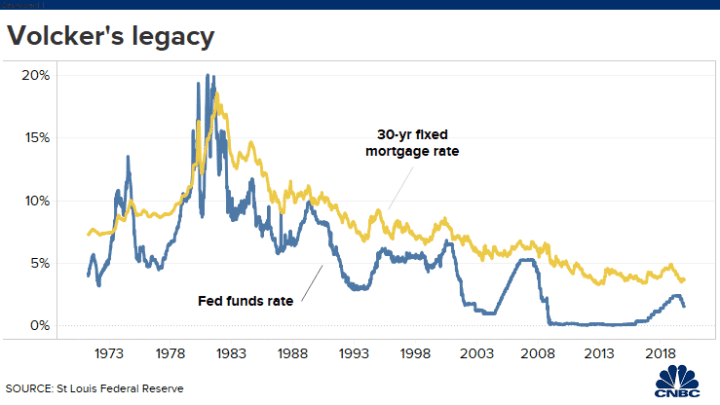

I had a wonderful time speaking at the Passive Investors Conference last night. One question I was asked was “Why doesn’t Powell (the current Fed Chair) pull “a Volcker” to cool inflation. She was referring to former Fed Chair Paul Volcker’s sudden raising of The Fed’s target rate which resulted in a cooling of inflation, but also an increase in the 30-year fixed mortgage rate to 16.63% in 1981.

Notice the trend in the Fed’s target rate and 30-year mortgage rate after Volcker’s rate shock. The trend in both has been downward as inflation was cooled.

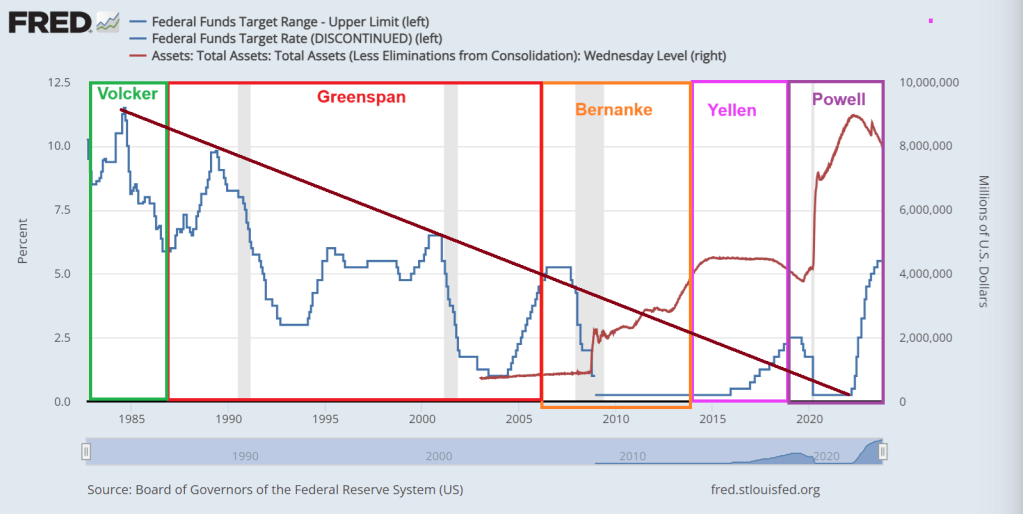

But, each Fed Chair ranged from hyperactive to hypoactive (meaning doing little). Volcker and Greenspan saw wild swings in The Fed’s target rate. Bernanke pretty much only lowered rates AND expanded the Quantitative Easing (QE) or asset purchases by The Fed. And nothing has been the same since.

Yellen, now Treasury Secretary, continued Bernanke’s practice of zero interest rate policies (ZIRP) and QE (asset purchases) … until Donald Trump was elected President. In fact, Yellen raise rates only once prior to Trump’s election as President. Then raises rates 8 consecutive times. This is why I call Yellen “TLTL Janet”. Too low for too long Janet.

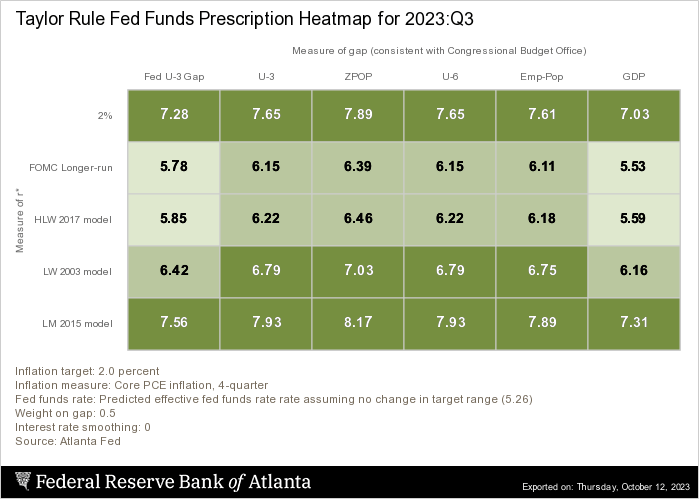

The she was replaced with DC insider Jerome Powell. Trump’s economy was strong (one explanation for Yellen trying to cool the economy with 8 consecutive rate hikes). But the Covid struck and Powell/Fed Open Market Committee overreacted, lowered the target rate back to 25 basis points and massively expanded the balance sheet. Powell also oversaw a rapid increase in the target rate, very Volckerish! But Powell stopped short of the rate suggested by The Taylor Rule of around 6.5% to 8.17%. The current target rate is 5.50%. So, Powell stopped far short of rates need to cool inflation.

But with Bidenomis came Bidenflation and a reversal of misfortunes for The Fed. They started rapidly raising rates … again.

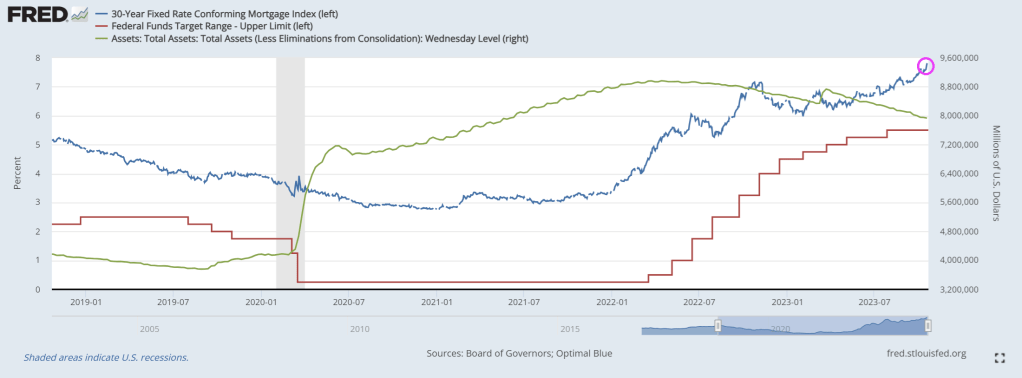

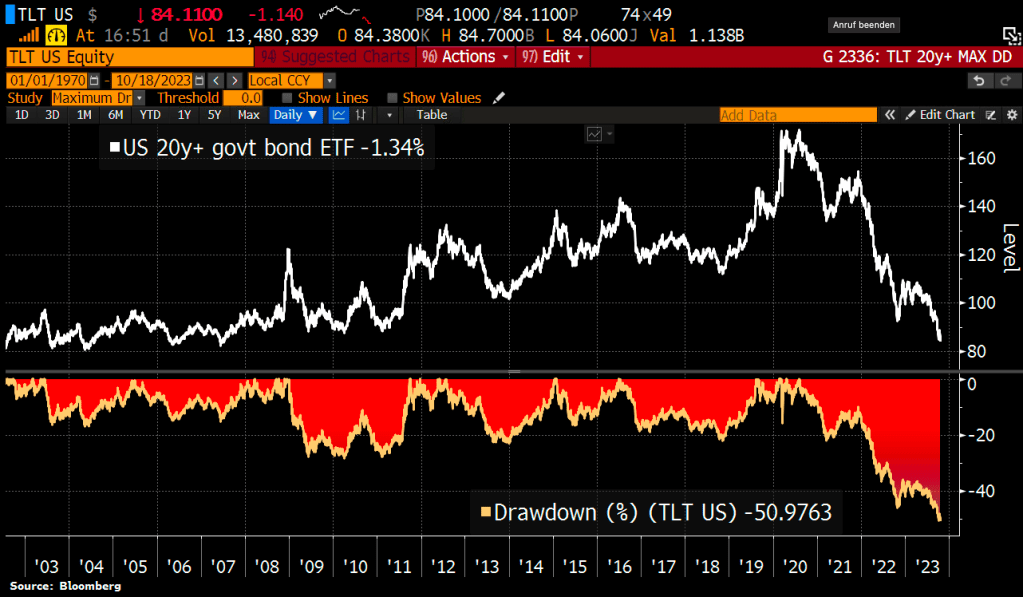

Mortgage rates continue to climb as The Fed stubbornly won’t reduce its balance sheet.

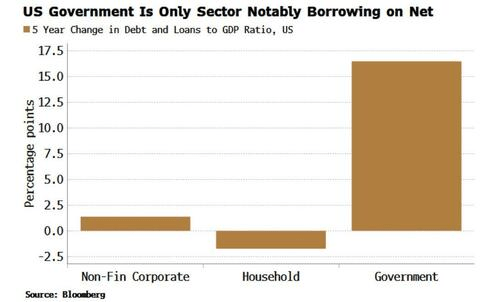

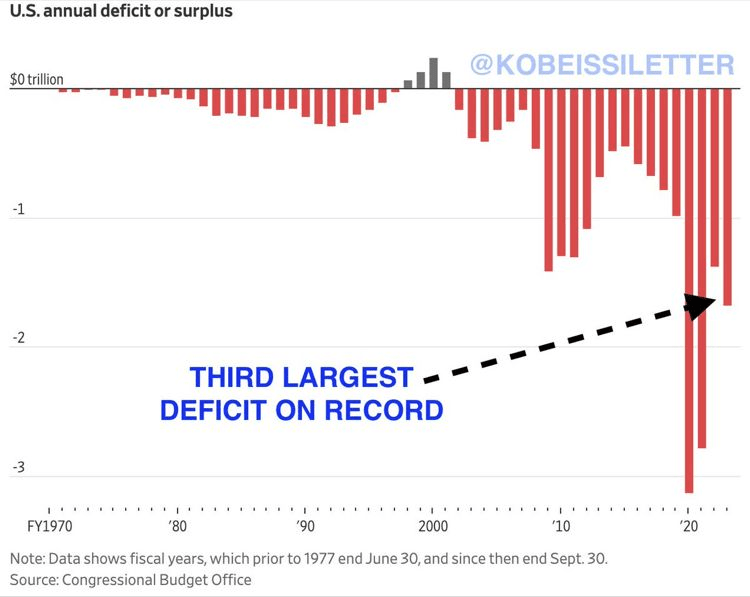

Biden/Congress have a broken fiscal model where spending is out of control. And The Fed can’t buy all the debt Biden/Yellen want to issue.

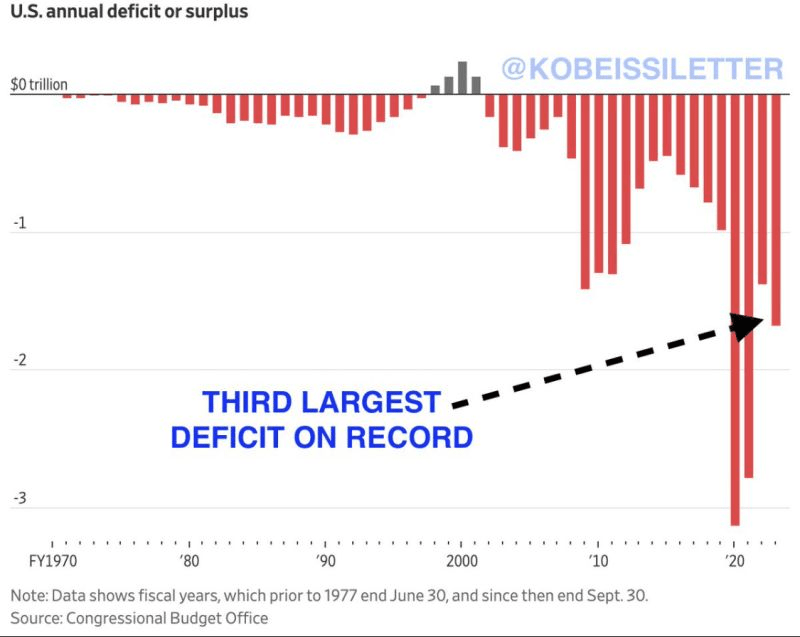

US deficits are the third highest on record.

We might as well have Taylor Swift as Fed Chair. And Travis Kelce as Treasury Secretary replacing TLTL Janet.

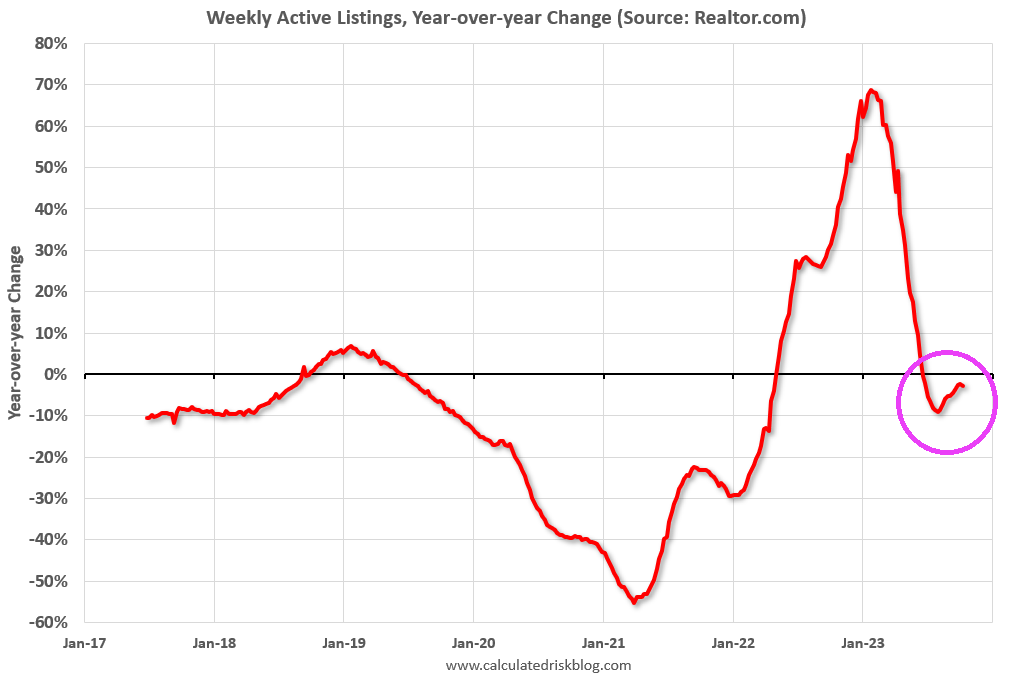

• Active inventory declined, with for-sale homes lagging behind year ago levels by 2.7%. For 17 straight weeks, the number of homes available for sale has registered below that of the previous year.

• New listings–a measure of sellers putting homes up for sale–were down again this week, by 4.4% from one year ago. Since mid-2022, new listings have registered lower than prior year levels, as the mortgage-rate lock-in effect freezes homeowners with low-rate existing mortgages in place. Although the year over year declines are smaller now than the double-digit pace seen earlier in 2023, declines from the pre-pandemic period are still substantial.

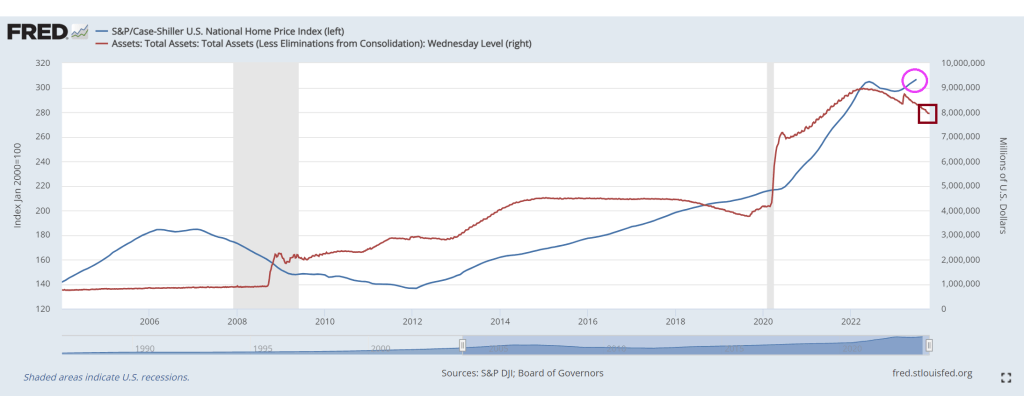

Inventory remains far below levels seen before the financial crisis. But Case-Shiller National Home Price Index (blue) remains elevated along with The Fed’s balance sheet (red) which is barely below $8 TRILLION. And Powell didn’t say much about speeding up the trimming of The Fed ballast.

Bidenomics strikes … again. No, not his inane ramblings about Hamas being “the other team” or that Hamas has to learn to shoot straight. But his policies freezing effects on the economy. Like housing.

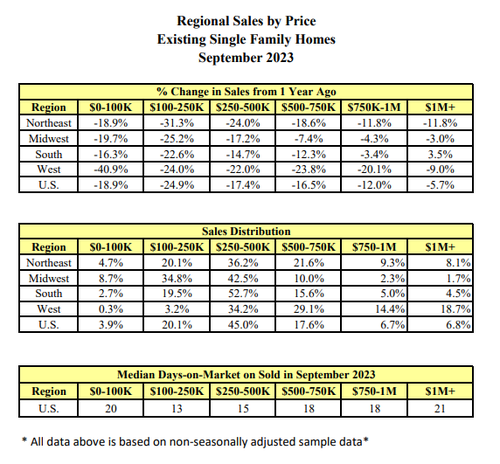

Existing-home sales faded in September, according to the National Association of REALTORS®. Among the four major U.S. regions, sales rose in the Northeast but receded in the Midwest, South and West. All four regions registered year-over-year sales declines.

Total existing-home sales – completed transactions that include single-family homes, townhomes, condominiums and co-ops – waned 2.0% from August to a seasonally adjusted annual rate of 3.96 million in September. Year-over-year, sales dropped 15.4% (down from 4.68 million in September 2022). … Total housing inventory registered at the end of September was 1.13 million units, up 2.7% from August but down 8.1% from one year ago (1.23 million). Unsold inventory sits at a 3.4-month supply at the current sales pace, up from 3.3 months in August and 3.2 months in September 2022.

The total existing home sales SAAR dropped back below 4mm for the first time since October 2010 (during the foreclosure crisis)…

Source: Bloomberg

Sales fell in all regions except the Northeast in September… and in every price range…

Single-family home sales fell to an annualized 3.53 million pace, the lowest since 2010. Condominium and co-op sales also declined.

“As has been the case throughout this year, limited inventory and low housing affordability continue to hamper home sales,” said Lawrence Yun, NAR’s chief economist.

“The Federal Reserve simply cannot keep raising interest rates in light of softening inflation and weakening job gains.”

First-time buyers made up a historically low 27% of purchases, down from the prior month.

Cash sales represented 29% of total sales, matching the highest level in over a decade. Investors, who often purchase with cash and are therefore less sensitive to mortgage rates, made up 18% of the market.

“It would be very unusual to have higher cash compared to first time buyers,” Yun said on a call with reporters.

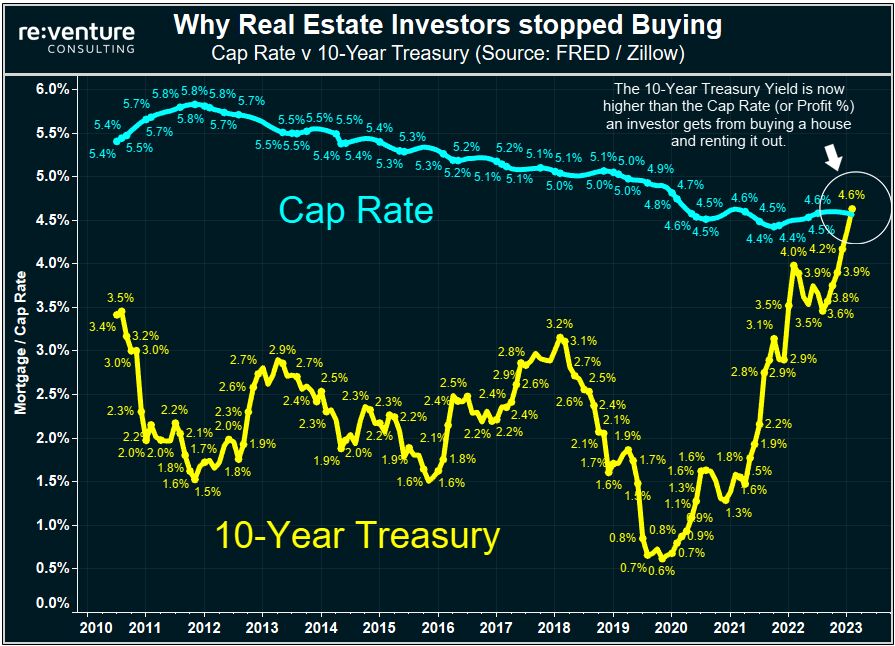

And, if mortgage rates (and thus affordability) are anything to go by, things are about to get real…

Source: Bloomberg

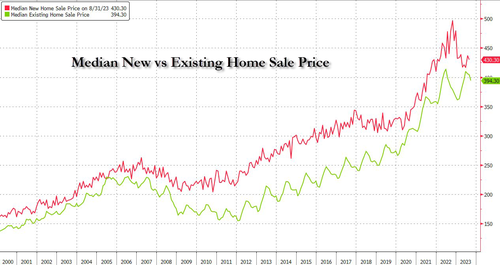

The median selling price rose 2.8% from a year earlier to $394,300, the highest September reading on record, pushing affordability even lower. But existing home prices are falling relative to new home prices (with the ratio near record lows)…

It looks like The House may elect a RINO as Speaker (Patrick McHenry, RINO-NC) to replace McCarthy. One RINO replacing another RINO … all so The House can continue its insane, inflation inducing spending.

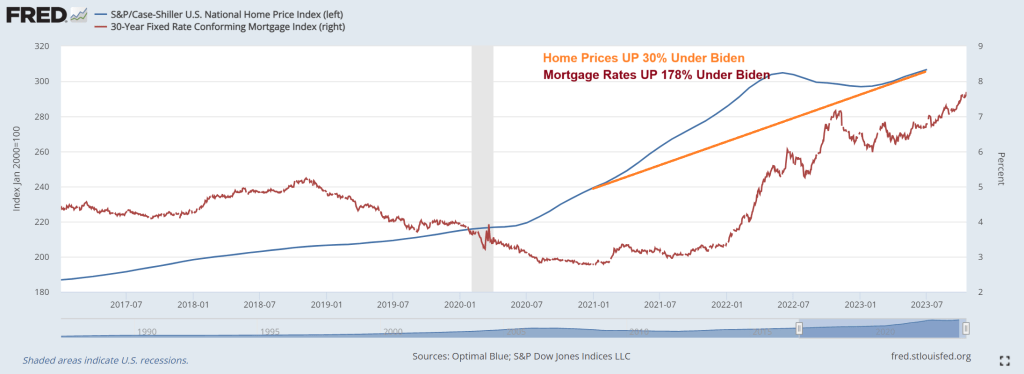

Under Bidenomics, home prices are up 30% while real weekly earnings growth has been negative for most of Biden’s Presidency. And mortgage rates are up 178% under Bidenomics.

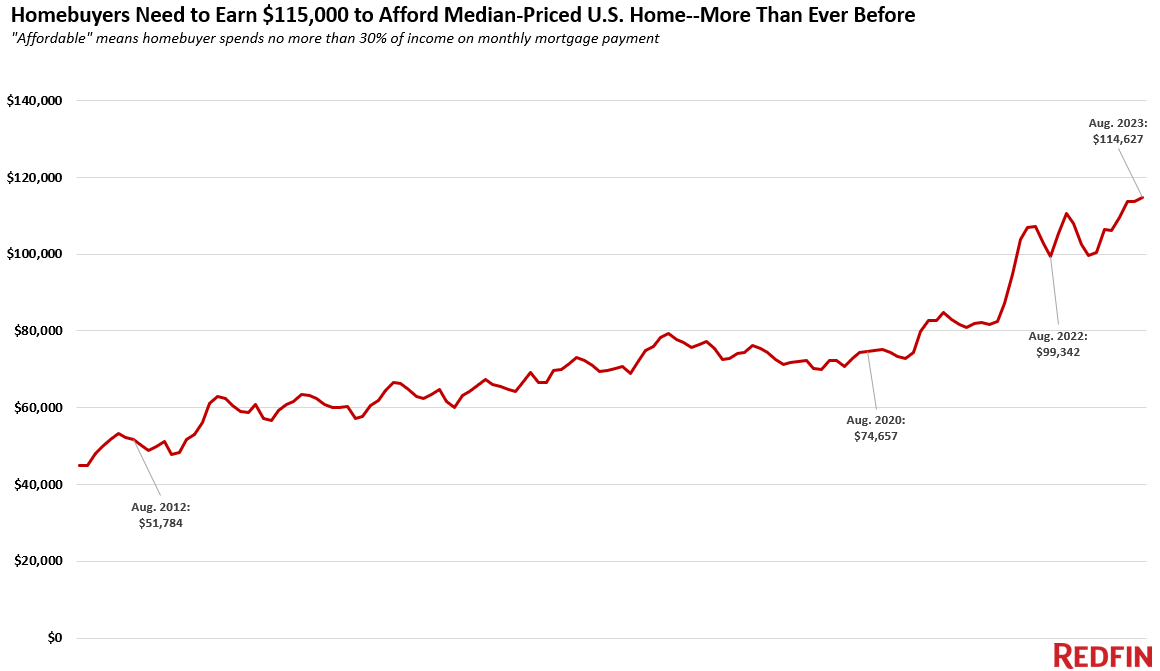

It’s harder than ever for Americans to afford a home.

A homebuyer must earn $114,627 to afford the median-priced U.S. home, up 15% ($15,285) from a year ago and up more than 50% since the start of the pandemic. That’s the highest annual income necessary to afford a home on record.

This is based on a Redfin analysis that compares median monthly mortgage payments for homebuyers in August 2023 and August 2022. The income data in this analysis is adjusted for inflation. See the bottom of this report for more on methodology.

Housing costs are higher than ever because of the one-two punch of sky-high mortgage rates and rising home prices. The average rate on a 30-year fixed mortgage was 7.07% in August. Mortgage rates have climbed even higher since then, hitting 7.57% during the week ending October 12–their highest level in over two decades. But even though soaring mortgage rates have dampened demand, low inventory is causing home prices to increase. The typical U.S. home sold for about $420,000 in August, up 3% year over year and just about $12,000 shy of the all-time high hit in mid-2022.

The typical U.S. homebuyer’s monthly mortgage payment is $2,866, an all-time high. That’s up 20% from $2,395 a year earlier, and by that time payments had already increased substantially from the beginning of the pandemic, a time of ultra-low mortgage rates and yet-to-skyrocket home prices. In August 2020, for instance, the typical monthly payment was $1,581, based on that month’s average mortgage rate of 2.94% and median home price of $329,000. At that time, a homebuyer would have needed to earn $75,000 per year to afford the typical home.

The typical American household earns about $40,000 less than the income needed to buy a median-priced home. The median household income was roughly $75,000 in 2022, the most recent year for which annual income data is available. Hourly wages have risen in 2023, but not nearly as fast as the income necessary to afford a home is rising: The average U.S. hourly wage has increased by about 5% over the last year.

“In a homebuyer’s ideal world, rising mortgage rates would push demand and home prices down enough to make up for high interest payments. But that’s not what’s happening now: Although new listings are ticking up slightly, inventory is still near record lows as homeowners hang onto their low mortgage rates–and that’s propping up prices,” said Redfin Economics Research Lead Chen Zhao. “Buyers–particularly first-timers–who are committed to getting into a home now should think outside the box. Consider a condo or townhouse, which are less expensive than a single-family home, and/or consider moving to a more affordable part of the country, or a more affordable suburb.”

Affordability is less of a problem for all-cash and move-up buyers. The major increase in income necessary to afford a home hits first-time homebuyers hardest. Buyers who can afford to pay cash aren’t impacted by high mortgage rates, and they likely earn more than the income necessary to purchase a home, anyway. Buyers who are selling a home to buy another one are in a better boat than first-timers because they have likely built up equity in their current home, which takes a bit of the sting out of soaring monthly payments. The caveat to the caveat is those who bought at the height of the pandemic-era market with an ultra-low mortgage rate and need to sell now: Not only are they giving up a low rate, they also may have lost money on their home.

Metro-level highlights: Income needed to buy a home has risen in all major metros, with biggest uptick in Miami and smallest in Austin

August 2023, analysis includes 100 most populous U.S. metros for which data is available

Metros where necessary income has increased most: In both Miami and Newark, NJ, homebuyers must earn 33% more than a year ago to afford the typical home–the biggest percent increase of the major U.S. metros. Homebuyers in Miami need to earn $143,000 annually to afford the area’s typical monthly mortgage payment of $3,580, and Newark buyers need to earn roughly $160,000 to afford that area’s $3,989 payment.

Other metros where necessary income has increased by over 30%: The income necessary to afford a median-priced home has increased by over 30% in four other metros, all in the eastern half of the country: Bridgeport, CT ($183,000); Dayton, OH ($60,000); Rochester, NY ($66,000); and Hartford, CT ($95,000).

Buyers need to earn more in every major metro: Skyrocketing mortgage rates have caused the income necessary to buy a home to increase in every major metro, even the places where prices have declined over the last year.

Necessary income has increased least in pandemic homebuying hotspots: Austin, TX homebuyers must earn $126,000 to afford the median-priced home, 8% more than a year ago–the smallest increase of all the major U.S. metros. That’s despite Austin home prices falling 7% year over year in August after they skyrocketed during the pandemic, with remote workers flocking in. Boise, ID, another pandemic homebuying hotspot where demand has since dropped, experienced the next-smallest increase: up 9% to $127,000. Salt Lake City, Fort Worth, TX and Lakeland, FL come next, with year-over-year increases of about 13% each. Home prices are down from a year ago in all those metros.

Homebuyers must earn six figures to buy a home in half the major metros in the country: In 50 of the 100 metros in this analysis, buyers must earn at least $100,000 to afford the median-priced home in their area. Buyers must earn at least $50,000 everywhere in the country.

Bay Area buyers must earn $400,000: Buyers in the most expensive markets in the country–San Francisco and San Jose, CA–must earn more than $400,000 to afford the median-priced home in their area, both up nearly 25% year over year. The next five metros are all in California: Anaheim ($300,000), Oakland ($250,000), San Diego ($241,000), Los Angeles ($237,000) and Oxnard ($233,000).

Rust Belt buyers need the least income–but it’s still up from a year ago: Detroit homebuyers must earn about $52,000 to afford the area’s median-priced home, up 19% from a year ago. That’s the lowest income required to afford a home in the U.S. Next come three Ohio metros (Akron, Dayton and Cleveland) and Little Rock, AR, all of which require roughly $60,000 in annual income to buy a home.

Face it, the US economy and housing/mortgage markets are addicted to gov!

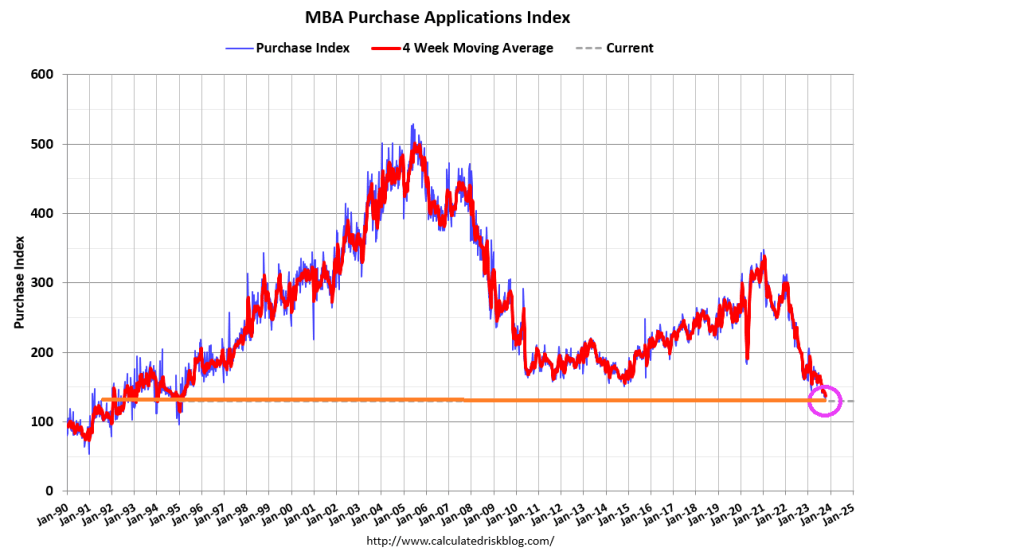

Mortgage applications decreased 6.9 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending October 13, 2023. Applications decreased to their lowest level since 1995, as the 30-year fixed mortgage rate increased for the sixth consecutive week to 7.70 percent – the highest level since November 2000.

The Market Composite Index, a measure of mortgage loan application volume, decreased 6.9 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 7 percent compared with the previous week. The Refinance Index decreased 10 percent from the previous week and was 12 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 6 percent from one week earlier. The unadjusted Purchase Index decreased 5 percent compared with the previous week and was 21 percent lower than the same week one year ago.

Well, the San Francisco 49ers are playing the Cleveland Browns today with the Browns missing injured RB Nick Chubb and QB Deshaun Watson, replacing them with QB Dorian Thompson-Robinson (aka, Do Not Resuscitate or DNR) and RB Jerome “Exploding Pinto” Ford. ESPN gives the Browns a 26% chance of winning. I am amazed it is that high!

But back to economic news!

Gold is soaring due to the instability in the Middle East (Iran/Hamas/Hezbollah attacks on Israel). Let’s see if Israel continues it assault on Gaza or not.

Janet Yellen, Biden’s Treasury apparatchik, was at the IMF/World Bank meetings in Marrakesh (yes, former students are expecting me to like Crosby, Stills and Nash “Marrakesh Express” but I detest CS&N). Instead, here is Them with Here Comes The Night which is more fitting about risks in the global economy.

The heavy debt burdens of advanced economies — from the United States to China and Italy — was a recurrent theme in the meetings, which came after financial markets in recent weeks pushed U.S. bond yields higher. Italian central bank governor Ignazio Visco said there was an impression markets were “reevaluating the term premium” as investors become more nervous about holding longer-term debt.

JPMorgan chair of global research Joyce Chang put it another way. “The bond vigilantes are back, and the Great Moderation is over,” she told a panel of the two-decade era of relative economic calm before the 2008/09 financial crisis.

The Federal Reserve still hasn’t shrunk their massive balance sheet and removed the Covid stimulus. Call it lack of Fed retreat.

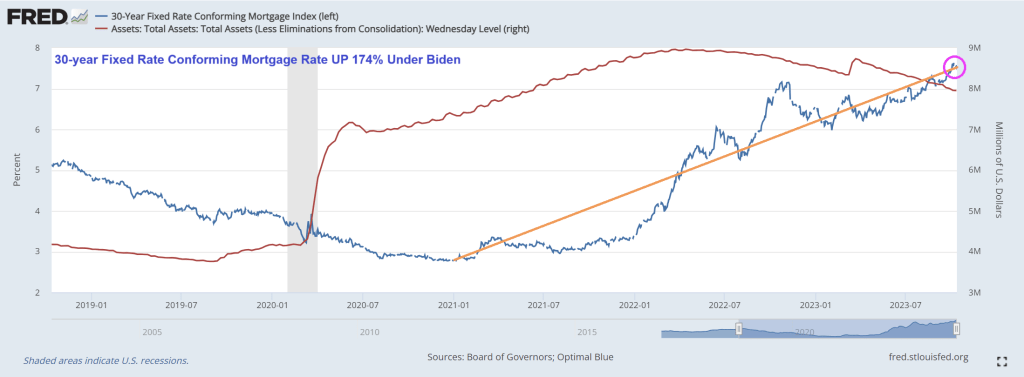

And mortgage rates continue to rise, up 174% under Stumblin’ Joe Biden despite The Fed not really shrinking their balance sheet.

I may be the only person in the US cheering for House Republicans being at an impasse over House Speaker. Why? Congress can’t approve massive spending bills with out a Speaker! Less spending, less inflation! There fixed inflation without The Fed.

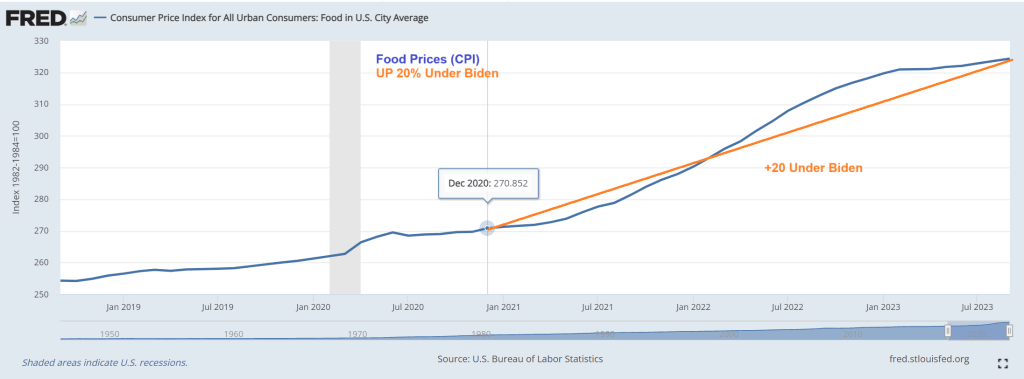

First, food prices are up 20% since December 2020. Talk about destruction of middle class wealth!

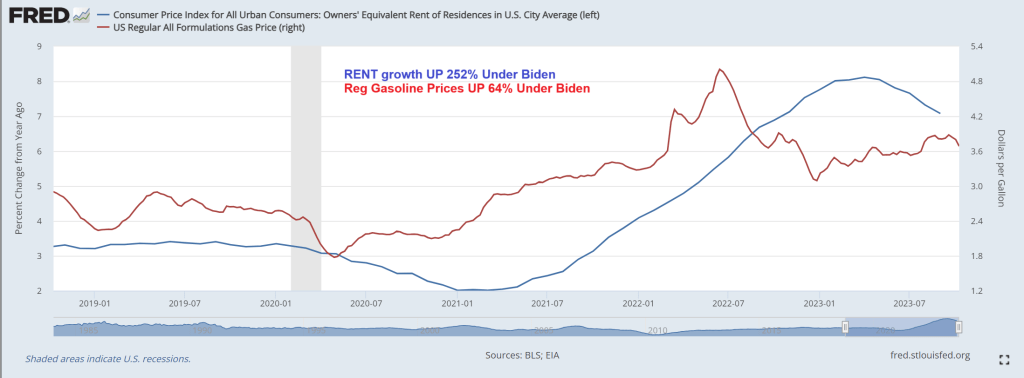

That is in addition to gasoline prices are up 64% under Biden while rent growth is up 252%. Well, Biden waived through millions of illegal immigrants and rent had to rise. Biden and Washington DC’s broken borders is Livin’ La Vida Loco.

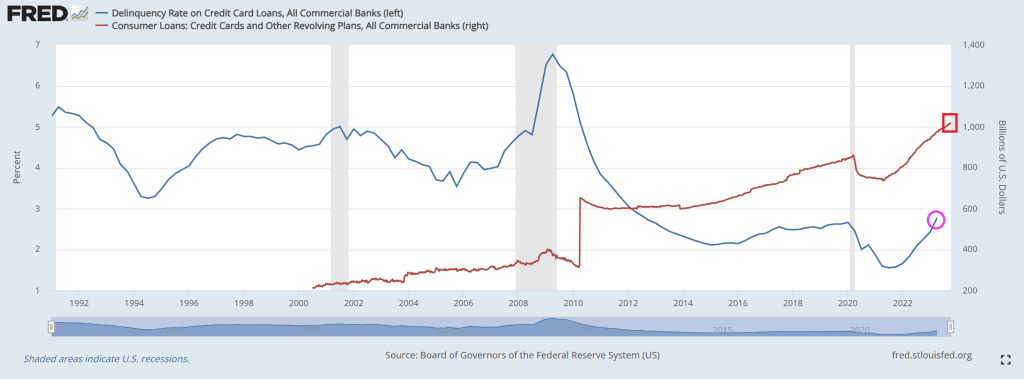

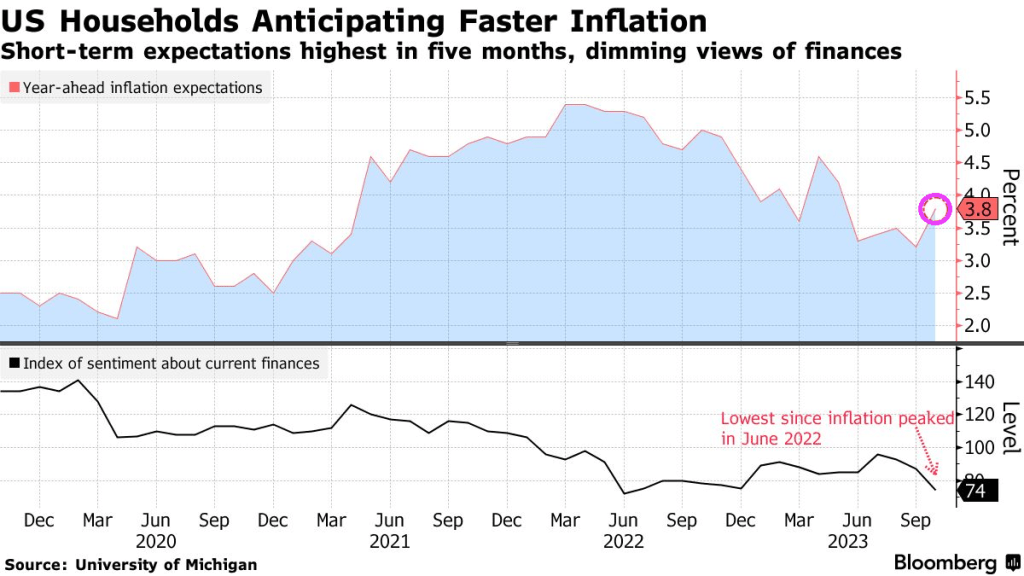

To cope with inflation (that Paul Krugman claims is over but the last inflation report showed that the tinders of inflation are hard to extinguish), consumers have turned to credit cards to survive. In fact, credit cards have expanded 38% since April 2021 despite rapidly rising interest rates. And credit card delinquency rates are rising and are now above Covid-era economic shutdown levels.

Like President Biden enjoying a barbeque at The White House with a live band (probably NOT Justin Moore singing “Small Town USA”) while Hamas declared war on Israel and Americans are being held hostage with the promise of public executions of hostages livestreamed. Nothing that “Empathy Joe” does ever surprises me anymore, but I am surprise that various Federal Reserve Presidents will speak today while Hamas terrorizes Israeli and US citizens.

It could be that investors think that Talking Heads at The Fed will claim that Fed rate increases are over. Then again, the Iran/Hamas terror campaign against Israel is spookking markets, driving up oil and gold prices and driving up “flight to safety” in US Treasuries.

President Biden called on Americans in Israel to book a commercial flight home, even though Israel has cancelled all flights. Does Old Joe even read the news??

Joe Biden, who has always been a compulsive liar but at least sounded cognicent, is now babbling and whispering that Bidenomics works. But for who?

Clearly not for first time homebuyers or people looking to move. Bankrate’s 30-year mortgage rate is up to almost 8%, the highest since July 2000 and Willy Slick Clinton. That is a 176% increase in mortgage rates under the most inept “Economic Sheriff” in history.

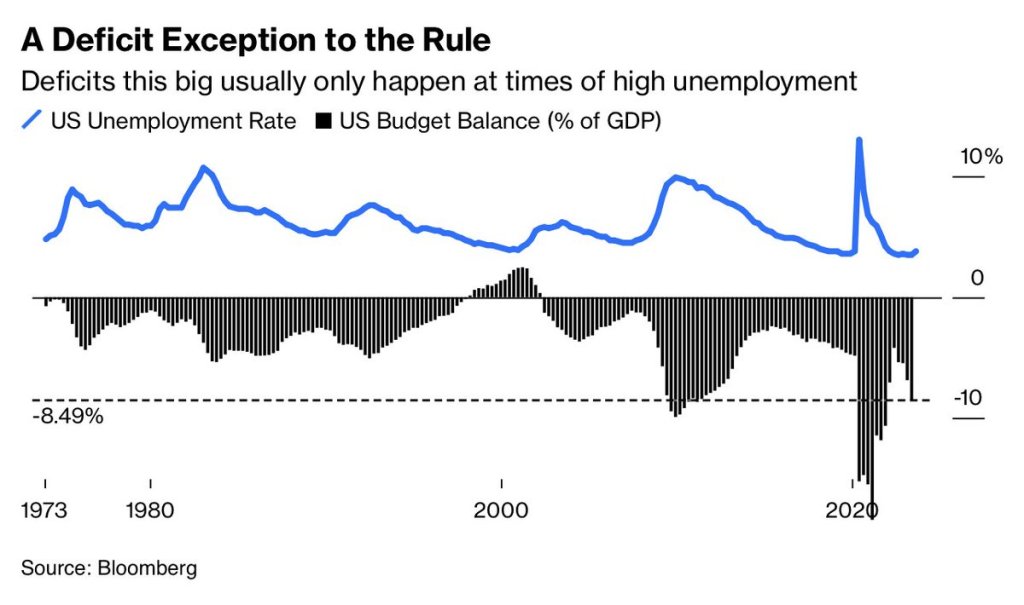

Deficits? Deficits (which Biden makes outlandish claims) are usually only this big at times of HIGH unemployment and recessions. So, are the staggering deficits under Biden a precursor to a hard landing (recession)? Don’t listen to what Biden or KJP say!!!

Biden’s outlandish claims that he single handedly reduced the deficit by the most in history is, well, typical Biden bloviating. Actually, tax receipts soared after Covid lockdowns ended. Period. Now that stimulus is wearing out, deficits are climbing again.

Hey Bartender! The leading employment gain under Bidenomics was … low paying leisure and hospitality jobs at 96k jobs added.

The US added a whopping 336K jobs, the highest monthly increase since January. This is surprising given that the ADP report was so weak.

And the BLS decided to UPWARD revised past numbers. The BLS revised not only August but also July higher: the change in total nonfarm payroll employment for July was revised up by 79,000, from +157,000 to +236,000, and the change for August was revised up by 40,000, from +187,000 to +227,000. With these revisions, employment in July and August combined is 119,000 higher than previously reported.

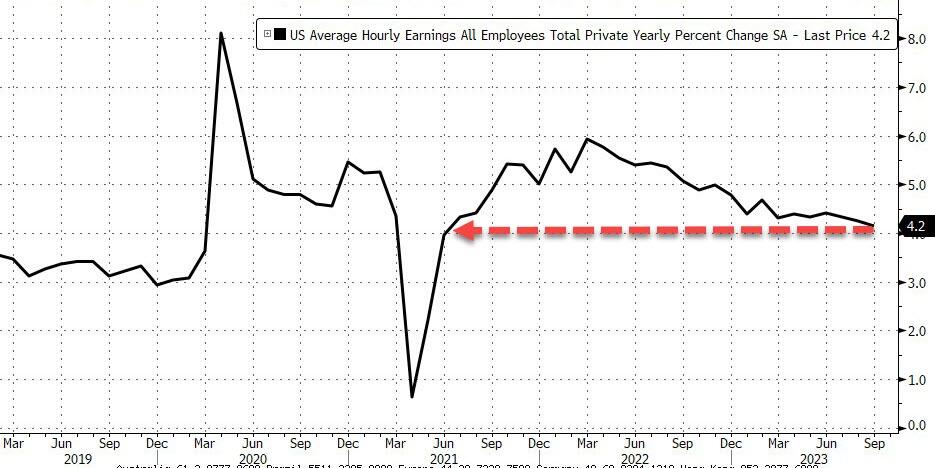

Meanwhile wage growth continued to cool, and in September average hourly earnings increased 0.2%, below the 0.3% expected, and resulted in a 4.2% increase YoY, down from 4.3% in August…

… as a result of a big bump in lower paying jobs.

But perhaps the most remarkable divergence in the report is that with headline payrolls surging 336K (establishment survey), the Household Survey indicated that the pain continues, as the number of people employed not only rose by less than 100K (86K to be precise), but it was all part-time workers, which increased by 151K. Full-time workers? Why, they dropped by 22K, and the lowest since February.

Leisure and hospitality added 96,000 jobs in September, above the average monthly gain of 61,000 over the prior 12 months.

But the jobs report highlights Bidenomics. Lots of government jobs and the private sector getting crushed. +1 million government jobs, -400K non-government.

Hmm. How will The Federal Reserve view this report? Focus on the red-hot headline gain of 336k job added or the fact that it is mostly part-time jobs added? Odds of a rate HIKE rise to 44% after September jobs report and Fed PAUSE expectations have been extended.

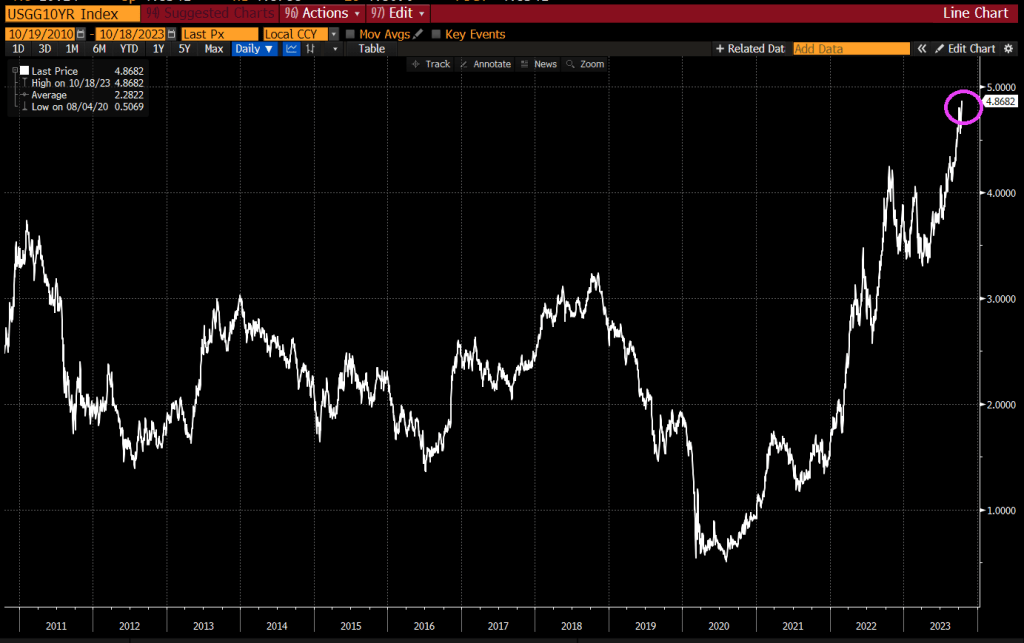

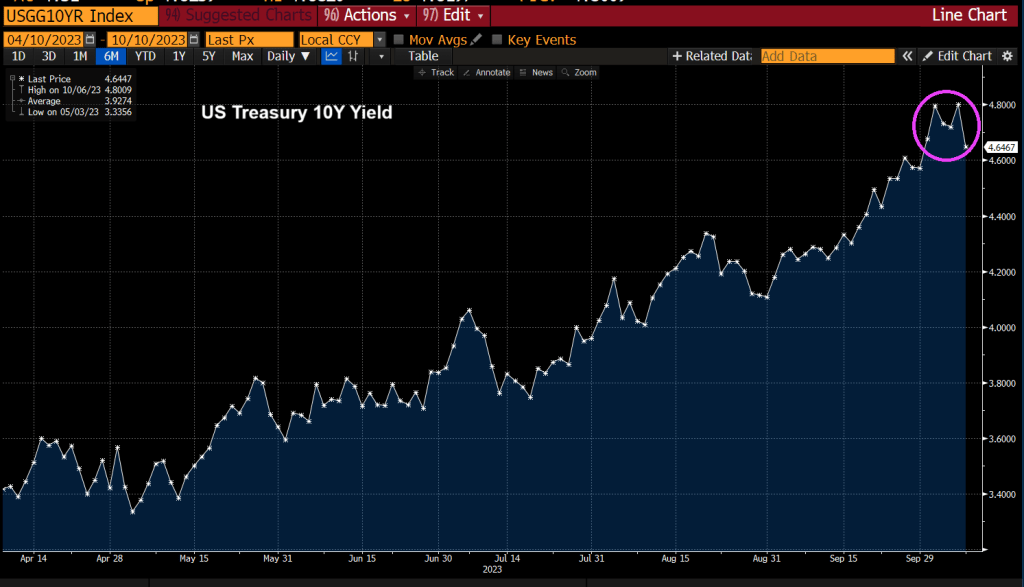

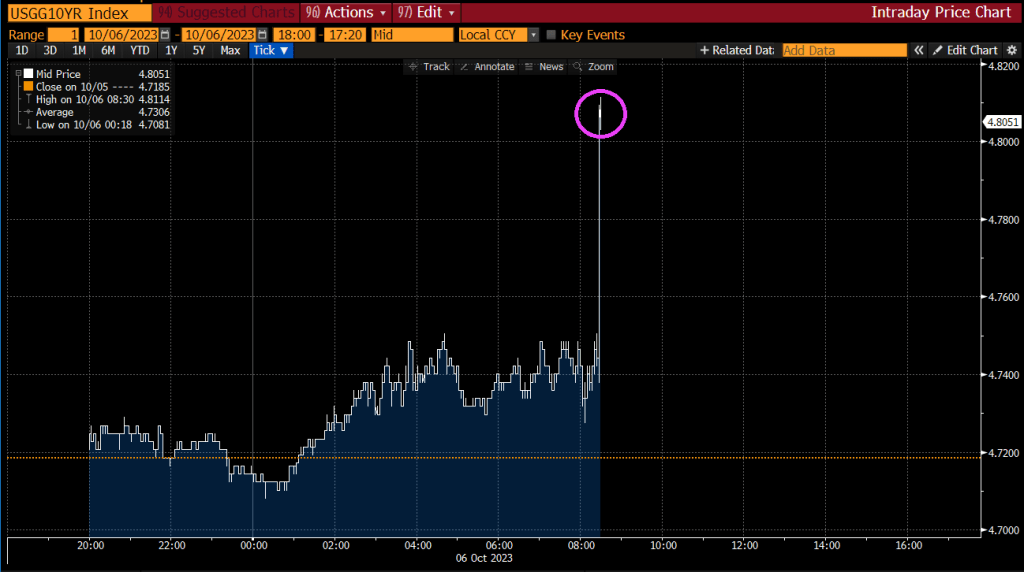

After the jobs report, the US Treasury 10Y yield soared.

The 10-year Treasury yield has risen dramatically under Biden’s Reign of (Economic) Error.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.