December’s housing construction numbers are a mixed bag. On the one hand, US housing starts are down -1.36% from November to December, but down -21,8% since December 2021 (YoY).

The good news? 1-unit (single family detatched) rose 11.26% from November to December (MoM). But 5+ (multifamily) starts are down -18.91% MoM.

But 5+ unit PERMITS are up 7.14%. Perhaps Hunter Biden can now rent an apartment rather than pay his father $50,000 a month in rent for Joe’s Wilmington Delaware house.

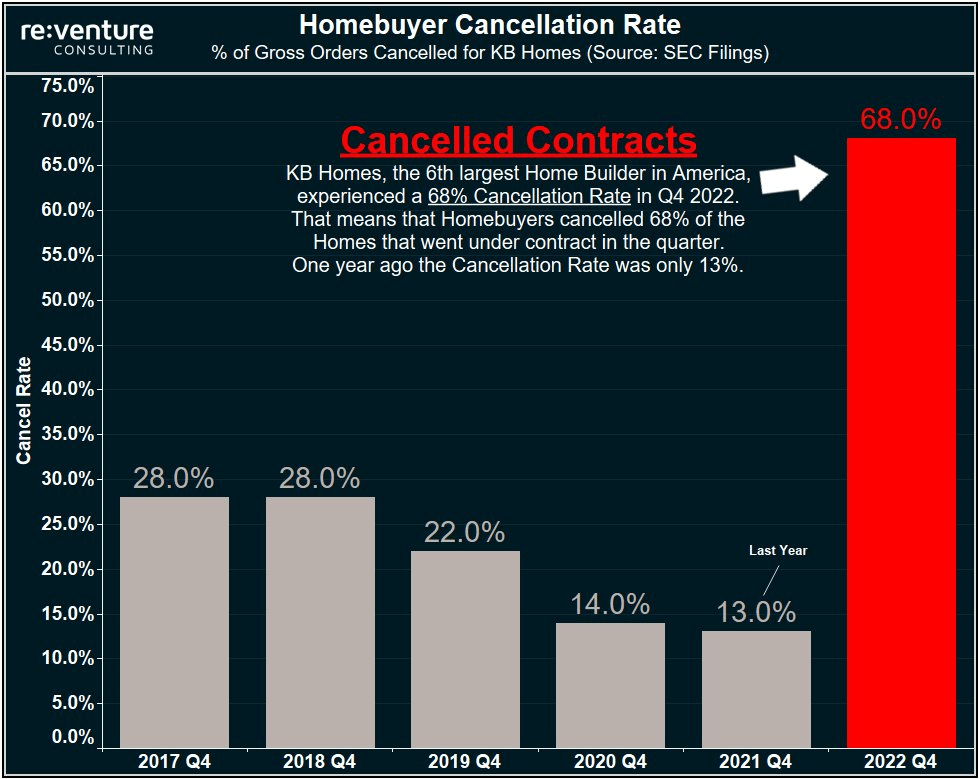

KB Homes experienced a 68% cancellation rate in Q4 2022.

This version of The Scream is one of four made by Edvard Munch, and the only one outside Norway. It is coming up for auction at Sotheby’s in New York.

The Federal Reserve continues to remove the monetary punch bowl despite the global yield curve inverting and The Fed fighting Bidenflation.

On the mortgage front, mortgage applications decreased 0.8 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending November 25, 2022. This week’s results include an adjustment for the observance of the Thanksgiving holiday.

The Refinance Index decreased 13 percent from the previous week and was 86 percent lower than the same week one year ago. The unadjusted Purchase Index decreased 31 percent compared with the previous week and was 41 percent lower than the same week one year ago.

On the housing front, US pending home sales fell for a fifth month in October as demand continued to sag under the weight of high mortgage rates.

The National Association of Realtors index of contract signings to purchase previously owned homes decreased 4.6% last month, according to data released Wednesday. And fell -36.7% YoY.

All together now. Look at pending home sales YoY and mortgage purchase applications SA compared with M2 Money YoY.

US mortgage rates fell last week by the most since the end of July, slipping below 7% and helping generate a bounce in purchase applications that otherwise remain depressed, but only in the Seasonally Adjusted data. The NON-Seasonally Adjusted data show a hefty decline.

The contract rate on a 30-year fixed mortgage decreased 24 basis points to 6.9% in the week ended Nov. 11, according to Mortgage Bankers Association data released Wednesday. The group’s index of applications to buy a home rose 4.4% — the most since June — but is still near the weakest level since 2015.

But the bounce was in Seasonally Adjusted data only. The NON-seasonally adjusted data remained depressed.

Mortgage applications decreased -10.0 percent SA from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending November 11, 2022. This week’s results include an adjustment for the observance of Veterans Day.

The Refinance Index decreased -11.44% percent from the previous week and was 88 percent lower than the same week one year ago.The unadjusted Purchase Index decreased -10 percent compared with the previous week and was 46 percent lower than the same week one year ago.

Mortgage purchase applications will continue to fall in NSA terms since it is the Winter and home buying season won’t really start until January. Refinancing applications actually dropped -11.44% even with the drop in mortgage rates.

The data. As my former students know, I like the “raw” data, better known as NON-seasonally adjusted (NSA) data and avoid seasonally-adjusted data (SA) since it hides what is going on.

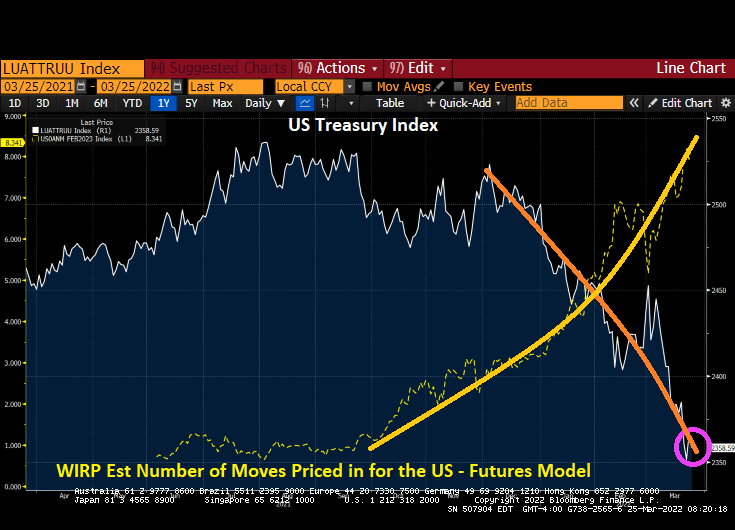

And on The Fed Futures Front, The Federal Reserve is still looking a hiking their target rate from 4% to just under 5%.

The University of Michigan’s consumer sentiment index for housing for October just fell to its lowest level since 1992 as The Fed counterattacks against Bidenflation, causing mortgage interest rates to rise.

Of course, despite slowing home price growth, expensive home prices are really hurting along with expensive rents. But how sustainable are high home prices when REAL average hourly earnings growth is negative??

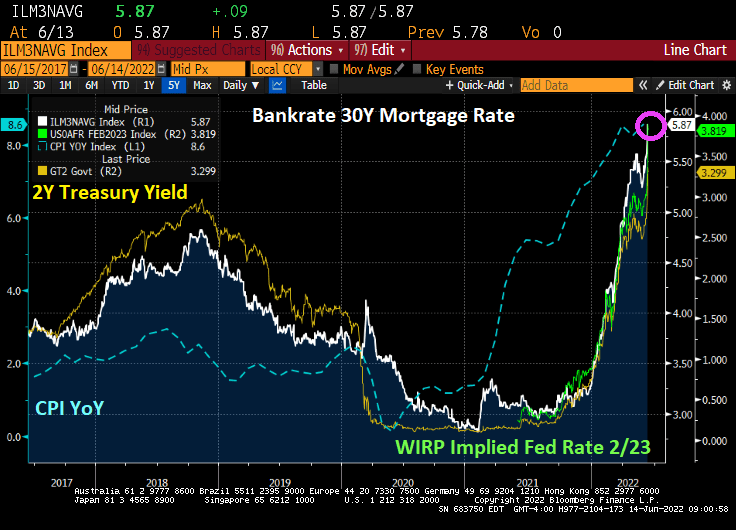

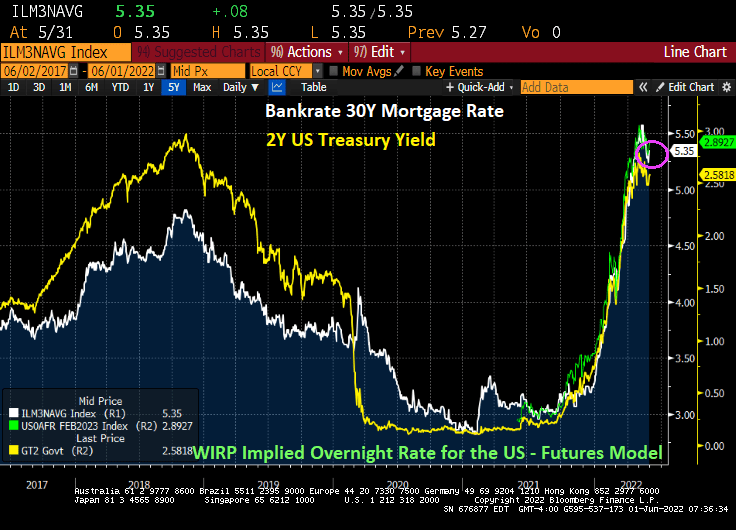

Another casualty of The Fed’s tightening and reduction in M2 Money supply are … the mortgage and housing markets. The US mortgage rate has soared to 7.04% (highest since 2000) and mortgage DEMAND has fallen to the lowest level in recorded history.

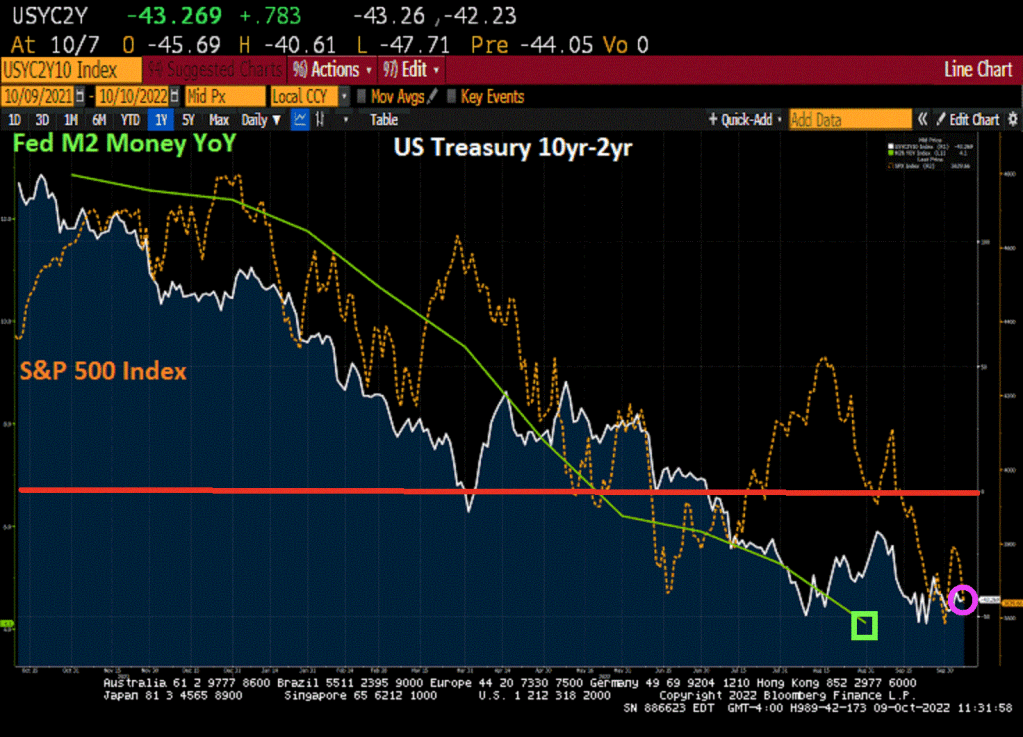

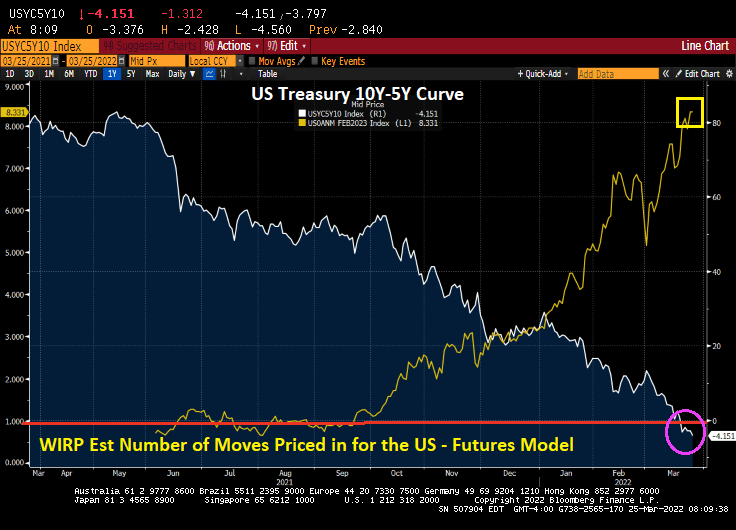

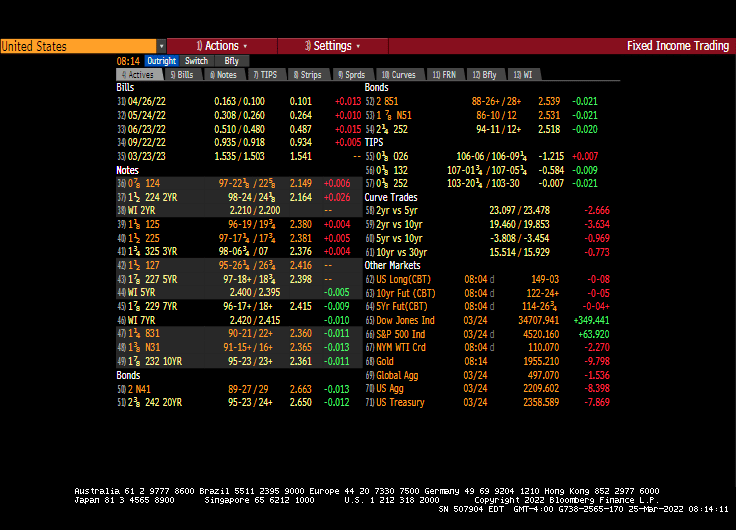

Here is my chart from yesterday showing the inversion of the US Treasury 10yr-2yr curve and decline in the S&P 500 index as The Fed tightens.

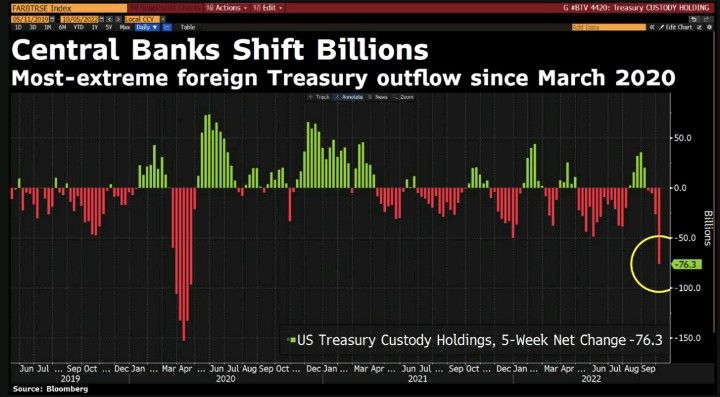

And then we have this chart showing the most-extreme foreign Treasury outflow since March 2020.

At least The Fed is predicted to start cutting rates again in March 2020.

Yes, Biden and Powell have reenacted Kevin’s famous chili spill. And Ben Bernanke, the creator of QE from late 2008 was just award the Nobel Prize in economics for distorting financial markets.

As the Biden Administration touts “affordable housing,” we are seeing the 30-year mortgage rate rise above 7% as The Federal Reserve fights inflation … caused by the Biden Administration. Meanwhile, US home prices are falling.

The Biden Administration launched a war on domestic energy production, resulting in crude oil prices rising 74% under Biden and regular gasoline prices rising 62.4%.

As Biden pleaded with OPEC to increase oil production, he was embarrassingly rejected. Hence, West Texas Crude Oil prices have begun to rise again along with gasoline prices (pink box).

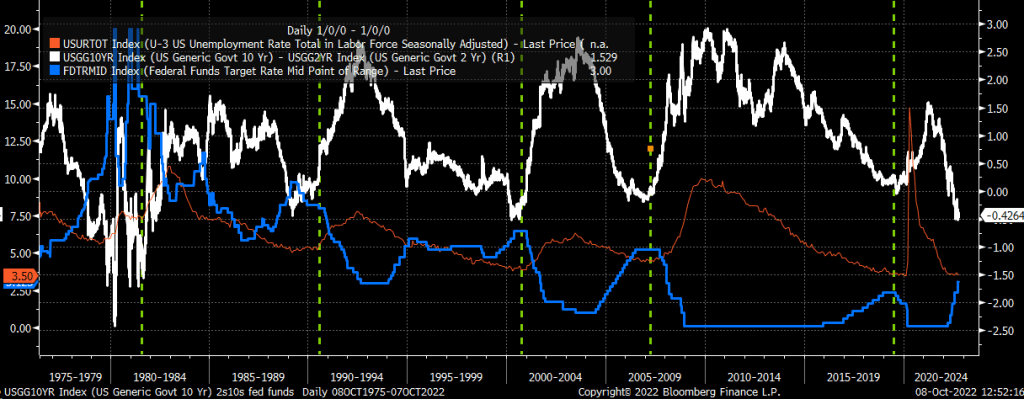

How about unemployment and the 10yr-2yr yield curve?

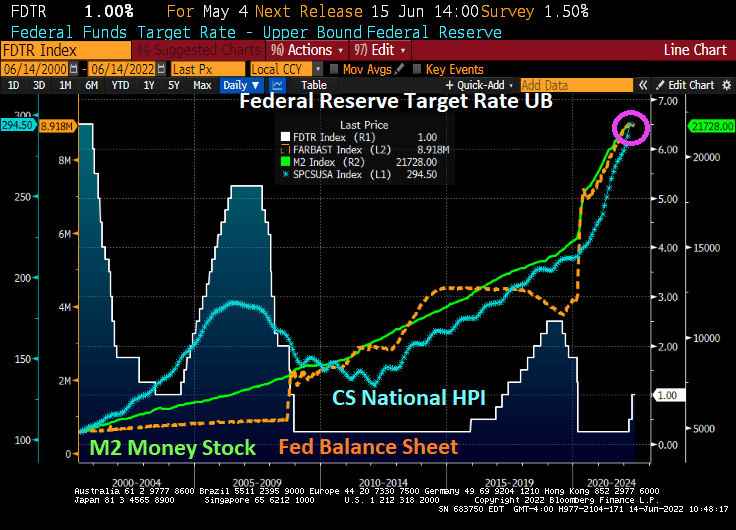

US home prices are still skyrocketing as The Federal Reserve kept its massive foot on the monetary accelerator pedal.

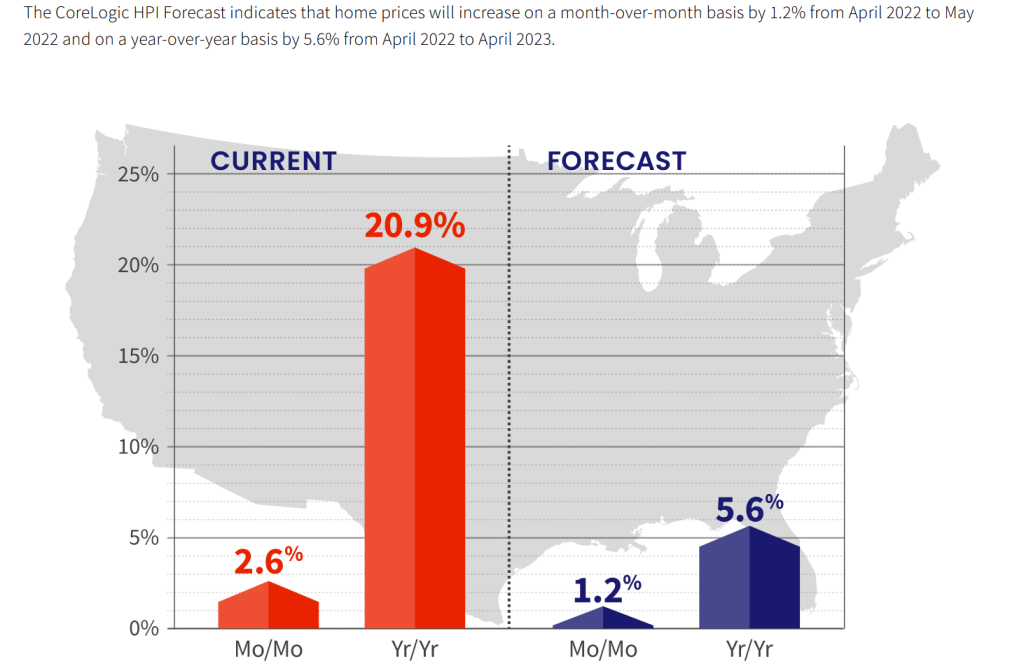

CoreLogic’s home price index grew at a 20.9% YoY pace in April, but is expected to slow to 5.6% YoY in late 2022.

Remember peeps, The Fed still have its staggering monetary stimulypto in place.

The Fed is signaling its withdrawal of stimulus, causing mortgage rates to soar.

Given the slowdown of the US and global economy, we shall see if The Fed keeps to its tightening plans. As of today, the market is expecting The Fed to raise its target rate from 1% to 3.819% by February 2023. That is a 291% increase in The Fed’s target rate.ng

The Fed trying to tame inflation (caused by The Fed and Biden’s energy policies and Congressional spending) is like Curly trying to eat oyster stew.

Heartaches By The Number … for American households and mortgage lenders as The Federal Reserve begins FINALLY removing monetary stimulus.

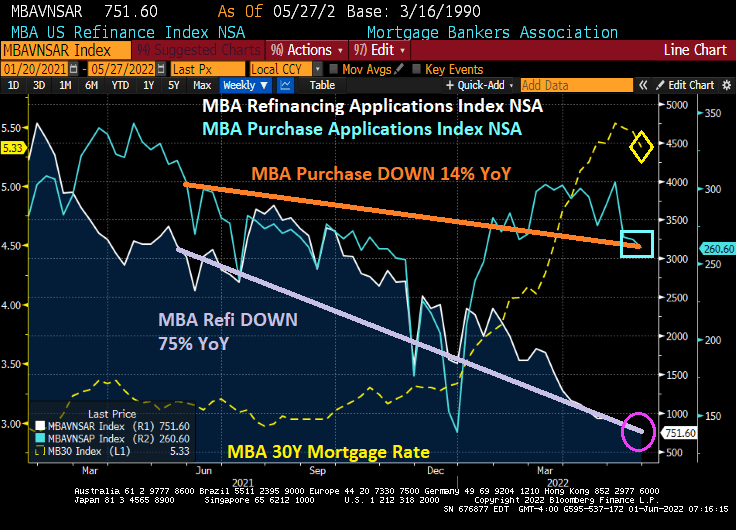

Mortgage applications decreased 2.3 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending May 27, 2022.

The Refinance Index decreased 5 percent from the previous week and was 75 percent lower than the same week one year ago.

The seasonally adjusted Purchase Index decreased 1 percent from one week earlier. The unadjusted Purchase Index decreased 2 percent compared with the previous week and was 14 percent lower than the same week one year ago.

Under Biden, mortgage refi applications are down -82.4%, purchase applications are down -7.5% and mortgage rates are up +80.7%.

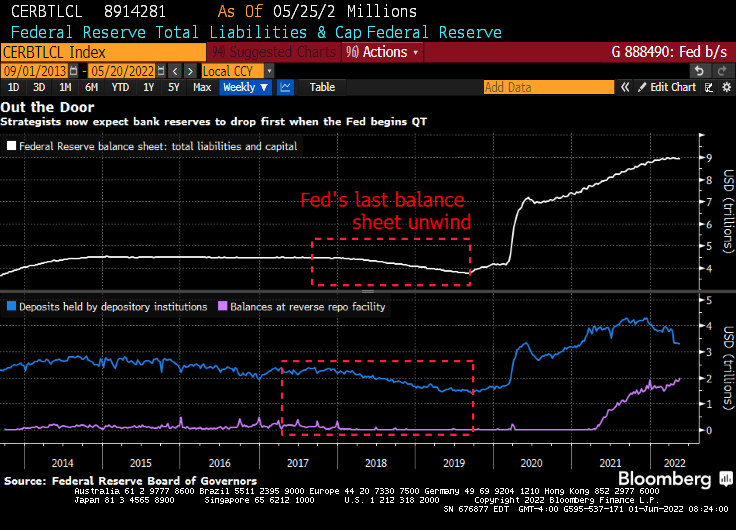

Then we have this headline: “Fed Starts Experiment of Letting $8.9 Trillion Portfolio Shrink”

The Fed is capping monthly runoff at $47.5 billion — $30 billion for Treasuries and $17.5 billion for mortgage-backed securities — until September. Those thresholds will then double to a combined $95 billion. That compares to a peak of $50 billion a month when the Fed performed the exercise starting in 2017.

As expectation of Fed rate hikes increase, mortgage rates have soared like Tom Cruise’s Super Hornet aircraft from Top Gun: Maverick climbing over the steep mountain.

And mortgage rates are up a bit today.

Meanwhile, The Federal Reserve begins shrinking their balance sheet for the first time since Yellen and company started shrinking it under Trump.

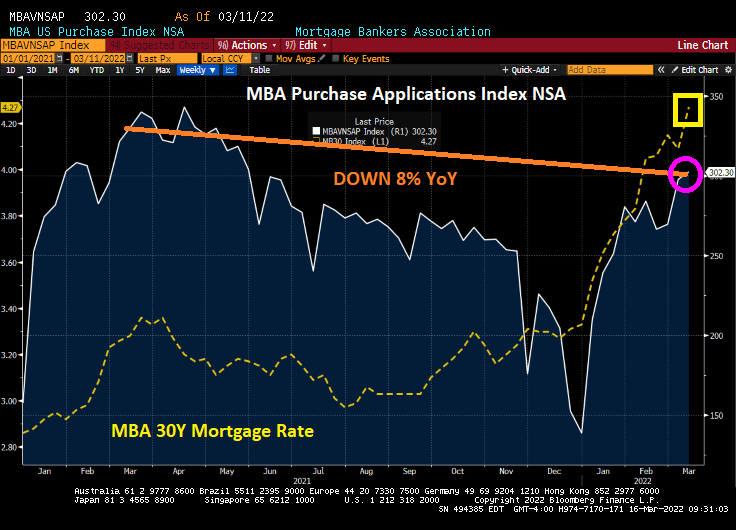

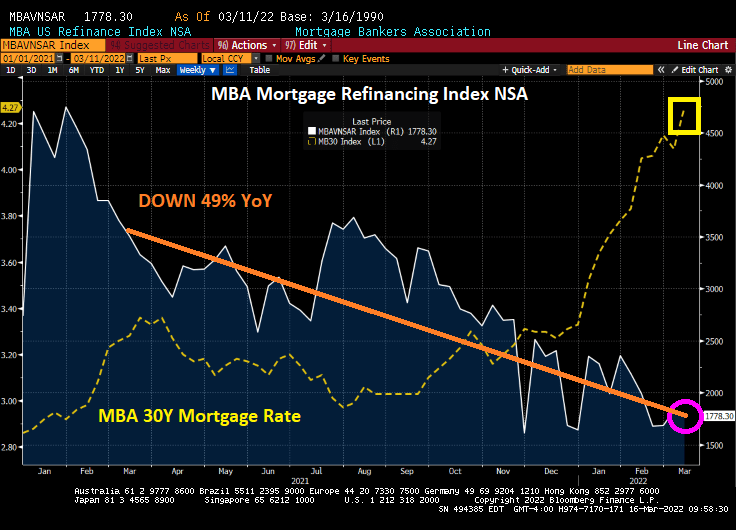

Mortgage applications decreased 1.2 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending March 11, 2022.

The seasonally adjusted Purchase Index increased 1 percent from one week earlier. The unadjusted Purchase Index increased 2 percent compared with the previous week and was 8 percent lower than the same week one year ago.

The Refinance Index decreased 3 percent from the previous week and was 49 percent lower than the same week one year ago.

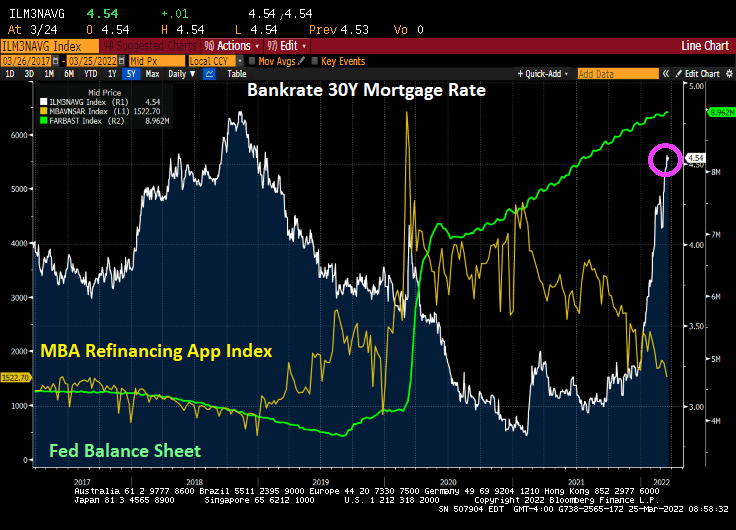

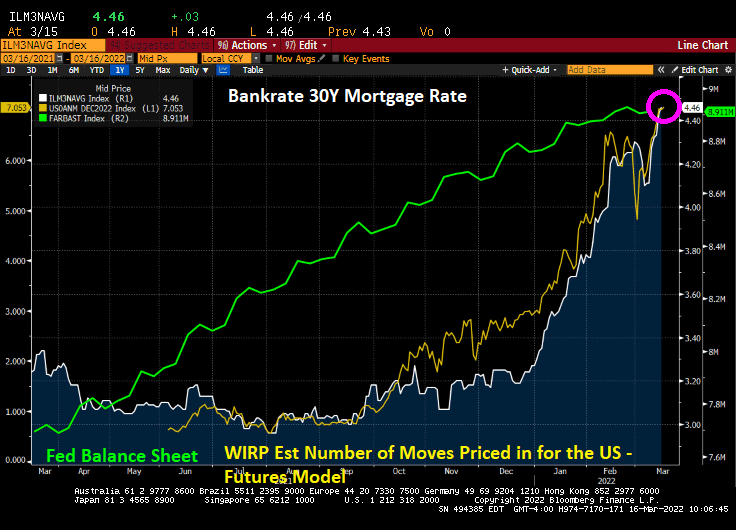

Bankrate’s 30-year mortgage rate has surged to 4.46%.

Here is a photo of alligators in Great Falls, Virginia, up-river from Washington DC. They are likely congregating for the Fed Open Market Committee (FOMC) announcement today.

You must be logged in to post a comment.