Dallas after midnight! Especially with a broken Congress and President.

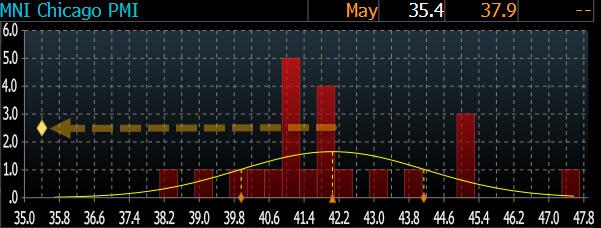

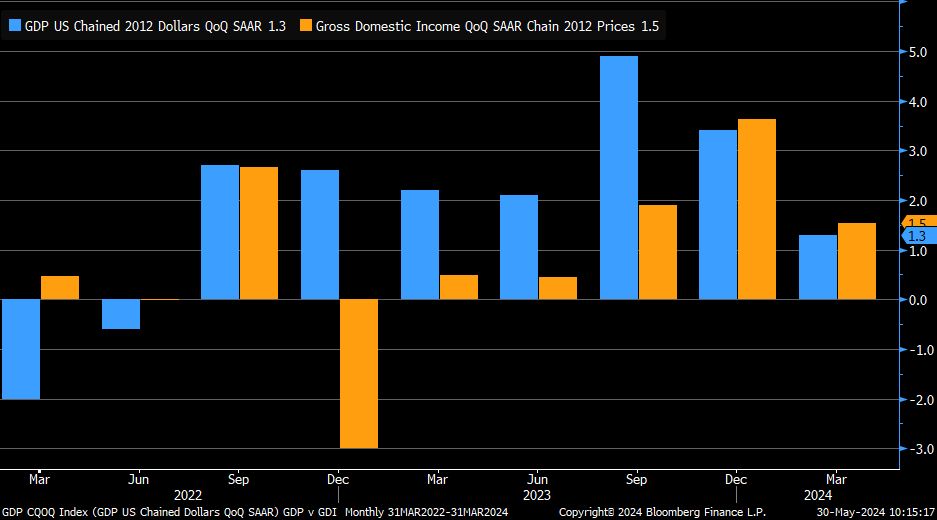

But, below the hood of the last one we see some more interesting dynamics evolving as revenues and employment decline while prices re-accelerate…

This is the 25th straight month of contraction (sub-zero) for the Dallas Fed Services index and judging by the respondents’ comments, there is a clear place to point the finger of blame:

Poor national leadership and lack of confidence have eroded the business environment.

- The Federal Reserve’s recent announcement of no rate cuts in the near future is concerning regarding the immediate and lag effect it could have on the local economy. We have received direct feedback from many of our clients in various industries, and they are increasingly concerned. They are freezing hires and spending, with many reducing spending. The primary reason is the economic stagnation locally and nationally affecting their businesses.

- People are adjusting to new economic realities. Few are expecting salary increases and are instead making lifestyle adjustments to deal with higher living costs. Reality is also setting in for the apartment owners we serve. They understand rents aren’t going up and interest rates aren’t coming down. As rate caps expire and loans mature, lenders are having to adapt as well. Ultimately, a lot of private equity (much in the form of individual retirement savings put into syndications) is getting wiped out.

- We need a rate cut before we will see any revenue improvement from home sales.

- As elections draw near, the political environment worsens, creating more uncertainty in our business.

- We feel inflation and fear of more inflation plus the rise in cost of living are holding consumers back. Hopefully we will adapt to the new realities soon.

Customers are concerned about the election, so they are holding off on large purchases.

- The lack of building activity is shutting down the appliance industry.

- Affordability has become an ever-increasing problem for new car dealers. The price increases of new cars combined with higher interest rates have put new cars out of reach for more and more people.

- [Car] inventories continue to swell, and interest rates remain high. Our grosses are off, and margins continue to decline. Profits are down 20 percent from the prior year.

- The economy is slowing. The consumer is more cautious and more reluctant to purchase at higher prices and payments.

And finally, this seemed to sum up just how business-owners feel in general about the current occupant of The White House:

“Our outlook depends heavily on the presidential election.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.