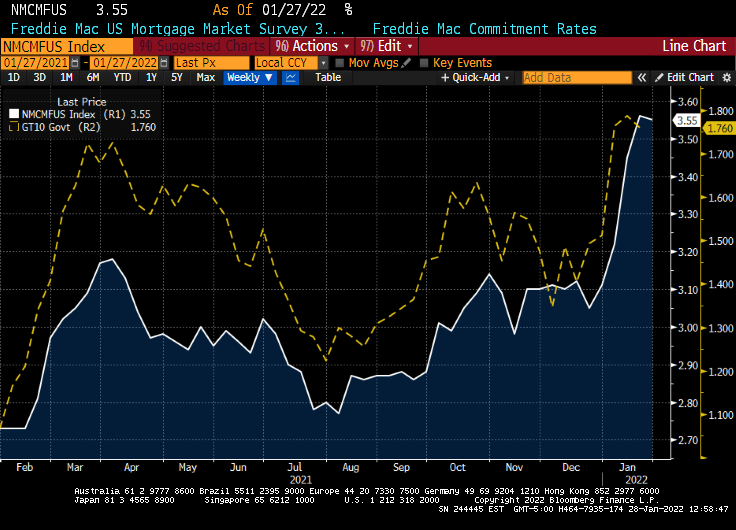

US 30-year mortgage rates are up 100 basis points and climbing since January 4, 2021. Most of the increase has occurred since the turn of the year into 2022. According to the Bankrate 30-year mortgage rate index, the 30-year rate is up 57 basis points just since December 31, 2021 as the benchmark 10-year Treasury yield rises.

Bear in mind that the REAL 30-year mortgage rate is now -3.2%. Get it while you can!!

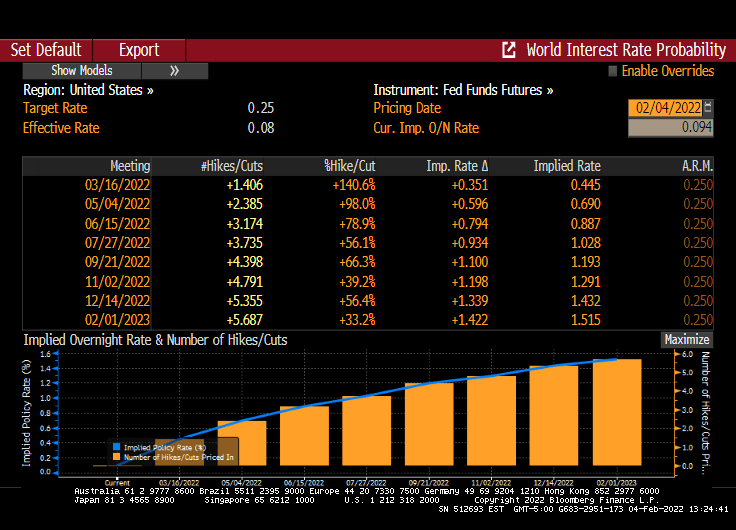

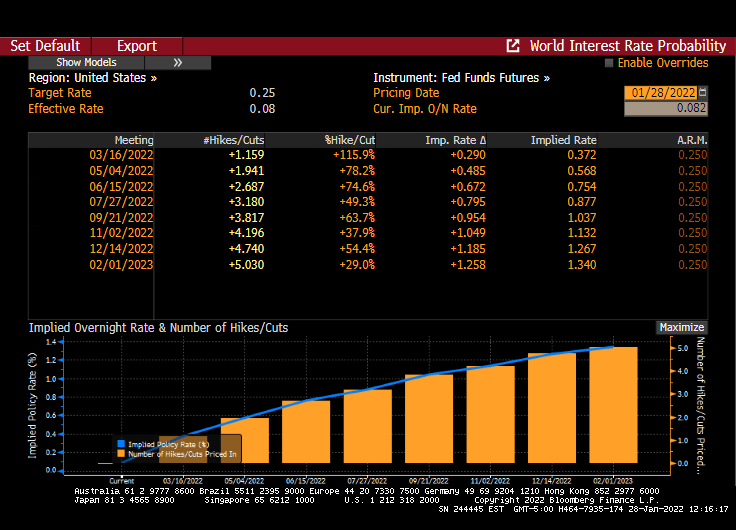

Given today’s surprise jobs report, The Fed now has a green light to raise rates.

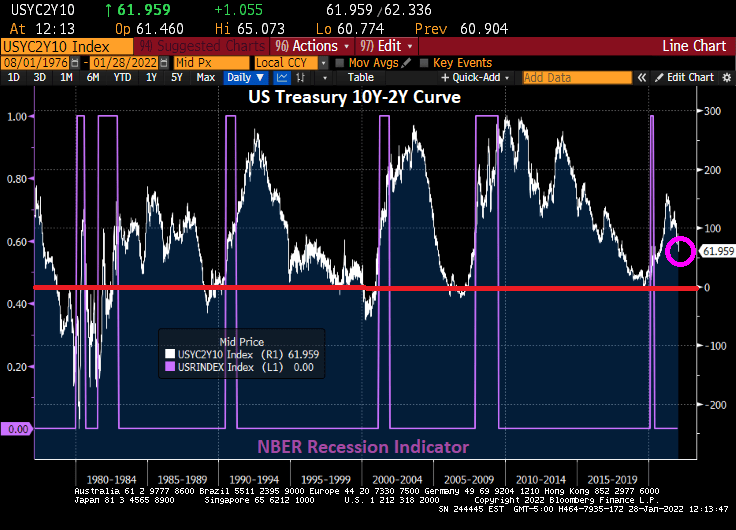

No, not the Klaus von Bulow type of “reversal of fortune” (when he killed his wife). I am talking about a reversal in fortune for America.

Let’s look at the 10Y-2Y Treasury curve. It typically falls below 0 basis points before every recession. Except the mini-COVID recession of 2020. But notice that the Treasury curve did not recover from the COVID recession as it typically did. More along the lines of 1984-1985.

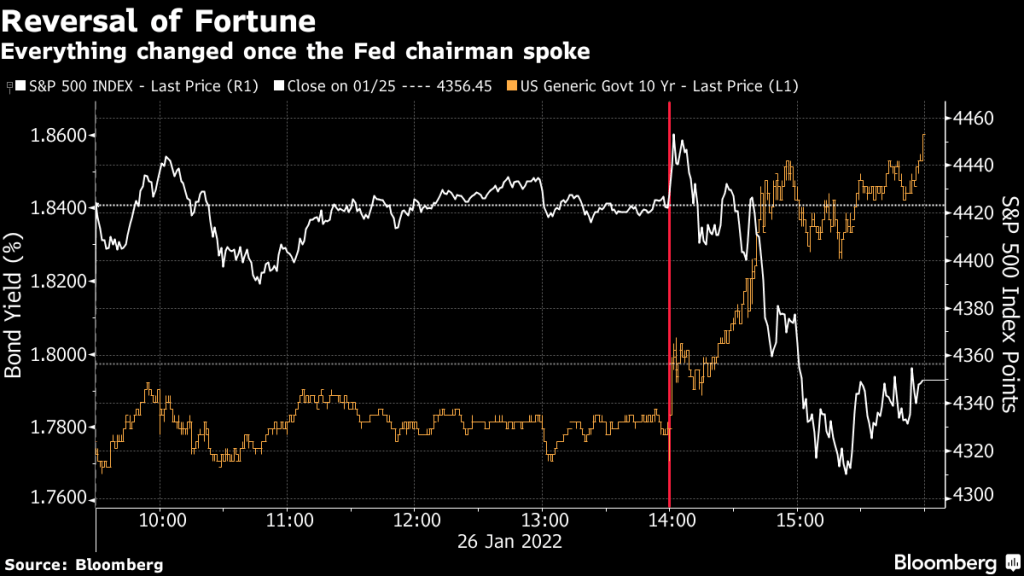

Speaking of Reversal of Fortune, everything changed once Fed Chair Powell started to speak after Tuesday’s FOMC meeting.

Hmm. Midterm elections, possible Russian invasion of The Ukraine, further problems in China, etc. While The Fed Funds Future data implies that The Fed may raise their target rate 5 times over the coming year, we’ll see.

If 2021 was a great year for the US housing market, 2022 faces “a new normal” marked by a slowing down of home price rises, job layoffs in the mortgage industry, and concerns over rising inflation and interest rate hikes, according to Douglas Duncan (pictured), Fannie Mae’s senior vice president and chief economist.

Duncan said “a shift” was underway in the market and the wider economy, which would result in far more moderate home price appreciation, expected to be between 7% and 7.5% this year due to the ending of fiscal and monetary stimulus.

“One of the elements of the shift is that you’re going to see house prices up, but not nearly as far as they were in the last two years because that was driven hugely by the fiscal and monetary stimulus (now) being removed,” he told MPA.

Ominously, he added that low interest rates “may never be seen again”. Or at least until Biden appoints more doves to The Federal Reserve Board of Governors.

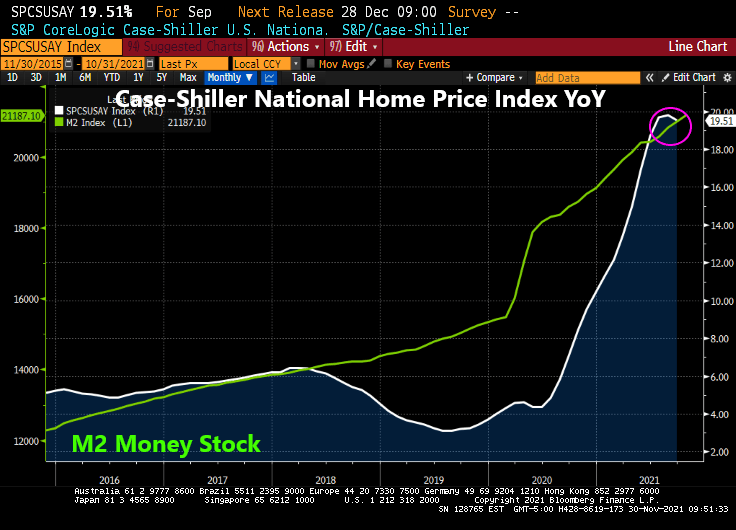

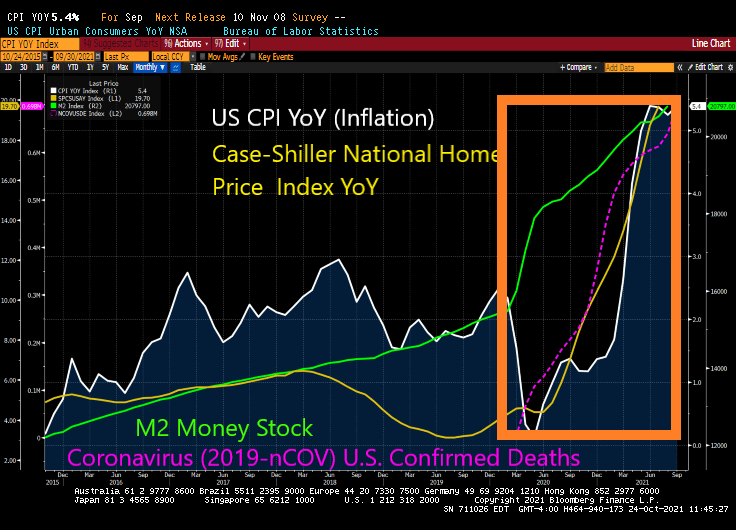

Once again, low available inventory of houses for sale coupled with outlandish Fed stimulus has resulted in a housing crisis where home price growth (+19.51%) exceeds hourly wage growth (+5.76%) by almost 4x.

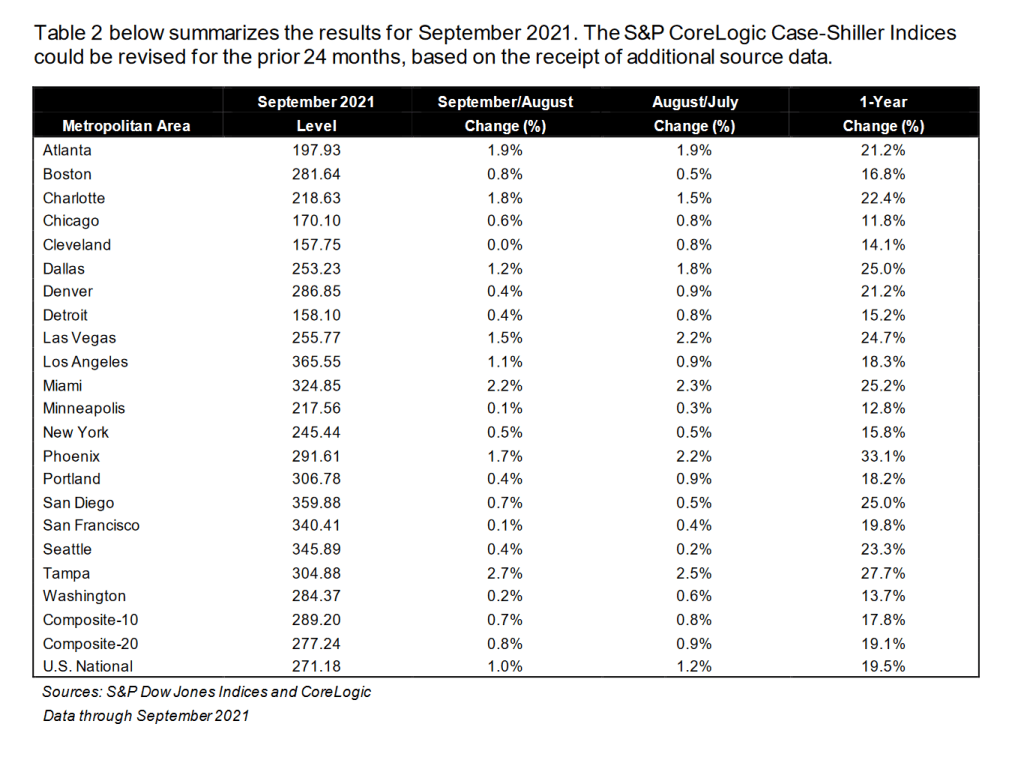

Where are all the home prices above 10% YoY? Every one of the 20 metro areas covered by Case-Shiller. Phoenix AZ leads at +33.1%. Chicago IL is the “slowest” at 11.8%.

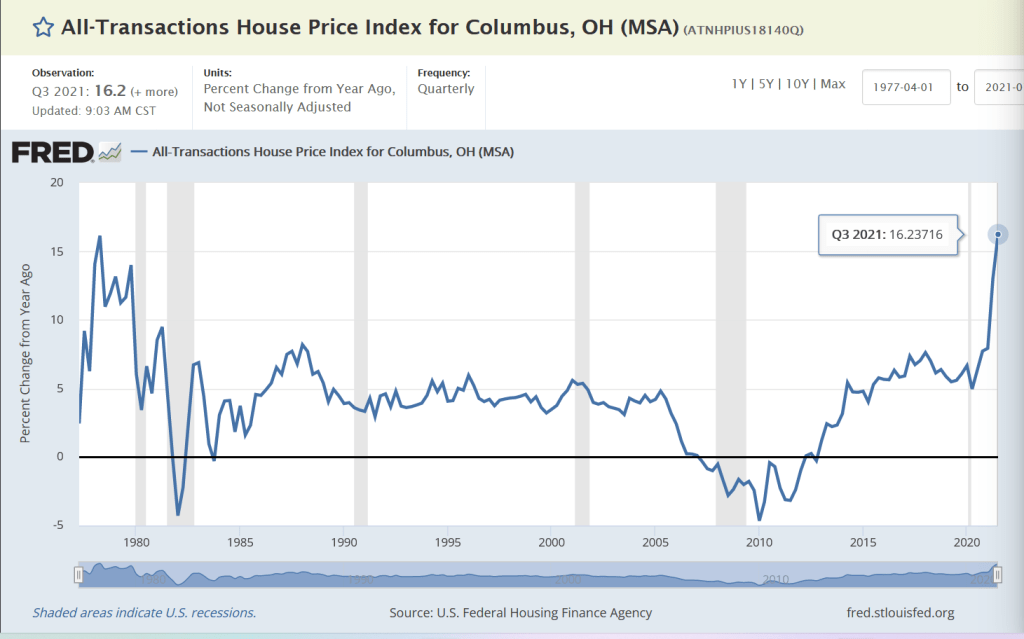

Although Columbus OH is the growth hub of the state, Case-Shiller only reports Cleveland. So here is Columbus’s all-transactions home price growth for Q3: +16.2% YoY placing Columbus at the top of the midwest metro areas of Detroit, Chicago, Minneapolis and Cleveland.

With the latest Omicron Variation (sounds like a Star Trek TV show episode), I will bet that The Fed will stay a little longer and keep rates low, leading to home price growth (with limited available inventory) to continue to grow at double digit speeds.

The Federal Reserve is helping to create inflation, particularly since their unorthodox surge in money supply around the Covid outbreak in early 2020. Home prices as of the latest Case-Shiller report are rising at nearly 20% year-over-year.

To add to the problem of The Fed’s overzealous money printing we have The Biden Administration (and puppy-torturer/killer Anthony Fauci) issuing Covid vaccine edicts that are wreaking havoc in labor markets further clogging the economic pipelines.

Between The Fed ZIRP policies and Biden/Fauci’s vax mandates, we are starting to see the rise (again) of the infamous MORTGAGE TILT EFFECT!

The Tilt Effect comes about as expected inflation gets priced into mortgage rates, the mortgage payment rises as the mortgage rate rises (of course), but the higher mortgage payment occurs with EXPECTED inflation in the future.

But not quite yet. Despite CPI inflation growing at 5.4% YoY, Freddie Mac’s 30-year mortgage survey rate is only 3.01% … for now.

As inflation continues to rise (thanks to ongoing Fed ZIRP policies and governments mandating Covid vaccine in order to keep your job, we should eventually see mortgage rates rise … leading to a return of THE TILT EFFECT. Which in turns make housing even MORE unaffordable.

We have tried numerous mortgage contracts in the past (mostly to offset Carter-era inflation) such as the PLAM (price-level adjusted mortgage) and the GPM (graduated payment mortgage). Now we have the PLUM (price level unadjusted mortgage) which is subject to the TILT EFFECT.

Federal Reserve Chair Jerome Powell sounded a note of heightened concern over persistently high inflation as he made clear that the central bank will begin tapering its bond purchases shortly but remain patient on raising interest rates.

“The risks are clearly now to longer and more persistent bottlenecks, and thus to higher inflation,” Powell said Friday during a virtual panel discussion hosted by the South African Reserve Bank and moderated by Bloomberg’s Francine Lacqua.

“I would say our policy is well-positioned to manage a range of plausible outcomes,” he said. “I do think it’s time to taper and I don’t think it’s time to raise rates.”

Good luck with that, Jay! You are going to raise the short-end of the yield that will lead to a flattening of the Treasury yield curve. But you are going to continue to buy Treasuries and Agency MBS in order to monetize the rampant spending by Congress and the Biden Administration? C’mon man!

You can see where Powell spoke today. It is when gold tanked along with the 10-year Treasury yield. Both rebounded a bit, but the 10-year Treasury yield continue its fall to 1.6324%.

The US dollar (green) fell when Powell opened his pie-hole. But Bitcoin (blue) fell in advance as if they knew what Powell was going to say.

A national mortgage lender has just introduced a 105 Loan-to-value (LTV) ratio loan and a lowering of FICO scores from 660 to 620.

Now, the loan still requires 97% LTV with downpayment assistance and gift funds permitted to boost CLTV to 105%.

With The Fed helping to raise home prices at a whopping 20% YoY, …

lenders are trying to find loan products for lower-income households so they can get in on the bubble! Hence, a 105% CLTV mortgage product with reduced credit requirements and increased Debt-to-income requirement rising from 43% to 45%. Also, borrowers can avoid the 3% downpayment requirement and put down only $500.

This is lending into the storm: softening of underwriting requirements as the house price bubble surges. Sound like 2005. This was not supposed to happen. After the housing bubble burst and the financial crisis, The Fed was supposed to encourage counter-cyclical lending (tighten credit standards as a housing bubble worsens). Instead, lenders are lowering credit standards, feeding the house price bubble.

If this was just one lender, I would have barely noticed. But this mortgage is being offered by most banks. And then sold to our GSEs: Fannie Mae and Freddie Mac.

Speaking of lending into a storm, as part of the raft of new legislation designed to spur first-time homeownership in America, a remarkable bill has joined the fray: its sponsors propose creating a new subsdizied 20-year-fixed-rate mortgage program through Ginnie Mae, HousingWire reports.

According to the bill, Ginnie Mae in tandem with the Department of the Treasury would subsidize the interest rate and origination fees associated with these 20-year mortgages, so that the monthly payment would be in line with a new 30-year FHA-insured mortgage. The move – which is an explicit subsidy of one share of the population by another – could, in theory, “allow qualified homebuyers to build equity-and wealth- at twice the rate of a conventional 30-year mortgage.” Instead, what it will do is lead to is an even bigger housing bubble.

Phil Hall of Benzinga wrote a series of excellent articles in four parts for MortgageOrb (although “The Orb” has removed his name). Here are the links to his stories.

After re-reading these excellent articles on the housing bubble and crash, I thought I would take the opportunity to present a few charts to highlight the housing bubble, pre-crash and post-crash.

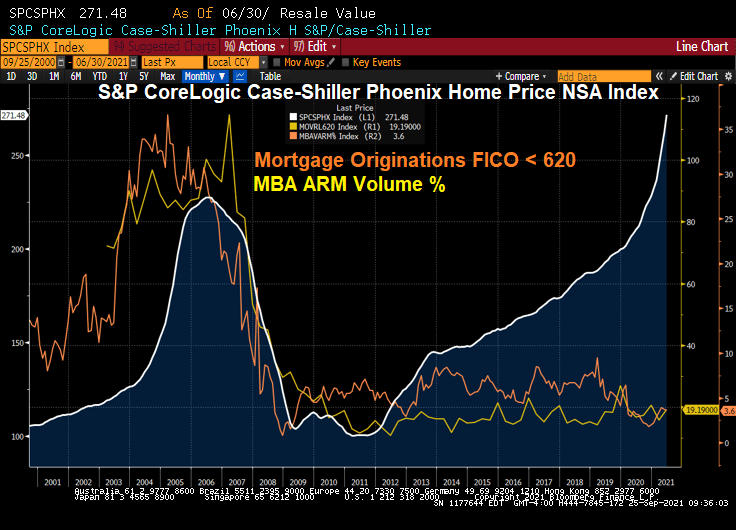

Here is a graph of Phoenix AZ home prices. Note the bubble that peaked in mid 2006. The Phoenix bubble correlates with the large volume of sub-620 FICO lending and Adjustable-rate mortgage (ARM) lending. Bear in mind, many of the ARMs prior to 2010 were NINJA (no income, no job) ARM loans.

What happened? Serious delinquenices at the national levels spiked as The Great Recession set in and unemployment spiked.

Since the housing bubble burst and surge in serious mortgage delinquencies, The Federal Reserve entered the economy with a vengeance. And have never left, and increased their drowning of markets with liquidity.

The Fed whip-sawing of interest rates in response to the 2001 recession was certainly a problem. They dropped The Fed Funds Target rate like a rock, then homebuilding went wild nationally and home prices soared thanks to Alt-A (NINJA) and ARM lending. But now The Fed is dominating markets like a gigantic T-Rex.

Oddly, then Fed Chair Ben Bernanke never saw the bubble coming. Or the burst.

Speaking of pizza, Donato’s from Columbus Ohio is my favorite. Founder’s Favorite is my favorite, but they do offer the dreaded Hawaiian pizza (ham, pineapple, almonds and … cinnamon?)

United Wholesale MortgageUWMC has announced plans to become the first national mortgage lender to accept cryptocurrency for home loans.

What Happened: CEO Mat Ishbia previewed the Pontiac, Michigan-based company’s expansion into the cryptocurrency realm during the second-quarter earnings call on Monday.

“We’ve evaluated the feasibility, and we’re looking forward to being the first mortgage company in America to accept cryptocurrency to satisfy mortgage payments,” Ishbia said. “That’s something that we’ve been working on, and we’re excited that hopefully, in Q3, we can actually execute on that before anyone in the country because we are a leader in technology and innovation.”

In an interview with the Detroit Free Press, Ishbia offered more details on which cryptocurrencies would be considered in transactions.

“I think we’re starting with Bitcoin, but we’re looking at Ethereum and others,” Ishbia said. “We’re going to walk before we run, but at the same time, we are definitely a leader in technology and innovation and we are always trying to be the best and the leader in everything we do.

“That’s the plan,” he added. “Obviously there’s no guarantees – we’re still working through some details. But absolutely.”

Why It Matters: One of the first homebuying deals in the U.S. involving cryptocurrency took place in 2014 with the $1.6 million sale of land in Lake Tahoe for a home site. The transaction was completed with payment via Bitcoin (CRYPTO: BTC).

However, the heavily regulated and risk-averse mortgage industry hasn’t embraced cryptocurrency. The government-sponsored enterprises that dominate the industry’s secondary market, Fannie MaeFNMA+ Free Alerts and Freddie MacFMCC+ Free Alerts, will not accept any transaction in a digital asset.

If UMC plans to package its cryptocurrency-based loans for secondary market sale, the borrower’s cryptocurrency payment would have to be converted into dollars and the borrower would need to provide documentation to verify ownership of the digital assets as part of the loan underwriting process.

You must be logged in to post a comment.