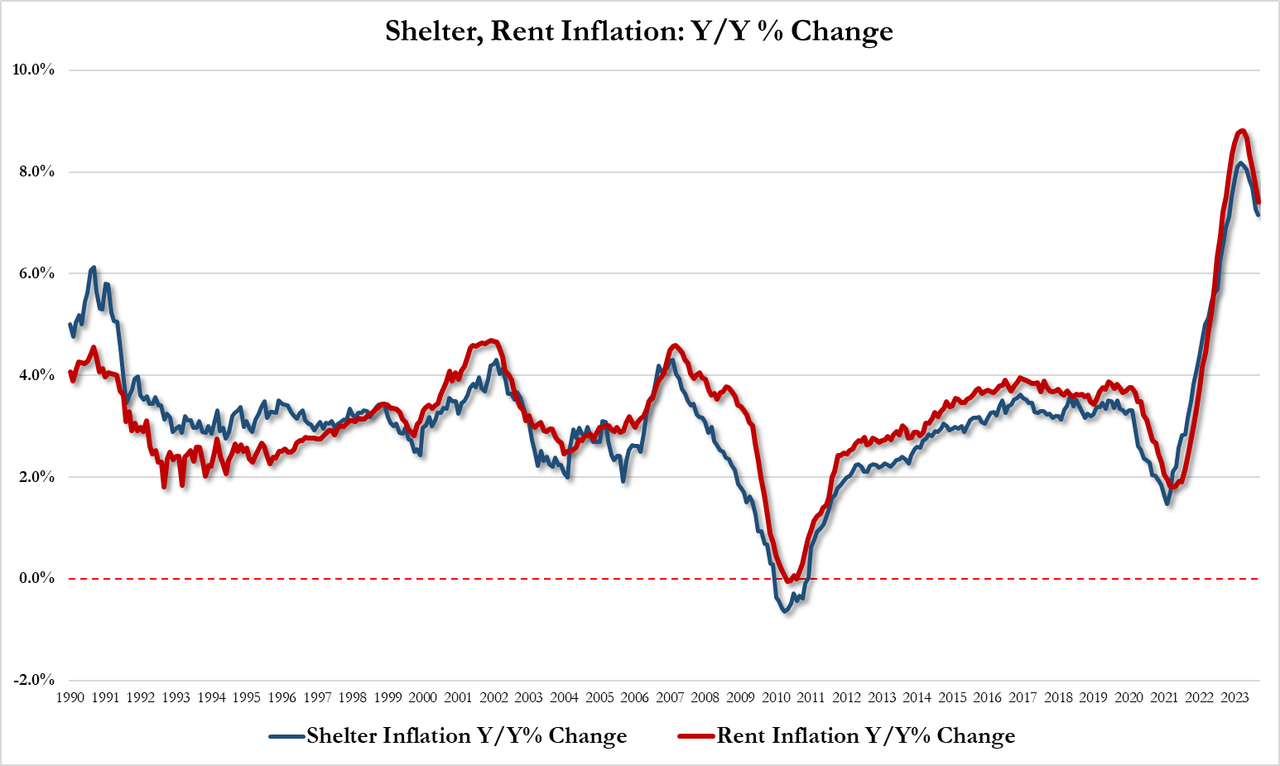

Krugman prefers core inflation, removing food, housing and energy. You know, the three things most Americans actually care about. Take shelter (or rent of residence) where rent is growing at a sizzling 7.1% YoY.

Under Biden and Congress’ reckless spending splurges (and inane Federal energy policies), regular gasoline prices are up 64%. Growth in rent of residence has grown 252%! So, Professor Krugman, Americans are far worse off than before Biden was President.

If prices return to December 2020 (or pre-Covid levels), I will declare a victory. But for right now, symbollically, the German army is occupying France and Paris with horrible suffering for the French people. In other words, Americans are still far worse off under Biden even though inflation is finally slowing.ew

Speaking of France and World War II, maybe we should consider Joe Biden as today’s Pierre Laval, leader of Vichy France since Biden seems more concerned with pleasing Klaus Schwab and The World Economic Forum than America’s middle class and low wage worker (like Laval was concerned with that German leader Adolf Hitler thought).

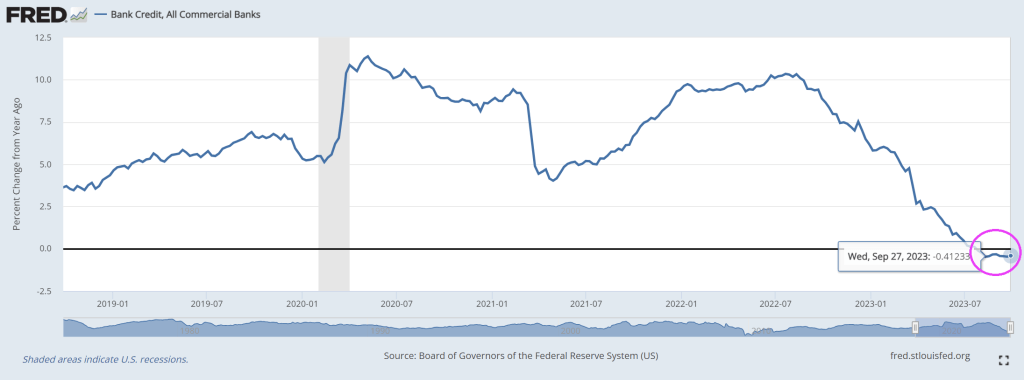

Bidenomics is failing catestropically. Example? As interest rates rise to fight Biden’s Federal spending splurges, bank credit growth slowed to -0.41% YoY for the 10th straight week of negative credit growth.

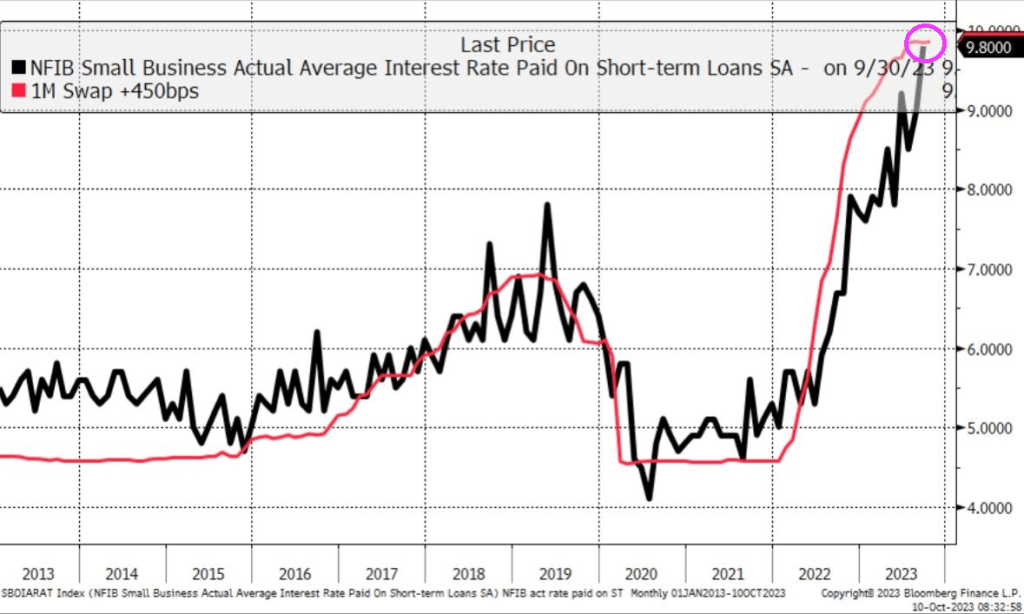

While interest paid on short-term loans almost 10%!!

“Jimmy, watch me tank the economy even worse than you did!”

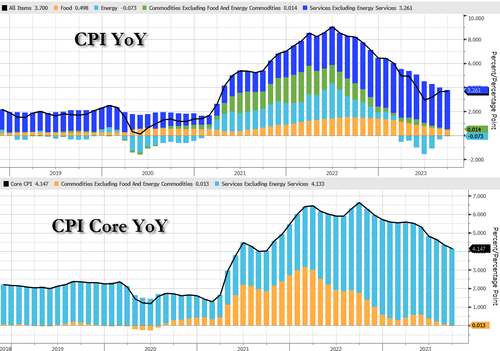

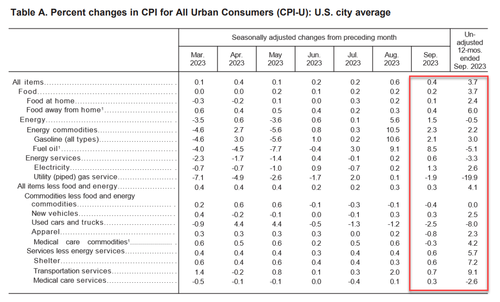

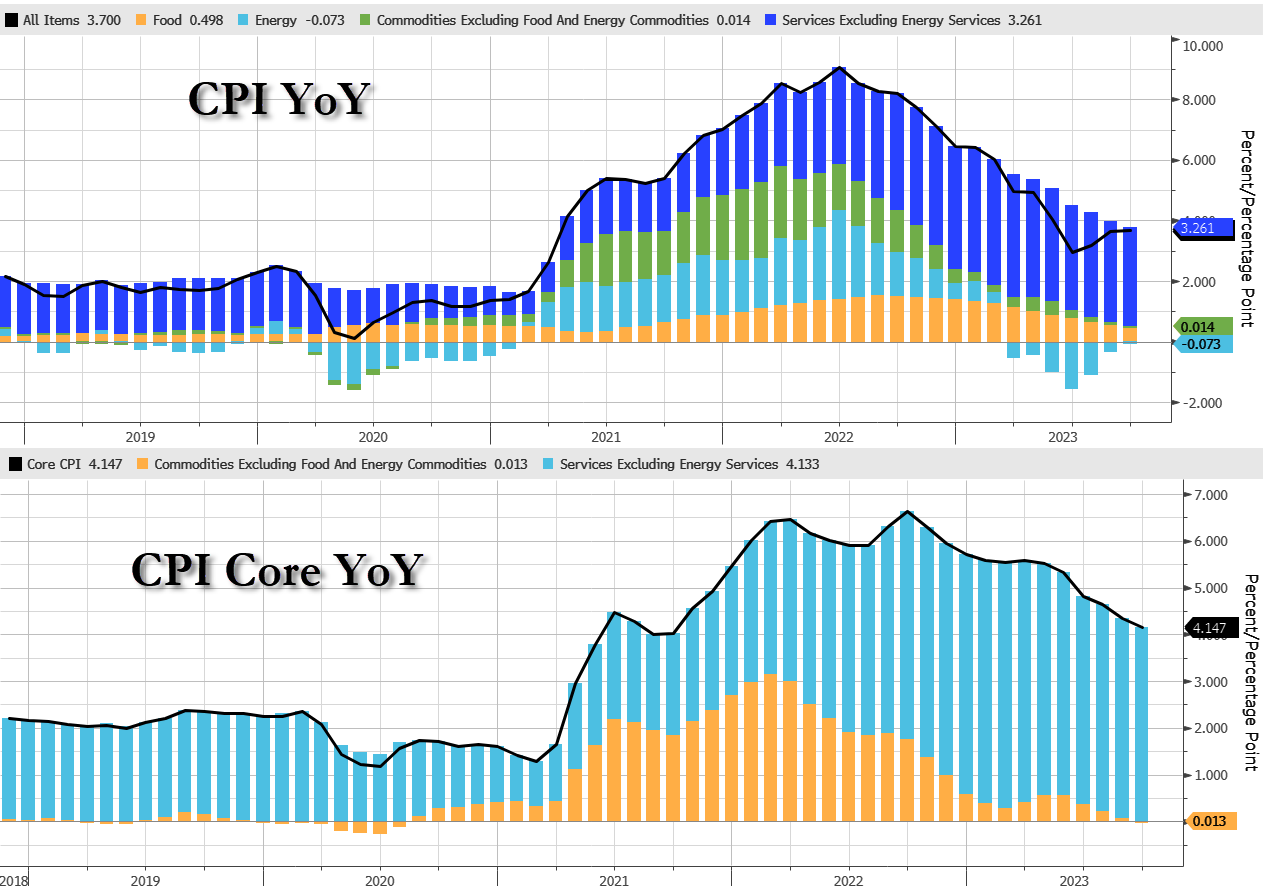

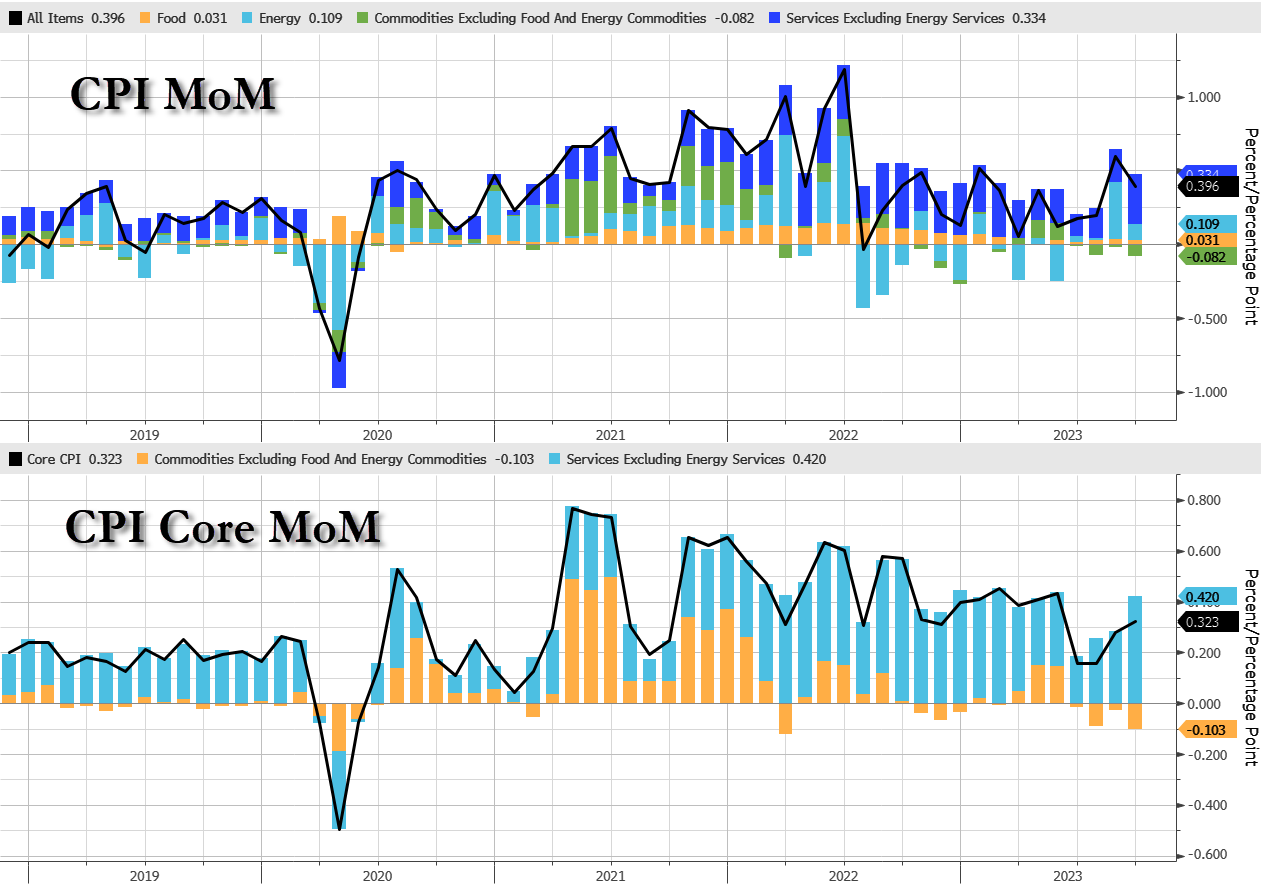

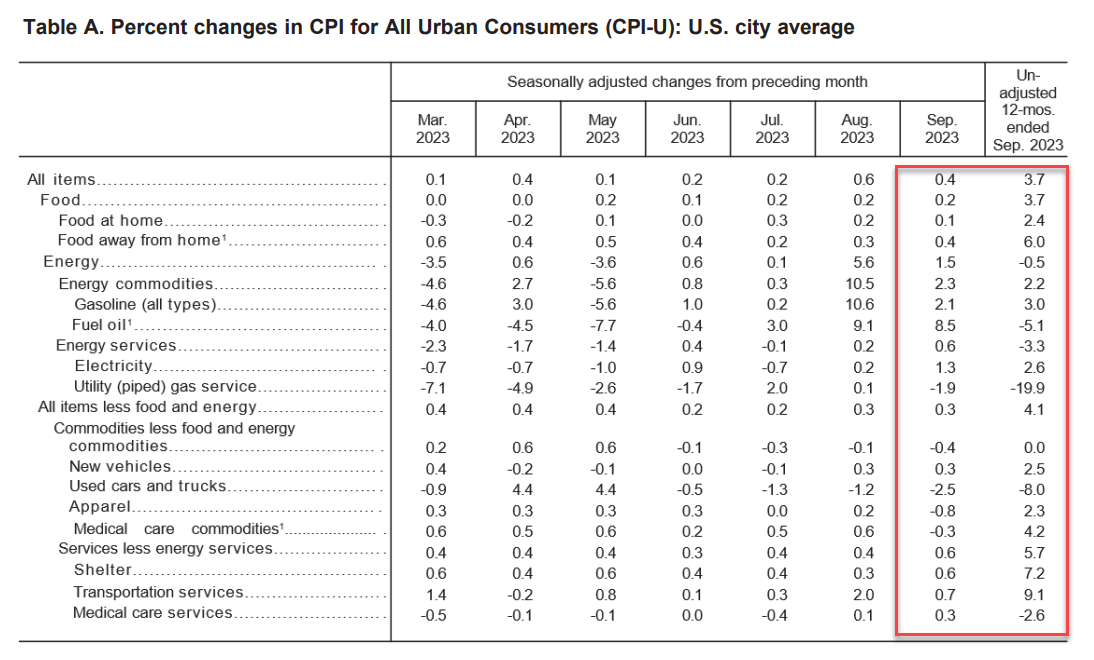

However, headline CPI came in modestly hot at +0.4%, with YoY at 3.7% – that is the 3rd monthly rebound in a row.

Source: Bloomberg

Core CPI rose 0.3% MoM, with YoY sliding to +4.1% YoY (as expected)… it still hasnt been below 4.00% since May 2021….

Source: Bloomberg

Food and Commodities contribution to YoY CPI slowed while Services increased…

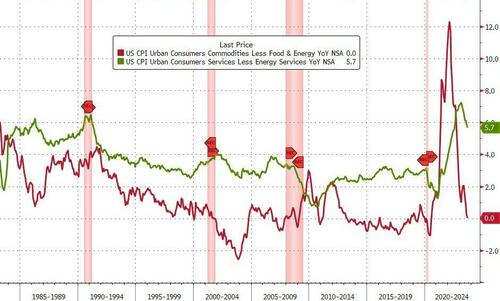

Goods inflation dipped back to unchanged YoY and Services CPI slowed to +5.7%…

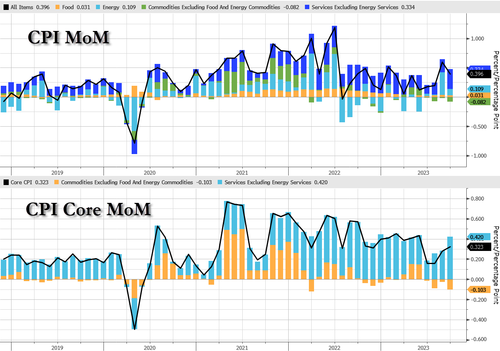

Services stands out on A MoM basis…

Under the hood, gasoline continues to rise and used car prices drop…

Rent of primary residence and owner’s equivalent rent YoY both exceeeded 7%. Fixing a car/truck rose 10.2% (will people start to notice that repairing EVs is outrageously expensive?).

The index for all items less food and energy rose 0.3 percent in September, as it did in August.

The shelter index was the largest factor in the monthly increase in the index for all items less food and energy.

The shelter index increased 0.6 percent in September, after rising 0.3 percent the previous month. The index for rent rose 0.5 percent in September, and the index for owners’ equivalent rent increased 0.6 percent over the month.

The lodging away from home index increased 3.7 percent in September, ending a string of 3 consecutive monthly decreases.

Among the other indexes that rose in September was the index for motor vehicle insurance, which increased 1.3 percent after rising 2.4 percent the preceding month.

The indexes for recreation, personal care, new vehicles, and household furnishings and operations also increased in September.

The medical care index rose 0.2 percent in September, as it did in August.

The index for hospital services increased 1.5 percent over the month, and the index for physicians’ services was unchanged.

The prescription drugs index fell 0.7 percent in September.

The index for used cars and trucks fell 2.5 percent in September, after decreasing 1.2 percent in August.

The apparel index declined 0.8 percent over the month, and the communication index was unchanged.

The index for all items less food and energy rose 4.1 percent over the past 12 months.

The shelter index increased 7.2 percent over the last year, accounting for over 70% of the total increase in all items less food and energy.

Other indexes with notable increases over the last year include motor vehicle insurance (+18.9 percent), recreation (+3.9 percent), personal care (+6.1 percent), and new vehicles (+2.5 percent).

Gasoline prices continue to rise…

Shelter costs are slowing, but accounted for the largest part of core CPI…

Rent inflation 7.41%, down from 7.76% in August and the lowest since Sept 2022

Shelter inflation 7.15%, down from 7.27% in August and the lowest since Nov 2022

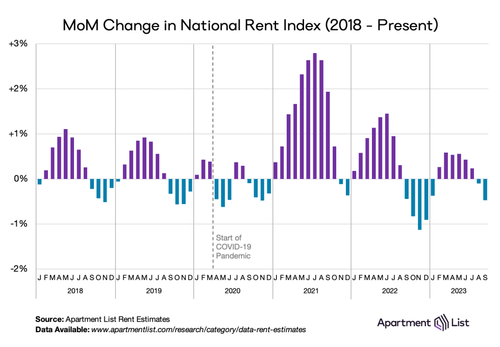

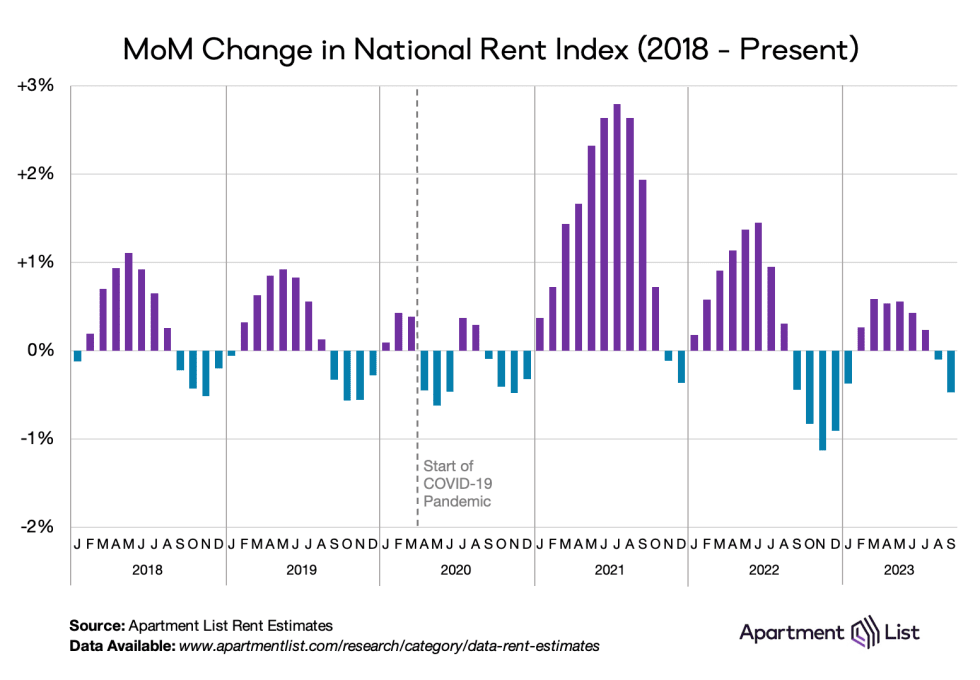

Bear in mind that while CPI very stale data is rising over 7%, real-time rent indicators are in freefall. Apt List’s Sept rent drop was the biggest on record…

And perhaps most importantly, one silver lining is that The Fed’s new favorite inflation signal – Core Services CPI Ex-Shelter YoY slowed to +3.74% (despite jumping 0.46% MoM). That is the lowest YoY since Dec 2021…

Is this third straight monthly increase in CPI YoY an inflection point? Or is M2 still leading the trend?

Turning from the cost of things to the ability to pay, “real” wages contracted 0.1% YoY (after 3 months positive)…

This is not the soft-landing cruise lower in inflation that the market (and The Fed) was hoping for…

Joe Biden is the Buzz Lightyear of the economy … and not in a good way. Under Biden and the Congressional spending sprees, the US debt is going to infinity … and beyond!

Twenty days.

That’s how long it took the Biden administration to add another half-trillion dollars to the national debt.

Bidenomics certainly requires a lot of borrowing and spending.

On September 15, the debt quietly blew passed $33 trillion. On October 5, it pushed above $33.5 trillion.

Don’t forget about the $194+ TRILLION in unfunded liabilities that politicians promised the non 1%.

By the way, it only took Biden and his willing accomplices in Congress three months to drive the national debt from $32 trillion to $33 trillion.

As of October 5, the debt stood at $33,513,382,512,663.51.

This is an unimaginable amount of money.

To put things into some perspective, the total output of the US economy as measured by GDP was only $25.46 trillion. That means the US economy would have to grow by 33.5% to cover the national debt.

At $33 trillion, the US national debt is more than the total economies of China, Japan, Germany, and the UK combined.

Looking at it another way, as of Oct. 10, every US citizen would have to write a $99,839 check in order to pay off the debt, and every American taxpayer is on the hook for $258,257.

Part of the reason the debt has increased so fast since June is because the Treasury is still rebuilding cash reserves that were depleted during the debt ceiling fight. But the fact remains – the federal government spends too much money.

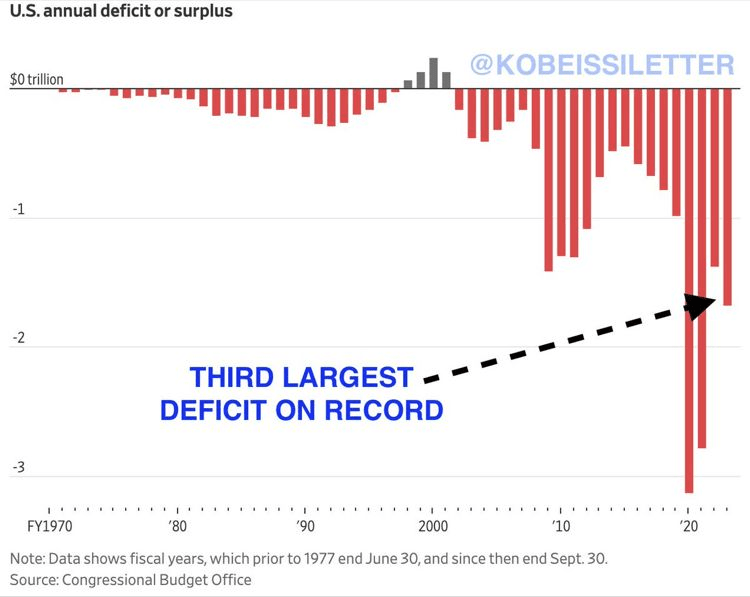

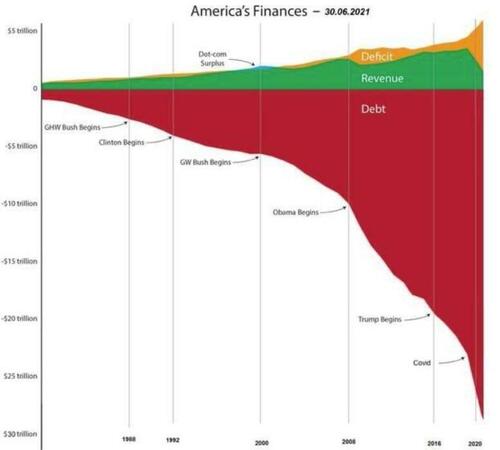

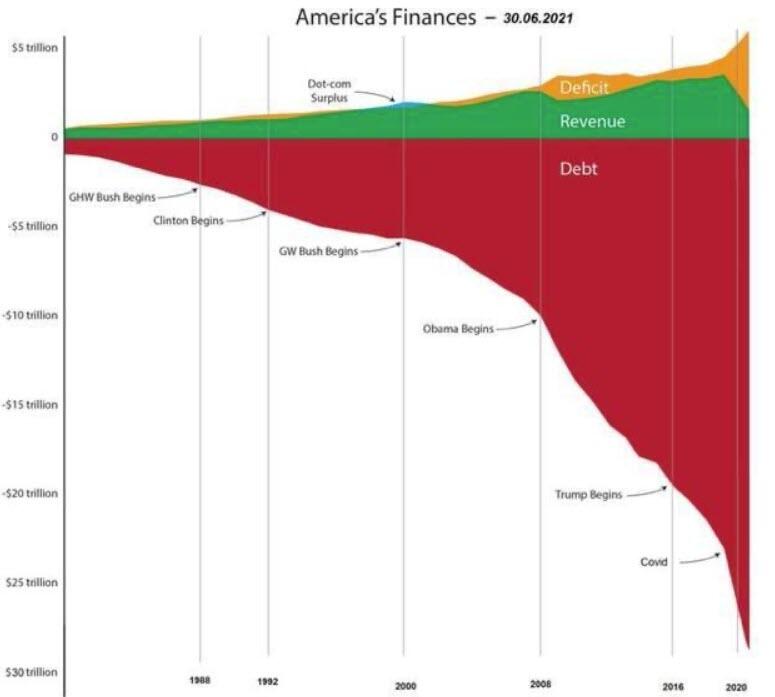

It’s hard to overstate just how bad the US government’s fiscal situation has become. We have a trifecta of surging debt, massive deficits, and declining federal revenue. The chart below provides a visual perspective – and it doesn’t even account for the last few years.

This relentless increase in debt is happening when the economy is supposedly strong. Typically, a strong economy generates more tax revenue, and deficits shrink. But this isn’t really a strong economy. It is a house of cards built on debt. Fiscal stimulus is helping to prop it up.

That means there is no end in sight to this upward-spiraling national debt.

The biggest issue is the federal government spending addiction. In August alone, the Biden administration spent over $527 billion.

In fact, the US can’t even afford the interest on the debt.

Uncle Sam’s interest expense is already rising at an astronomical rate, and it’s set to explode.

The federal government has paid well over half a trillion dollars ($630 billion) on interest payments alone in fiscal 2023, with one month left to go. Interest on the debt paid in July exceeded the amount spent on national defense that month. Uncle Sam is well on the way to spending more on interest payments than any line item other than Social Security and Medicare.

The average interest rate on the debt is now at the highest level since 2011, coming in at 2.92% as of the end of August. But that’s still relatively low, and the debt is more than double what it was back in the good ol’ days of 2011.

Meanwhile, the average interest rate is poised to climb rapidly. A lot of the debt currently on the books was financed at very low rates before the Federal Reserve started its hiking cycle. Every month, some of that super-low-yielding paper matures and has to be replaced by bonds yielding much higher rates. That means interest payments will quickly climb much higher unless rates fall.

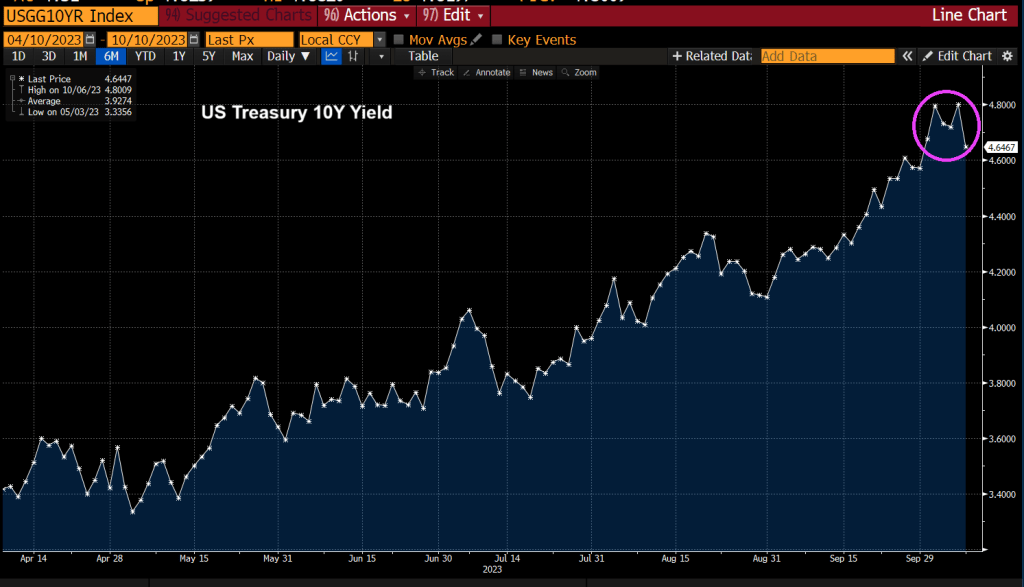

To give you an idea of where we’re heading, T-bills currently yield about 5.5%, the two-year yield is over 5% and the 10-year currently yields around 4.7%.

This has driven interest payments as a percentage of total tax receipts to over 35%. In other words, the government is already paying more than a third of the taxes it collects on interest expense.

If interest rates remain elevated, or continue rising, interest expenses could climb rapidly into the top three federal expenses. (You can read a more in-depth analysis of the national debt HERE.)

People tend to yawn at the ever-increasing national debt, but it is a ticking time bomb. Who knows how much time is left, but the timer is ticking relentlessly toward zero.

Like President Biden enjoying a barbeque at The White House with a live band (probably NOT Justin Moore singing “Small Town USA”) while Hamas declared war on Israel and Americans are being held hostage with the promise of public executions of hostages livestreamed. Nothing that “Empathy Joe” does ever surprises me anymore, but I am surprise that various Federal Reserve Presidents will speak today while Hamas terrorizes Israeli and US citizens.

It could be that investors think that Talking Heads at The Fed will claim that Fed rate increases are over. Then again, the Iran/Hamas terror campaign against Israel is spookking markets, driving up oil and gold prices and driving up “flight to safety” in US Treasuries.

President Biden called on Americans in Israel to book a commercial flight home, even though Israel has cancelled all flights. Does Old Joe even read the news??

Joe Biden, who has always been a compulsive liar but at least sounded cognicent, is now babbling and whispering that Bidenomics works. But for who?

Clearly not for first time homebuyers or people looking to move. Bankrate’s 30-year mortgage rate is up to almost 8%, the highest since July 2000 and Willy Slick Clinton. That is a 176% increase in mortgage rates under the most inept “Economic Sheriff” in history.

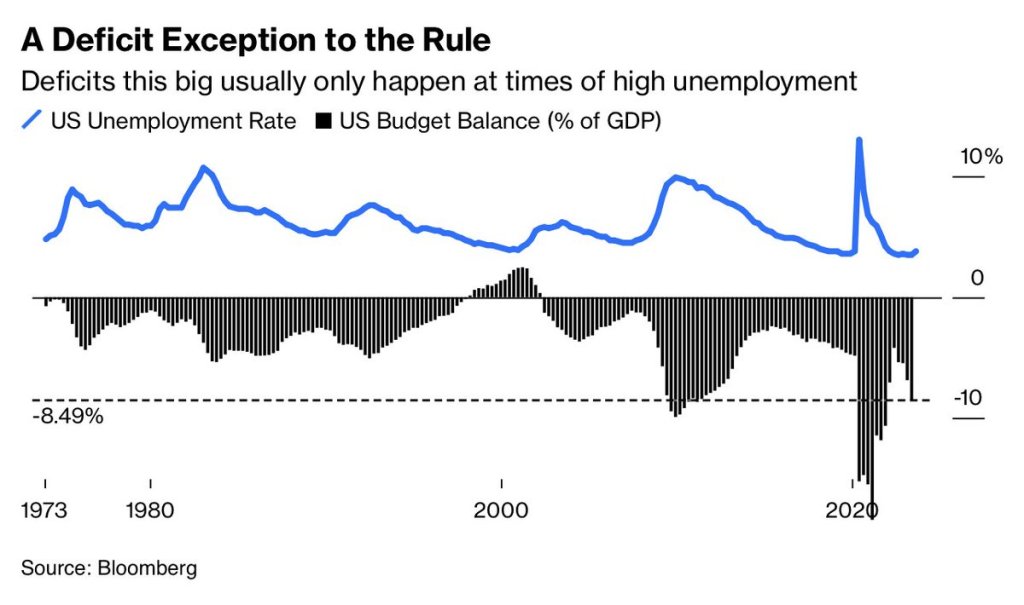

Deficits? Deficits (which Biden makes outlandish claims) are usually only this big at times of HIGH unemployment and recessions. So, are the staggering deficits under Biden a precursor to a hard landing (recession)? Don’t listen to what Biden or KJP say!!!

Biden’s outlandish claims that he single handedly reduced the deficit by the most in history is, well, typical Biden bloviating. Actually, tax receipts soared after Covid lockdowns ended. Period. Now that stimulus is wearing out, deficits are climbing again.

As Biden sleeps through the Hamas invasion of Israel, that is nothing new. Biden is sleeping through a disastrous downturn in the economy and pretending that Bidenomics is working. It isn’t Joe!

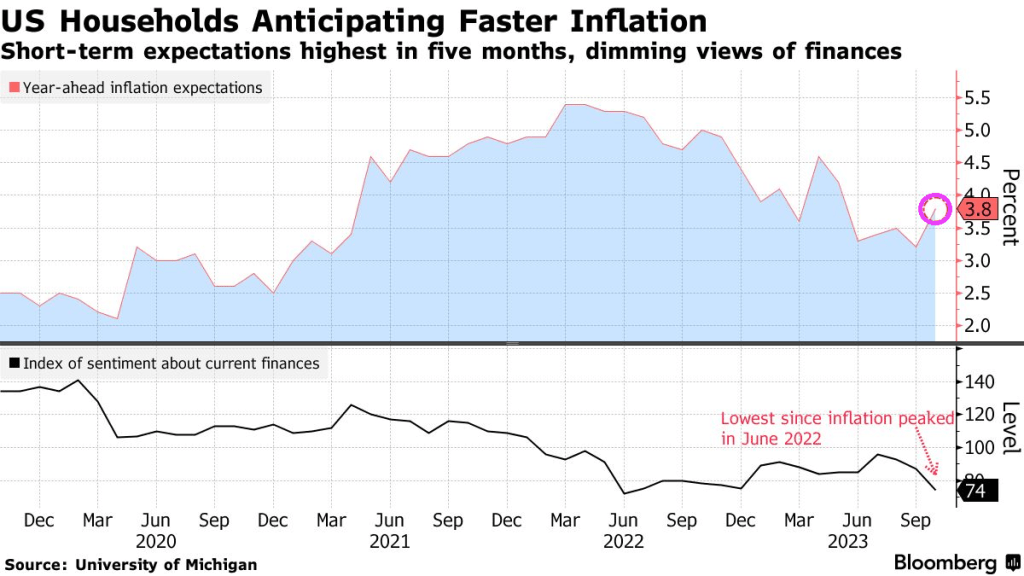

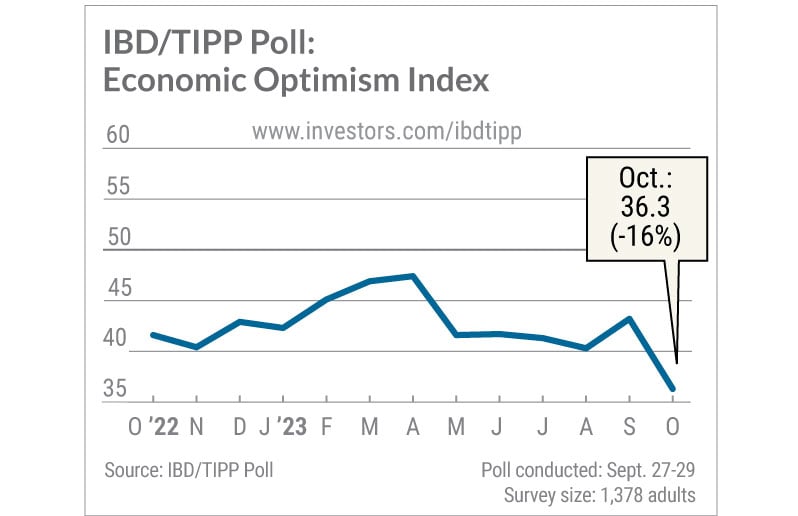

The IBD/TIPP U.S. Economic Optimism Index sank to a 12-year low in October as confidence in the near-term economic outlook crashed to the lowest level in the poll’s history. The survey casts doubt on the Federal Reserve’s justification for turning more hawkish last month: robust consumer spending.

The overall IBD/TIPP U.S. Economic Optimism Index dived 6.9 points to 36.3, the lowest since August 2011. Readings below the neutral 50 level reflect pessimism. The 6-month economic outlook index cratered 9.6 points to 28.7, a record low since the IBD/TIPP Poll began in early 2001.

That means the outlook suddenly appears worse than it was at the depths of the dot-com crash, the great financial crisis and the coronavirus pandemic.

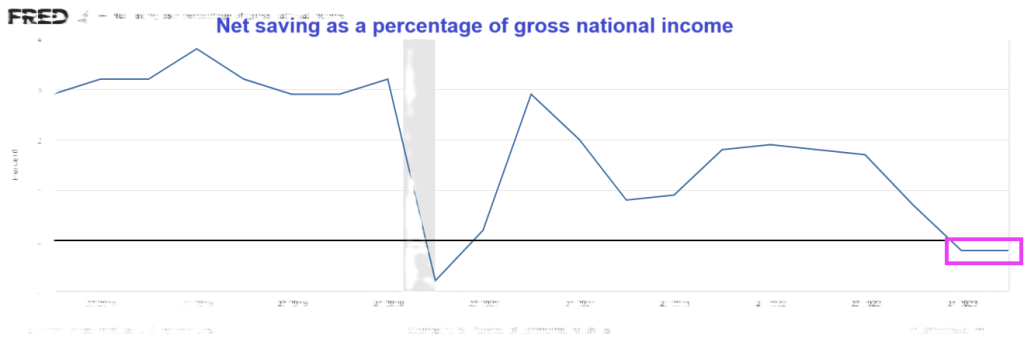

And on the personal savings front, net savings as a percentage of gross national income was negative for the second straight quarter.

Sleepy Joe, wake up! The US economy is slowing down REALLY fast!

Hey Bartender! The leading employment gain under Bidenomics was … low paying leisure and hospitality jobs at 96k jobs added.

The US added a whopping 336K jobs, the highest monthly increase since January. This is surprising given that the ADP report was so weak.

And the BLS decided to UPWARD revised past numbers. The BLS revised not only August but also July higher: the change in total nonfarm payroll employment for July was revised up by 79,000, from +157,000 to +236,000, and the change for August was revised up by 40,000, from +187,000 to +227,000. With these revisions, employment in July and August combined is 119,000 higher than previously reported.

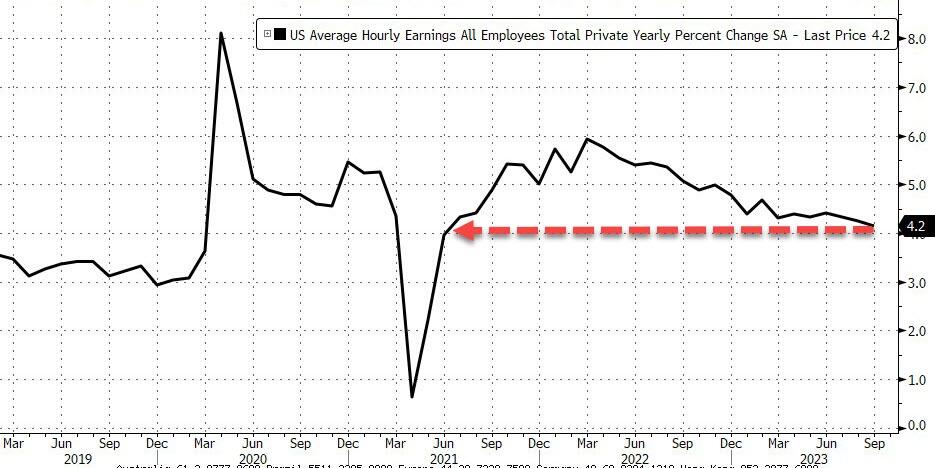

Meanwhile wage growth continued to cool, and in September average hourly earnings increased 0.2%, below the 0.3% expected, and resulted in a 4.2% increase YoY, down from 4.3% in August…

… as a result of a big bump in lower paying jobs.

But perhaps the most remarkable divergence in the report is that with headline payrolls surging 336K (establishment survey), the Household Survey indicated that the pain continues, as the number of people employed not only rose by less than 100K (86K to be precise), but it was all part-time workers, which increased by 151K. Full-time workers? Why, they dropped by 22K, and the lowest since February.

Leisure and hospitality added 96,000 jobs in September, above the average monthly gain of 61,000 over the prior 12 months.

But the jobs report highlights Bidenomics. Lots of government jobs and the private sector getting crushed. +1 million government jobs, -400K non-government.

Hmm. How will The Federal Reserve view this report? Focus on the red-hot headline gain of 336k job added or the fact that it is mostly part-time jobs added? Odds of a rate HIKE rise to 44% after September jobs report and Fed PAUSE expectations have been extended.

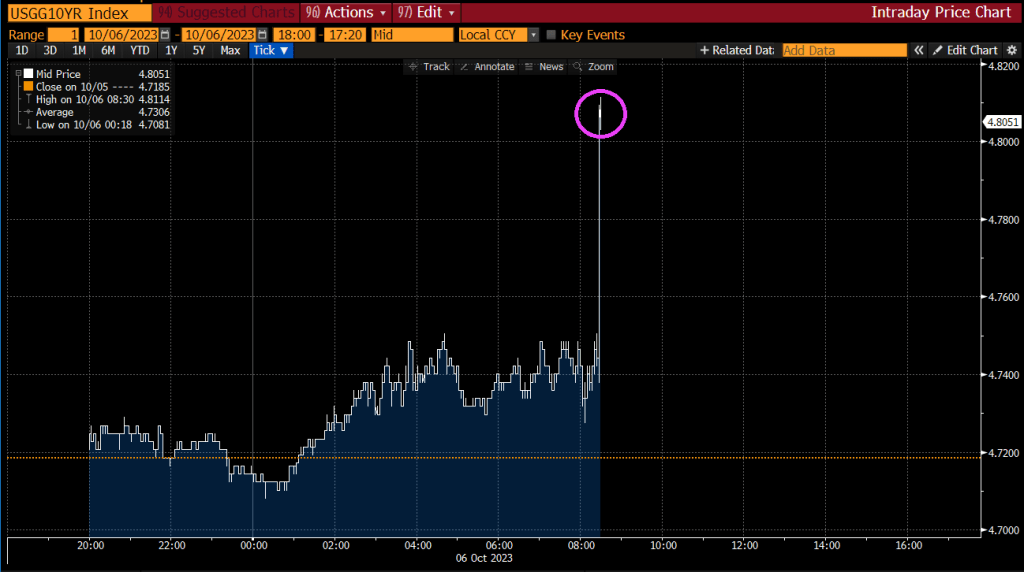

After the jobs report, the US Treasury 10Y yield soared.

The 10-year Treasury yield has risen dramatically under Biden’s Reign of (Economic) Error.

The Fed erroneously does not consider rising home prices as inflation. Here’s the result in pictures.

Case-Shiller national and 10-city home prices vs CPI, Rent, and Owners’ Equivalent Rent

Chart Note

Case-Shiller measures repeat sales of the same home over time. This ensures an accurate comparison of room size, yard size, and amenities. The only drawback is the data lags a bit. The most current data is from July representing transactions in May and June.

OER stands for Owners’ Equivalent Rent. It’s the price of rent one would pay to rent one’s own house, unfurnished without utilities.

For 12 years, home prices, OER, Rent, and the overall CPI all rose together. That changed in 2000 with another trendline touch in 2012. Then it was off to the races as the Fed did round after round of QE, suppressing mortgage rates.

Case-Shiller Home Price vs Hourly Earnings, the CPI, and Rent

Case-Shiller national home prices vs CPI, Rent, and Average Hourly Earnings.

As with the previous chart, for 12 years, home prices, rent, the overall CPI and hourly earnings all rose together. That changed in 2000 with another trendline touch in 2012.

How Much Are Homes Overpriced?

If the 12-year trend of home prices rising with average hourly earnings stayed intact, the home price index would be 211, not 308.

From that we can calculate home prices are ((308-211) / 211) percent too high, roughly 46 percent too high. If you prefer, home prices would need to fall ((308-211) / 308), roughly 31 percent.

Alternatively, if home prices stagnate for years, wages may eventually catch up.

Case-Shiller Home Price 1988=$150,000

The same home that cost $150,000 in 1988 now costs $678,366. But wages have gone up too. And mortgage rates have had wild swings.

Mortgage Payment and Wage Adjusted Mortgage Payment

The Least Affordable Mortgages in History

Factoring in wage growth, home prices, and mortgage rates, homes are the most expensive ever.

It’s actually much worse than the chart indicates because property taxes and insurance are not factored into.

Mortgage Rates

Mortgage Rate chart courtesy of Mortgage News Daily.

Through massive and totally unwarranted QE, foolishly hoping to create more inflation, the Fed suppressed interest rates to record lows and mortgage rates followed.

Anyone with an an existing mortgage could and did refinance at 3.00 percent or below.

This increased “affordability” and we now have two classes of people courtesy of the Fed: winners and losers (existing home owners who refinanced low and those who want to buy).

“Mortgage rates continued to move higher last week as markets digested the recent upswing in Treasury yields. Rates for all mortgage products increased, with the 30-year fixed mortgage rate increasing for the fourth consecutive week, up to and above 7.53 percent – the highest rate since 2000,” said Joel Kan, MBA’s Vice President and Deputy Chief Economist. “As a result, mortgage applications ground to a halt, dropping to the lowest level since 1996.The purchase market slowed to the lowest level of activity since 1995, as the rapid rise in rates pushed an increasing number of potential homebuyers out of the market. ARM loan applications picked up over the week and the ARM share increased to 8 percent, as some borrowers searched for ways to lower their payments.”

What About the Winners?

Good question. The winners refinanced at 3.0 percent or below. This put extra money in their pockets every month to spend.

And rising wages further stimulated ability of the winners to buy goods and services.

Thus the Fed is still paying for its asinine push to create inflation.

Meanwhile, the housing market is dead and will remain dead with mortgage rates approaching 8.00 percent.

What About Rent?

CPI data from the BLS, chart by Mish.

That’s another good question. For 24 months or so, economists have been predicting an ease in rent inflations.

The price of gasoline rose 10.6 percent, rent another 0.5 percent, shelter, 0.3 percent, and new cars 0.3 percent leading the way for a 0.6 percent increase in the CPI in August.

The price of rent has gone up at least 0.4 percent for 25 straight months. Not to worry, Paul Krugman says this is lagging.

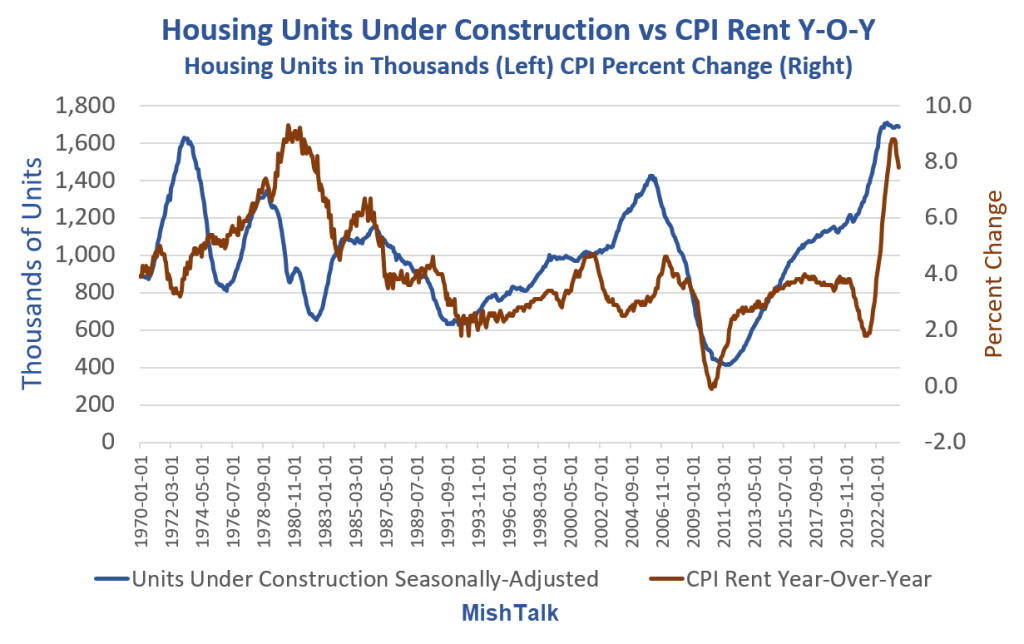

When Will Record Housing Units Under Construction Ease Rent Inflation?

That’s really a trick question. For a better question, remove the lead “when” from the sentence.

The answer is: I don’t know, nor does anyone else, although people claim to be clairvoyant.

Housing Units Under Construction vs CPI Rent Year-Over-Year

Housing units from Census Department, Rent CPI from BLS, chart By Mish

I saw the theory that rent would collapse as soon as housing units get completed so many times that I almost started believing it myself.

However, the data shows no discernable correlation no matter how you shift the lead or lag times.

The chart looks totally random. So perhaps rent abate. Perhaps not. The data itself provides no reason to believe anything.

Regardless, please note the floor. Year-over-year rent has a floor of about 2 percent except in the Great Recession housing crash.

And these charts are not imputed Owner’s Equivalent Rent prices for which people pay no actual rent. These charts reflect rent of primary residence.

34 Percent are Screwed

Well, don’t worry. Only 34 percent of the nation rents, and besides, rent is lagging.

Sarcasm aside, the Fed blew huge asset bubbles and did not see that as inflation. Nor did the Fed see that three massive rounds of fiscal stimulus would cause inflation.

Real Income and Spending Billions of Chained Dollars

Note the three rounds of massive fiscal stimulus in the Covid pandemic. This triggered the most inflation since the 1970s. Economists debate how much “excess savings” still remains.

The Fed never saw this coming, never saw a housing bubble in 2007, and has never once predicted a recession.

Heck, former Fed chair Ben Bernanke denied a housing bubble and denied a severe recession that had already started.

Expect More Inflation Everywhere

Unfortunately, Biden is doing everything humanly possible to stoke inflation with EV mandates, natural gas mandates, union pandering, student debt forgiveness, and regulations, some of which is blatantly unconstitutional.

If you are looking to buy your first home and need to finance, good luck.

The longer the Fed holds rates high, the longer the housing transaction crash lasts. But cutting rates will further expand the housing bubble, asset bubbles in general. And bubbles are destabilizing.

That is the Fed’s tightrope dilemma, of its own making.

If you are one of the winners, congrats. But that extra money the Fed put in your pocket every month may stoke inflation for a long time.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.