Well, the Fed’s talking heads have been saying a 50 basis point hike was coming in May … and it appeared!

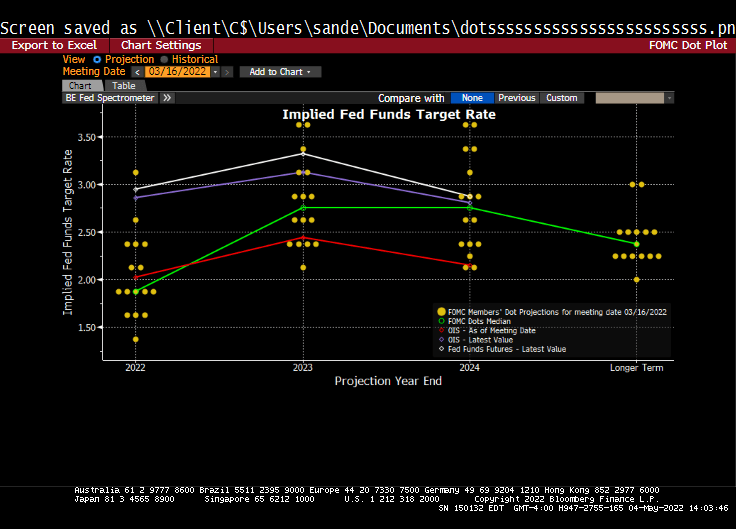

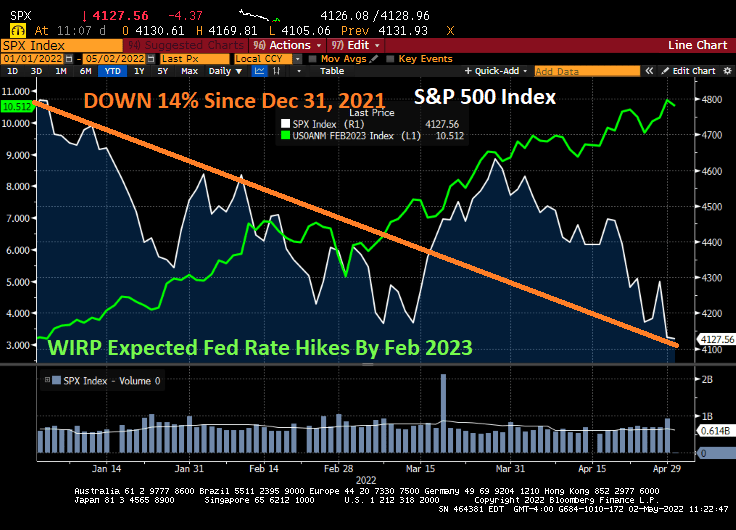

And it looks like 9 rate hikes are a comin’ by February 2023.

The Fed’s Dot Plots shows a cooling of Fed rate hikes by 2024 and beyond.

Here is the path of Balance Sheet peel-off.

The US Treasury actives curve is up by 14 bps at the 10-year tenor and up 17 bps at the 2-year tenor.

The plan will see $30 billion of Treasuries and $17.5 billion on mortgage-backed securities roll off. After three months, the cap for Treasuries will increase to $60 billion and $35 billion for mortgages.

I could read the Fed’s speech on their decision, but since The Fed has been so highly politicized, I don’t really care what they say. Only what they do.

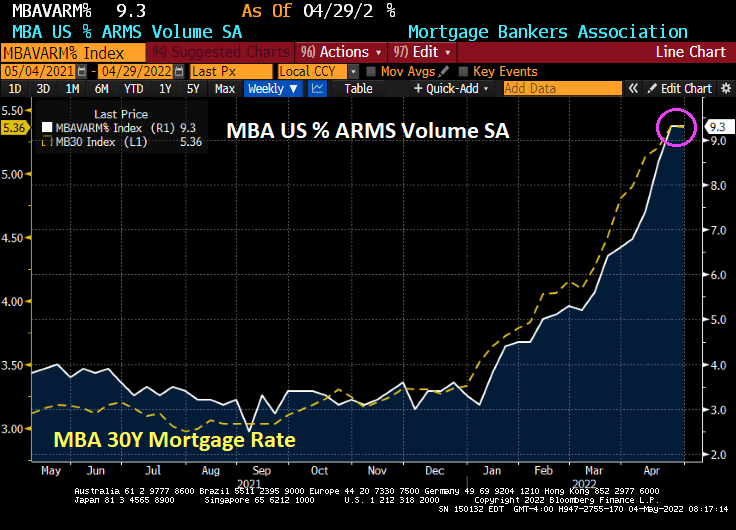

Simply unaffordable! US housing, that is. As The Federal Reserve tries to fight inflation caused by Biden’s Medusa-like policies, mortgage rates are soaring and we are seeing an INCREASE in mortgage purchase applications ahead of Fed tightening. Panic in (Fed) Needle Park!

Mortgage applications increased 2.5 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending April 29, 2022. The Refinance Index increased 0.2 percent from the previous week and was 71 percent lower than the same week one year ago.

The seasonally adjusted Purchase Index increased 4 percent from one week earlier. The unadjusted Purchase Index increased 5 percent compared with the previous week and was11 percent lower than the same week one year ago.

Adjustable rate mortgage (ARM) share has risen to 9.3% along with mortgage rates.

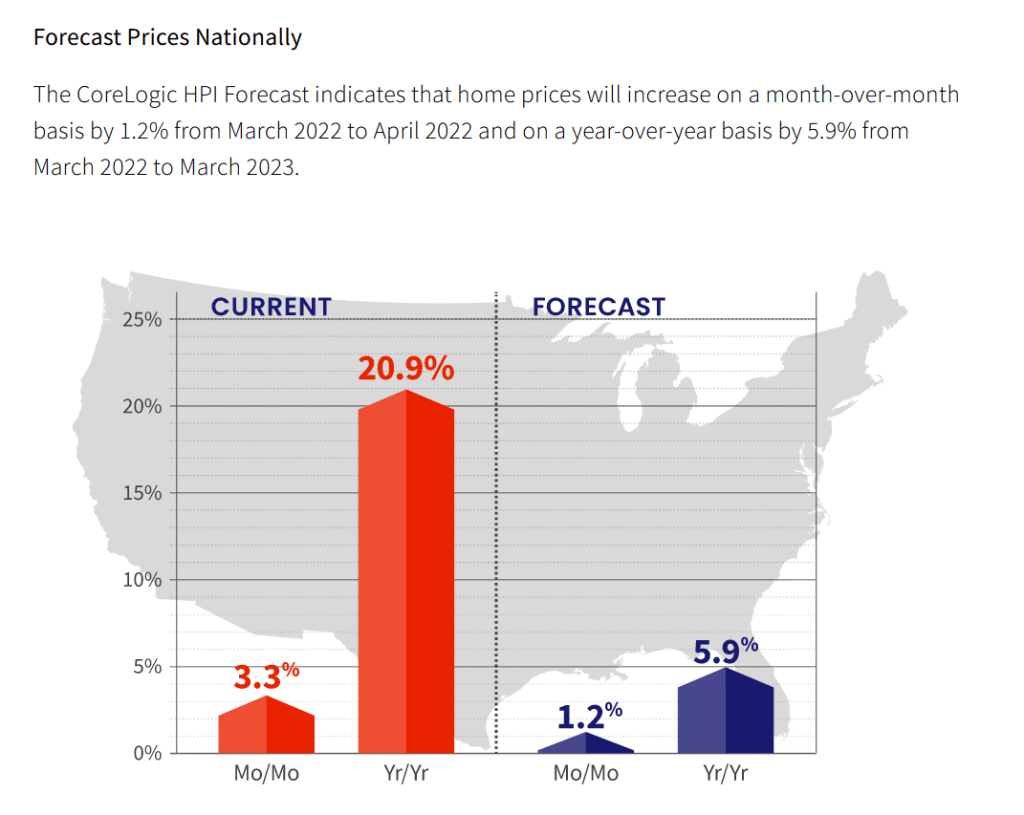

Between Biden’s energy policies, Congressional Covid relief and seemingly perpetual monetary stimulus from The Fed, we have 20% growth in home prices despite mortgage rates soaring.

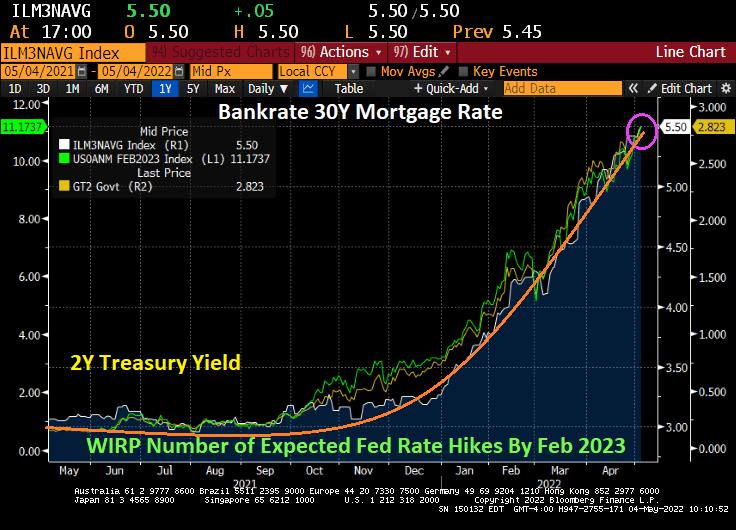

And as The Fed is expected to tighten, mortgage rates hit 5.50%.

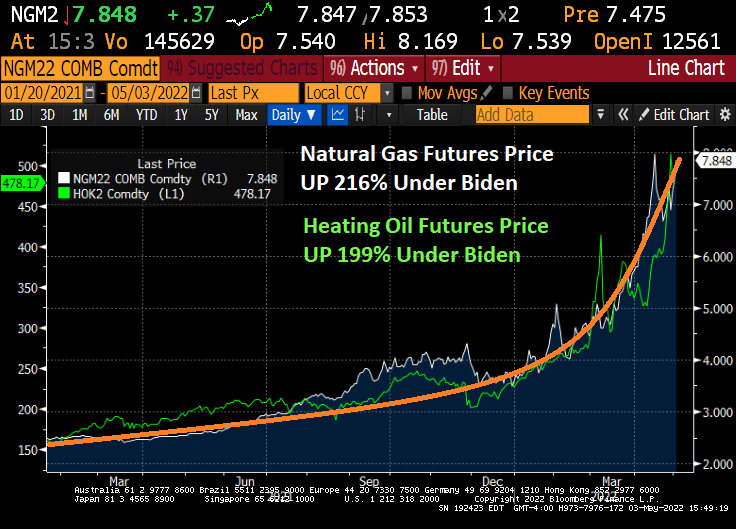

President Joe Biden should do an ad for his energy policies ala Game of Thrones, “Bundle up! Winter is Coming!”

Since Biden was installed as President in January 2021, natural gas futures prices are UP 216% and heating oil is up 199%.

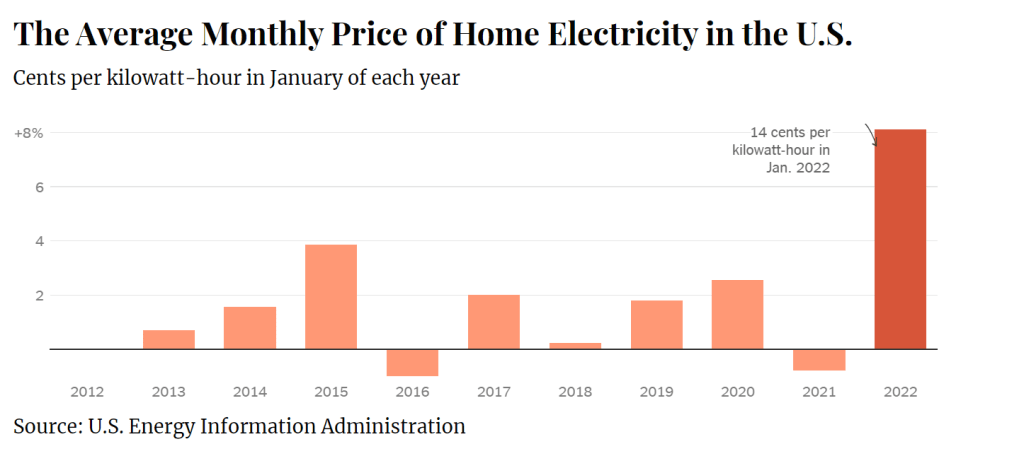

The average price of home electricity has SOARED under Biden, as has the prices of many things.

Fortunately for Biden and Congress, they live in well-heated (and air-conditioned) digs in the DC area and are not exposed to the damage done by Biden’s executive orders on energy.

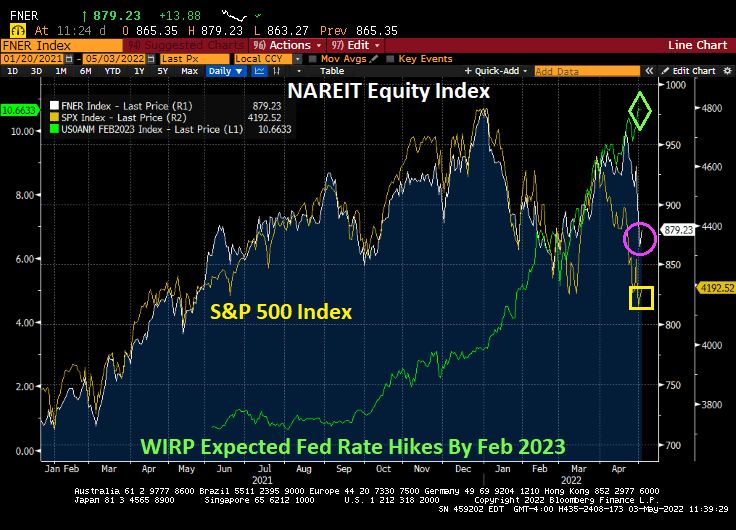

As The Federal Reserve seems hellbent on raising interest rates to fight the rapid increases caused by Biden’s follicies, we see the S&P 500 index taking a hit in 2022, but NAREIT’s all equity index as well.

An example of how a REIT can be impacted by The Fed is the Industrial REIT index that tanked with Amazon’s declining earnings prospects.

While industrial REITs is a broad category, Amazon’s crashing EPS has certainly shocked the market.

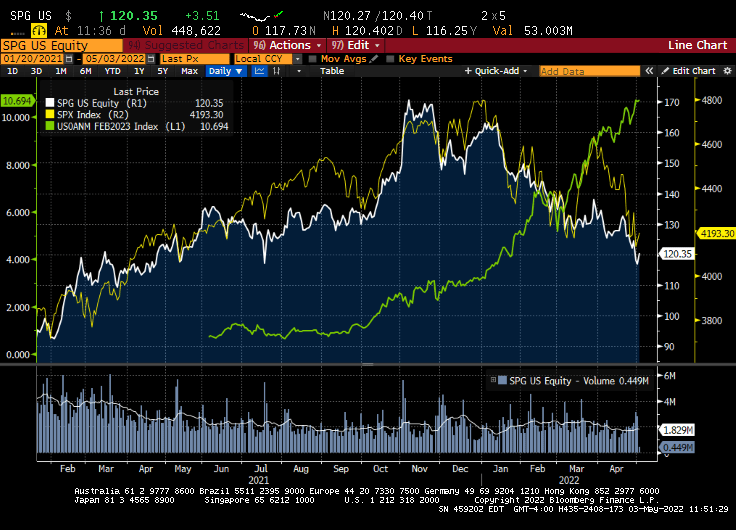

Retail REITs? How about Simon Properties? Simon Properties, a large mall REIT, go “Fauci’d” as the Covid economic shutdown really caused pain for shopping malls. Simon’s occupancy rate has increased as the economy opens back up (we hope).

Meanwhile, Simon Properties equity has declined along with the S&P 500 index as The Fed raises rates. In other words, both the S&P 500 and shopping mall REITs are getting “Fauci’d” by The Fed. Or Powell’d.

The U.S. Treasury market is showing signs of stress that may have implications for whether the curve keeps steepening.

Over the past month the curve has retraced from an inversion to a steepening driven by a surge in yields on benchmark 10-year bonds. That has led to interesting outlier indications, as traders weigh the outlook for Federal Reserve interest rate increases and inflation.

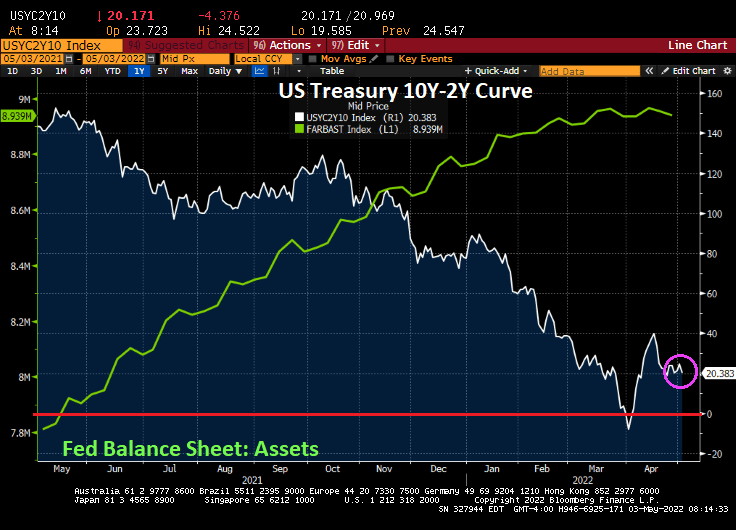

The US Treasury yield curve has settled-in at 20.383 bps (effectively zero) as The Fed continues its war on inflation.

On the SOFR front, we see SOFR Coupons being slow to benefits from Fed rate hikes. So, SOFR Coupons are behaving like Stouffer’s lasagna, frozen and tasteless.

On the other hand, mortgage rates continue to soar on EXPECTATIONS of Fed rate hikes.

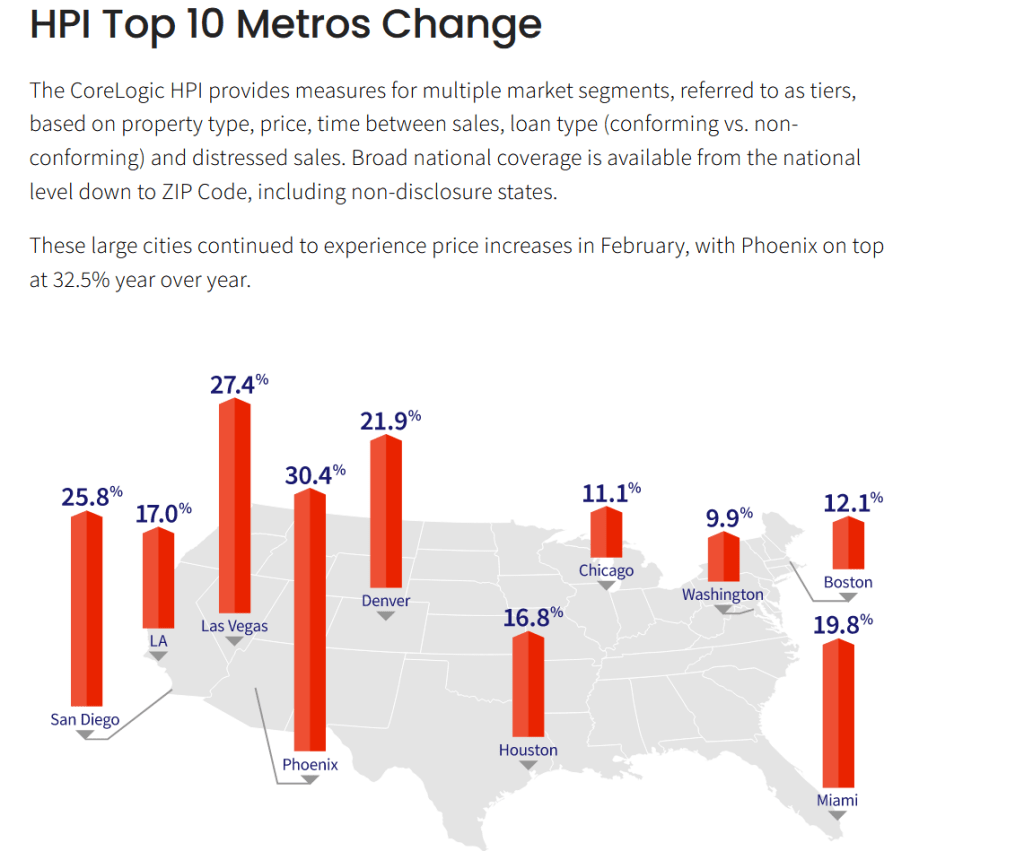

Phoenix AZ leads the top ten at 30.4% with Washington DC lagging at 9.9%.

So, its official. The Federal Reserve is best exemplified by former Yankee/Mets first baseman “Marvelous” Marv Throneberry. When players presented Mets’ manager Casey Stengel with a birthday cake but neglected to give piece of cake to Throneberry, Stengel replied to Throneberry when asked why no cake, “Because I was afraid your were going to drop it.”

Just like The Federal Reserve, the honorary Marv Throneberry of the the global economy.

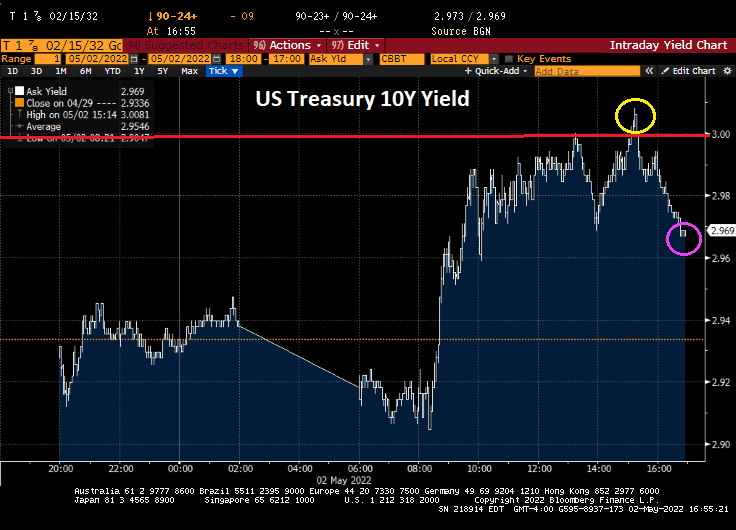

Today we saw the 10-year Treasury Note yield break through the 3% barrier, then retreat as is there was a reflecting barrier at 3%.

And in Europe, we saw a flash crash allegedly caused by Citi’s trading desk.

The selloff was triggered by a large erroneous transaction made by the U.S. bank’s London trading desk, according to people with knowledge of the matter who asked not to be identified discussing private information. A knee-jerk selloff in OMX Stockholm 30 Index in five minutes wreaked havoc in bourses stretching from Paris to Warsaw toppling the main European index by as much as 3% and wiping out 300 billion euros ($315 billion) at one point.

The US Dollar rose again as expectations of Fed monetary tightening due to inflation become a reality.

A measure of U.S. manufacturing activity unexpectedly dropped in April to the lowest level since 2020 as growth in orders, production and employment softened.

The Institute for Supply Management’s gauge of factory activity fell to 55.4 last month from 57.1, according to data released Monday. The Manufacturing Prices index remained elevated.

As the 10-year Treasury yield tries to breech the 3% barrier.

And as The Fed continues to threaten tightening of their monetary follicies, the S&P 500 index is down 14% since Dec 31, 2021.

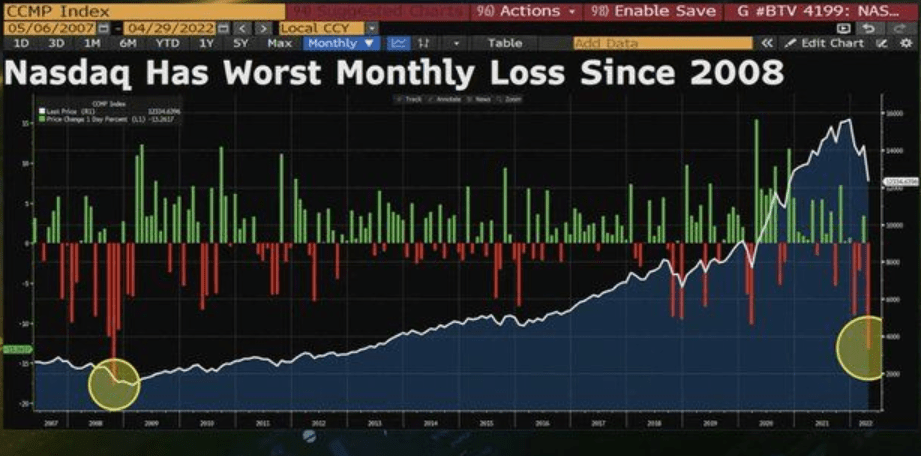

And the NASDAQ had it worst monthly loss since 2008.

We now have the proverbial double whammy happening … soaring home prices AND soaring mortgage rates.

The theory is, of course, that The Federal Reserve will slowly remove its staggering monetary stimulus leftover from 1) the financial crisis of 2008 and 2) the Covid recession of 2020. As you can see, the sheer volume of monetary stimulus remains outstanding and it is the EXPECTATIONS of The Fed tightening that is caused the 30-year mortgage rate to rise.

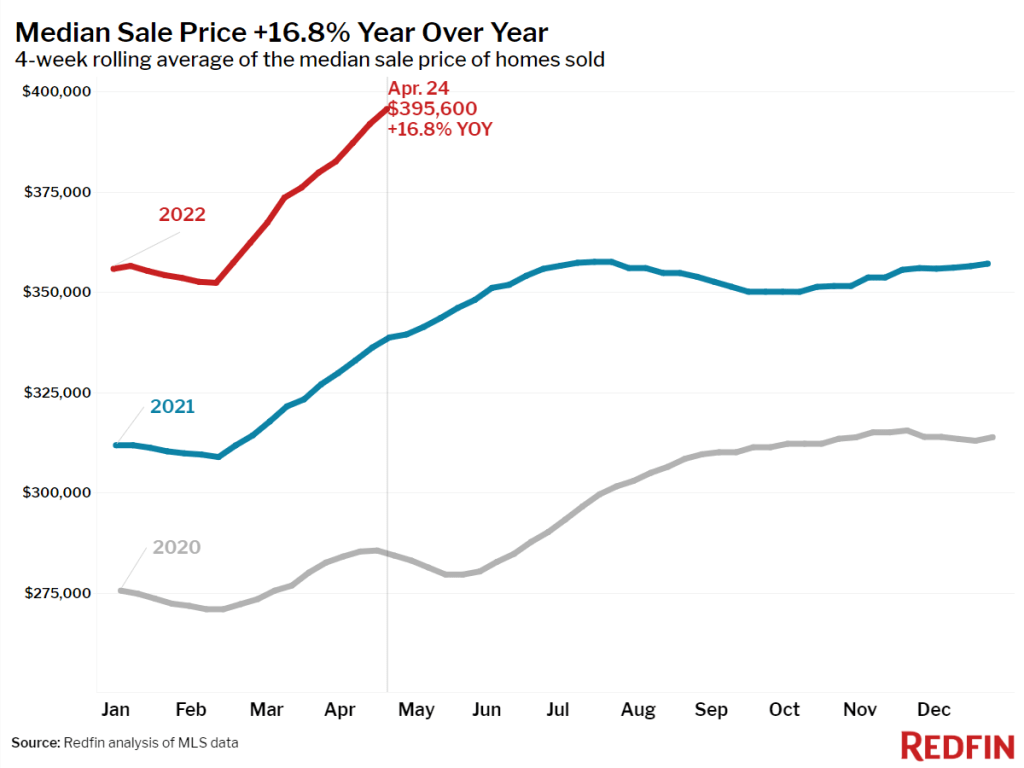

While I used the Case-Shiller National Home Price Index YoY, Redfin shows more contemporaneous home price data with April 24 median home sales price at 16.8%.

Thanks to The Fed, we are seeing homebuyer mortgage payments are up 39.4% YoY.

As inflation continues to damage America’s middle-class and low- wage workers, we may see regulations going into effect from the Consumer Financial Protection Bureau protecting consumers from … themselves.

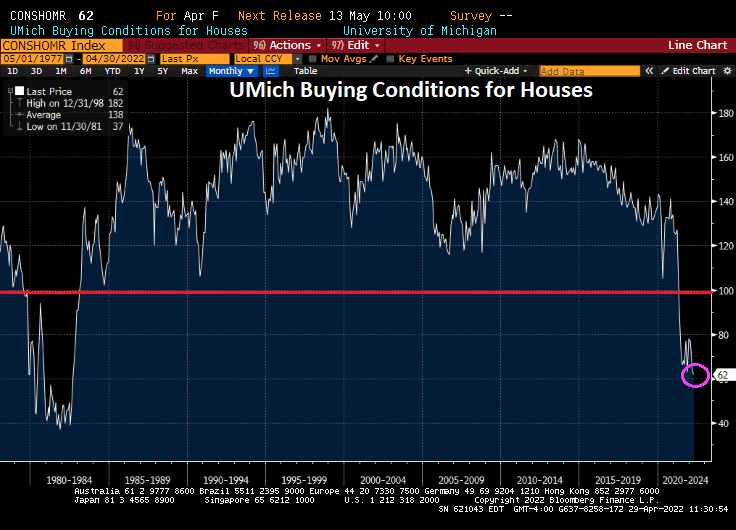

Rising home prices and The Fed signaling an end to the perpetual punch bowl have resulted in the University of Michigan buying conditions for houses to hit the lowest level since 1982.

While bearish sentiment in markets highest since 2009 in the stock market.

I don’t get why Biden created a “Disinformation Control Board” led by Nina Jankowicz – a disinformation spewer. We already have disinformation media outlets like CNN, MSNBC, ABC, CBS, NBC, New York Times, Washington Post, etc., so why create a Federal control board? All in time for the midyear elections!!

If this move by Biden doesn’t terrify you, then you didn’t study history.

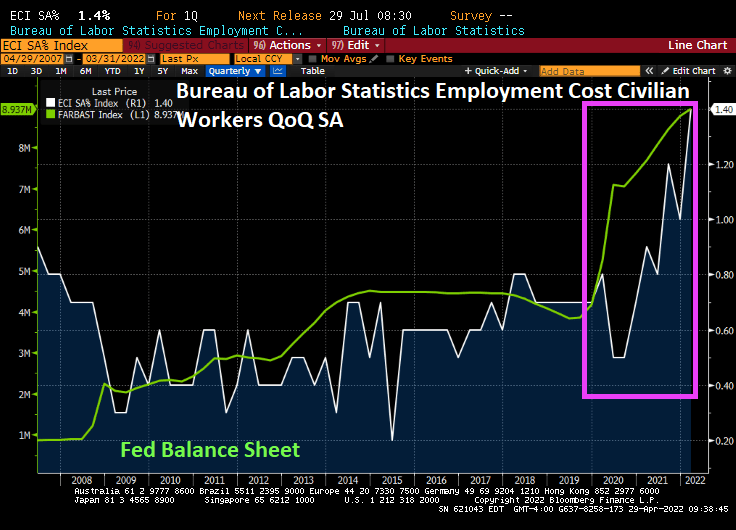

Not only has The Federal Reserve driven M2 Money Velocity to near historic lows, but now we find out that the Employment Cost Index just rose to a historic high.

Of course, a variety of minimum wage laws have helped drive up employments costs. Don’t tell lawmakers that minimum wage laws lead to higher inflation since they typically deny responsibility for anything. But I can almost picture the 4 Horsemen of the Inflation Apocalypse (Powell, Biden, Pelosi, Schumer) sitting around asking “What we can do to make inflation worse?”

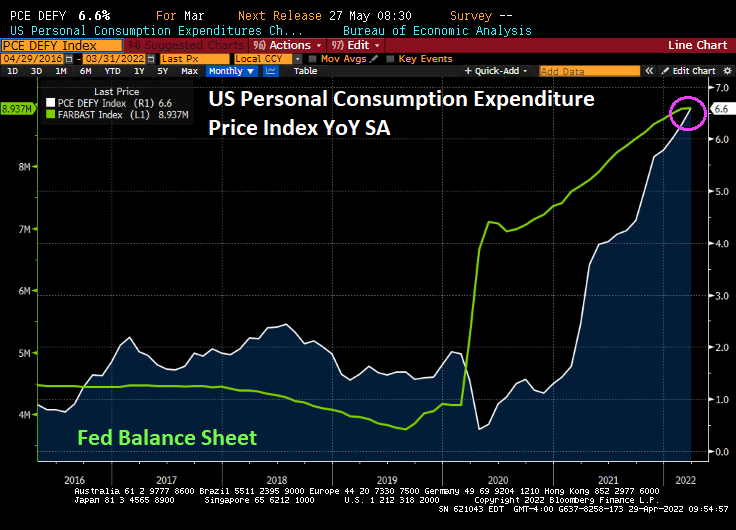

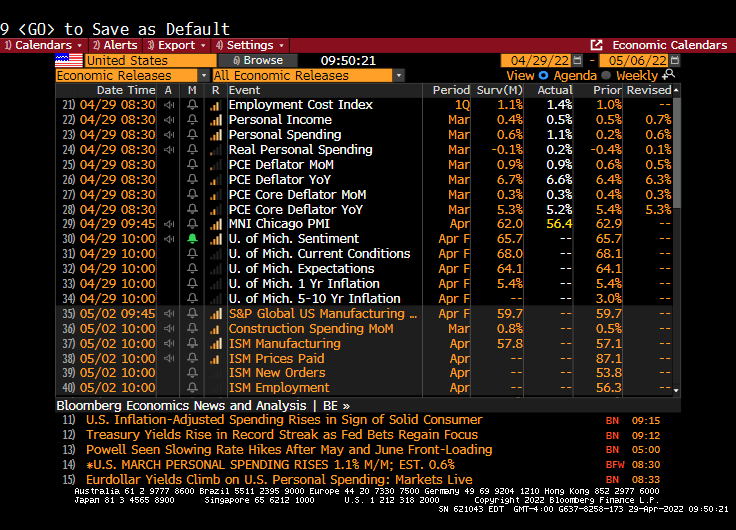

We did see the PCE Deflator YoY rise to 6.6%, the highest since 1982, the highest in 40 years.

Personal spending increased to 1.1% in March, probably panicking buying over further inflation.

A PCE Deflator of 6.60% leads to a Taylor Rule estimate of 9.05% for The Fed Funds Target Rate.

You must be logged in to post a comment.