The US is teetering on World War III with tensions soaring in the Middle East, Ukraine, and southeast Asia. And Biden wanders off to Rehobeth Beach Delaware to relax … while over 200 Americans are still held hostage by terrorist group Hamas. The bad news? Biden is back in Washington DC trying to make the border crisis even worse by demanding funding for “border security” in the form of transporting illegal immigrants to US cities. Is The Squad running The White House??

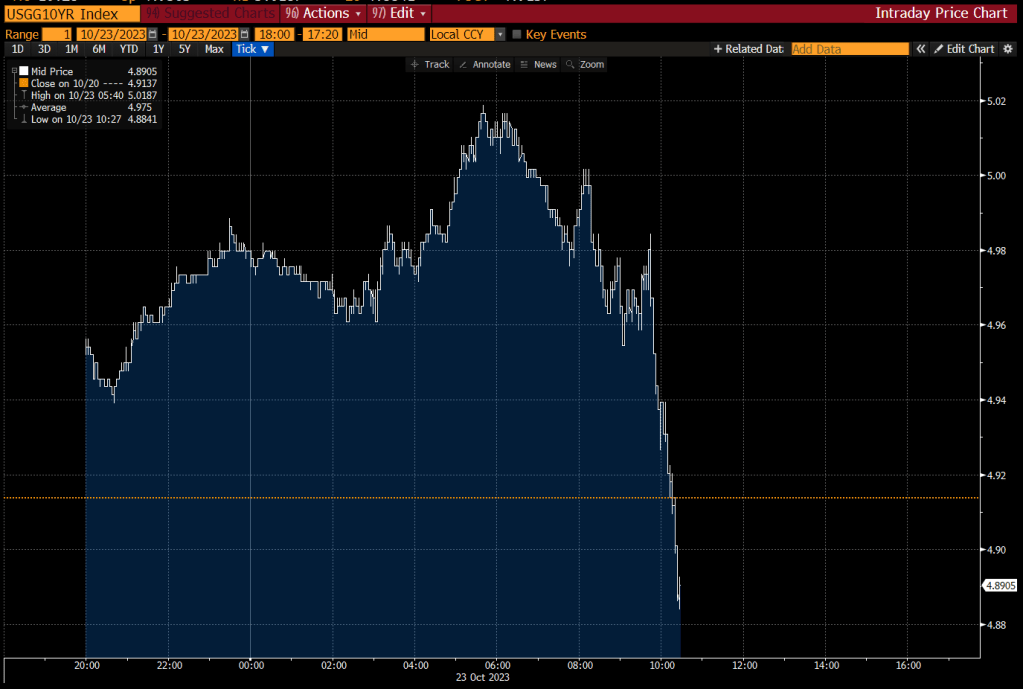

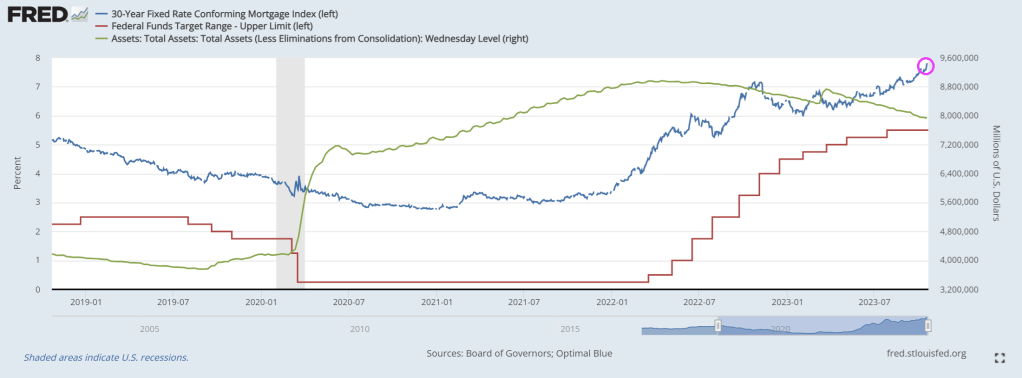

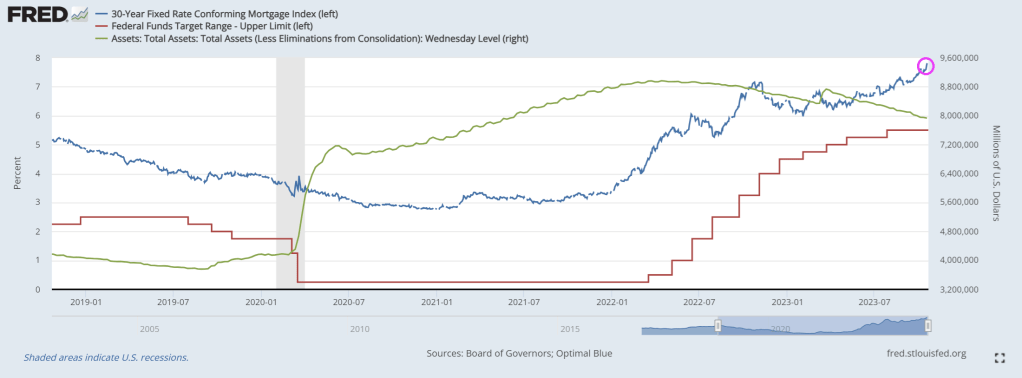

But on the housing/mortgage front, we have another week of declining mortgage demand/applications as mortgage rate hit almost 8%.

Mortgage applications decreased 1.0 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending October 20, 2023.

The Market Composite Index, a measure of mortgage loan application volume, decreased 1.0 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 1 percent compared with the previous week. The Refinance Index increased 2 percent from the previous week and was 8 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 2 percent from one week earlier. The unadjusted Purchase Index decreased 2 percent compared with the previous week and was 22 percent lower than the same week one year ago.

Mortgage rates followed Treasuries higher, with the 30-year fixed mortgage rate jumping 20 basis points to 7.9 percent – the highest since 2000. Rates have now risen seven consecutive weeks at a cumulative amount of 69 basis points.

Hey Joe, I’ll bet those 200+ US hostages held by Hamas aren’t enjoying ice cream cones.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.