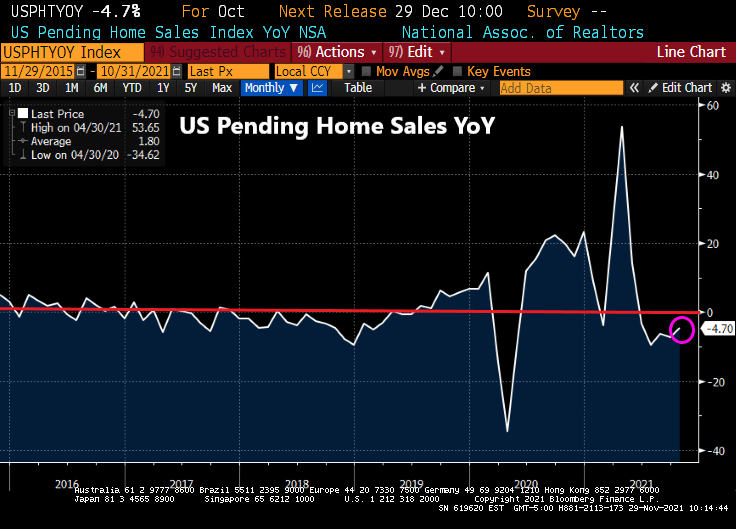

A forward-looking gauge of U.S. home purchases rebounded in October to a 10-month high, signaling steady housing demand despite growing affordability concerns among many prospective buyers.

The National Association of Realtors’ index of pending home sales increased 7.5% from a month earlier to 125.2, according to data released Monday. The median estimate in a Bloomberg survey of economists called for a 1% advance.

But it is the fifth straight month of year-over-year declines.

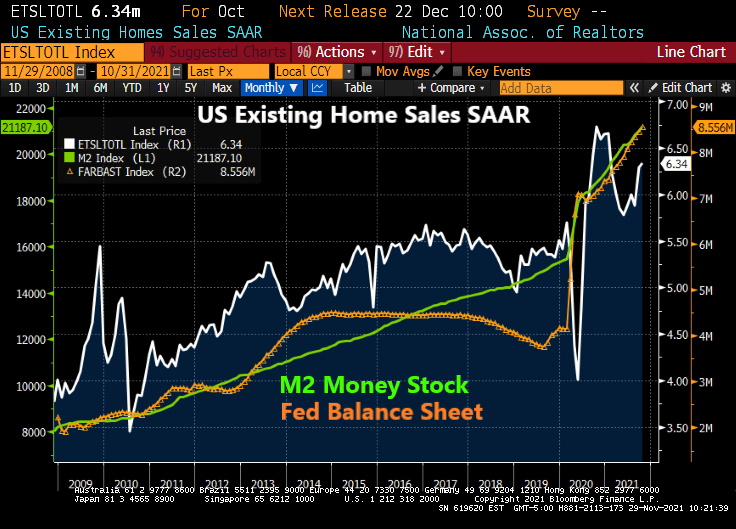

Low mortgage rates and solid job growth have supported housing demand this year as pandemic-weary buyers seek more spacious accommodations. Existing home sales are on track to exceed 6 million in 2021, which would be the strongest in 15 years, Lawrence Yun, NAR’s chief economist, said.

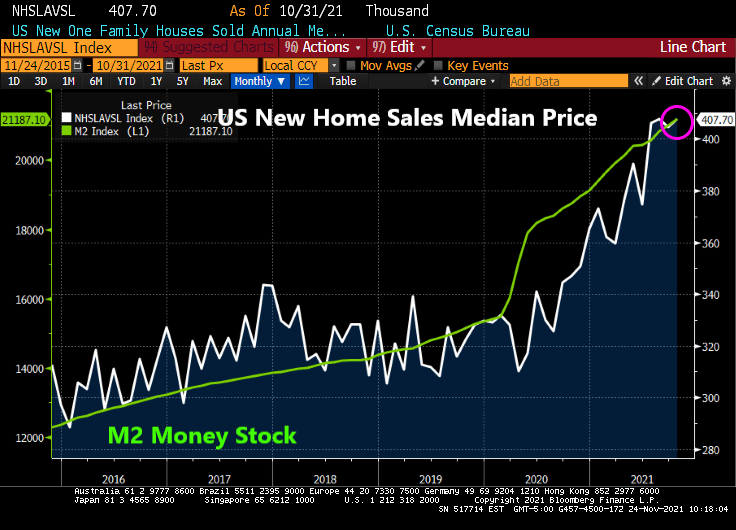

Yes, humongous stimulus from The Federal Reserve will help push existing home sales to exceed 6 million in 2021.

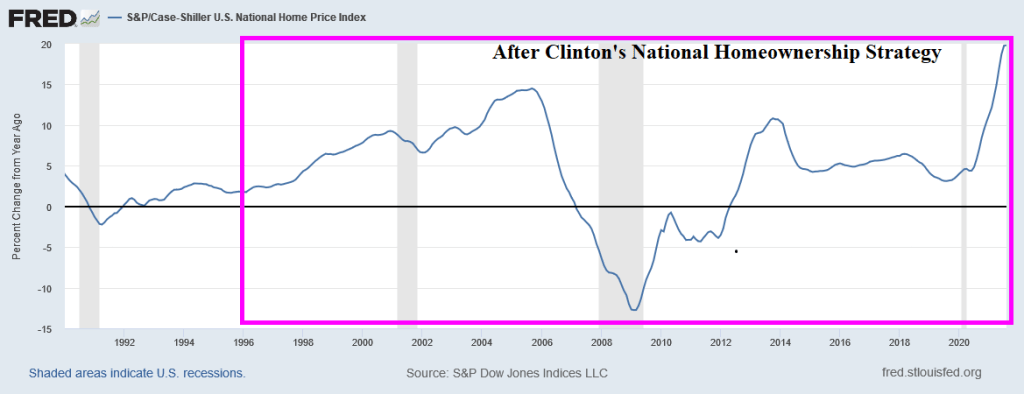

Still, competition over a scant number of listings — particularly on the lower, more affordable end of the resale market — has pushed prices out of reach for many prospective buyers. Builders have struggled to fill the void as supply-chain delays and labor shortages upend construction schedules, exacerbating the inventory crunch.

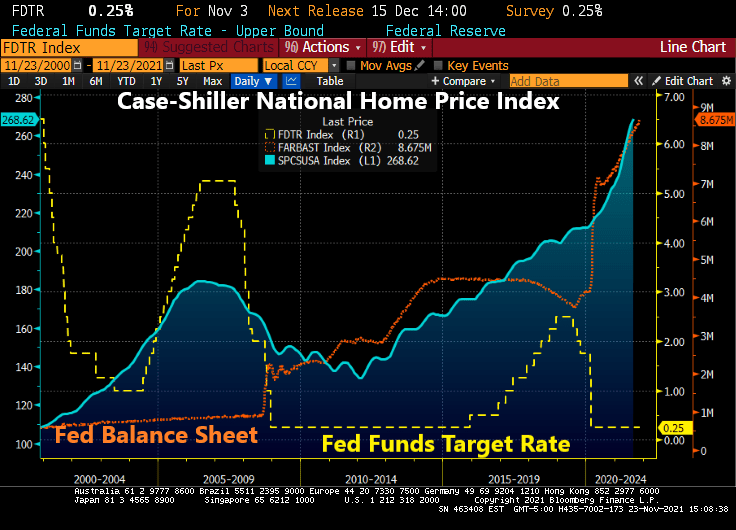

Yes, inventory of homes available for sale is almost 1/3rd of the homes available in 2010.

Ten years after ... and we have progressively less inventory available.

You must be logged in to post a comment.