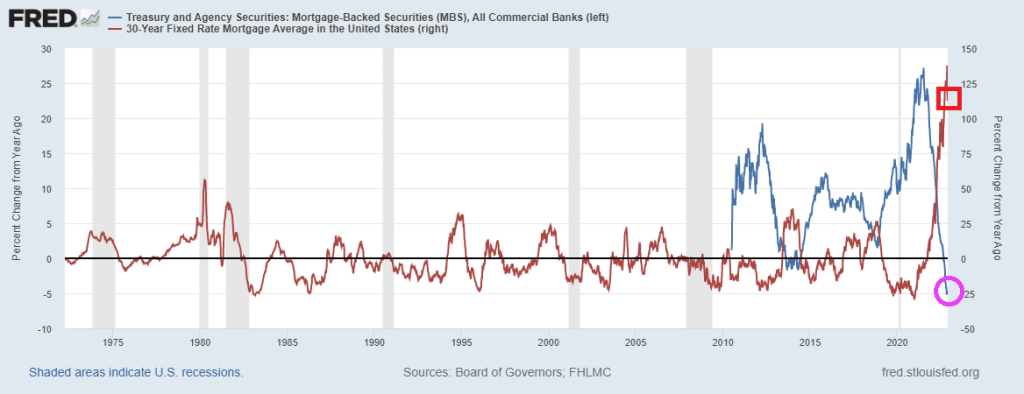

As The Federal Reserve continues its assault on inflation by raising their target rate, Blackstone Inc.’s $69 billion real estate fund for wealthy individuals said it will limit redemption requests, one of the most dramatic signs of a pullback at a top profit driver for the firm and a chilling indicator for the property industry.

Blackstone Real Estate Income Trust Inc. has been facing withdrawal requests exceeding its quarterly limit, a major test for the one of the private equity firm’s most ambitious efforts to reach individual investors. The news, in a letter Thursday, sent Blackstone stock falling as much as 10%, the biggest drop since March.

You can see the problem facing commercial real estate. Since December 31, 2021, NAREIT’s all-equity REIT index has fallen -23.6% while NAREIT’s mortgage REIT index has fallen -28.6%. It looks like Blackstone’s Real Estate Income Trust has a decline coming.

If I look at NCREIF’s commercial property index, we can see that The Fed helped boost CRE values. But what will happen if and when The Fed actually shrinks its balance sheet.

I call The Fed’s attempts at cooling inflation “Fed Dead Redemption” since it resulted in redemptions from real estate funds.

You must be logged in to post a comment.