REAL average hourly earnings growth remain in the toilet at -3.06% YoY.

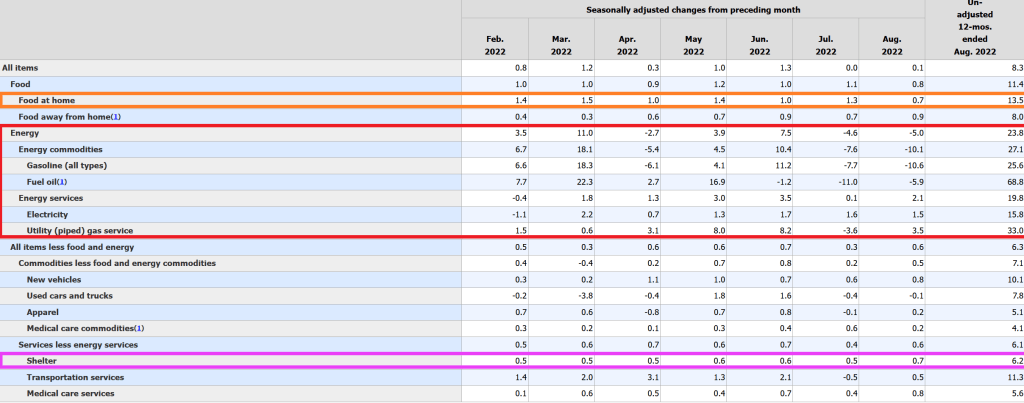

Fuel oil used to heat homes rose 68.8% YoY. Food at home rose 13.5% YoY while rent (shelter) rose “only” 6.2% YoY. Wow, renters are REALLY getting the short-end of the stick from The Fed and the Biden Administration!!

New vehicles are UP 10.1% YoY. Good luck buying those “cheap” electric cars that Mayor Pete Buttigieg trumpets! And wait for the bill when the battery needs to be replaced!!!

Freddie Mac’s 30-year mortgage commitment rate just rose to its highest level since … The Fed initiated Quantitative Easing (aka, fanatical money printing) during the financial crisis.

The good news? The US inflation report is likely to show a slowing of the inflation rate to around 8% YoY and -0.1% MoM. Why? Gasoline prices are cooling thanks to the global economic slowdown.

While gasoline and food prices are falling, CORE US inflation, the inflation rate excluding food and energy, is expected to rise to around 6.1% YoY and +0.30% for August.

The Federal government reaction to the Covid outbreak in early 2020 included massive monetary stimulus, Federal government spendathons and Biden’s green energy policies have resulted in a sizzling 8.5% inflation rate (update on Monday morning).

The problem is that The Federal Reserve is far behind the inflation curve with their target rate at only 2.5%. And The Fed’s balance sheet remains near $9 TRILLION in assets held.

In Euroland, we are seeing a similar problem (Frankfurt, we have a problem!). The Eurozone inflation rate is at 9.1% while their version of The Fed Funds Target rate is only 0.75%, a large catch-up gap.

If we look at the Taylor Rule for the US using headline inflation, we see that The Fed needs to raise their target rate to … 21.72% to crush inflation.

In Euroland, the problem is similar. At 9.10% inflation, the ECB will have to raise their version of The Fed’s target rate to 16.80% to combat inflation. As if that will happen in either the US or Euroland.

On a different note, is it my imagination or does US Democrat Senate candidate from Pennsylvania John Fetterman look like the alien from the flick “Battleship”?

The US housing market is facing stress thanks to The Federal Reserve’s “war on inflation.” As The Fed starts trimming its excess ballast and M2 Money growth YoY slows to the lowest since Pre-Covid, we are seeing housing markets like San Francisco beginning to experience declines in home prices.

According to Redfin, Oakland California is leading the nation in terms of declining sales prices at -15.1% over a 3 month period. Followed by Silicon Valley and San Jose at -12.7%. San Francisco is in third place at -11.2% (I will ignore Lake Havasu AZ since it is teeny but does have one of the London Bridges) and Austin TX is in 5th place at -9.7%.

(Bloomberg)Investors who might be looking for the world’s biggest bond market to rally back soon from its worst losses in decades appear doomed to disappointment.

The US employment report on Friday illustrated the momentum of the economy in face of the Federal Reserve’s escalating effort to cool it down, with businesses rapidly adding jobs, pay rising and more Americans entering the workforce. While Treasury yields slipped as the figures showed a slight easing of wage pressures and an uptick in the jobless rate, the overall picture reinforced speculation the Fed is poised to keep raising interest rates — and hold them there — until the inflation surge recedes.

Swaps traders are pricing in a slightly better-than-even chance that the central bank will continue lifting its benchmark rate by three-quarters of a percentage point on Sept. 21 and tighten policy until it hits about 3.8%. That suggests more downside potential for bond prices because the 10-year Treasury yield has topped out at or above the Fed’s peak rate during previous monetary-policy tightening cycles. That yield is at about 3.19% now.

Then we have Bankrate’s 30-year mortgage rate soaring on Fed intervention expectations.

Inflation? US inflation is near its highest in 40 years and the USDollar Plain Vanilla Swap was at 0.50 when Biden first took office as President and is now 3.371 (quite an increase!).

Here is an interesting chart of FNCL 2% Agency MBS.

The August jobs report is out. 315k jobs were added, which was considerably higher than the ADP jobs added report of 132k. Hmm.

Be that as it may, US Average Hourly Earnings YoY remained at 5.2%. That’s a shame since the last inflation report had US inflation at 8.5%. That translates to REAL Average Hourly Earnings YoY of … -3.3%.

Labor force participation rose to 62.4%.

This is a decent jobs report and will likely lead The Fed to continue raising rates, particularly when The Fed sees that multiple jobholders has increased to cope with inflation.

When we look at tomorrow’s US jobs report, it is important to acknowledge that 1) The Federal Reserve has not yet removed the Covid stimulus (green line) and 2) the ADP payroll jobs added was only 132k in August while non-farm payrolls jobs added in July was 528k. That is quite a spread!

(Bloomberg)The hotly anticipated US jobs report has the potential to tip the scales toward a third jumbo-sized hike in interest rates later this month after a wave of data that point to a resilient consumer and high labor demand.

Friday’s report is one of the last marquee releases Fed officials will have in hand before the mid-September policy meeting to help them decipher a complex economic and inflationary puzzle.

Forecasts call for a healthy, yet more moderate 298,000 gain in August payrolls and for the unemployment rate to hold steady at 3.5%, matching the lowest in five decades. Solid wage growth is also expected amid a persistent mismatch between labor demand and supply.

Such figures, in conjunction with a blowout July employment print, improving consumer sentiment figures and a surprise pickup in job openings, could be enough to push the Fed to raise borrowing costs by 75 basis points, extending the steepest interest-rate hikes in a generation to curb an inflation surge.

As of this morning, Fed Funds futures data is still pointing to The Fed Funds Target rate rising from 2.50% to around 4% by the March FOMC meeting. That is still a large jump of another 150 basis points anticipated.

When inflation is so bad that REAL wage growth is negative (-3.31% YoY), I would hardly call that a strong economy for the middle class and low-wage workers.

We also see that REAL home price growth (existing home sales median price YoY – CPI YoY) has slowed to only 2.23% YoY in July.

As The Fed tightens, it is only growing to get worse.

You must be logged in to post a comment.