Like virtually everything in Biden’s economy, the price of turkey (often the main staple for Thanksgiving dinner) is way up in price. Turkey prices are UP 73% since last year. The price per pound of an 8- to 16-pound turkey has risen to $1.99, a 73% increase from $1.15 last year, according to USDA data.

Speaking of turkeys, in recent speeches, President Joe Biden has been misleadingly taking credit for cutting federal deficits by historic amounts, though most of the reduction in deficits is the result of expiring emergency pandemic spending. Deficits fell between fiscal year 2020 and 2021 far less than initially projected after Biden added to them with more emergency pandemic and infrastructure spending.

And apparently Biden (or Jill) haven’t looked at the data recently. While there was a momentary budget surplus in April 2022, the Federal budget deficit has increased dramatically in September 2022 to the worst deficit since March 2021 shortly after Biden took office.

The only thing that is strong under Biden is the labor market. But even the accomplishment is grossly misleading. Under Trump, the U-3 unemployment rate was 3.5% in February 2020 just before Covid-13 struck and the Fauci-ites shut down the economy causing unemployment to rise to 14.7% in April 2020. Most of the reduction in the unemployment rate was the result of the economy slowly opening back up under Trump. When Biden took over, the unemployment rate was 6.4% and it is finally back to Trump’s 3.5% in September 2022. At least Biden didn’t screw that up, as Obama has said. Perhaps that should be his new midterm campaign slogan!

But Biden DID screw up the labor market with Bidenflation. REAL average hourly earnings growth (yellow line) is NEGATIVE..

And yes, the US is rapidly approaching recession which will result in a spike in unemployment. So much for Biden’s “Strong as hell!” economy.

Sweet home DC! At least for the ruling elites. For the rest of us mortals, Bidenflation is crushing our finances.

To combat Bidenflation, The Fed has signaled that they will continue to raise interest rates. But at what cost?

(Bloomberg) — The world’s leading central banks are finally pushing their interest rates into restrictive territory, causing fears of overkill in financial markets and stoking chatter that policymakers may need to pivot at some point.

And with the withdrawal of monetary stimulus comes the slowdown of US M2 Money growth (green line). And with that slowdown, we see a declining stock market and an inverted US Treasury yield curve.

Of course, Biden could reverse his green energy agenda and allow for oil and natural gas exploration … again. Or begin building nuclear power plants again. But nooooo.

Another peril is rising mortgage rates.

Here is the S&P 500 against global liquidity.

Speaking of Freddie King, here is Joe Biden’s favorite song: hideaway.

Yesterday, I told my family “The good news is that Rotolo’s Pizza tastes even better reheated in the morning. The bad news? I ate the only two piece left.”

Which brings me to the September jobs report. The good news is that 263k jobs were added to the US economy. That means 10,521k jobs have been added in the 21 months under Biden! (Bear in mind that 12,100k jobs were added in the 7 months under Trump following the Covid economic shutdown, yet no media outlet trumpeted that accomplishment).

The bad news? While nominal average hourly earnings grew by 5% YoY, when I subtract Bidenflation from that number I get -3.06% growth. Or should I say that REAL wages are shrinking under Biden.

Now for the “Biden Miracle” of jobs being added. Here is a chart of NFP jobs added (white line) against M2 Money and headline inflation. Both The Fed and the Federal government pumped trillions into the economy leading to the highest inflation rate in 40 years. Once governments stopped with their Covid shutdown nonsense, jobs would return regardless of who was President. BUT Federal spending and Fed money printing went off the rails in early 2020.

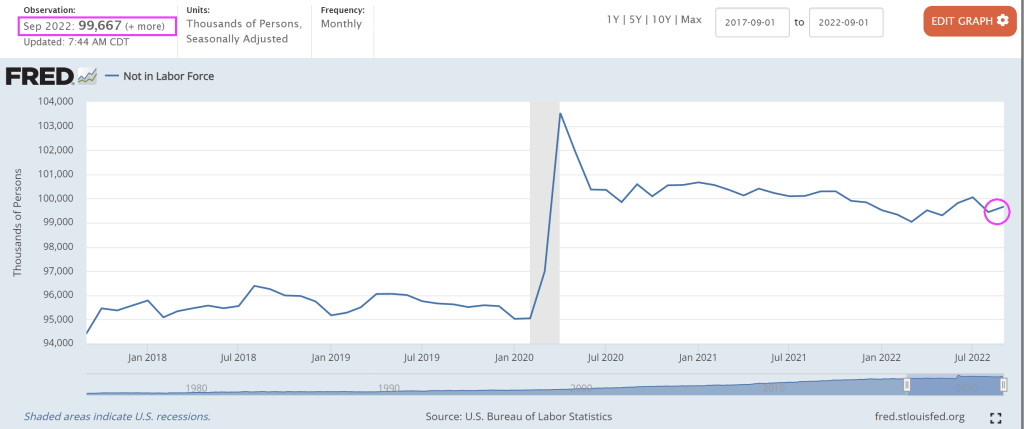

As Paul Harvey used to say, “Here is the rest of the story.” Labor force participation fell in September and the U-3 unemployment rate fell slightly to 3.5%.

But labor force dropouts increased leading U-3 unemployment to decline. The number of people NOT in the labor force grew to nearly 100 million. Nothing has been the same since Covid.

So what will The Fed do? According to Fed Funds Futures data (WIRP), The Fed will keep raising rates until March ’23 then slowly start lowering interest rates again.

And with that “positive” jobs report, The Dow is down almost -500 points and the NASDAQ is down over -3%.

And with Fed tightening, we are seeing a collapse in M2 money supply.

Thanks to Federal Reserve increases in their target rate, the 30-year mortgage rate has risen above 6%.

What drives me crazy about The Fed is their failure to removed monetary stimulus following the financial crisis of 2008 when they dropped their target rate to 25 basis points (0.25%) and began assets purchases (orange line). The Fed raises their target rate only once during Obama’s Presidency but then raised rates 8 times after Trump was elected President.

Now we are seeing The Fed NOT shrinking their balance sheet in a meaningful way. However M2 Money growth YoY (green line) has slowed to 5.2%.

While it is a good thing that The Fed is FINALLY reducing some of the monetary stimulus in place since 2008, the bad thing is that mortgage rates are rising rapidly.

The Fed’s quantheads are predicted to resume easing in March 2023.

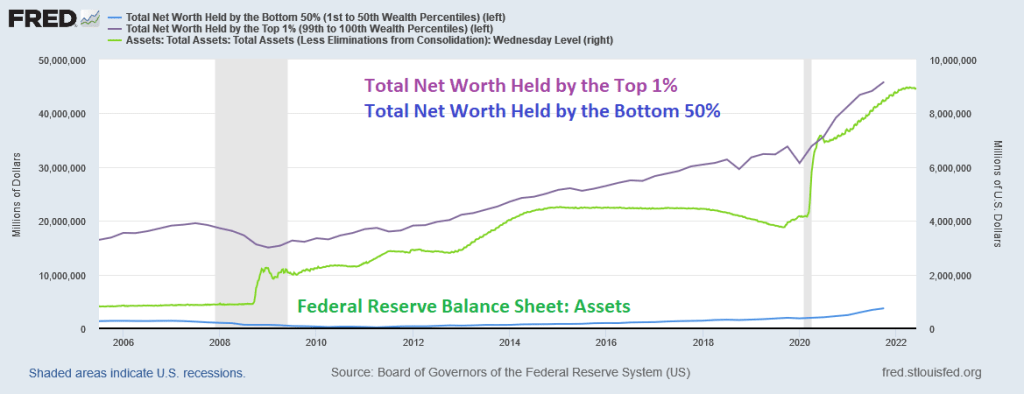

Pennies from Heaven. That is what the bottom 50% received from The Federal Reserve’s massive doses of monetary stimulus (or stimulypto).

There was one big dose of monetary stimulus in late 2008 surrounding the financial crisis and housing bubble burst, another doses (aka, QE 2 and QE3) then the biggest dose of all with the outbreak of Covid in early 2020.

President Biden should have mentioned on Jimmy Dimmel last night that The Federal Reserve has helped the bottom 50% with its endless monetary stimulus.

But if you were fortunate enough to own a home (the top 1% are likely homeowners), then you benefited from The Fed’s monetary stimulypto.

And I noticed that Biden didn’t mention plunging REAL average weekly earnings YoY.

The Federal Reserve’s monetary “policies” have benefited the top 1% and homeowners relative to the bottom 50% (who often rent and got clobbered with 20% growth in rents).

Great job, Fed! Making housing more unaffordable for rents (combine rising rents and declining REAL wages and we have a real affordability problem).

Home affordability for first time homebuyers?

And what is with Biden’s ear lobes? As inflation is rising, his ear lobes are shrinking.

The inflation numbers are out tomorrow. I noticed that Biden and Jimmy Dimmel only discussed gun control, not the sad state of the economy under Biden.

The US Q1 GDP report is due out tomorrow morning. The forecast is for -1.3% decline in GDP.

The Atlanta Fed GDPNow real-time GDP tracker is for 1.806% for Q2. If this holds, then recession fears will diminish.

Even though the US may avoid consecutive negative GDP quarters, M2 Money Velocity (GDP/M2 Money) got crushed by The Fed’s reaction to Covid back in 2020.

The Biden Administration and The Federal Reserve together should be called “The Cooler Kings” in that their policies are putting a Big Chill on the mortgage market and equities.

Mortgage rates are skyrocketing thanks to the Federal Reserve.

The 30-year fixed-rate mortgage averaged 5.27% for the week ending May 5, according to data released by Freddie Mac FMCC, -1.62% on Thursday. That’s up 17 basis points from the previous week — one basis point is equal to one hundredth of a percentage point, or 1% of 1%.

House price growth to wage growth is below the all-time high, but remains above housing bubble levels of 2005-2007.

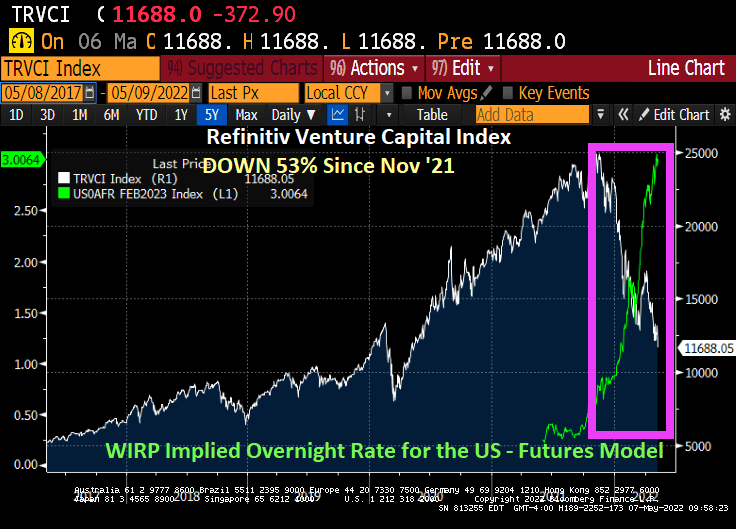

The Refinitiv Venture Capital Index is down 53% since November ’21 as The Fed cranks up interest rates.

Well, at least commodities are soaring under “The Cooler Kings.” Pretty much everything else is sucking wind.

The question, of course, is whether The Federal Reserve will back off its plans to aggressively raise interest rates in lieu of crashing stock market, venture capital, and possibly home prices.

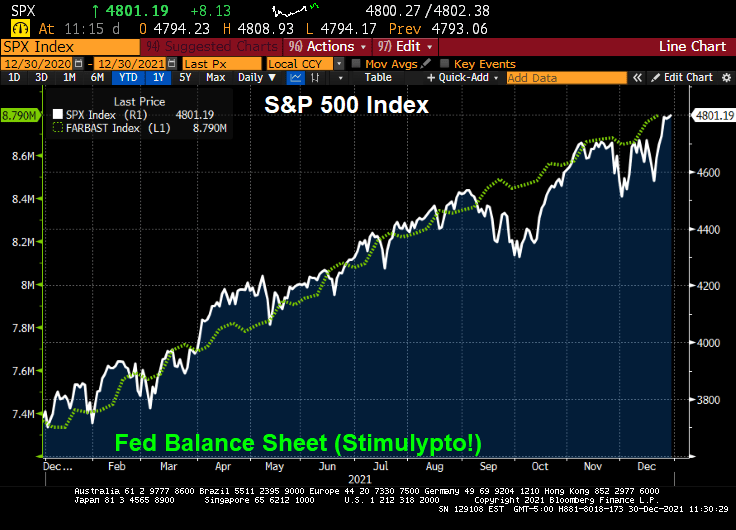

2021 saw the S&P 500 index generate a return of 28.7%. Much of it thanks to The Federal Reserve “stimulypto” or excessive monetary easing.

But only three hedge funds beat the S&P 500 index: Senvest, Impala and SR. Thanks to fees (trading and management), the other hedge funds underperformed the S&P 500 index. And underperformed The Fed!

Melvin Capital was the worst performing hedge fund of the ones examined.

You must be logged in to post a comment.