As part of the Biden administration’s plan to make housing affordable for everyone (we’ve seen this story before), upfront fees for loans backed by Fannie Mae and Freddie Mac will be adjusted based on the borrower’s credit score. Borrowers with high credit scores will pay more in fees, while those with lower credit scores will pay less.

The Wall Street Journal cited data from Evercore ISI that shows borrowers with credit scores between 720-759 who make around 15-20% down payments will see loan-level pricing adjustment (LLPA) costs rise by .750%. Inversely, under the new adjustments, risky borrowers with a credit score below 639 and who put down only 5% of the value of their home will only have to pay 1.750%, compared with 3.750% under old rules.

Backlash over LLPA changes prompted the FHFA to publish a statement last week, calling such concerns “a fundamental misunderstanding.” The Biden administration ensures the new changes are meant to help those with poor credit scores obtain homes amid the worst housing affordability in a generation. Note that Biden did not speak on this himself since he would undoubtedly get confused and call people names. And get lost leaving the podium.

According to the FHFA, the new adjustments will redistribute funds to reduce the interest rate costs paid by risky borrowers. This sounds like socializing home buying to us.

Even more alarming is data from the American Enterprise Institute found that default rates of Fannie/Freddie owner-occupied 30-year fixed-rate purchase loans acquired in 2006-2007 were between 39.3% and 56.2% for borrowers with credit scores between 620 and 639 and less than 4% down payments. Those with credit scores between 720 and 769 and 20% down payments had default rates between 4.2% and 8.8%.

Joe Biden’s new nickname is “The Punisher.” Not only for this sick and twisted theft from people who work hard and are careful with their credit, but also for his crazy obsession with going green and driving energy prices (and inflation) through the roof.

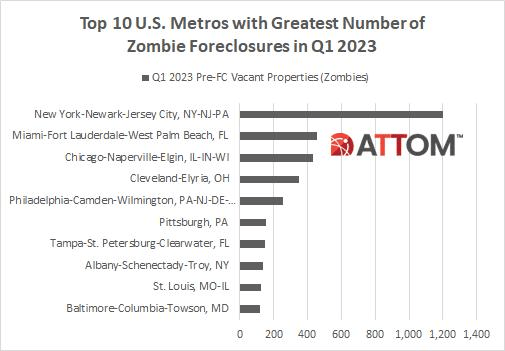

A zombie foreclosure refers to a situation where a homeowner vacates their property after receiving a notice of default, expecting they will lose the home in the pending foreclosure. The foreclosure may get canceled for any number of reasons and never completed.

New York City and its surrounding areas lead the nation in zombie foreclosures. Followed by Miami. Chicago and Cleveland. Then Philadelphia.

US inflation is the highest in 40 years, yet inflation may be slowing as 1) The Fed cranks up interest rates and 2) the global economy is slowing.

US inflation data in the coming week may stiffen the resolve of Federal Reserve policy makers to proceed with another big boost in interest rates later this month.

The closely watched consumer price index probably rose nearly 9% in June from a year earlier, a fresh four-decade high. Compared with May, the CPI is seen rising 1.1%, marking the third month in four with an increase of at least 1%.

While persistently high and broad-based inflation is seen persuading Fed officials to raise their benchmark rate 75 basis points for a second consecutive meeting on July 27, recession concerns are mounting. There are signs, though, that price pressures at the producer level are stabilizing as commodities costs — including energy — retreat.

But the expectations of inflation, as measured by The Fed’s 5-year forward breakeven inflation rate, just crashed to 1.8437%.

The breakeven inflation rate is a market-based measure of expected inflation. It is the difference between the yield of a nominal bond and an inflation-linked bond of the same maturity.

The USD Inflation Swap Forward 5Y5Y is also falling like a rock as The Fed hikes their target rate (green line).

Could it be that inflation is cooling with Fed rate hikes (but not the shrinking of their $8 trillion balance sheet)?

Currently, Fed Funds Futures are pointing to a Fed target rate of 3.552% by February 2023. And with that, Bankrate’s 30-year mortgage rate rose to 5.75%. Once again, like velociraptors from Jurassic Park, The Fed’s balance sheet is still out in force.

Fed Chair Jerome Powell and Atlanta Fed President Raphael Bostic are keeping The Fed’s balance sheet at near $9 trillion as they hunt assets to inflate.

You must be logged in to post a comment.