The US Producer Price Index (PPI) final demand rose 10% YoY in February, further evidence of spiraling inflation under Biden/Pelosi/Schumer’s reign of error.

And speaking of Senate Majority Leader Chuck Schumer (D-NY), the Empire State Manufacturing Survey (General Business Conditions) crashed to -11.8.

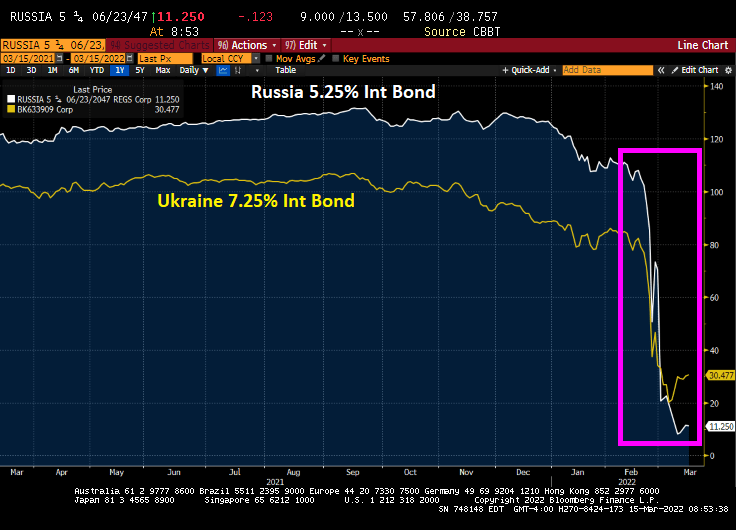

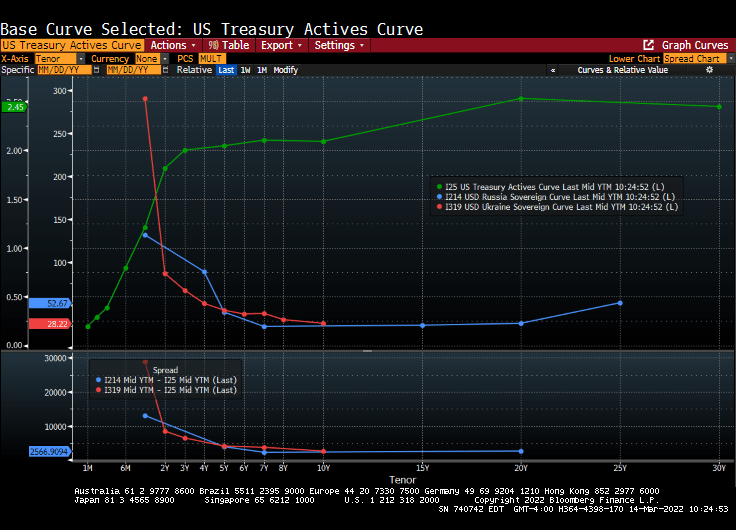

And Russia is losing the economic demolition derby with Ukraine (at least for sovereign debt).

I am still trying to figure out what House Speaker Nancy Pelosi (D-San Francisco) meant by “When we’re having this discussion, it’s important to dispel some of those who say, well it’s the government spending. No, it isn’t. The government spending is doing the exact reverse, reducing the national debt. It is not inflationary.”

Really Nancy?

Here is a chart of Federal government outlays and inflation. Massive expenditures and growth in Federal debt and the resulting inflation. Nancy?

Yes, it is the much anticipated Fed Week! The Fed Open Market Committee (FOMC) will announce it decision (probably the first rate hike under Biden of 25 basis points).

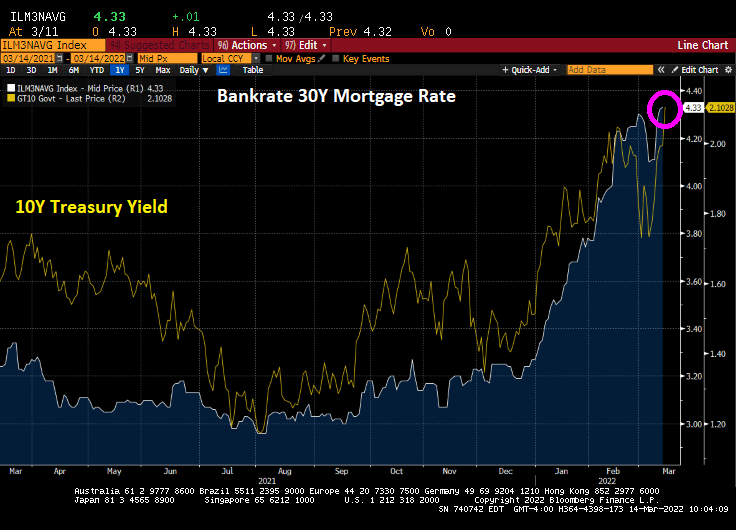

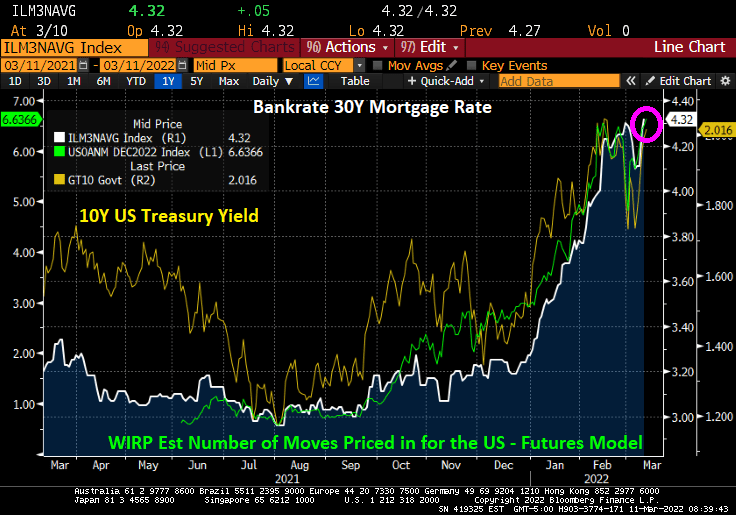

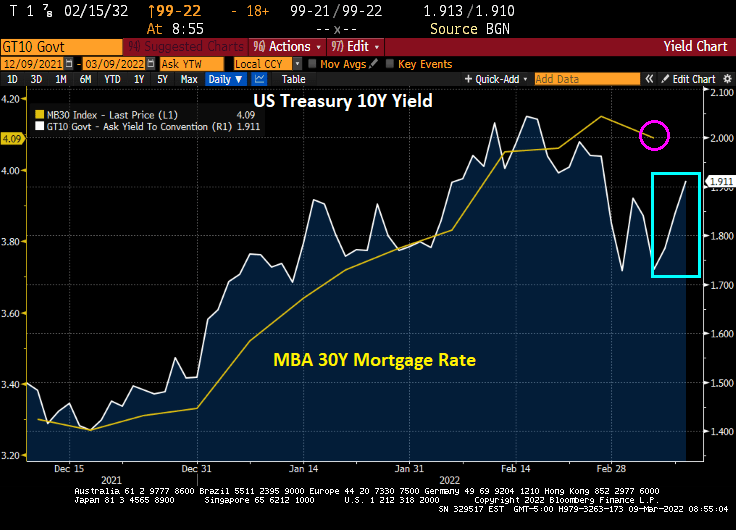

This morning, the 10-year Treasury yield rose by 11.1 basis points and the Bankrate 30Y mortgage rate rose to 4.33%.

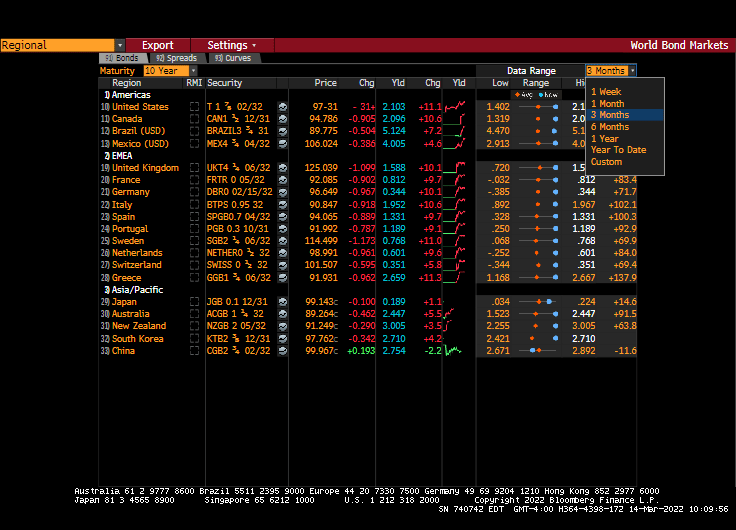

Actually, sovereign yields are up around 10 basis points in the US, Canada, and across the pond.

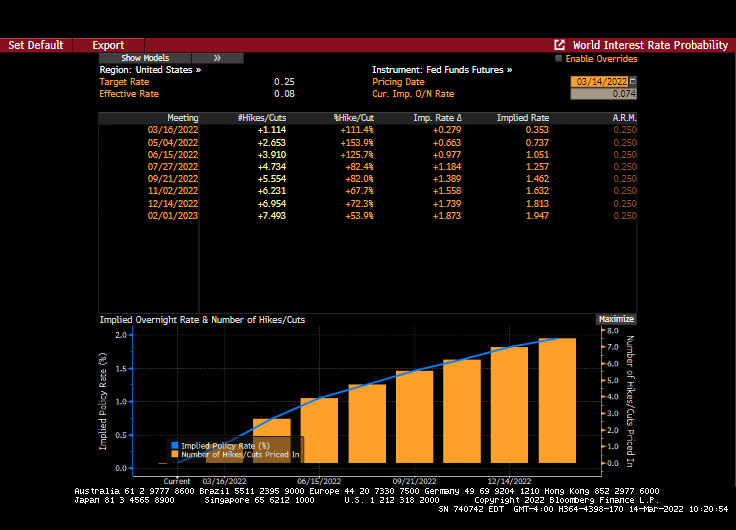

Fed Funds Futures are pointing to 7 rate hikes over the next year with 1.114 rate hikes on Wednesday. That means The FOMC may raise rates MORE than the 25 basis points expected my many (including me).

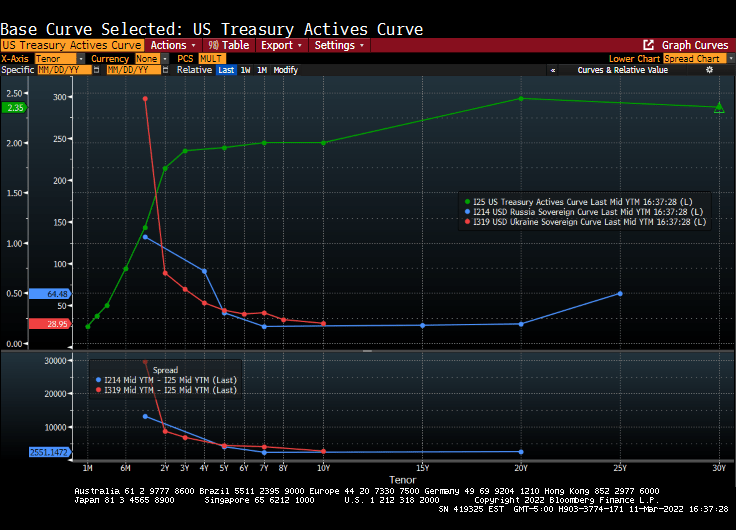

The US Treasury actives curve remains steeply upward sloping while both the Russian and Ukraine sovereign curves are steeply inverted and crashing.

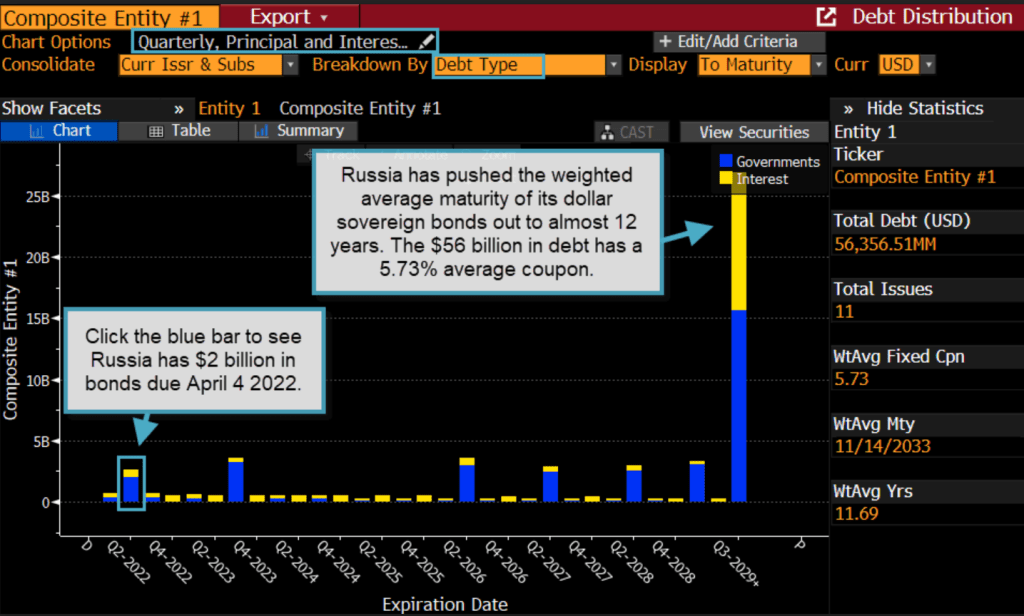

Russia has pushed the weighted average maturity of its dollar sovereign bonds out to almost 12 years.

The most hilarious headline of the day is a Bloomberg opinion piece: “Fighting Inflation May Require the Fed to Be Brutal: Clive Crook” How about the Biden Administration relaxing oil drilling and pipeline restraints? Otherwise, brutal translates into causing a recession. Great suggestion, Clive! … NOT!

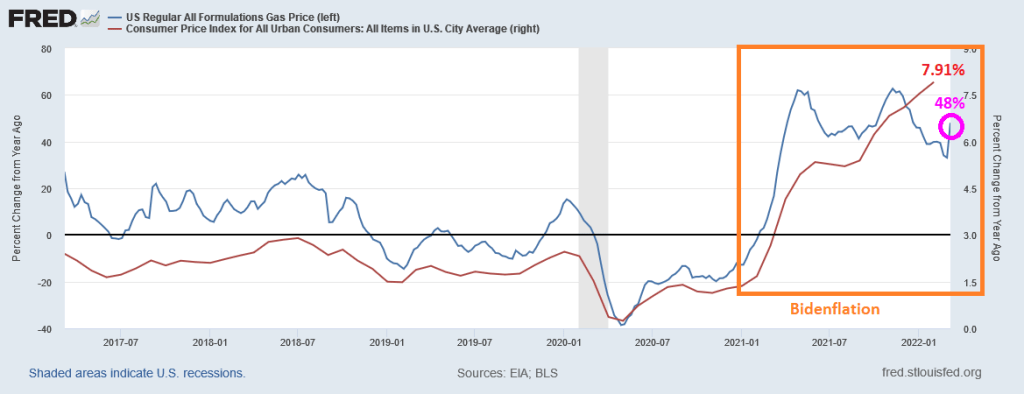

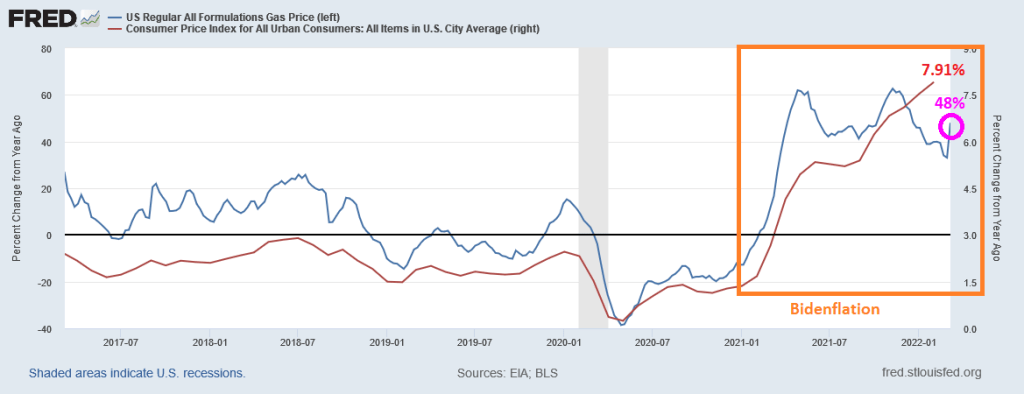

Well, so much for rising gasoline prices being the fault of Vlad “The Ukrainian Impaler” Putin and Russia invading Ukraine. In fact, gasoline prices were rising at a 62% YoY pace in April 2021, well before Russia’s invasion of Ukraine.

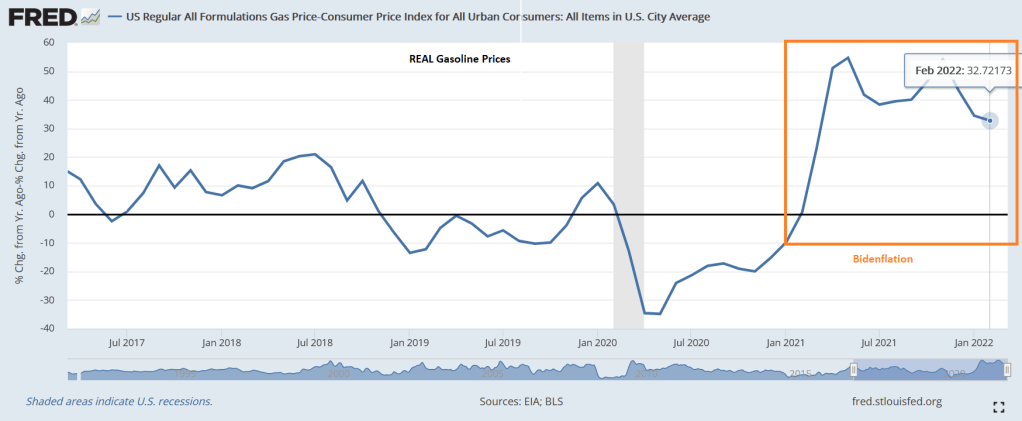

REAL gasoline prices (nominal gasoline prices less inflation) are up 32.72% YoY in February.

Press secretary Jen Psaki can take the opportunity to proclaim that REAL gasoline prices have actually declined in February.

I keep waiting for the Biden Administration and Congress to launch price controls and supply rationing rather than simply allow the Keystone Pipeline to be built and allow drilling on Federal lands.

Coindesk: The foundations of Bretton Woods II crumbled last week when the G7 seized Russia’s foreign exchange reserves, the investment bank said.

The Russian-Ukrainian war will create a new world financial order from which Bitcoin is set to benefit, according to Credit Suisse.

Zoltan Pozsar, global head of short-term interest rate strategy at the giant investment bank, wrote in a Monday report that Western sanctions on Russia are likely to cause a paradigm shift in the way the world organizes money and reserves, a “Bretton Woods III” kind of scenario.

“From the Bretton Woods era backed by gold bullion, to Bretton Woods II backed by inside money, to Bretton Woods III backed by outside money,” the strategist wrote.

Pozsar argues that the fall of Bretton Woods II ensued last week as G7 countries decided to seize Russia’s foreign exchange (FX) reserves, leading to a rise of outside money – reserves kept as commodities – over inside money – reserves kept as liabilities of global financial institutions.

“We are witnessing the birth of Bretton Woods III – a new world (monetary) order centered around commodity-based currencies in the East that will likely weaken the Eurodollar system and also contribute to inflationary forces in the West,” the report states.

Russia, a surplus agent in the financial system, can now no longer make use of the hefty FX reserves it accumulated through its commodity exports over the decades to defend its falling ruble or aid its local economy. Moreover, Russia’s ability to export its commodities has been severely hurt due to the “buyer’s strike” in the West.

“What we are seeing at the 50-year anniversary of the 1973 OPEC supply shock is something similar but substantially worse – the 2022 Russia supply shock, which isn’t driven by the supplier but the consumer,” the strategist wrote. “The aggressor in the geopolitical arena is being punished by sanctions, and sanctions-driven commodity price moves threaten financial stability in the West.”

Pozsar argues that while Western central banks cannot close spreads between Russian and non-Russian commodity prices as sanctions lead them in opposite directions, the People’s Bank of China can “as it banks for a sovereign who can dance to its own tune.”

“If you believe that the West can craft sanctions that maximize pain for Russia while minimizing financial stability risks and price stability risks in the West, you could also believe in unicorns,” Pozsar wrote.

As outside money keeps trumping inside money, this crisis will likely emerge and end differently than all others ever since Nixon broke off the gold standard in 1971 – which marked the end of the era of commodity-based money.

Meanwhile, US Treasury Secretary Janet Yellen said the U.S. dollar is in no danger of losing its status as the world’s dominant reserve currency as a result of sanctions imposed against Russia over its invasion of Ukraine.

“I don’t think the dollar has any serious competition, and is not likely to for a long time,” Yellen told reporters in response to questions following a speech in Denver on Friday.

Some commentators, including Credit Suisse Group AG interest-rate strategist Zoltan Pozsar, have warned sanctions that blocked Russia’s access to its foreign currency reserves could drive other countries away from the dollar.

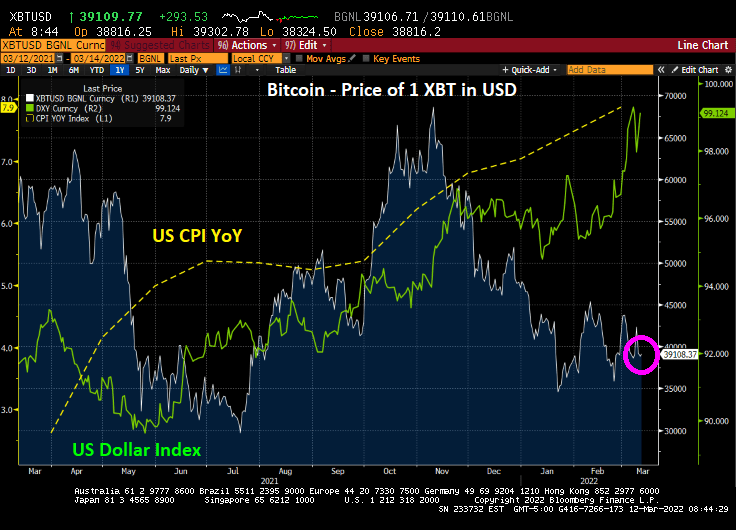

Well, what Zoltan says may be true, but not so far. Bitcoin has been plunging since November 2021 as inflation keeps rising.

Zoltan: “..and Bitcoin (if it still exists then) will probably benefit from all this.” The US Treasury yield curve is listing towards inversion, a signal of impending recession.

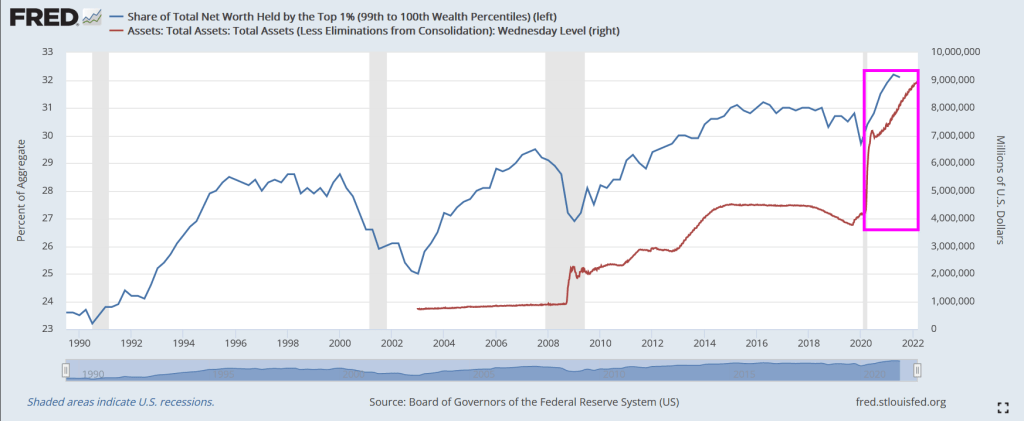

Following the financial crisis of 2008/2009, The Federal Reserve began their dramatic purchase of assets such as Treasuries and Agency mortgage-backed securities (AgencyMBS). And then Covid struck and The Fed went berserk with asset purchases.

So, who benefited the most? The top 1% or the bottom 50%?

Answer? The top 1%. The share of total net worth spiked dramatically after the Fed infusion.

Even the bottom 50% benefited with The Fed’s Covid stimylpto, but no where near how the top 1% benefited.

World Economic Forum’s elitist Klaus Schwab approves of this message!

On an unrelated note, the US Treasury yield curve is strongly UPWARD sloping, while Russia’s and Ukraine’s yield curves are inverted and collapsing.

US 30-year mortgage rates rose to 4.32% (Bankrate) as the 10-year Treasury yield broke through the 2% barrier. This is happening as Fed Funds Futures are pointing toward 6+ rate increases over the coming year.

Actually, Fed Funds Futures are pricing in 7 rate increases over the coming year.

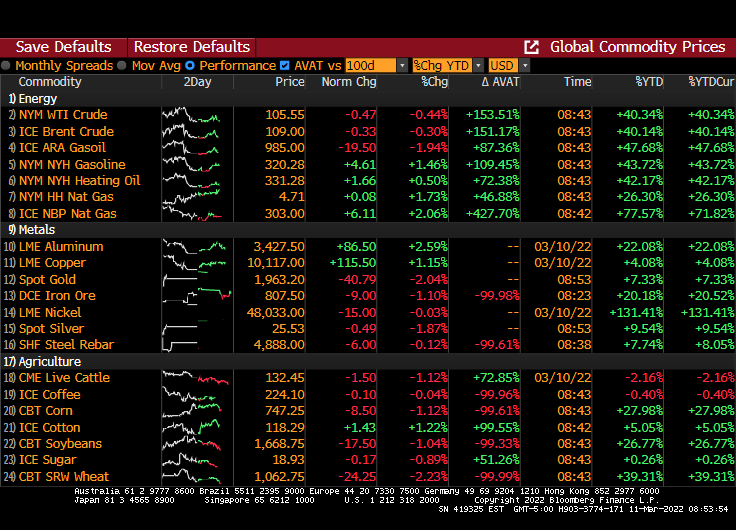

At least all is quiet on the commodities front.

So, it appears that Fed Chair Jay Powell will follow-through with numerous rate hikes over the coming year.

I guess Powell is tired of being a low-rate chump instead of a high-rate champ?

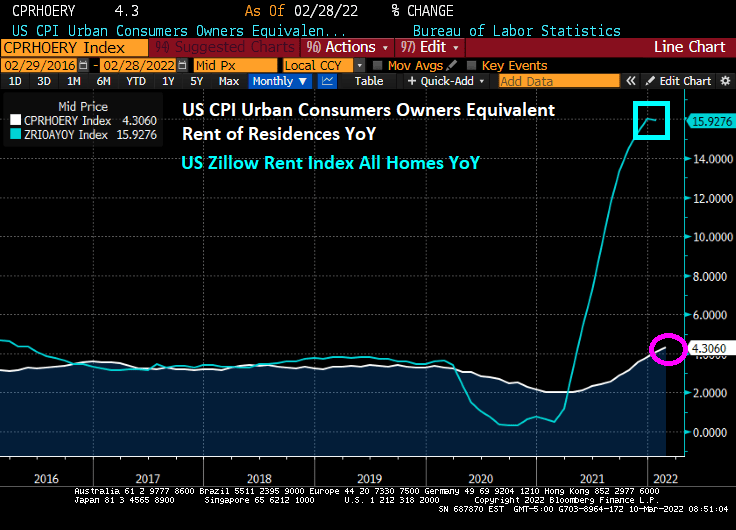

US rent inflation (owner’s equivalent rent of residence YoY) surged to 4.30%. However, Zillow’s rent index last month was 15.93% YoY.

But if we look at US Monthly Rent YoY, we see that rents are climbing at a 17.6% rate.

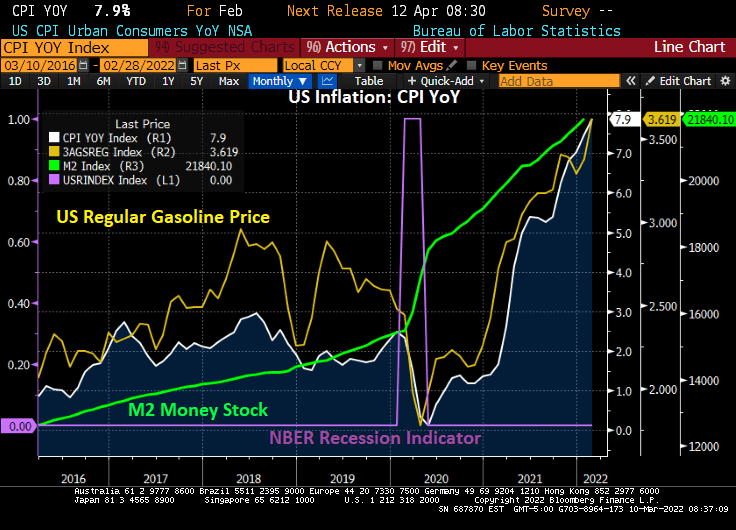

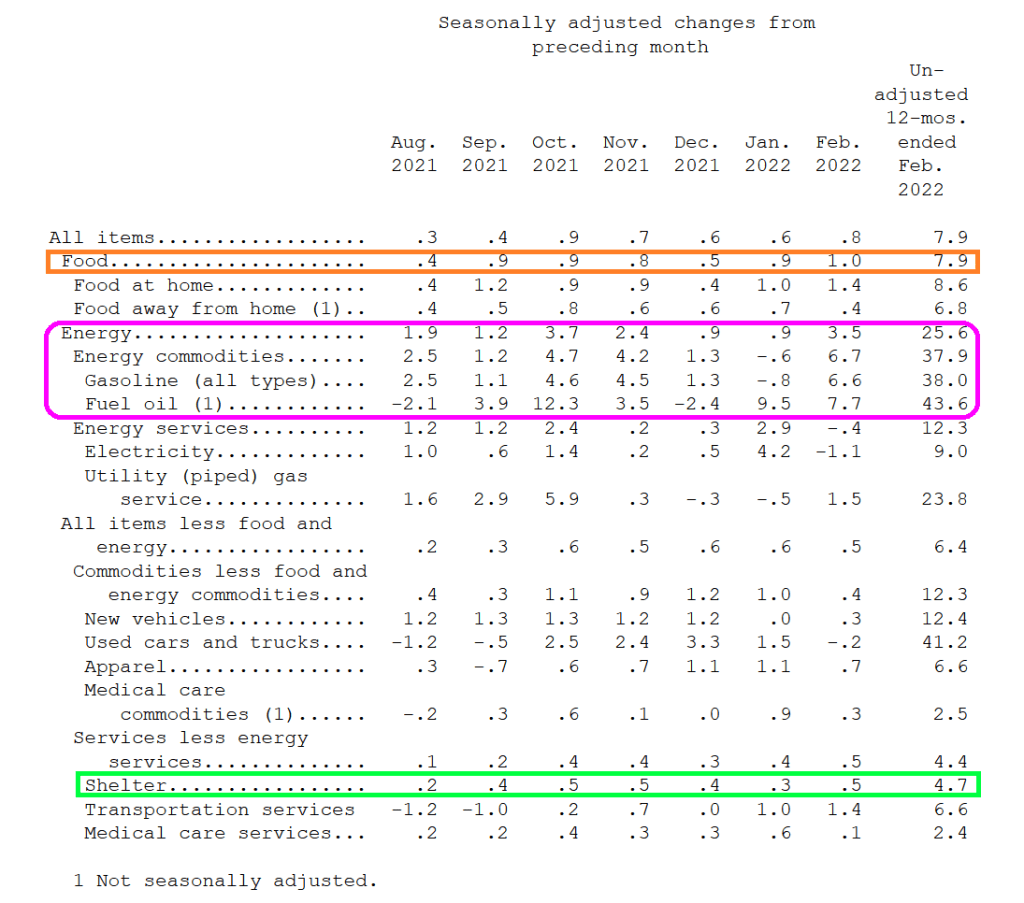

Energy costs soared in February YoY. Gasoline was up 38%. Fuel Oil was up 43.6%. Food was up 7.9%.

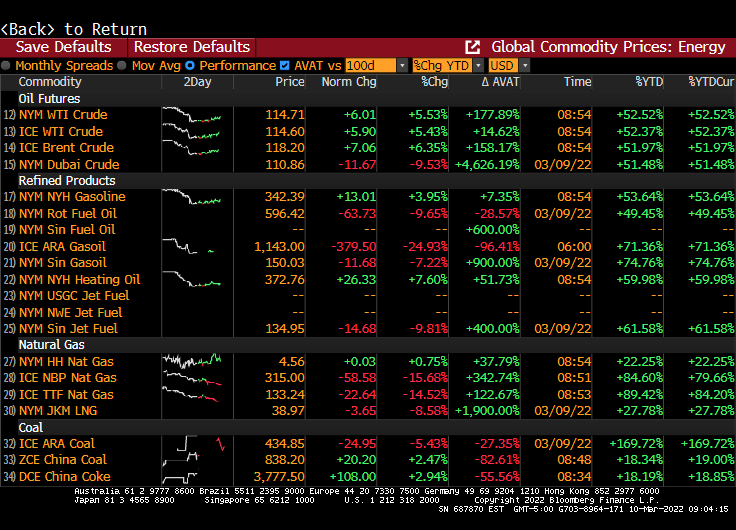

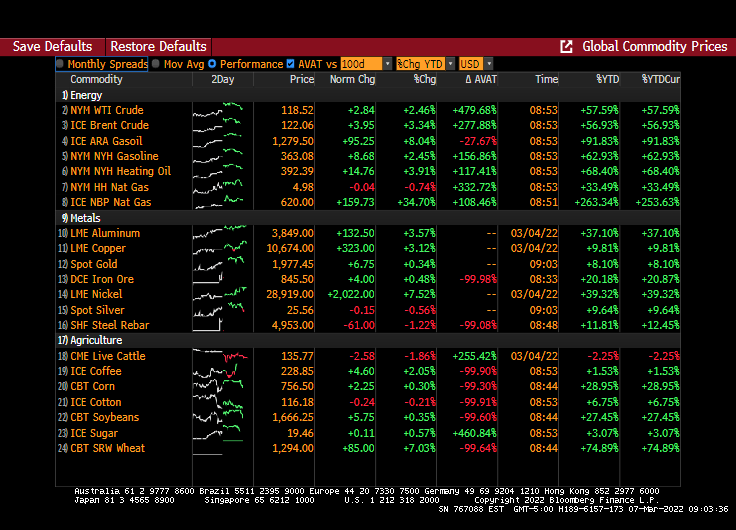

Volatility (AVAT) rages in the energy sector.

There are still 7 rate hikes in the cards from The Federal Reserve.

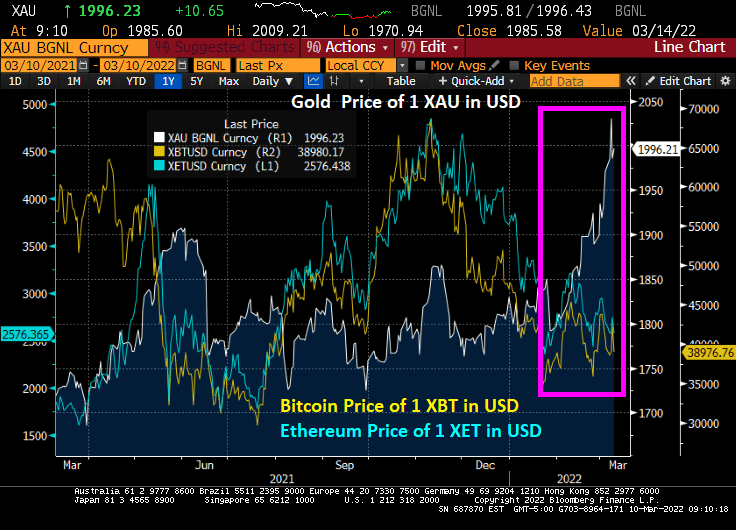

Gold has been climbing as Russia invades Ukraine. Cryptos Bitcoin and Ethereum are steady, even as the Biden Administration issues an executive order to “study” cryptocurrencies.

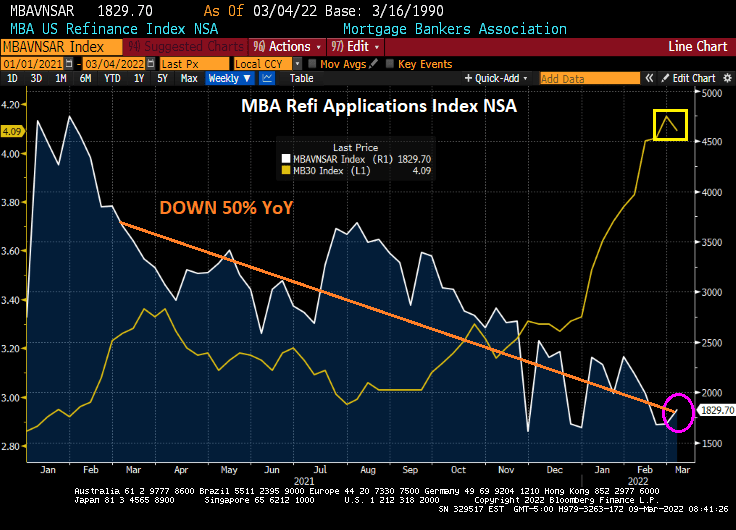

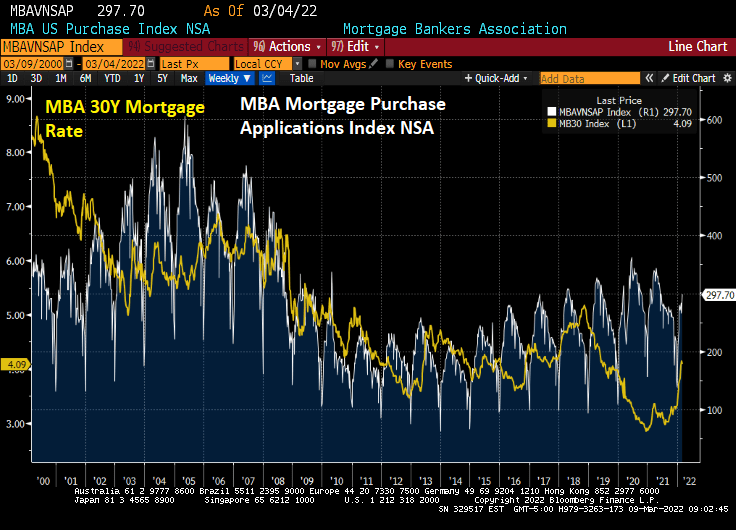

The mayhem caused by the Russian invasion of Ukraine is helping drive down interest rates … for the time being … and this is helping push down mortgage rates and increase mortgage applications.

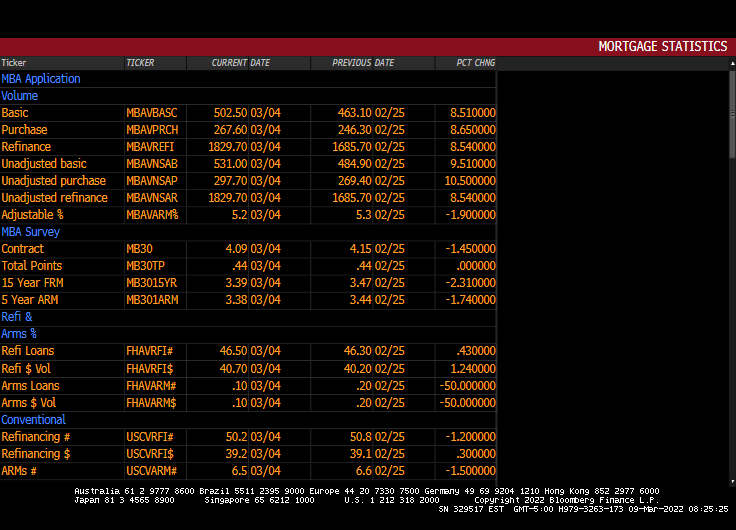

Mortgage applications increased 8.5 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending March 4, 2022.

The seasonally adjusted Purchase Index increased 9 percent from one week earlier. The unadjusted Purchase Index increased 11 percent compared with the previous week and was 7 percent lower than the same week one year ago.

The Refinance Index increased 9 percent from the previous week and was 50 percent lower than the same week one year ago. Diane Olick at CNBC has the hilarious headline “Brief drop in mortgage rates sparks mini refinance boom.” The slight rise in refi applications from the previous week is more of a firecracker going off than a boom given that refi apps are still down 50% from the same week last year.

Bear in mind that the US Treasury 10-year yield is up since the MBA’s reporting week ended on March 4, 2022. So, look for Olick’s mini-refi boom to end as quickly as it started.

Here is the rest of the MBA story.

The MBA Mortgage Purchase applications index typically peaks in mid-to-late April, so we still have another month (seasonality) until purchase applications begin declining again.

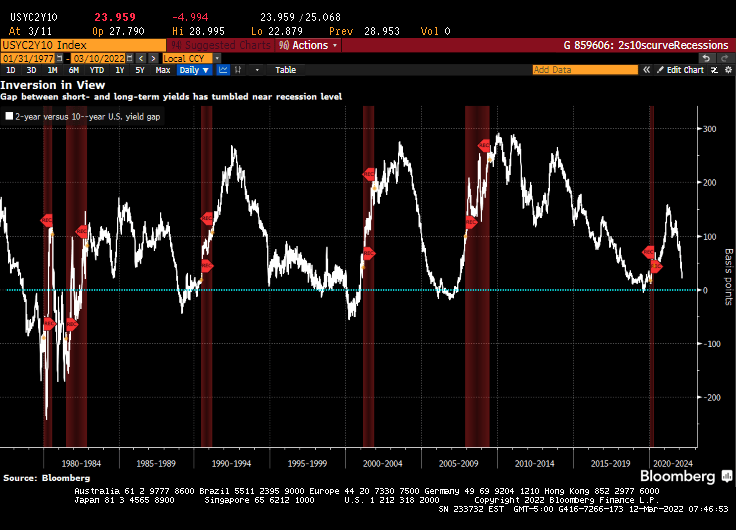

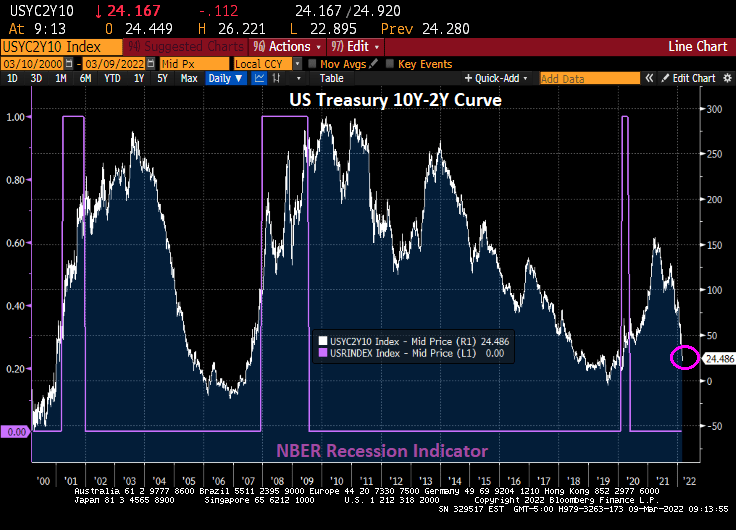

The US Treasury 10Y-2Y curve continues to flatten and is the worst curve recovery in modern history.

The general rise in US mortgage rates is more closely tied to expectations of Fed rate increases than Fed Agency MBS holdings.

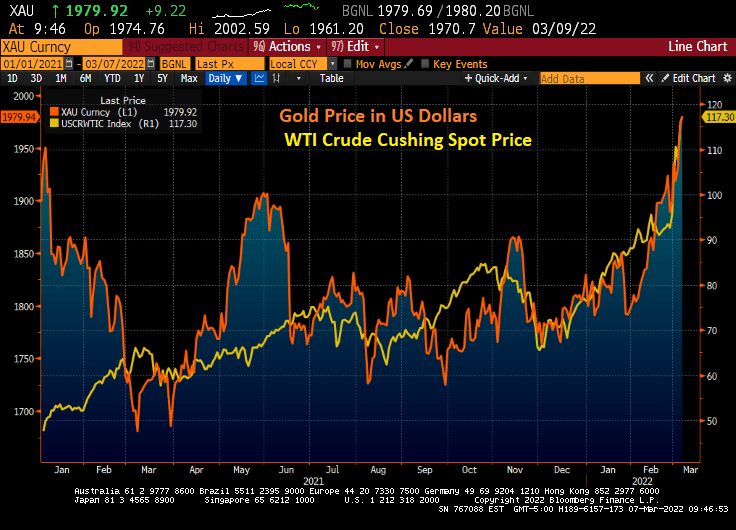

WTI Crude Oil spot price was up 91% from the beginning of 2021 to the Russian invasion of Ukraine. Now it is up 142% thanks to the invasion of Ukraine.

Energy prices are still soaring with UK Natural Gas prices up another 34.70% today with Brent Crude futures up 3.34%. Wheat futures are up 7.03%.

The US Treasury 10Y yield rose 6.8 bps this morning (UK takes the lead with a 10.3 bps increase).

The US Treasury 10Y-2Y yield curve slope continues to swoon to where it is now flatter than when President Biden entered office.

Gold is now at it highest level since before Biden was sworn-in as President as WTI Crude Oil soars.

Gold hit $2,000 before retreating back down.

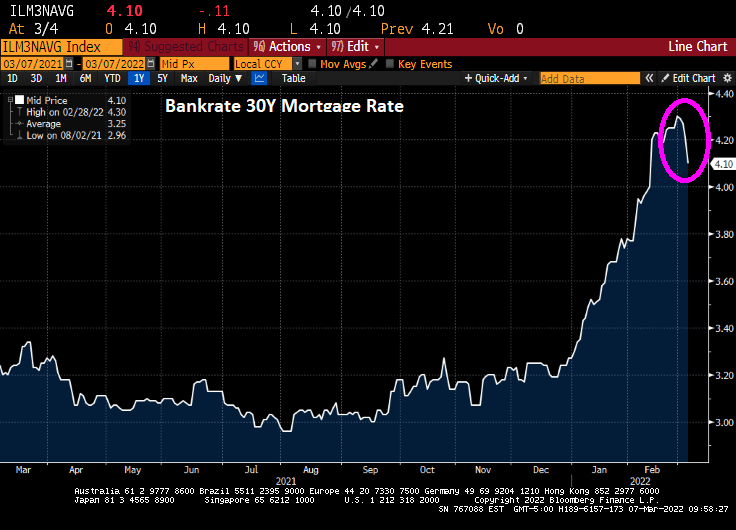

And Bankrate’s 30Y mortgage rate declined to 4.10%.

Russia is the world’s largest exporters of wheat and Ukraine is the 5th largest exporter.

You must be logged in to post a comment.