The global economy has certainly been turned on its head by the COVID outbreak in early 2020. Not so much by the virus itself, but by Central Bank hysteria in terms of rate lowering and balance sheet expansion. Which The Fed has not yet unwound.

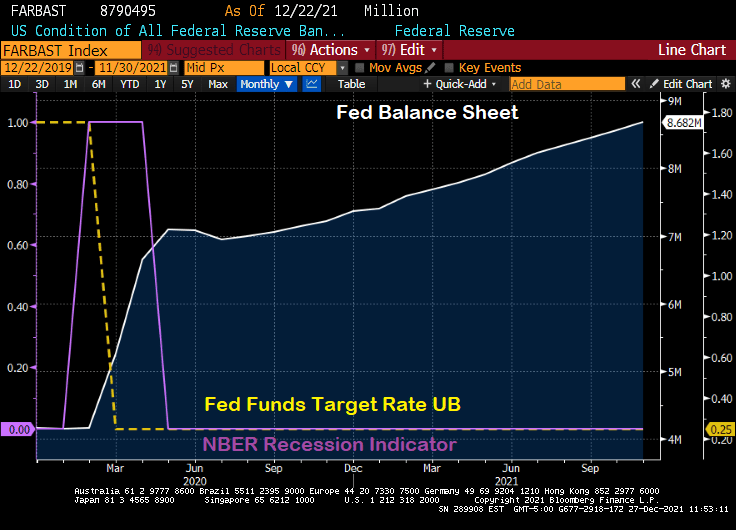

Let’s look at what has happened since the mini-recession caused by COVID in early 2020. The shortest recession in US history, a measly 2 months. The Fed expanded its balance sheet from $4.17 million in February 2020 to $8.79 million today. That is, The Fed over doubled the size of their balance sheet in reaction to the shortest recession in US history. Overreaction much?

What has happened since the mini-recession and The Fed’s massive overreaction?

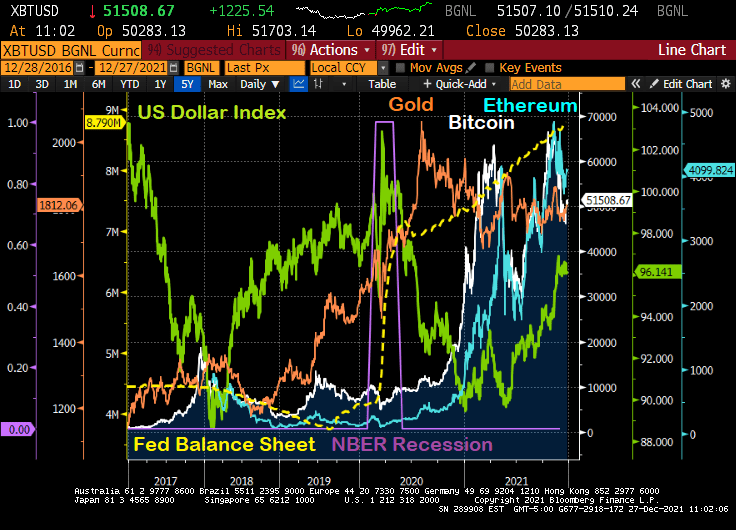

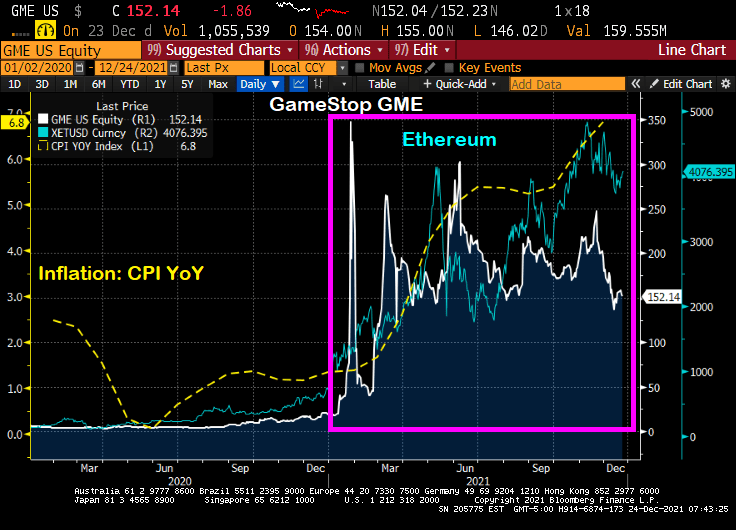

First, gold (gold line) surged then calmed down. Then cryptocurrency Bitcoin (while line) surged, then calmed down, then surged again only to calm down again. Then crypto Ethereum surged, calmed, surged, calmed. Meanwhile the US Dollar Index crashed only to start rising again.

The Fed’s overreaction and failure to withdraw excessive stimulus has led to the rise of alternatives to the deflating dollar due to inflation.

When will The Fed ACTUALLY start removing the overreaction stimulus? Let’s get it started.

Perhaps only April Ludgate can kill The Fed’s overreaction stimulus.

2021 has been a very weird year. Inflation has boomed (highest in 40 years) after the election of Joe Biden as President of the USA (call it Bidenflation). Then we have The Federal Reserve barely acting on the booming inflation (keeping rates at 25 basis points while withdrawing the COVID-related monetary stimulus).

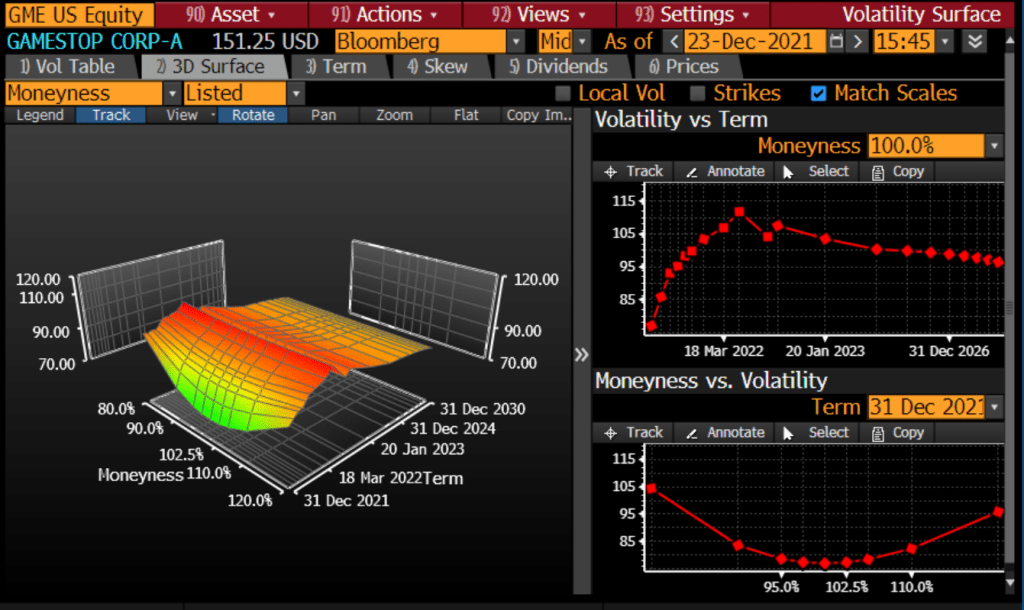

Given the volatility of GameStop (Reddit-inspired), you can see the strange shape of GameStop’s volatility surface.

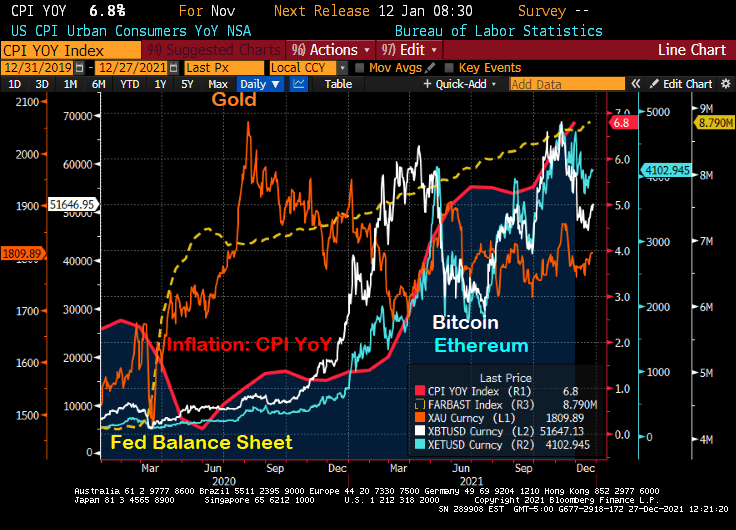

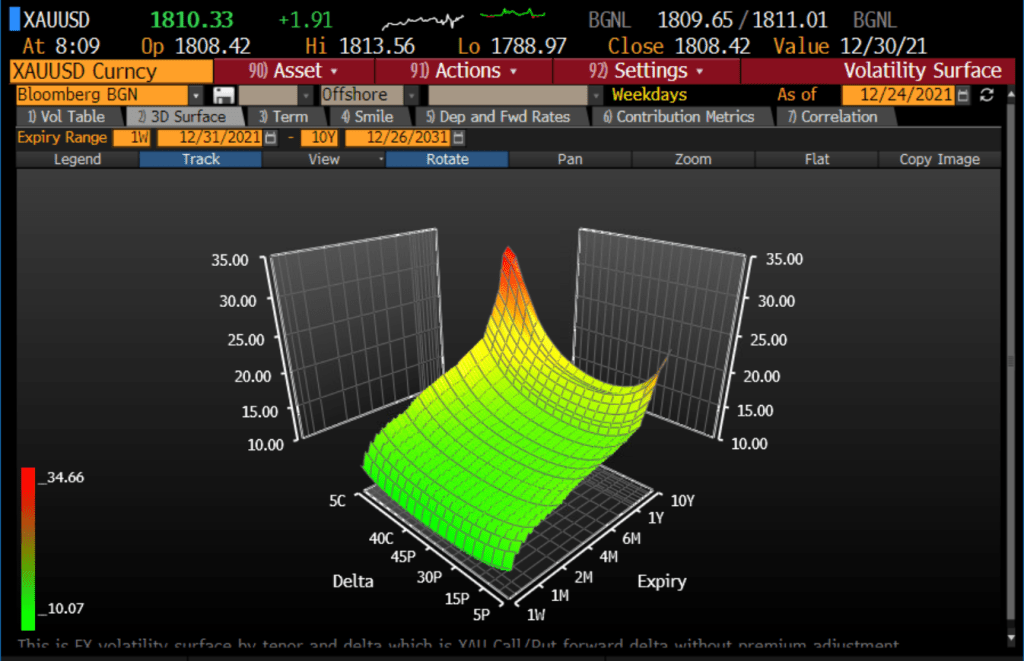

By contrast, gold is now where it was was at the beginning of 2021 and the surge of Bidenflation.

Here is volatility surface for gold.

So, there are a number of meme stocks (GameStop is just one example), gold, silver, cryptos such as Bitcoin and Ethereum. But gold seems to be placid with respect to inflation, but the meme stocks and cryptos seem to be motoring. Or is it rage against the financial machine? Or rage against Bidenflation??

The US stock and bond markets are closed today and tomorrow, Christmas day.

Have a Merry Christmas! And celebrate the “Santa Pause” as Powell refuses to raise rates to combat inflation until 2022.

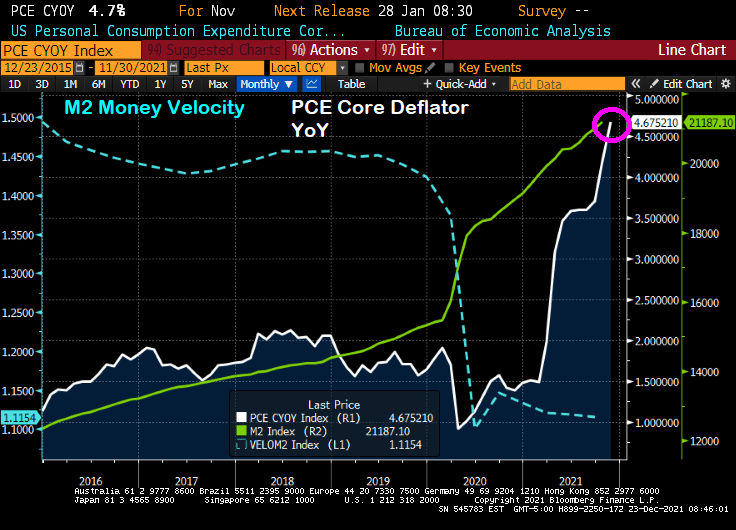

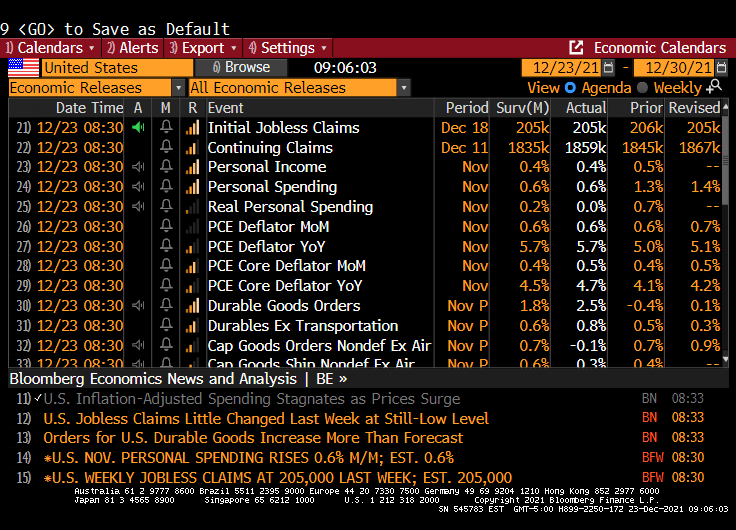

The core Personal Consumption Expenditures (PCE) deflator numbers for November were released this morning and the print was a whopping 4.7% YoY, the highest rate since 1989.

Meanwhile, U.S. consumer spending, adjusted for inflation (aka, REAL personal spending), stagnated in November as the fastest price gains in nearly four decades eroded purchasing power. Stagnated to 0.

Purchases of goods and services, after adjusting for higher prices, were little changed following a 0.7% gain in October, Commerce Department figures showed Thursday.

And as Paul Harvey would say, here is the rest of the story.

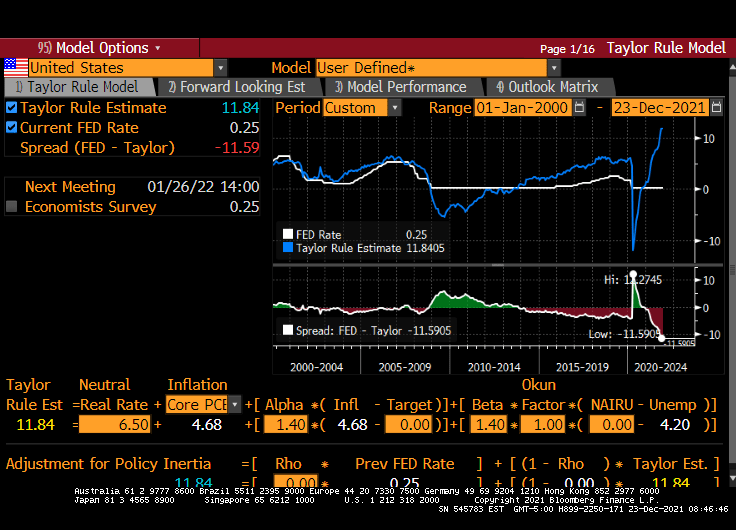

Core PCE growth YoY of 4.68% implies a Fed Funds target rate of 11.84%. Powell and the gang have the target rate at 0.25%. But the Taylor Rule doesn’t take into account the latest FEAR raging in Washington DC … the Omicron variant. Just another excuse for The Fed to do nothing and let asset bubbles blow out of control.

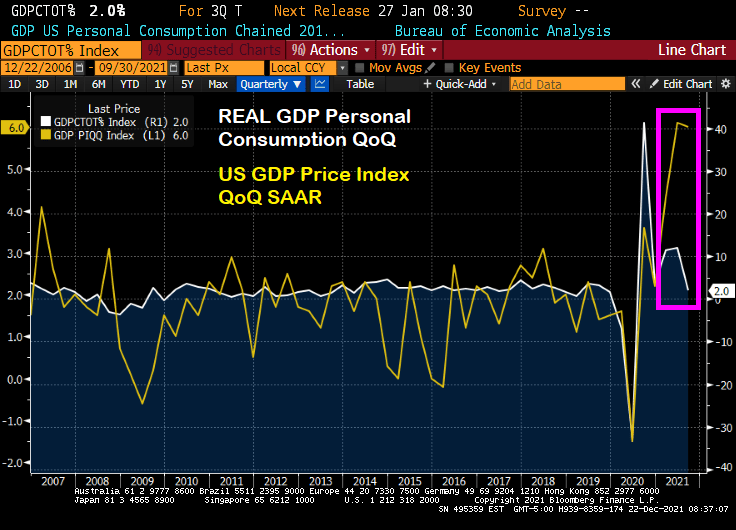

The good news is that US Real GDP grew at 2.3% QoQ in Q3 thanks to massive Federal government and Federal Reserve stimulus. The bad news? Prices are growing at rate of 6% QoQ, three times higher than the growth of real personal consumption.

Runaway inflation, cooling personal consumption. This is the definition of “stimulyltpo”: the excessive spending by Washington DC in conjunction with excessive monetary stimulus from The Federal Reserve.

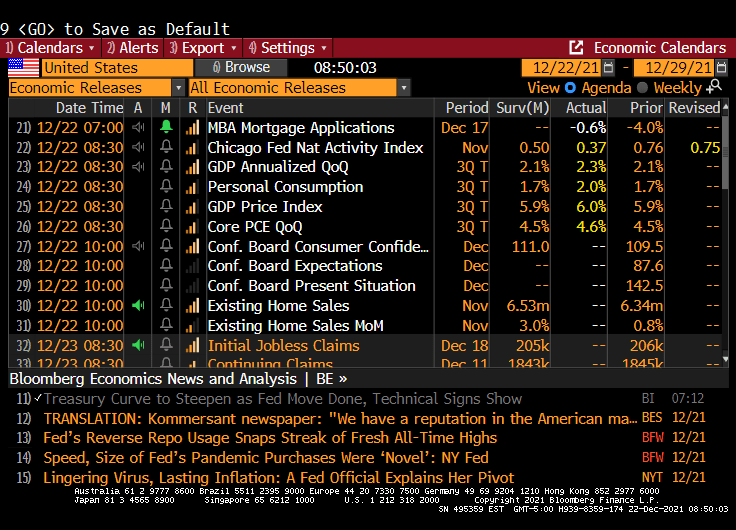

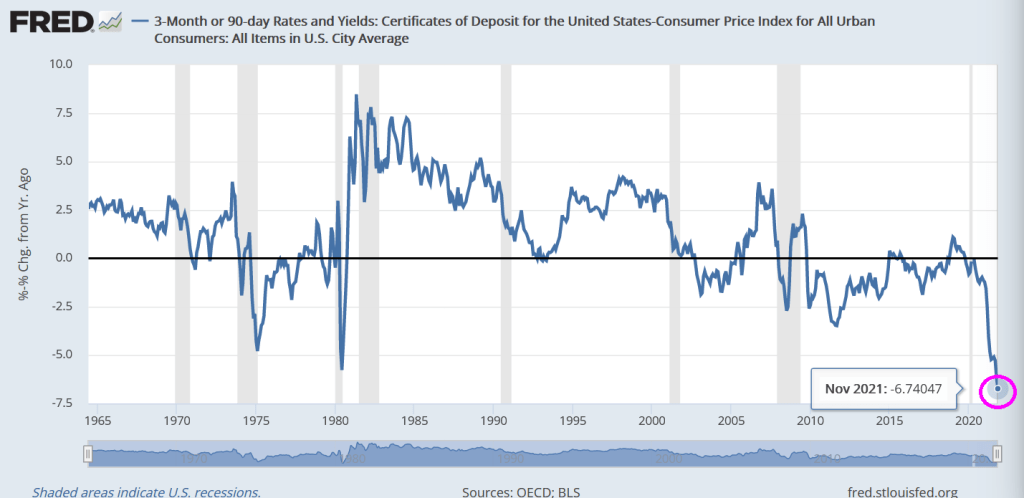

The Federal Reserve’s zero-interest rate policies (ZIRP) has The Fed Funds Target Rate at a measly 25 basis points or 0.25%. While this is great for some, it is disastrous for savers. Once we subtract off the inflation rate (CPI YoY), we find that the REAL 90-day Certificate of Deposit (CD) rate is a horrifying -6.74%.

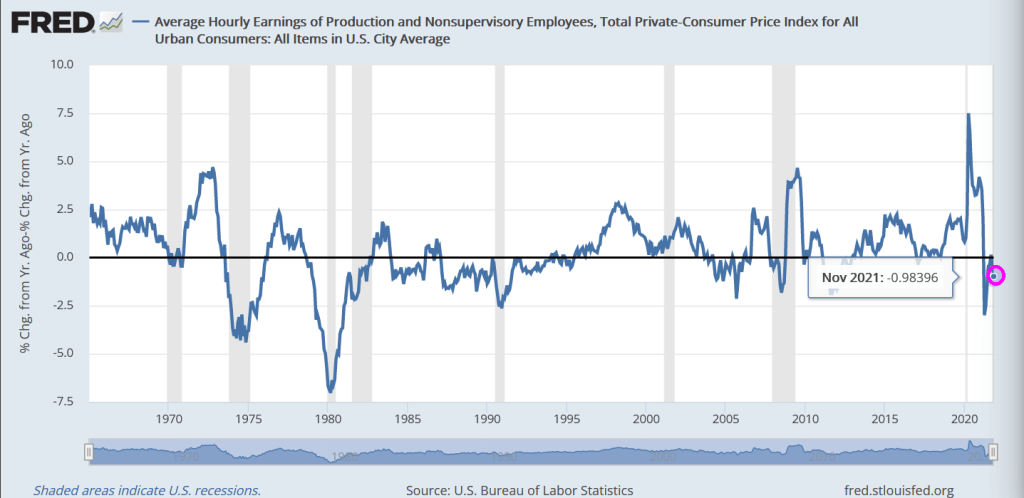

I don’t think that Congress or the Biden Administration really think about how their spending may contribute to inflation and crush savers. Or the American worker who is seeing NEGATIVE real average hourly earnings growth (yes, Biden said that Americans have more money this holiday season … but not if we account for reduced spending power, also known as inflation.

Here is US Treasury Secretary Janet Yellen singing “Goodbye Savers.”

Goodbye Savers Will we ever meet again Feel sorrow, feel shame Come tomorrow, feel lots of pain

I love how The Federal Reserve talking heads, the media, economists like Paul Krugman, all refer to inflation as “transitory” and excessive liquidity as “temporary.”

Let’s look at a variety of alternative investments to the S&P 500, GameStop, Bitcoin, Ethereum and Gold after The Federal Reserve’s and Federal government massive (over)reaction to COVID in early 2020. Gold is the first asset to surge after M2 Money surged, but has declined since. Game Stop had a big surge (likely due to positive vibes on Reddit), but has been volatile and generally falling since “The Surge.” Bitcoin had a delayed surge as did Ethereum. Despite fear about government regulation, Ethereum in particular remains elevated.

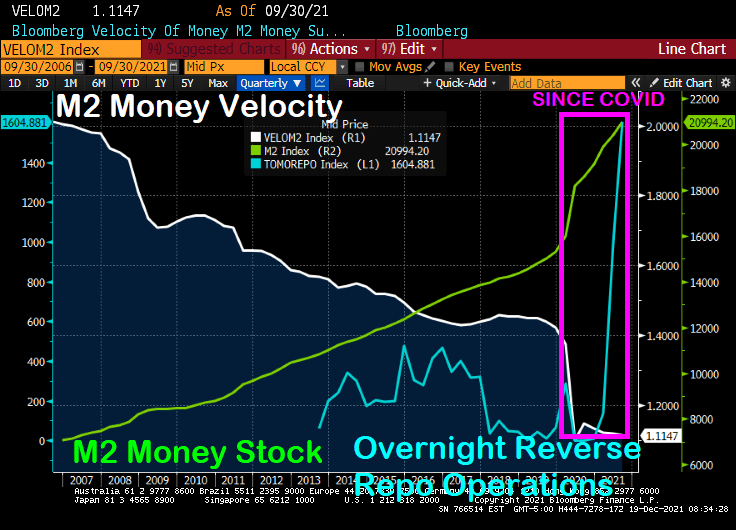

The “temporary” stimulus has resulted in the lowest M2 Money velocity in history. And we will have to see if the “temporary” excess liquidity in the financial system is truly temporary.

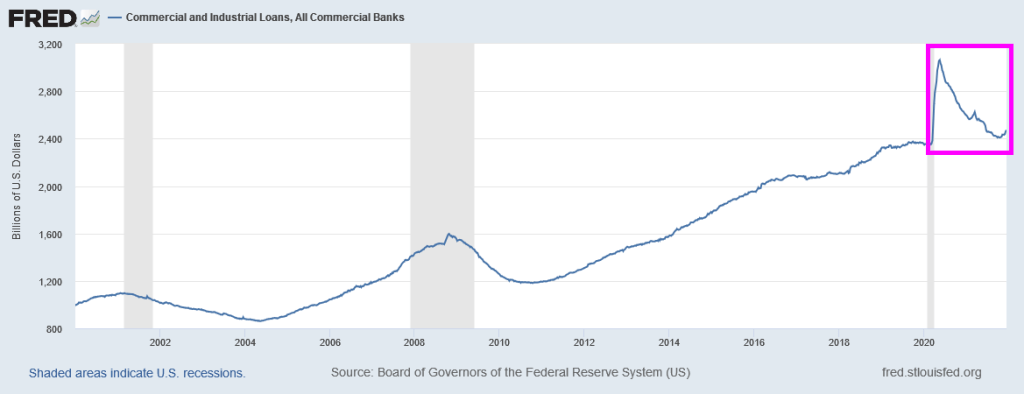

Here is a chart to show the “Stimulytpo” effect on commercial and industrial loans which surged (including PPP loans) but have simmered down to pre-COVID levels.

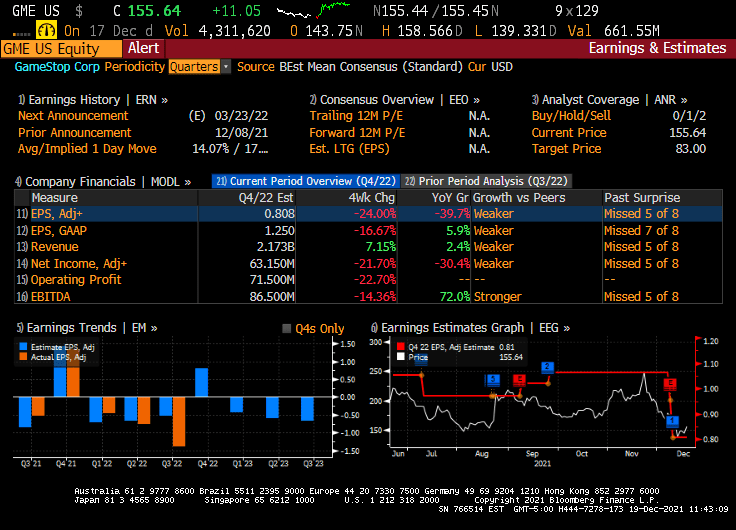

The earnings for GameStop were terrible (down 39.7% YoY). But at least Christmas season is upon us and maybe GameStop will surge with a good retail spending season.

But what happens to markets if the Federal government “stimulypto” is removed? If it ever is.

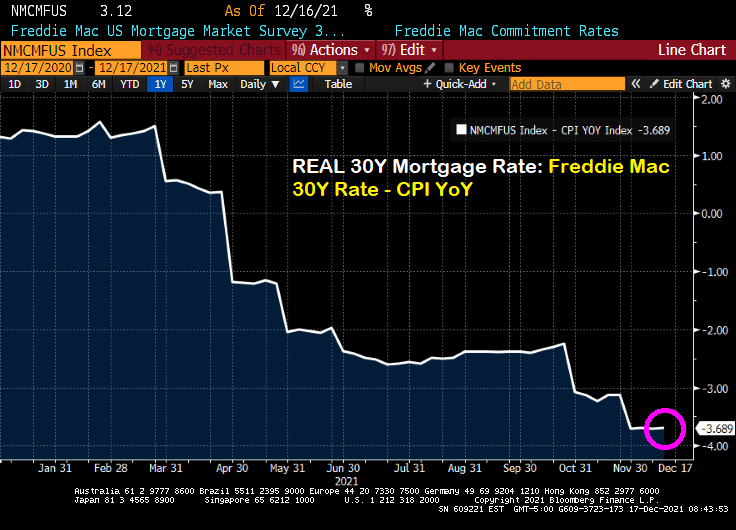

The Freddie Mac 30-year mortgage commitment rate rose to 3.12%. But once we subtract the gut-wrenching inflation rate, the REAL 30-year mortgage rate is -3.689%.

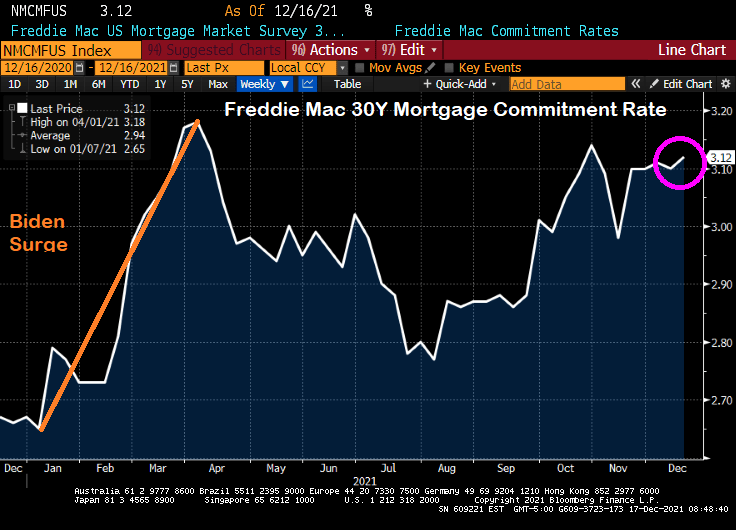

The nominal Freddie Mac 30-year commitment rate rose to 3.12% which is still lower than 3.18% back on April 1, 2021 after surge in rates following Biden’s taking the office of Presidency in January.

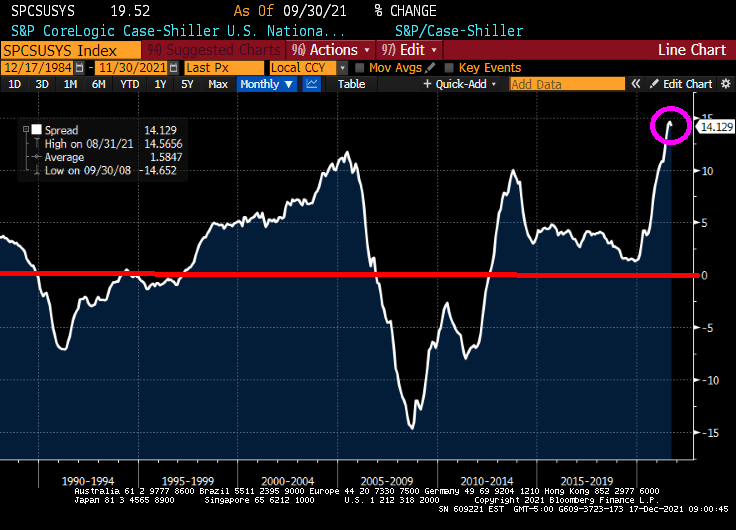

Meanwhile, the REAL Case-Shiller National home price index (CS National YoY – CPI YoY) is growing at the fastest rate in history. Great if you already own a home, but lethal if you are renting and want to move to homeownership.

Meanwhile, REAL wage growth is at -1.94% YoY.

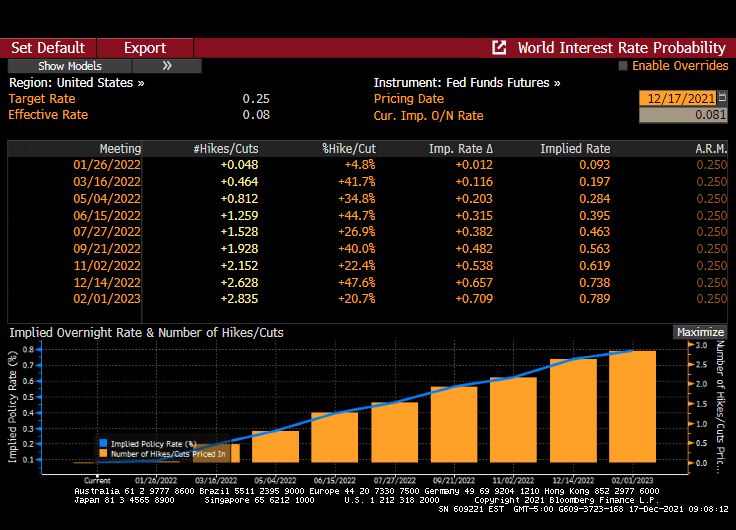

Well, Chairman Powell and The Gang failed to raise the Fed Funds Target Rate yet again, but let us know that they will tighten someday soon. The Fed Funds Futures are signalling a rate hike at the June 2022 meeting and another at the November meeting.

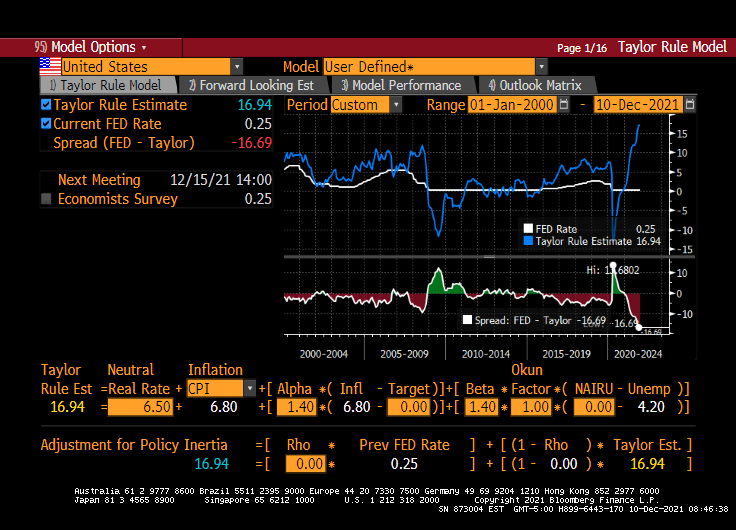

While The Fed couldn’t care less about the Taylor Rule, it is still interesting to note just how out of touch The Fed FOMC is with reality. The Taylor Rule indicates that their target rate should be 16.94% rather than the current target rate of 0.25%.

Keeping the target rate unchanged in the face of gut-wrenching inflation is a bold strategy, Cotton.

Like John Belushi from The Blues Brothers, Fed Chair Jerome Powell is saying that the markets lackluster response in terms of bond yields to his “hawkish” announcement yesterday “isn’t his fault.”

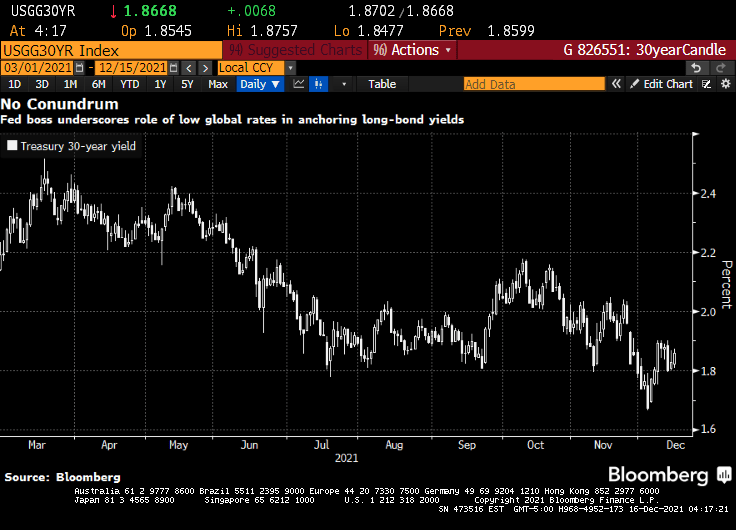

(Bloomberg)Federal Reserve boss Jerome Powell appears unperturbed by the fact that longer-term bond yields remain low even as officials lay the ground work for tighter policy and inflation is ticking higher.

While the drop in longer-term rates may be viewed by some as indicative of where so-called terminal rates for U.S. policy might ultimately lie, Powell on Wednesday emphasized the impact of ultra-low yields in places like Japan and Germany in helping to keep them anchored.

“A lot of things go into the long rates and the place I would start is just look at global sovereign yields around the world,” Powell said at a news conference following the Fed’s final scheduled policy meeting for the year, which saw officials ramp up the pace of stimulus withdrawal and boost predictions for rate hikes in 2022. The Fed Chair noted that rates on Japanese and German government bonds are “so much lower” than those on Treasuries and that with currency hedging taken into account American debt provides investors with a higher yield. “I’m not troubled by where the long bond is,” he said.

This stands as something of a contrast to the view expressed back in 2005 by one of Powell’s predecessors. Back then, Fed chief Alan Greenspan described a decline in long-term bond yields even in the face of six policy rate increases as a “conundrum.”

Or it could be that no one REALLY believes that Central Banks will ever cut interest rates, despite surging inflation.

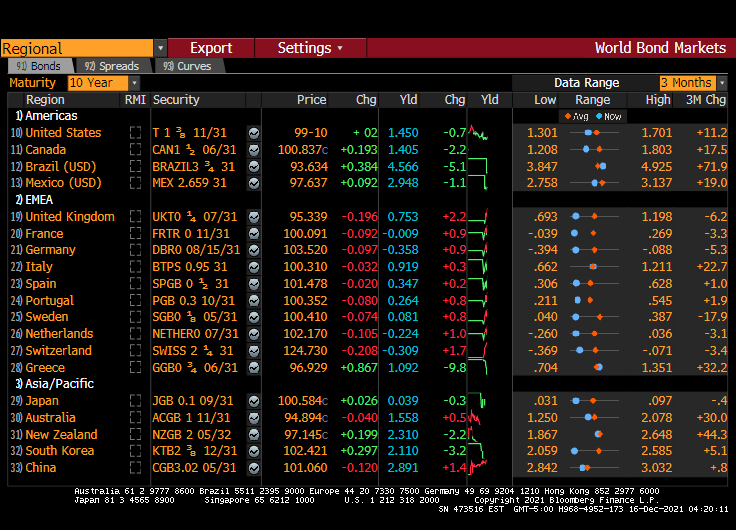

The US Treasury 10-year yield dropped 7 basis points overnight and remains just south of 1.50%. The Eurozone remains below 1% (with Germany at -0.358% and France at -0.009% at the 10-year mark). Japan is at 0.039%. This is what Powell means by low global rates keeping US long-term rates down.

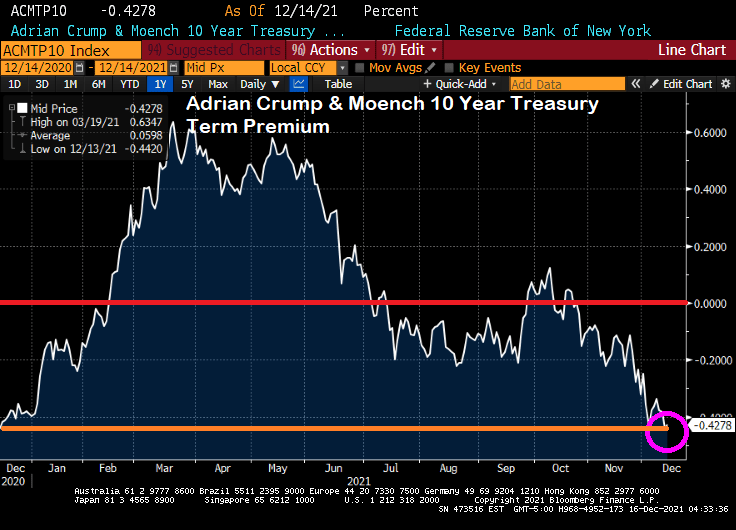

The 10-year Treasury term premium (measured before Powell’s head fake on raising rates) has returned to pre-Biden levels.

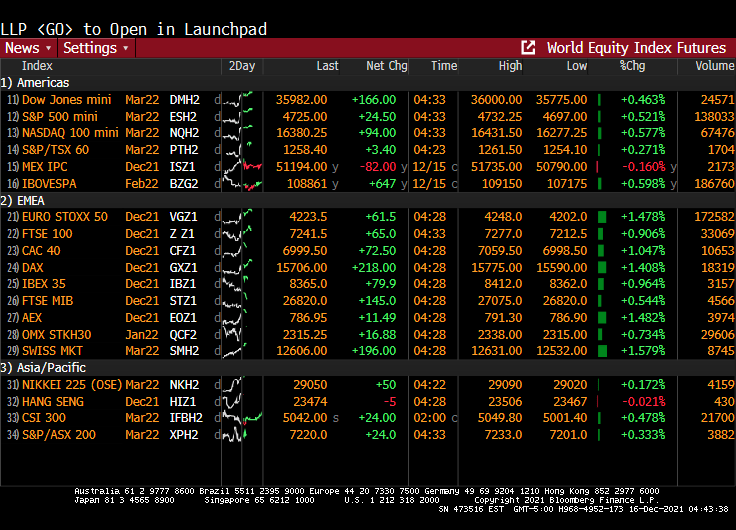

Meanwhile, global equities futures are up across the board (well, except for Mexico).

The Fed could have raised their target rate if they were REALLY interested in cooling inflation. The Taylor Rule remains at 14.94% while The Fed is stalled at 0.25%. Even if you don’t like the Taylor Rule, it still highlights how ridiculous Fed Stimulypto is.

Well, we do have a government-propelled economic recovery, but at a cost of declining REAL wages thanks to the highest inflation rate in 40 years.

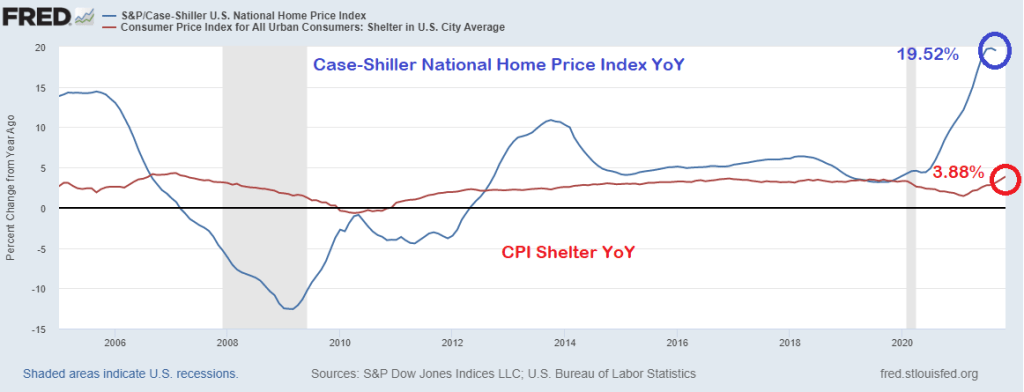

But that 6.9% YoY is very misleading because of the strange way the Bureau of Labor Statistics measures the largest asset in most households’ expenditures: housing.

The BLS measures inflation in housing using the Shelter measurement. Which was only 3.88% YoY. The problem is that the Case-Shiller National Home Price Index was 19.52% in its last reading. That is quite a discrepancy.

So, if we substitute the Case-Shiller National home price index for the CPI Shelter, we get an inflation rate of greater than 11%.

You must be logged in to post a comment.