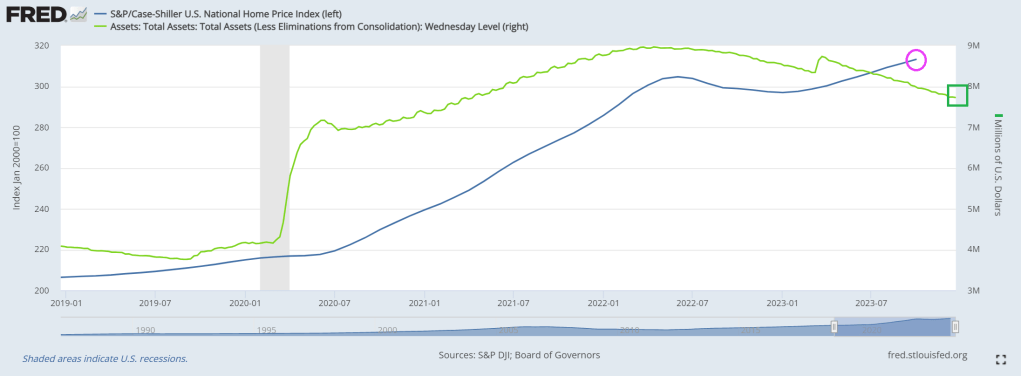

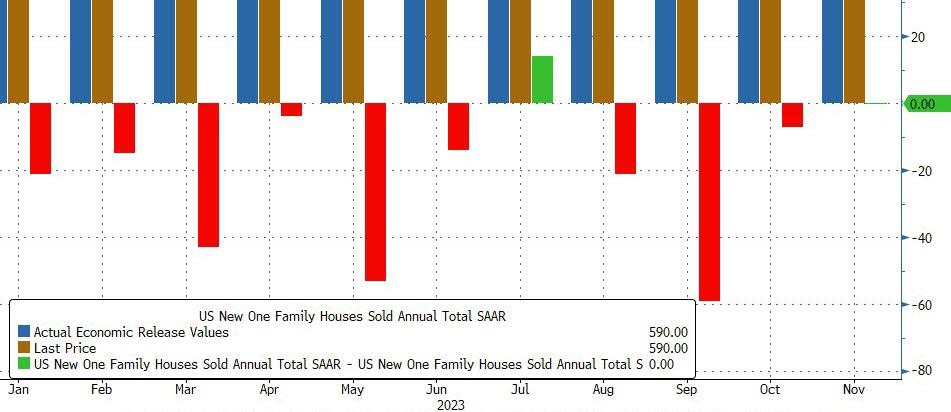

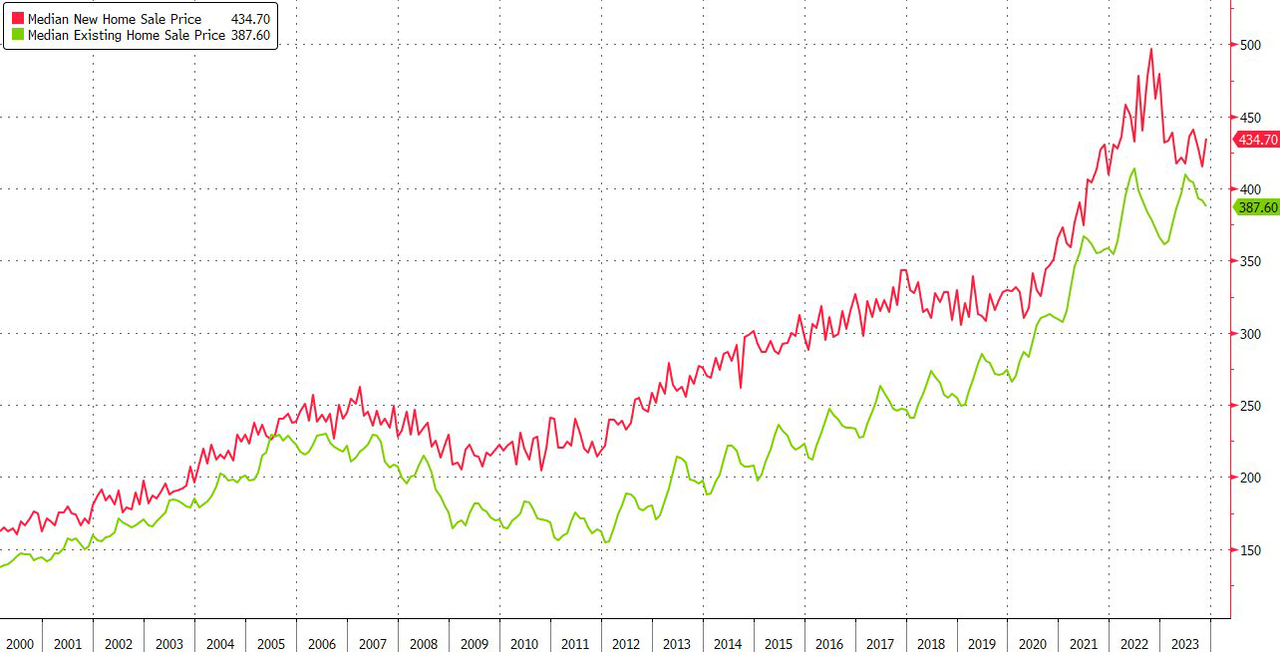

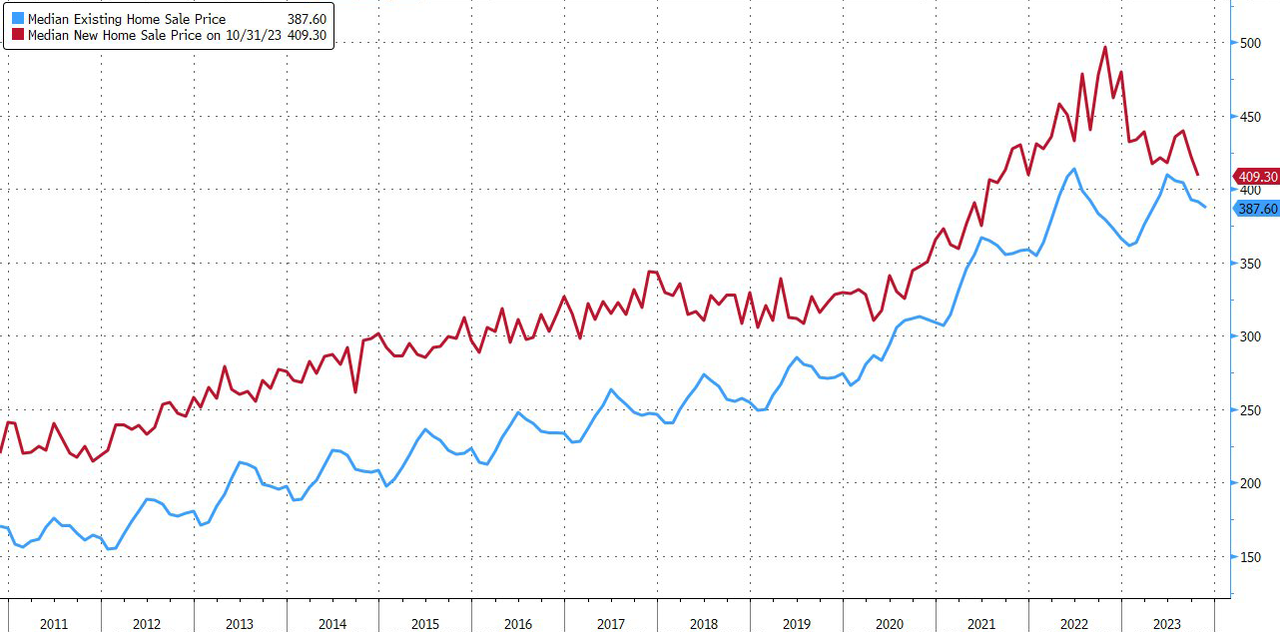

So much for “The Fed killed inflation” narrative. Inflation is still alive and well in housing prices. Particularly in cities like Miami and Detroit? Maybe the Lions winning their division for the first time in 30 years helped!

The S&P CoreLogic Case-Shiller U.S. National Home Price NSA Index, covering all nine U.S. census divisions, reported a 4.8% annual change in October, up from a 4% change in the previous month. The 10-City Composite showed an increase of 5.7%, up from a 4.8% increase in the previous month. The 20-City Composite posted a year-over-year increase of 4.9%, up from a 3.9% increase in the previous month. Detroit reported the highest year-over-year gain among the 20 cities with an 8.1% increase in October, followed again by San Diego with a 7.2% increase. Portland fell 0.6% and remained the only city reporting lower prices in October versus a year ago.

The Case-Shiller National Home Price index was up 4.8% in October as The Federal Reserve keeps its monstrous foot on the balance sheet pedal.

Home prices in America’s 20 largest cities rose for the 9th straight month in October (the latest data released by S&P Global Case-Shiller today), up 0.64% MoM (slightly better than the +0.60% MoM expected).

That pushed the YoY rise in prices up 4.87% – the fastest pace since Dec ’22…

…but as the chart shows the MoM gains are slowing rapidly.

“U.S. home prices accelerated at their fastest annual rate of the year in October”, says Brian D. Luke, Head of Commodities, Real & Digital assets at S&P DJI.

“We are experiencing broad based home price appreciation across the country, with steady gains seen in nineteen of twenty cities.”

Miami and Detroit saw the biggest MoM gains while the West Coast dominated the MoM price declines with San Francisco, Portland, and Seattle worst.

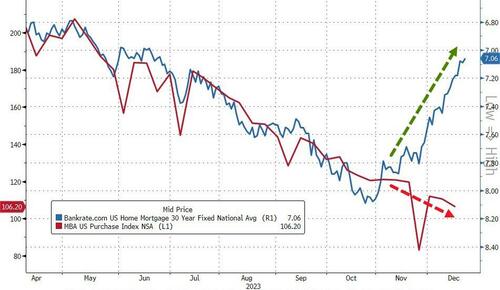

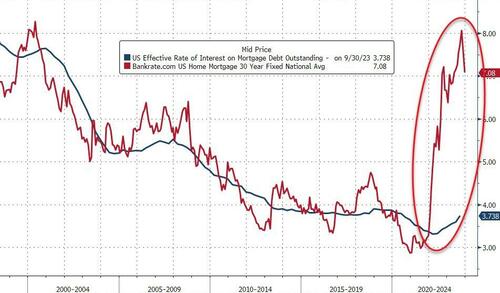

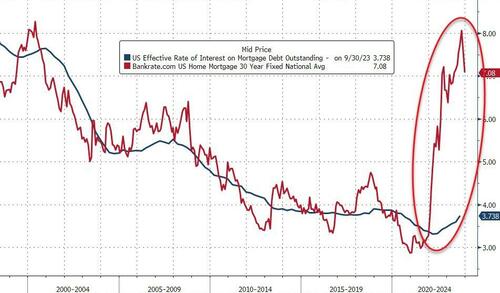

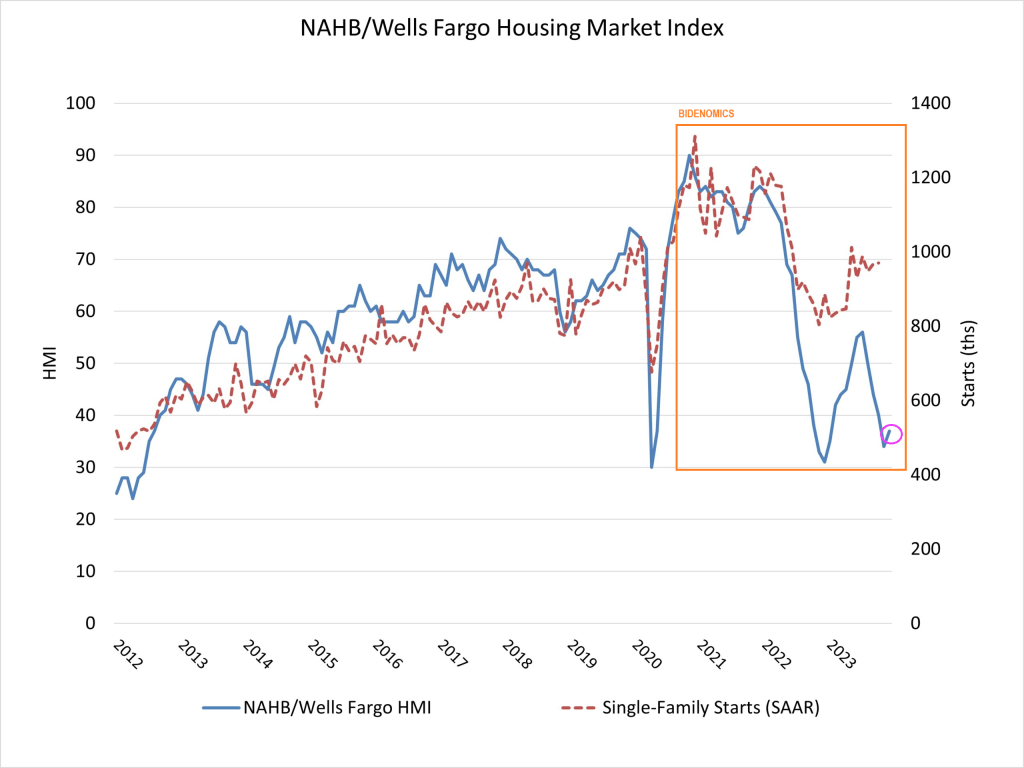

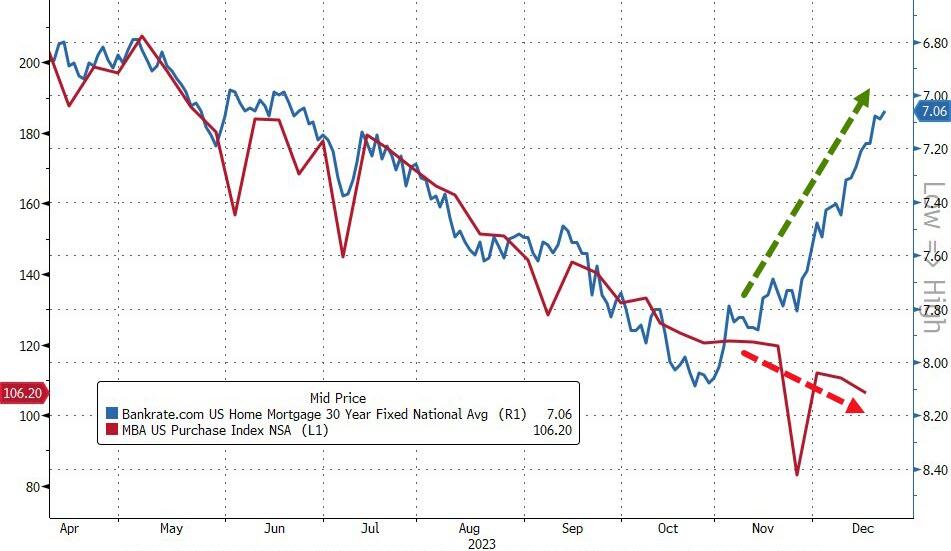

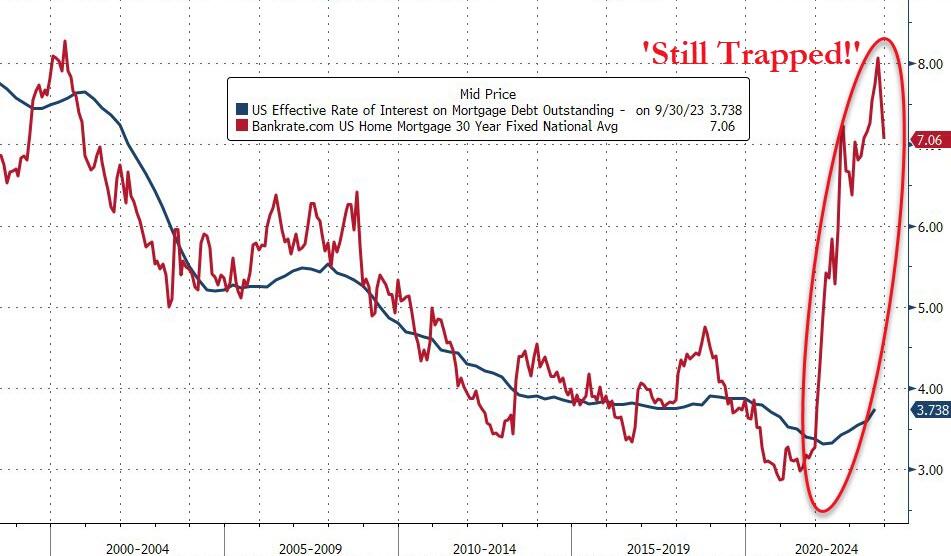

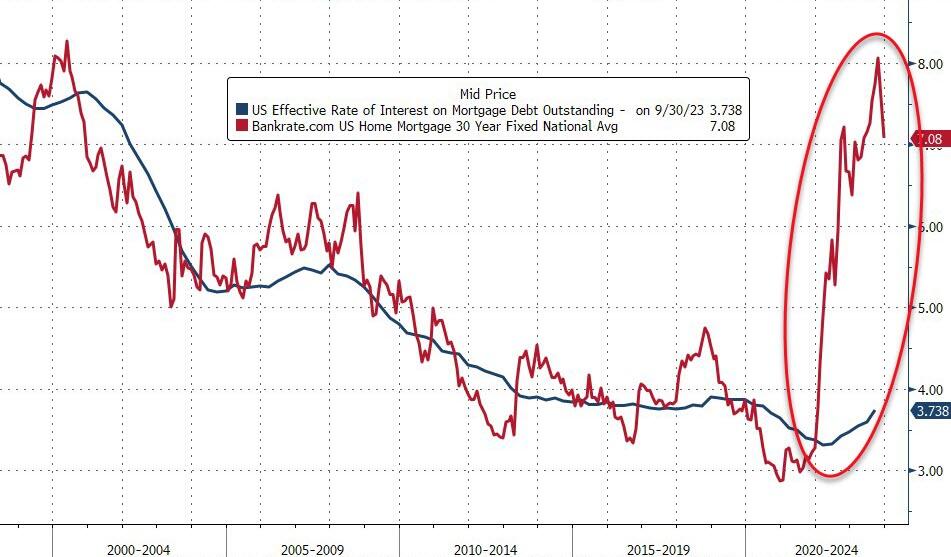

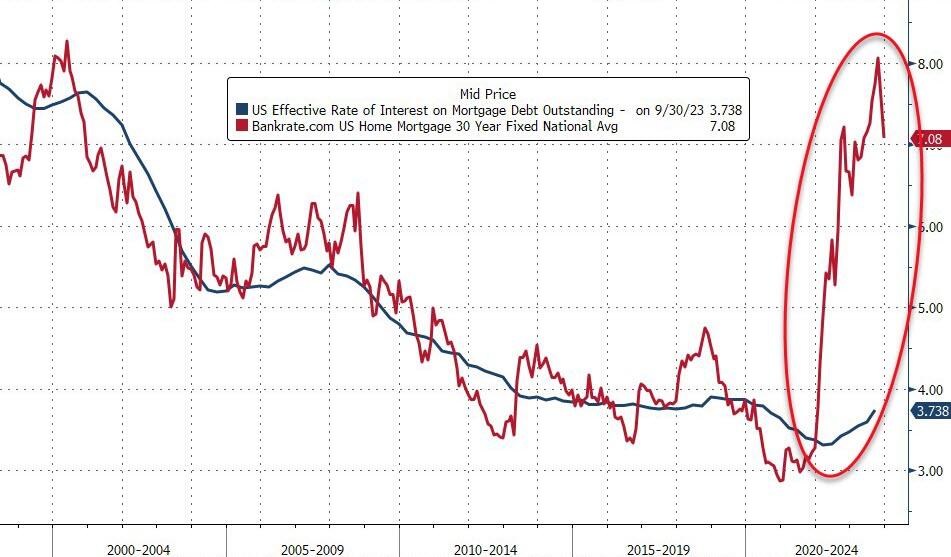

But, judging by the resumption of the rise of mortgage rates since the Case-Shiller data was created, we would expect prices to also resume their decline…

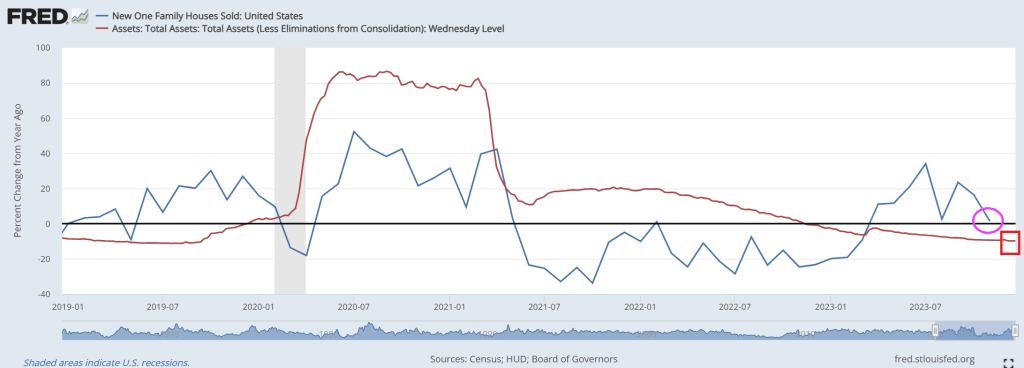

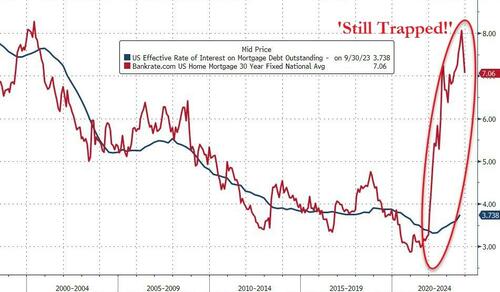

So prices are up, mortgage rates are actually falling again now (lagged)… so The Fed is re-blowing the same bubble?

Well, at least Detroit is near the top! Playing in Rocket Mortgage stadium.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.