More bad news about the economy and housing sector under Biden/Yellen/Powell’s Reign of Economic Error.

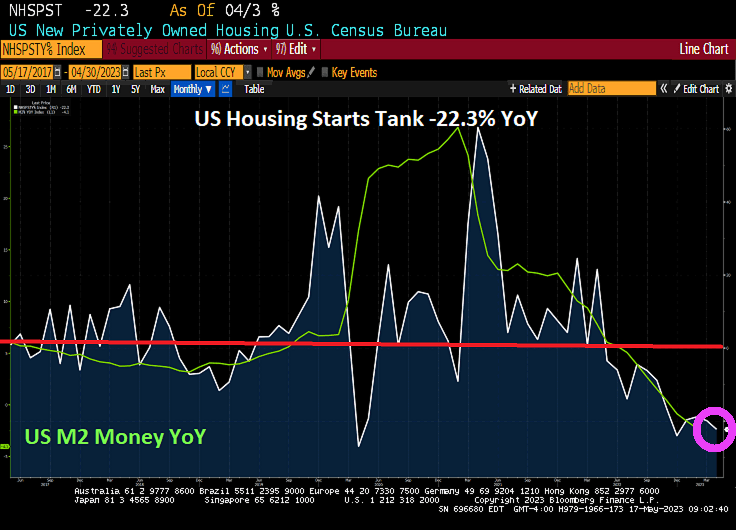

US housing starts are out for April 2023. The bad news? Housing starts tanked -22.3% year-over-year (YoY).

The good news? US housing starts were up 2.19% from March to April. 1-unit detached starts were up 1.56% MoM while 5+ unit starts up 5.24% MoM. Permits for multifamily were down -9.71% from March to April.

The media will no doubt try to ignore the horrifying Durham Report. The report showed that Hillary Clinton and the Obama administration knowingly smeared Presidential candidate Donald Trump with false Russian misinformation and knowingly tried to steal an election. I wonder if Attorney General Merrick Garland will open an investigation into Hillary Clinton’s involvement in election tampering? Oh wait, the IRS was told to stop investigating Hunter Biden’s nefarious dealings. Never mind.

On the corporate side, US bankruptcies in 2023 had the worst start to a year since 2010 and the financial crisis.

On the personal finance side of the ledger, the delinqueny rate on credit cards is growing at the faster rate since 2010.

Throw in 22 straight months of negative REAL wage growth, and have a scary situation facing middle America.

And the shate of outstanding subprime auto debt (30 days or more delinquent) is up to the highest rate since … well, you know when. The financial crisis of 2009-2010.

There was a hilarious film with Hillary Swank and Aaron Ekhart called “The Core” where earth’s core stops spinning and the earth gets cooked by the Sun’s rediation. Now we learn that the Earth’s inne core has actually stop spinning. This time, however, all that has happened is that Joe Biden is President which is almost as bad,

But also related to “The Core” is that the important Personal Consumption Expenditures (PCE) are out for December along with PCE price deflator numbers. In short, personal income was up 0.2% month-over-month (MoM) in December while personal spending was down -0.2%. REAL personal spending was down -0.3% MoM.

But the all important PCE deflators numbers were down all well. The REAL PCE price index (or deflator) was down to 5.0% YoY in Decmember while REAL CORE price index was down to 4.40%. All this is happening as M2 Money growth has stop spinning (down to -1.3% YoY in December).

Based on a CORE PCE YoY of 4.40%, the Taylor Rules suggest that The Fed Fund Target rate should be … 10%. However, the current Fed Funds Target rate is only 4.50%, so The Fed is not even half way there.

Fed Funds Futures are pointing to a peak rate of 4.90% by the June ’23 FOMC meeting, then a pivot (despite denials from Fed talking heads).

Of course, The Fed doesn’t follow the Taylor Rule or any other transparent rule for rate management. Rather, Fed Chair Powell like former Chair (and current Treasury Secretary Janet Yellen) follow a more seat-of-the-pants approach.

No problemo, says James “Bully” Bullard, President of the St Louis Federal Reserve. Bullard said that US recession fears are overblown with consumers “healthy.”

Really Jim?

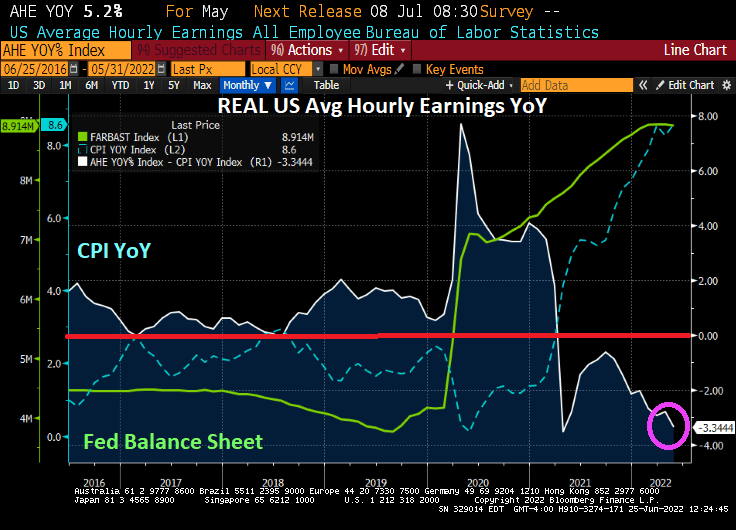

Inflation is so bad they REAL average hourly earnings growth keeps falling and is now -3.34% YoY.

Apparently, real GDP growth of ZERO doesn’t bother Bullard either.

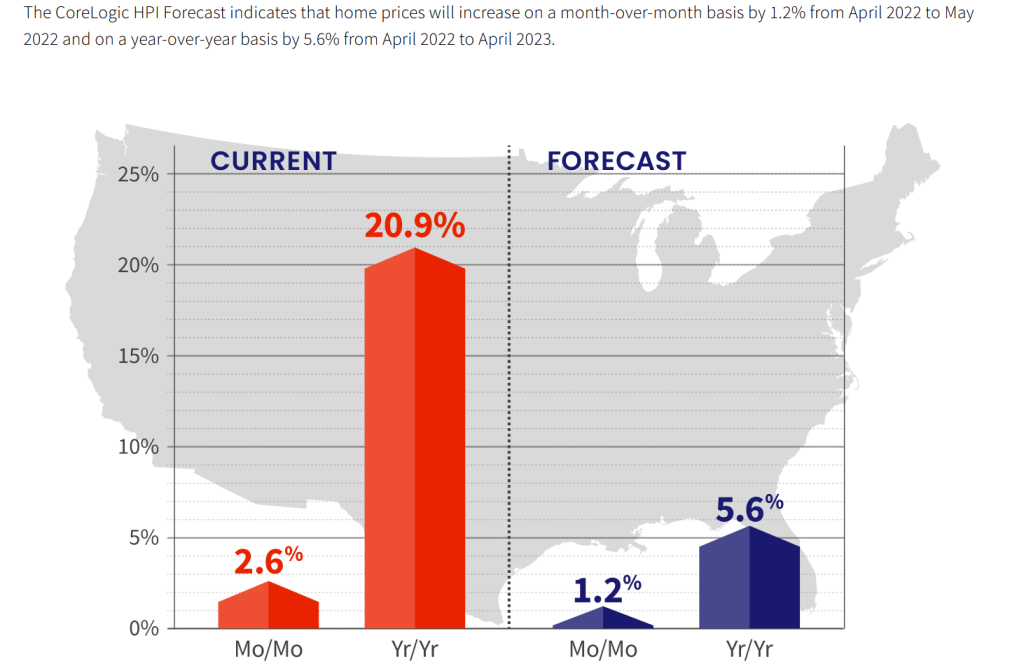

US home prices are still skyrocketing as The Federal Reserve kept its massive foot on the monetary accelerator pedal.

CoreLogic’s home price index grew at a 20.9% YoY pace in April, but is expected to slow to 5.6% YoY in late 2022.

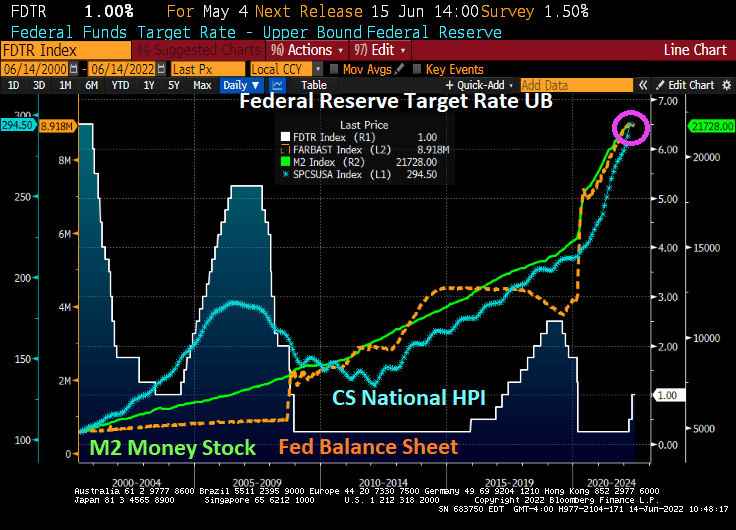

Remember peeps, The Fed still have its staggering monetary stimulypto in place.

The Fed is signaling its withdrawal of stimulus, causing mortgage rates to soar.

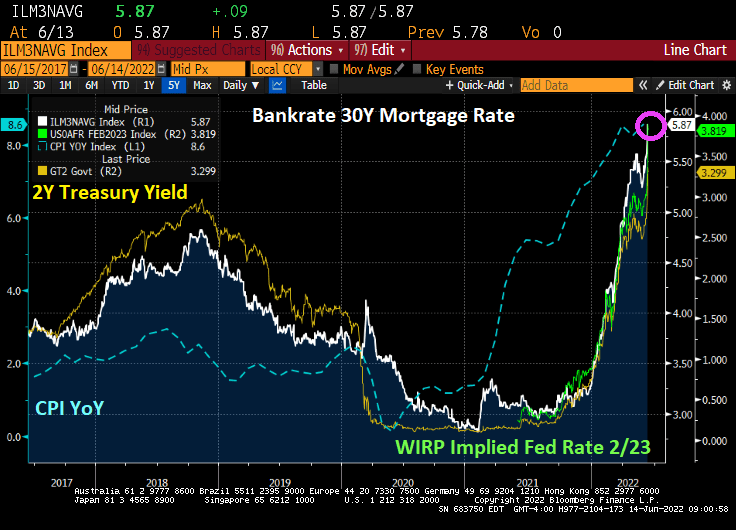

Given the slowdown of the US and global economy, we shall see if The Fed keeps to its tightening plans. As of today, the market is expecting The Fed to raise its target rate from 1% to 3.819% by February 2023. That is a 291% increase in The Fed’s target rate.ng

The Fed trying to tame inflation (caused by The Fed and Biden’s energy policies and Congressional spending) is like Curly trying to eat oyster stew.

The CPI news on Friday was so awful that it changed the bond market’s view of Fed trajectory, and the weakest sector broke. In bond jargon, MBS went “no-bid.”No buyers for MBS. Then a few posted prices beyond borrower demand, not wanting to buy except at penalty prices. (Courtesy of Cherry Creek Mortgage)

Despite what Treasury Secretary Janet Yellen has said, Friday’s inflation report demonstrated that inflation is no longer transitory. And with that realization, there was a dearth of bidders for Agency Mortgage-backed Securities (Agency MBS) on Friday.

As a result, agency MBS 2.5% dropped to under $90 as markets expect The Fed to keep raising rates to combat inflation.

Duration of the FNCL 2.5% agency MBS has been extending with growing inflation. Duration was under 1 on August 2, 2021 but is now 7 times greater at almost 7.

Note to Yellen: inflation seems be permanent, not transitory. Or at least inflation will remain high for the foreseeable future, crushing the life out of Agency MBS.

You must be logged in to post a comment.