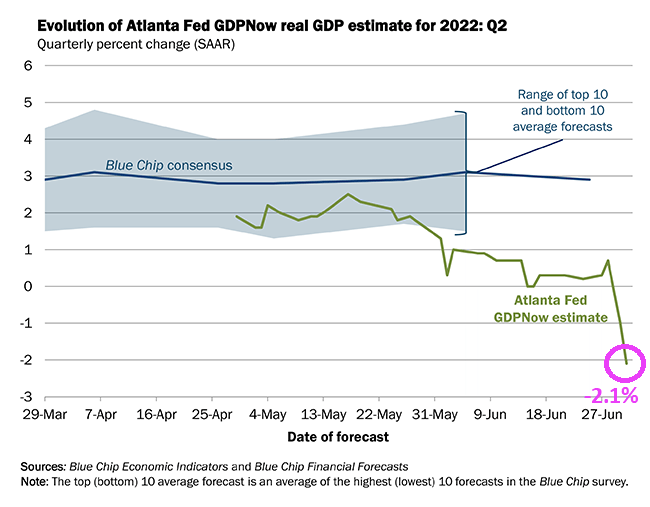

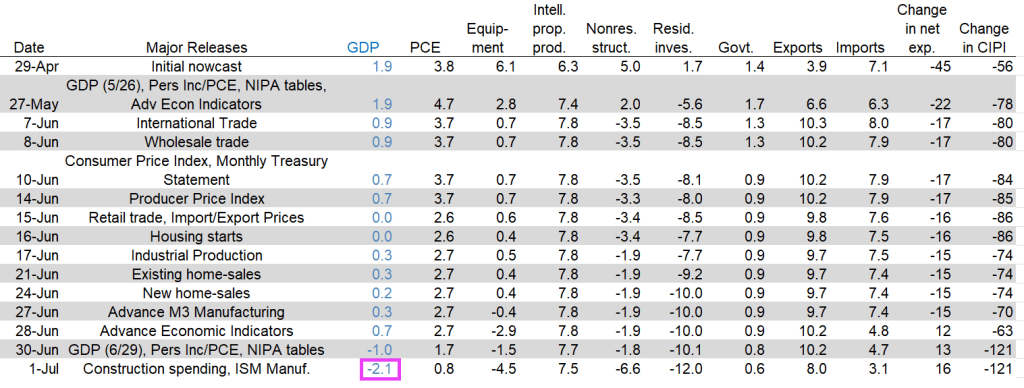

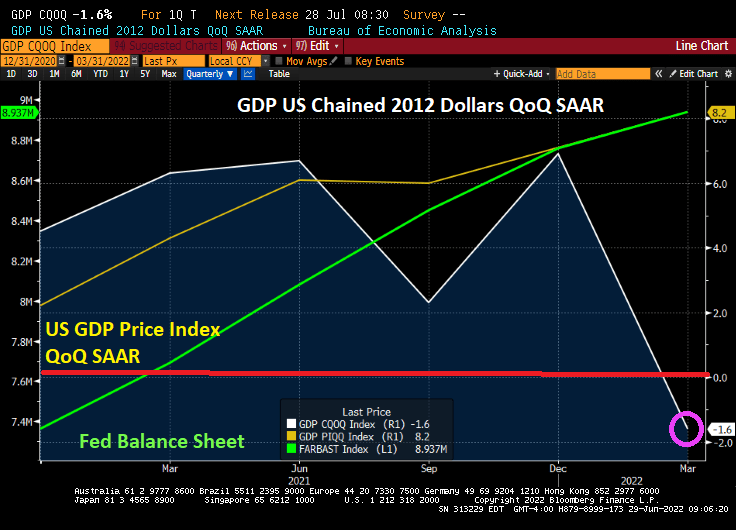

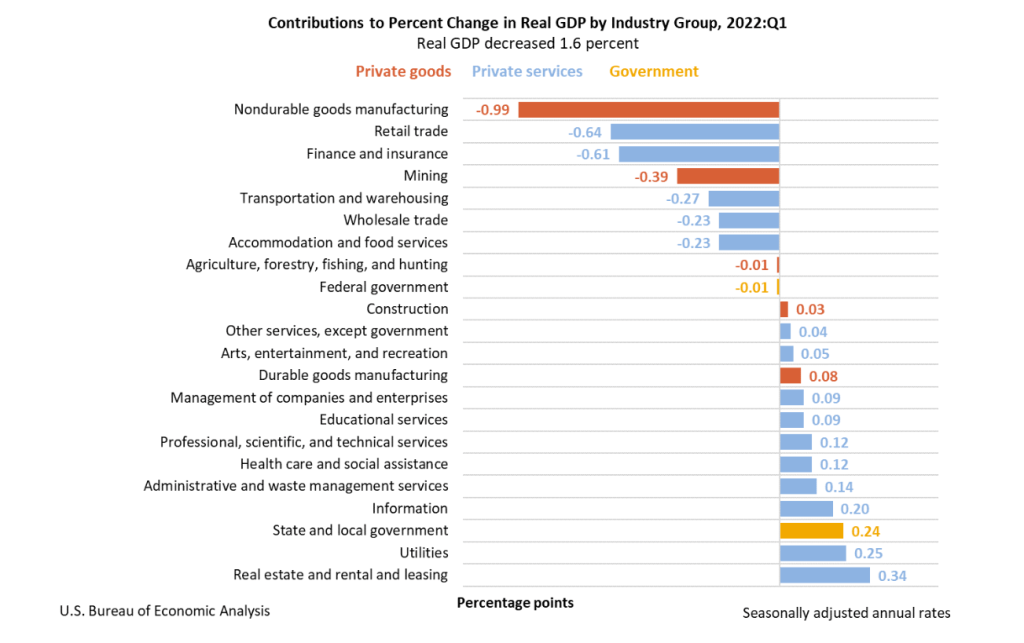

Which is bad news for Biden and Democrats after Q1’s bad GDP report of -1.6% “growth”, we now see the Atlanta Fed’s real-time GDP report for Q2 at -2.1%.

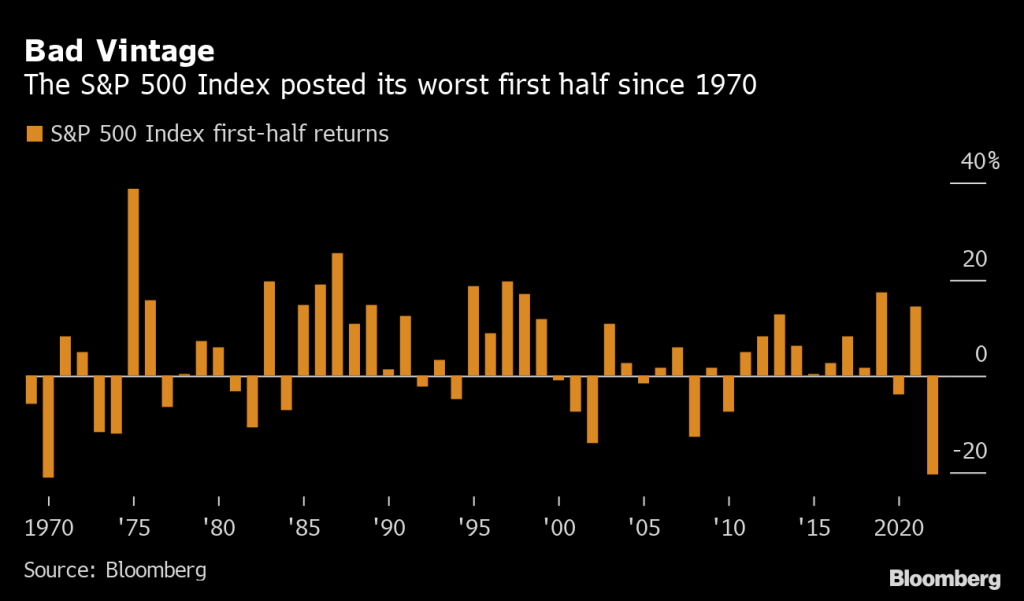

A “recession shock” begins for markets following the worst first-half for the S&P 500 in more than 50 years.

And investors are running to Treasuries for safety as US Treasury 10-year yields tank 14 basis points.

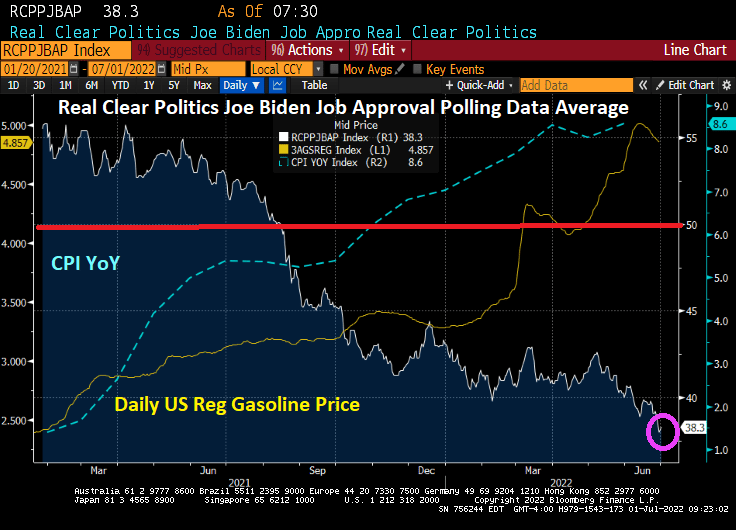

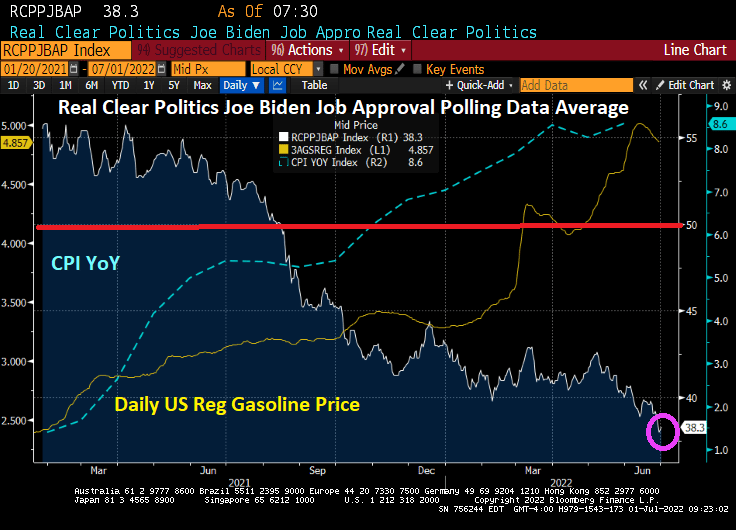

Biden’s approval rating has collapse with inflation and rising gasoline prices. Note that Biden’s approval rating dropped below 50 in mid-August 2021, long before the Russian invasion of Ukraine in late February 2022. Gasoline prices had risen 49% since Biden’s inauguration as President, but before the Russian invasion of Ukraine.

Financial markets are anticipating what Mester is saying: rapidly rising interest rates. But as you can see from the following chart, gasoline prices (orange line) are driving rising US prices. So it is doubtful that monetary tightening will slow price increases. But Mester and company can only control monetary stimulus.

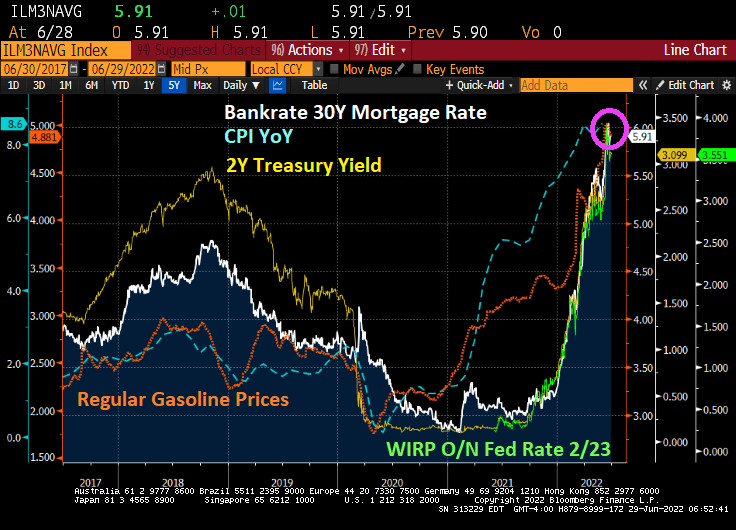

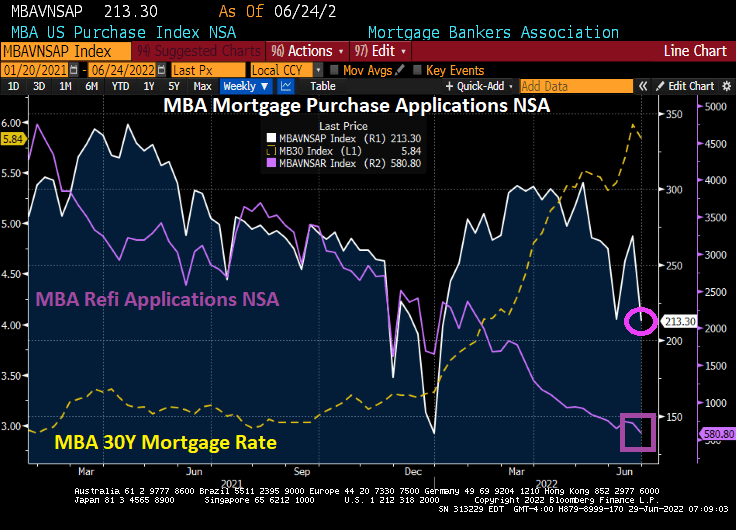

Mortgage rates have soared as The Fed attempts to crush inflation. And mortgage purchase applications fell -21% WoW in the most recent Mortgage Bankers Association survey.

The Refinance Index increased 2 percent from the previous week and was 80 percent lower than the same week one year ago. The seasonally adjusted Purchase Index increased 0.1 percent from one week earlier. The unadjusted Purchase Index decreased 21 percent compared with the previous week and was 24 percent lower than the same week one year ago.

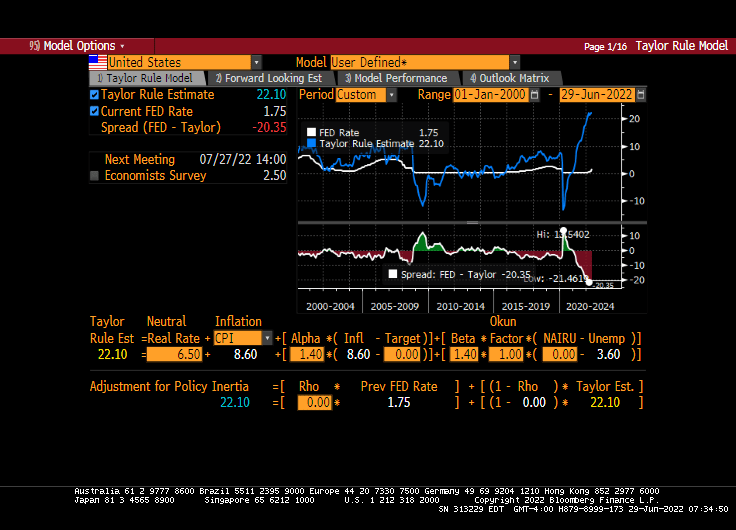

It almost seems like Mester is following the Taylor Rule (not really). But using CPI YoY, the Taylor Rule is saying that The Fed Funds Target Rate should be … 22.10%. It is only 1.75% after years of excessive stimulus following the banking crisis of 2008/2009. And Yellen who seemingly never met a rate hike that she liked.

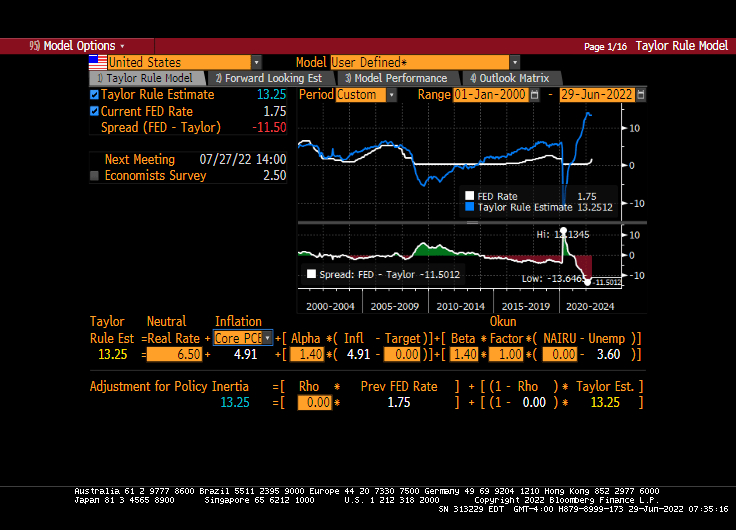

If we use core PCE as our measure of inflation, the Taylor Rule is still high at 13.25%, a whopping 11.50 spread over the current target rate.

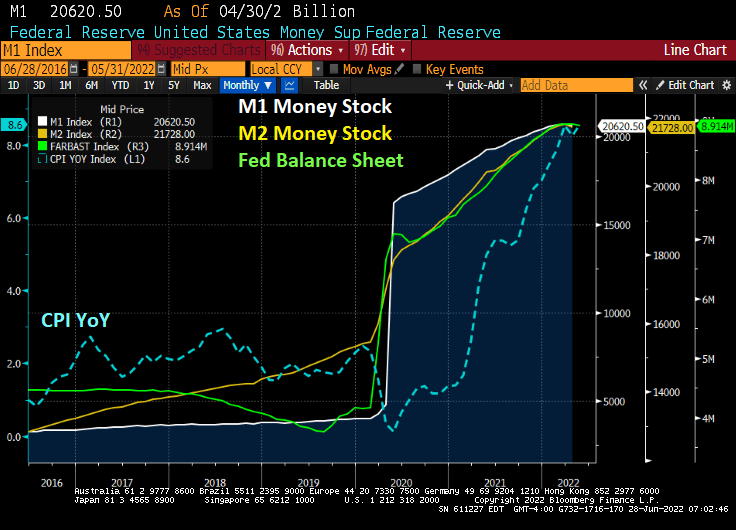

It took a while and trillions in fiscal and monetary stimulus to recover from Covid-era economic lockdowns, but now that the monetary stimulus is being withdrawn, the economy is stalling.

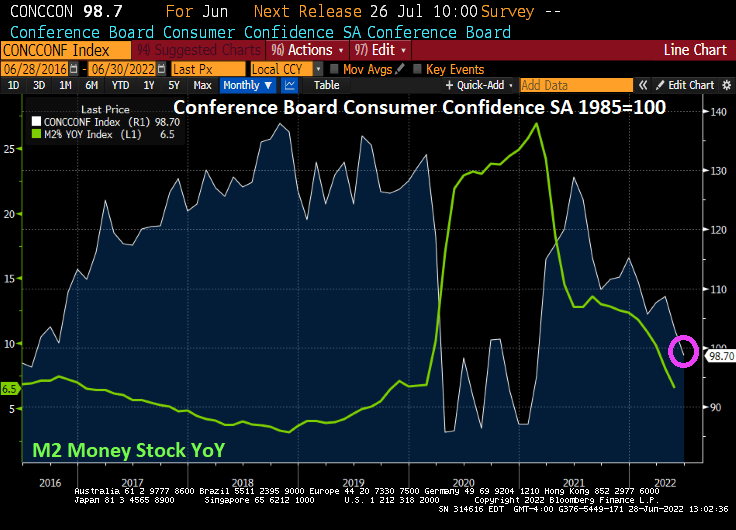

If you look at the chart below, you can see that “The Thrill Is Gone” from monetary and fiscal stimulus.

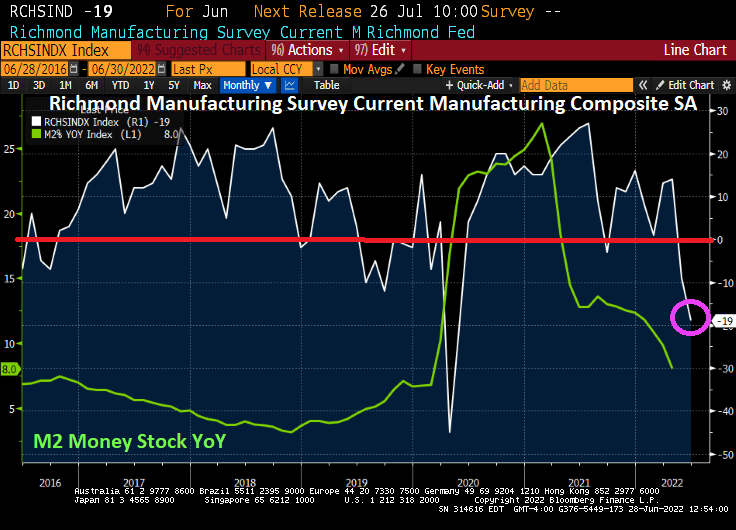

And The Conference Board’s Consumer Confidence Index fell below 100 as M2 Money Stock YoY returns to pre-Covid levels.

A national measure of prices climbed 20.4% in April, down from the 20.6% gain in March, the S&P CoreLogic Case-Shiller index showed Tuesday. Craig Lazzara, a managing director at S&P Dow Jones Indices, noted that April data was showing initial, but inconsistent, signs of a deceleration in price gains.

Mortgage rates have nearly doubled since the end of 2021. The run-up in rates, combined with high prices, are squeezing potential buyers and starting to slow housing markets in some of the most popular pandemic boomtowns.

Covid monetary stimulus remains in place at inflation hits 8.6%.

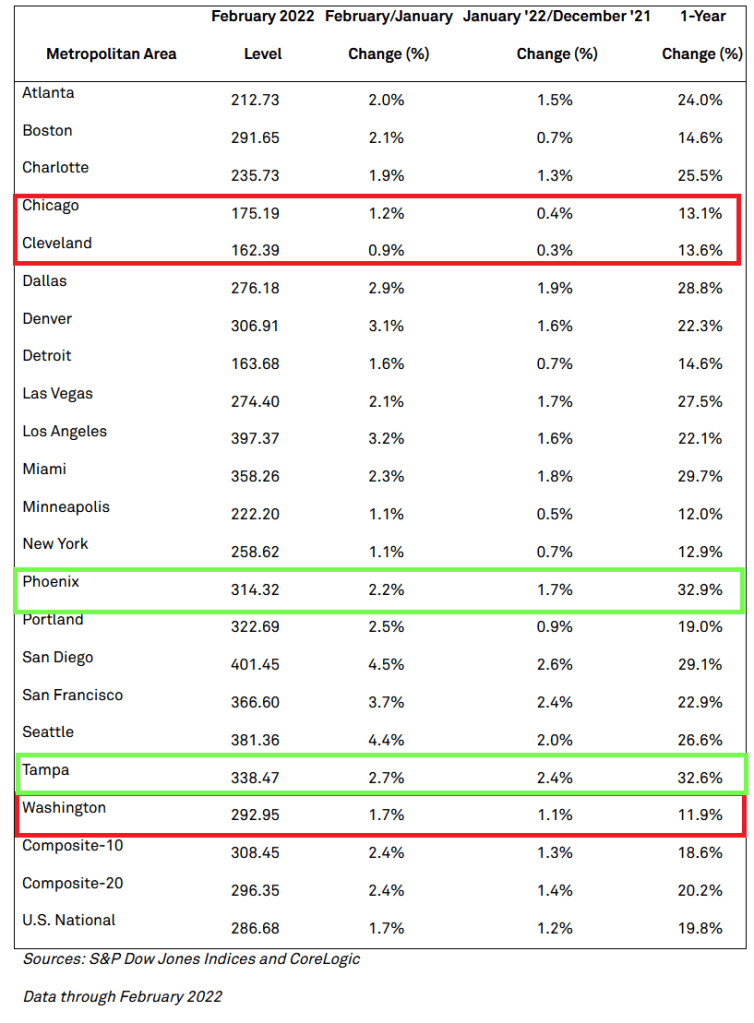

Washington DC has the slowest growth in home prices at 11.9% with Chicago and Cleveland close behind. Phoenix barely beat Tampa, FL for hottest home prices with both above 30% YoY.

The ECB is planning on a Blitzkrieg Bop, monetary style.

When Lagarde talks about the first line of defense, all I can picture is The Maginot Line in France, a failed defensive line that was easily bypassed by the German Wehrmacht (army).

The European Central Bank will activate the bond-purchasing firepower it’s earmarked as a first line of defense against a possible debt-market crisis on Friday, according to President Christine Lagarde.

Applying “flexibility” to how reinvestments from the ECB’s 1.7 trillion-euro ($1.8 trillion) pandemic bond-buying portfolio are allocated is aimed at curbing unwarranted turmoil in government bonds as interest rates are lifted from record lows to curb unprecedented inflation.

Net buying under a separate asset-purchase program is also set to end on Friday.

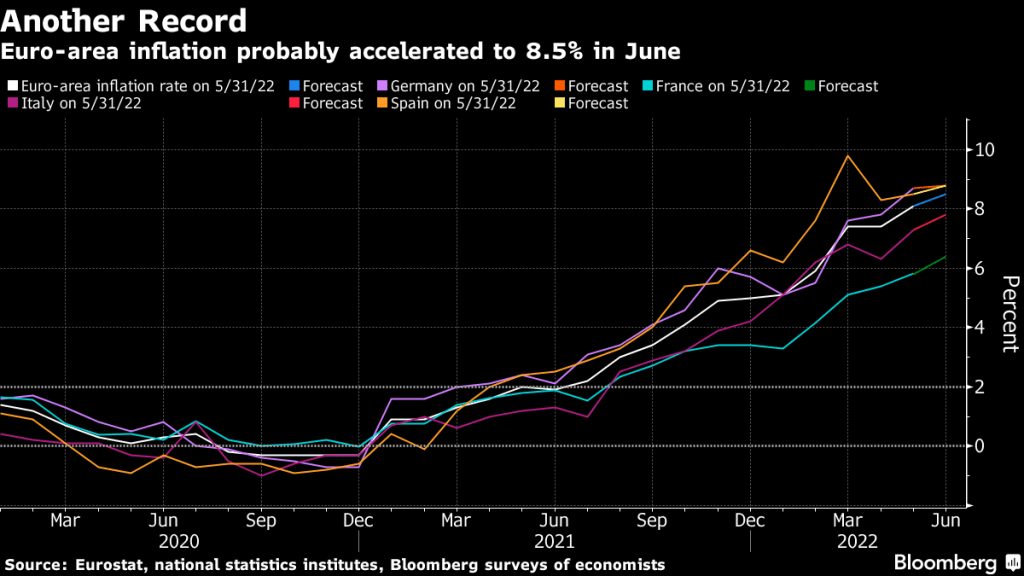

In other words, Euro-area inflation has exploded in 2021, just like the USA.

But the US also has an inflation problem caused in part by Covid and the government’s reaction to Covid: economic shutdown and massive Federal monetary and fiscal stimulus. The stimulus is still in play.

The bond market is already anticipating an about-face by The Federal Reserve (implied overnight rate peaking at the March 2023 FOMC meeting, then receding.

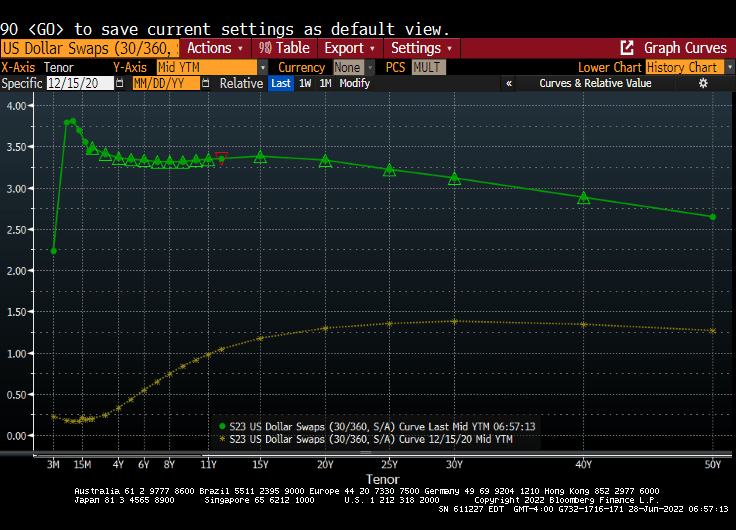

Again, nothing has been the same since the Covid outbreak of 2020 and Fed monetary blitz. Here is the US Dollar Swaps curve before Covid (yellow line) and today’s Fed-enhanced curve (green).

Mortgage rates in the US have climbed to 6% then backed-off slightly. The good ole Back-off Boogaloo as The Fed attempts to unwind its monetary stimulypto.

The French Maginot Line, easily bypassed by German tanks. The Federal Reserve is the US’s Maginot Line. The Yellenot Line??

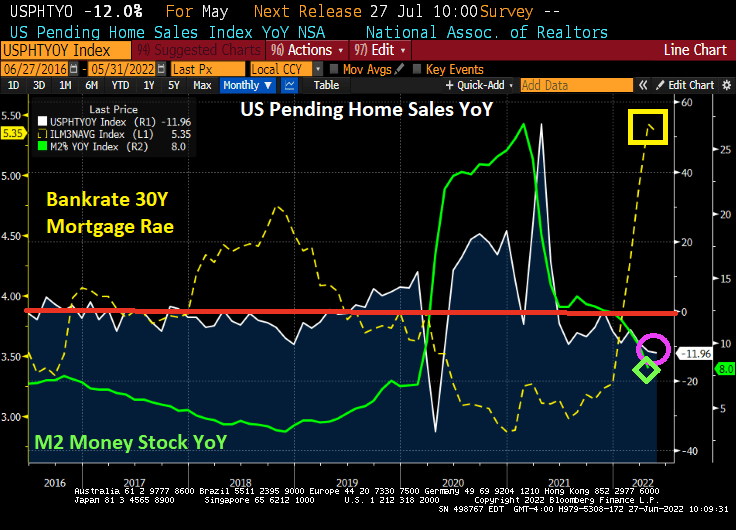

US pending home sales declined -12% YoY in May as The Fed cranked up mortgage rates. That was 11 out of the last 12 months had declining pending home sales.

Consumers are healthy? It is true that the US U-3 uemployment rate is low (3.6% versus 14.70% in April 2020 thanks to government shutdowns over Covid). But even though unemployment is low, consumer sentiment is at its lowest point since 1977.

Generally, consumer sentiment is high when unemployment is low, but not this time around. Currently, inflation is at the highest level since March 1980 even though consumer sentiment bottomed-out in April 1980.

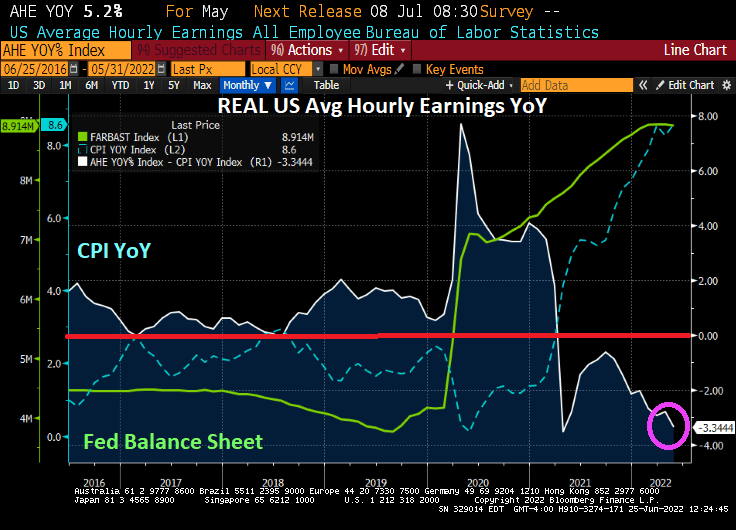

Here is my chart showing that REAL average hourly earnings growth YoY is negative and getting worse, hardly a sign of “healthy consumers.”

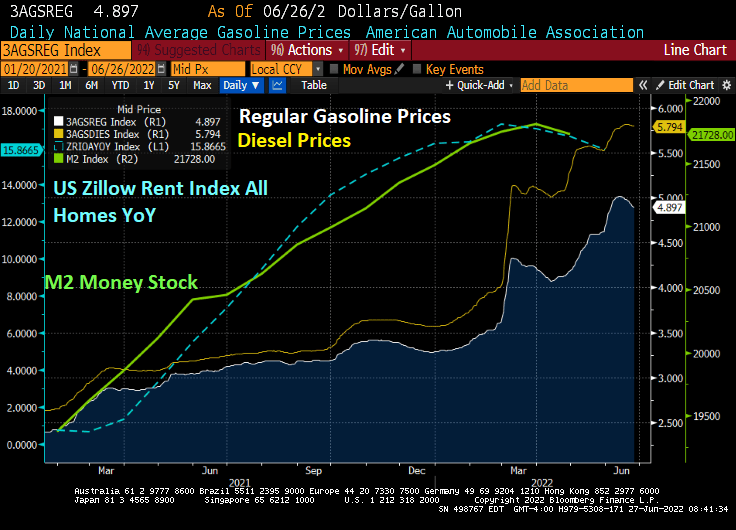

Of course, rising gasoline and diesel prices have risen dramatically since 2021, but are declining slightly thanks to the global economic slowdown (read “lower demand”).

And a M2 Money Stock (green line) declined, US rents (blue line) declined as well.

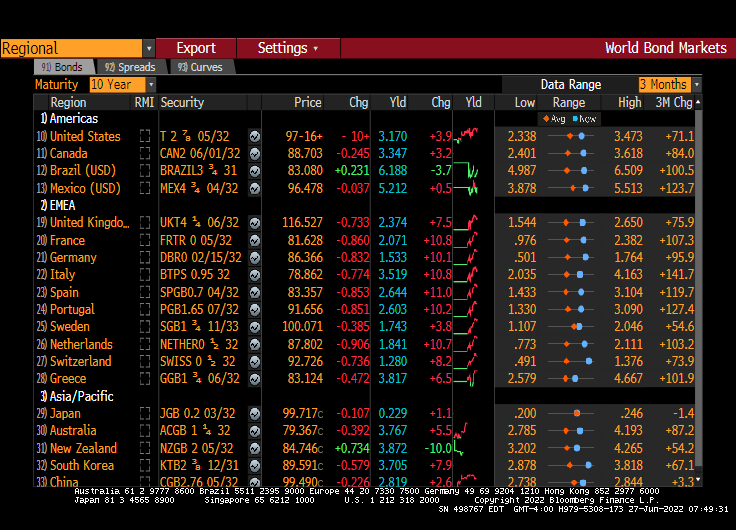

Russia defaulted on its foreign-currency sovereign debt for the first time in a century, the culmination of ever-tougher Western sanctions that shut down payment routes to overseas creditors.

For months, the country found paths around the penalties imposed after the Kremlin’s invasion of Ukraine. But at the end of the day on Sunday, the grace period on about $100 million of snared interest payments due May 27 expired, a deadline considered an event of default if missed.

It’s a grim marker in the country’s rapid transformation into an economic, financial and political outcast. The nation’s eurobonds have traded at distressed levels since the start of March, the central bank’s foreign reserves remain frozen, and the biggest banks are severed from the global financial system.

But given the damage already done to the economy and markets, the default is also mostly symbolic for now, and matters little to Russians dealing with double-digit inflation and the worst economic contraction in years.

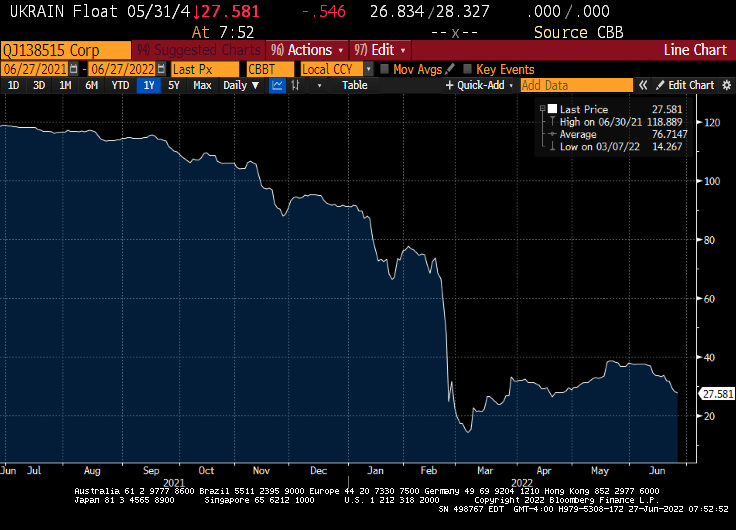

War is hell and Ukraine is paying the price as well.

Meanwhile, European sovereign bond yields are up over 10 basis point this morning, but not UK and Sweden (non-ECB nations).

You must be logged in to post a comment.