I love listening to Fed talking heads (or Fear The Talking Fed). They mostly seem to acknowledge that inflation is a problem and that the excessive monetary stimulus should be reduced.

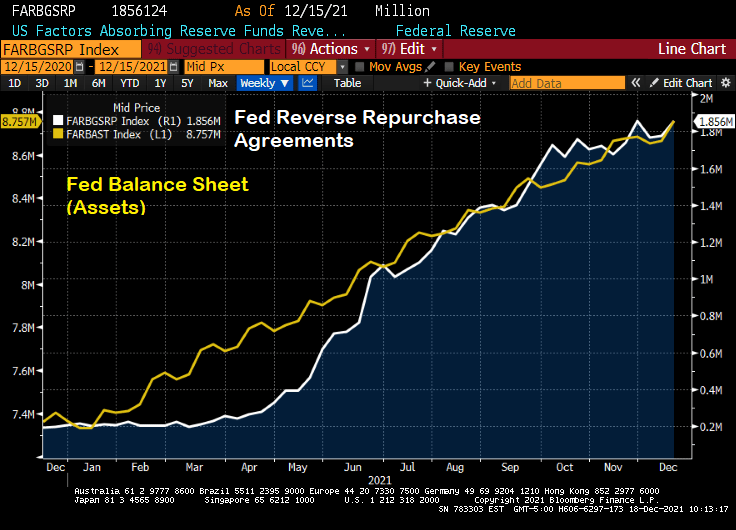

But then I see the chart of The Fed’s balance sheet and The Fed’s reverse repo operations.

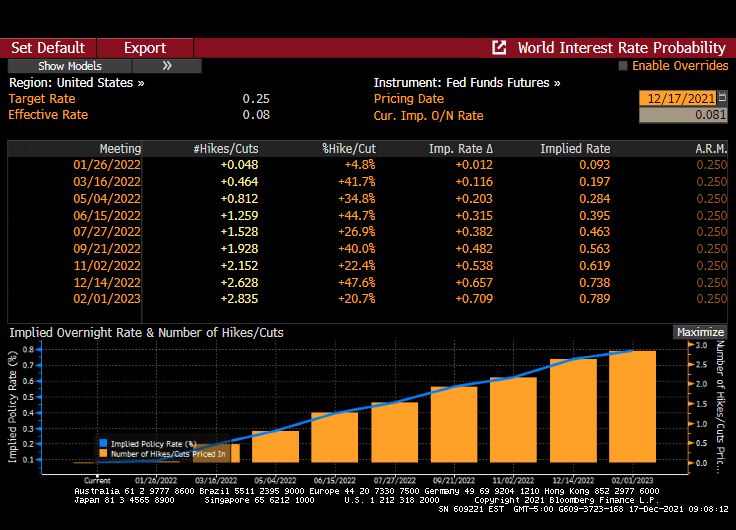

Then we have Federal Reserve Governor Christopher Waller saying that Th Fed could start raising interest rates as early as its March 15-16 meeting, after deciding to end asset purchases sooner than planned. My question is … why wait until the March meeting?

Is it fear of the Omincron Variant (which sounds like a Frederick Forsyth thriller)? Does The Fed not want to rock the boat prior to the Christmas season? The US is at or near full employment, so what is the real reason for delaying a rate increase until March or June? Or the fear that Congress won’t pass Biden’s Build Back Better Act?

Fed Funds Futures infer that one rate hike will occur at the June Fed Open Market Committee (FOMC) meeting and one at the November meeting.

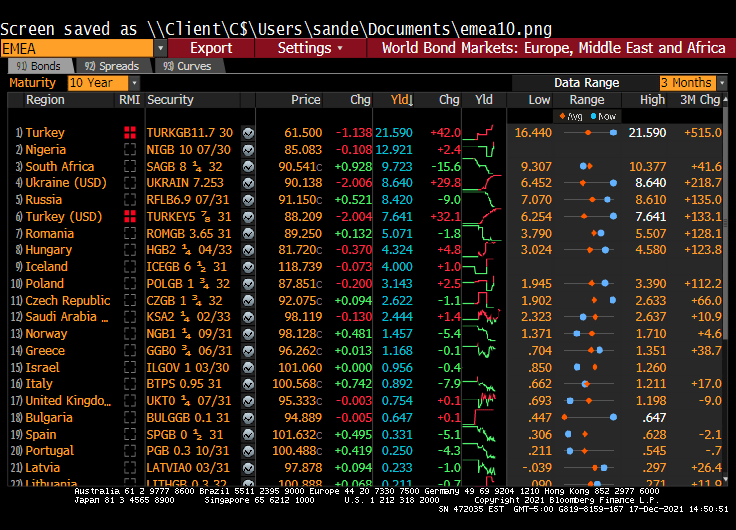

Turkey (the nation, not the bird) is now the Venezuela of Europe/Middle East, where insane government policies are destroying both nations.

(Dow Jones) — Turkey’s central bank intervened to arrest the plunge in the country’s currency, which lost as much as 8% of its value against the dollar on Friday in an ongoing crisis that is straining the country’s financial system.

The crash followed another decision by the central bank on Thursday to cut interest rates under pressure from President Recep Tayyip Erdogan, who favors lower rates as a part of a vision to grow the Turkish economy. Mainstream economists have urged the government to raise interest rates to control Turkey’s rising inflation, which reached more than 21% last month, according to official statistics.

The ongoing plunge is putting increasing pressure on ordinary Turks who have seen their savings evaporate, and adding to pressure on the banking system which has high levels of foreign-currency-denominated loans to repay within the next 12 months.

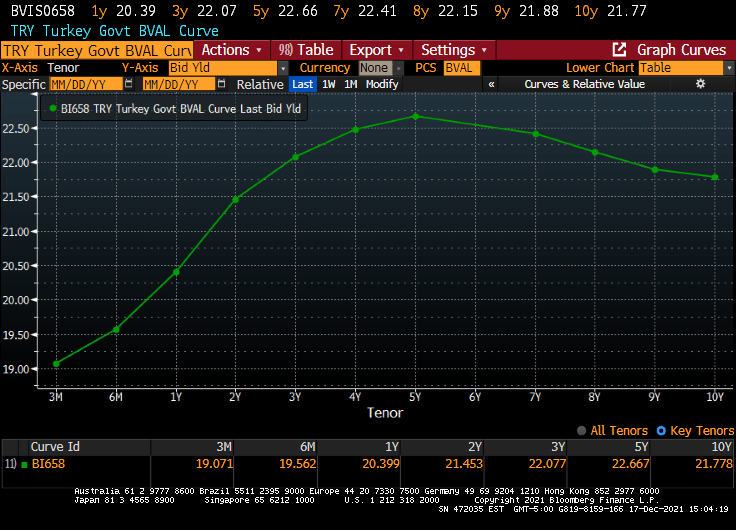

Wow. Turkey’s 10-year sovereign yield rose 42 BPS today to 21.590%. Turkey is looking like the Venezuela of Europe and the Middle East.

The Turkish sovereign curve in their home currency is humped.

But the Turkish yield curve (in US Dollars) looks more like the US Treasury actives curve.

The Turkish Lira is crashing against the US Dollar.

Meanwhile, the Central Bank of Turkey is cutting their repo rate as inflation soars. WTF???

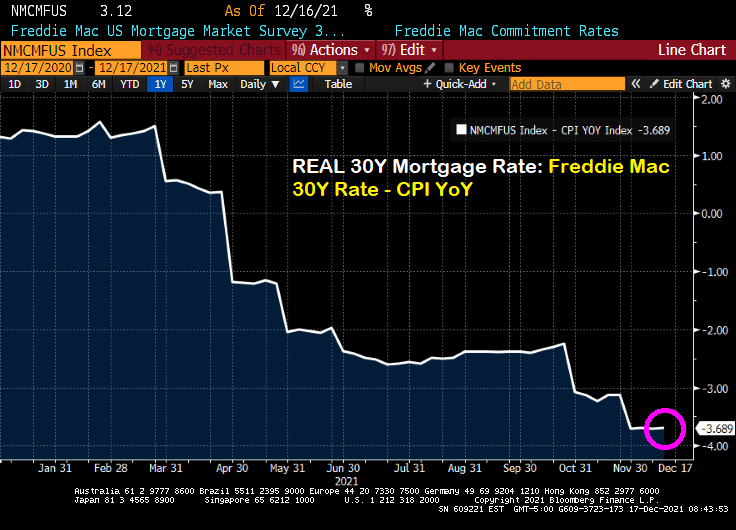

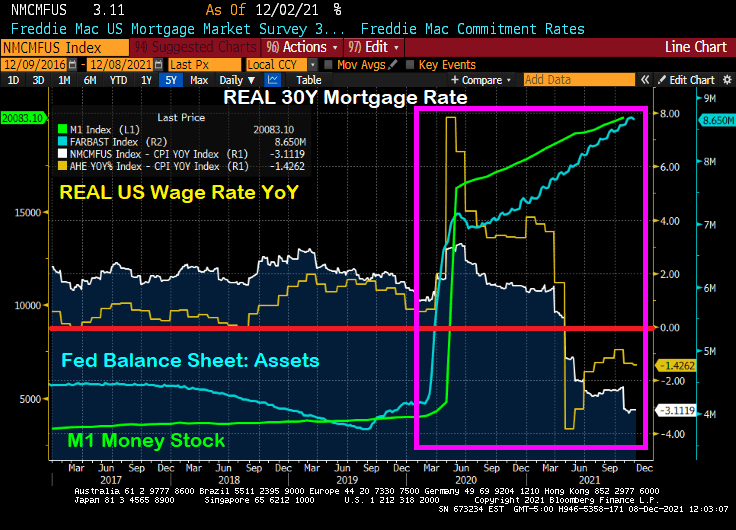

The Freddie Mac 30-year mortgage commitment rate rose to 3.12%. But once we subtract the gut-wrenching inflation rate, the REAL 30-year mortgage rate is -3.689%.

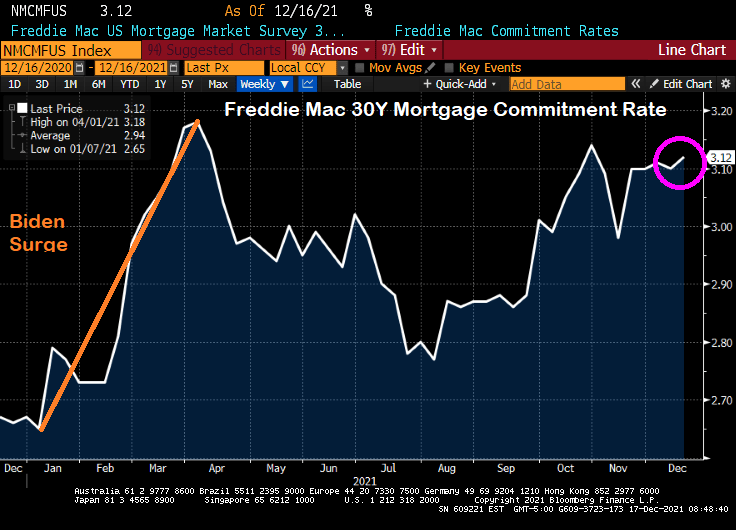

The nominal Freddie Mac 30-year commitment rate rose to 3.12% which is still lower than 3.18% back on April 1, 2021 after surge in rates following Biden’s taking the office of Presidency in January.

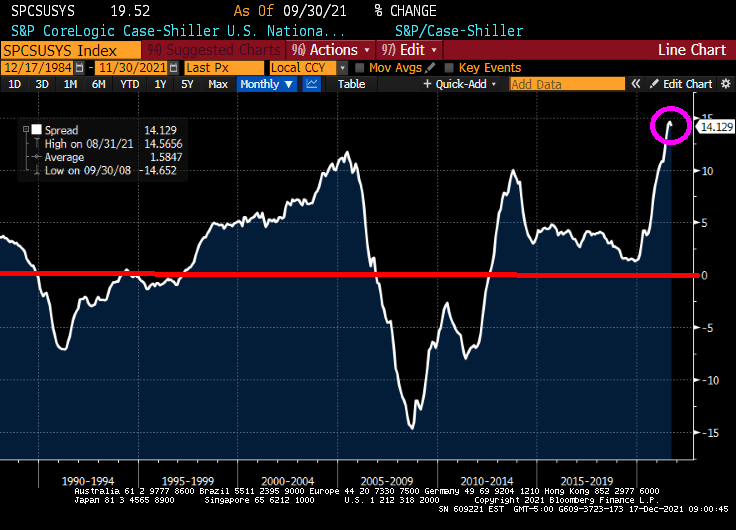

Meanwhile, the REAL Case-Shiller National home price index (CS National YoY – CPI YoY) is growing at the fastest rate in history. Great if you already own a home, but lethal if you are renting and want to move to homeownership.

Meanwhile, REAL wage growth is at -1.94% YoY.

Well, Chairman Powell and The Gang failed to raise the Fed Funds Target Rate yet again, but let us know that they will tighten someday soon. The Fed Funds Futures are signalling a rate hike at the June 2022 meeting and another at the November meeting.

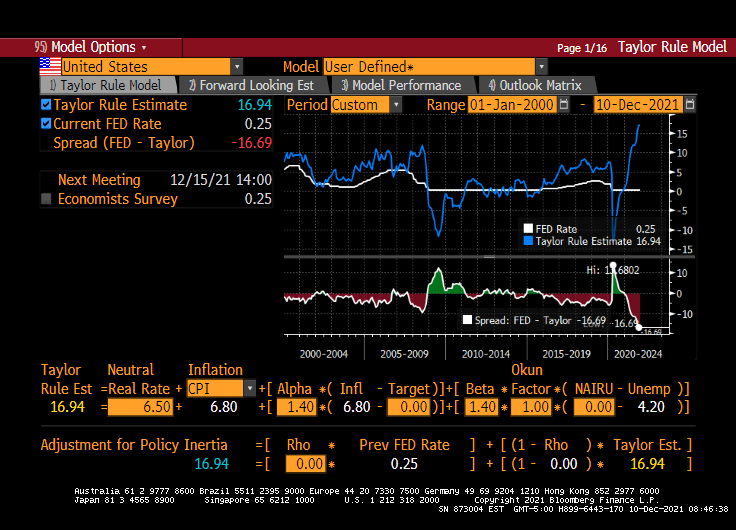

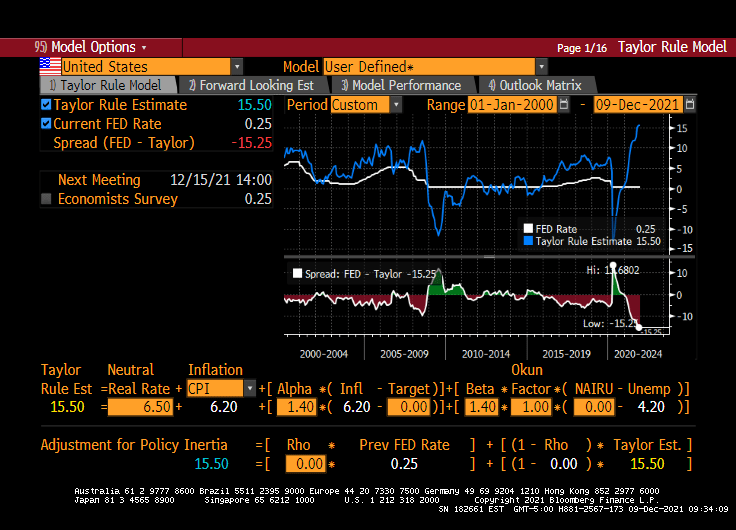

While The Fed couldn’t care less about the Taylor Rule, it is still interesting to note just how out of touch The Fed FOMC is with reality. The Taylor Rule indicates that their target rate should be 16.94% rather than the current target rate of 0.25%.

Keeping the target rate unchanged in the face of gut-wrenching inflation is a bold strategy, Cotton.

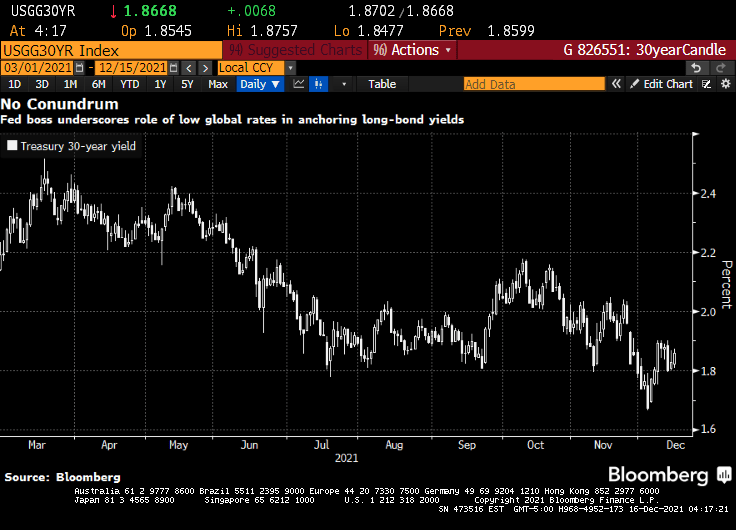

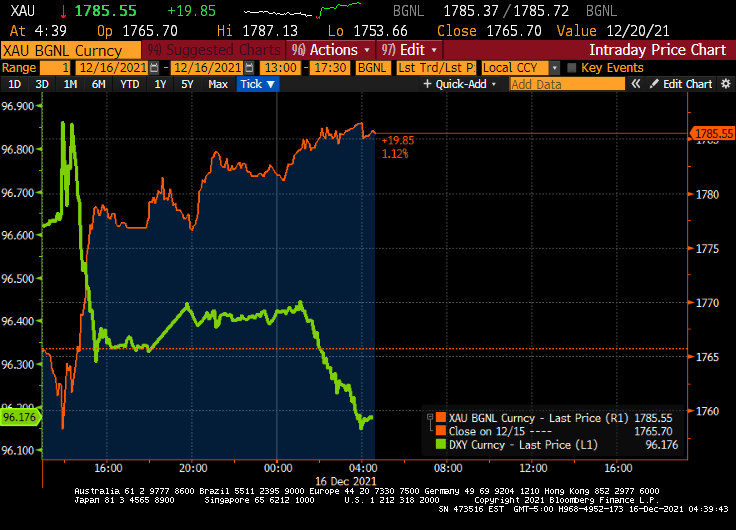

Like John Belushi from The Blues Brothers, Fed Chair Jerome Powell is saying that the markets lackluster response in terms of bond yields to his “hawkish” announcement yesterday “isn’t his fault.”

(Bloomberg)Federal Reserve boss Jerome Powell appears unperturbed by the fact that longer-term bond yields remain low even as officials lay the ground work for tighter policy and inflation is ticking higher.

While the drop in longer-term rates may be viewed by some as indicative of where so-called terminal rates for U.S. policy might ultimately lie, Powell on Wednesday emphasized the impact of ultra-low yields in places like Japan and Germany in helping to keep them anchored.

“A lot of things go into the long rates and the place I would start is just look at global sovereign yields around the world,” Powell said at a news conference following the Fed’s final scheduled policy meeting for the year, which saw officials ramp up the pace of stimulus withdrawal and boost predictions for rate hikes in 2022. The Fed Chair noted that rates on Japanese and German government bonds are “so much lower” than those on Treasuries and that with currency hedging taken into account American debt provides investors with a higher yield. “I’m not troubled by where the long bond is,” he said.

This stands as something of a contrast to the view expressed back in 2005 by one of Powell’s predecessors. Back then, Fed chief Alan Greenspan described a decline in long-term bond yields even in the face of six policy rate increases as a “conundrum.”

Or it could be that no one REALLY believes that Central Banks will ever cut interest rates, despite surging inflation.

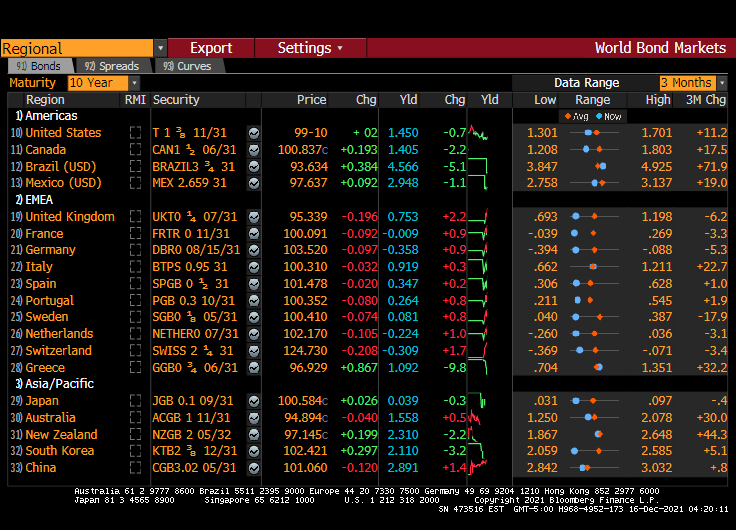

The US Treasury 10-year yield dropped 7 basis points overnight and remains just south of 1.50%. The Eurozone remains below 1% (with Germany at -0.358% and France at -0.009% at the 10-year mark). Japan is at 0.039%. This is what Powell means by low global rates keeping US long-term rates down.

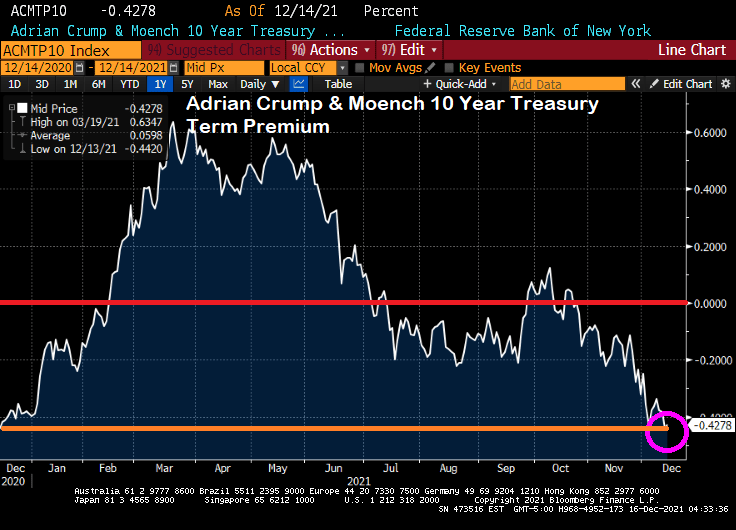

The 10-year Treasury term premium (measured before Powell’s head fake on raising rates) has returned to pre-Biden levels.

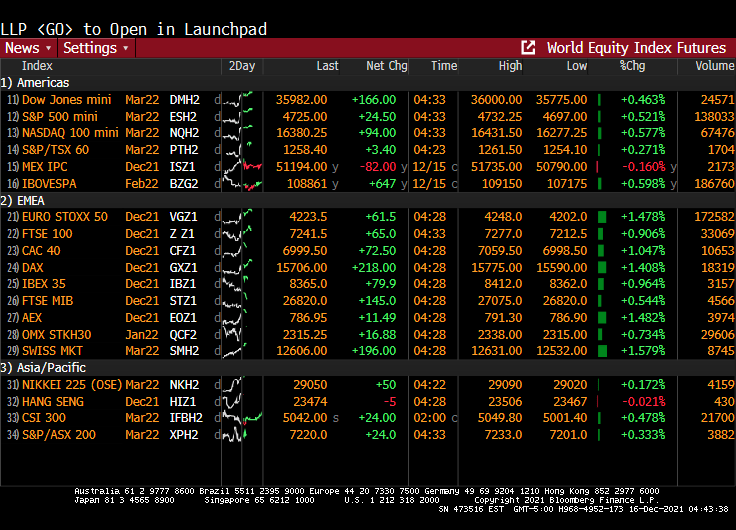

Meanwhile, global equities futures are up across the board (well, except for Mexico).

The Fed could have raised their target rate if they were REALLY interested in cooling inflation. The Taylor Rule remains at 14.94% while The Fed is stalled at 0.25%. Even if you don’t like the Taylor Rule, it still highlights how ridiculous Fed Stimulypto is.

Well, we do have a government-propelled economic recovery, but at a cost of declining REAL wages thanks to the highest inflation rate in 40 years.

If price stability is squandered, financial stability is put at risk. If financial stability is lost, the economy is imperiled and the social contract is threatened.

During the past several quarters, U.S. inflation has surged—now running about triple the Federal Reserve’s 2% target. The surge in prices is unlikely to reverse on its own. The longer that prices are unstable, the greater the challenge to the conduct of macroeconomic policy. The last thing the country needs is its third major economic upheaval in a decade and a half.

The consequences of inflation—and the attendant risks—have long been understood. In 1898 economist Knut Wicksell explained: “Changes in the general level of prices have always excited great interest. Obscure in origin, they exert a profound and far-reaching influence on the whole economic and social life of a country.”

I agree with the op-ed, but as Paul Harvey liked to say, “And now for the rest of the story.”

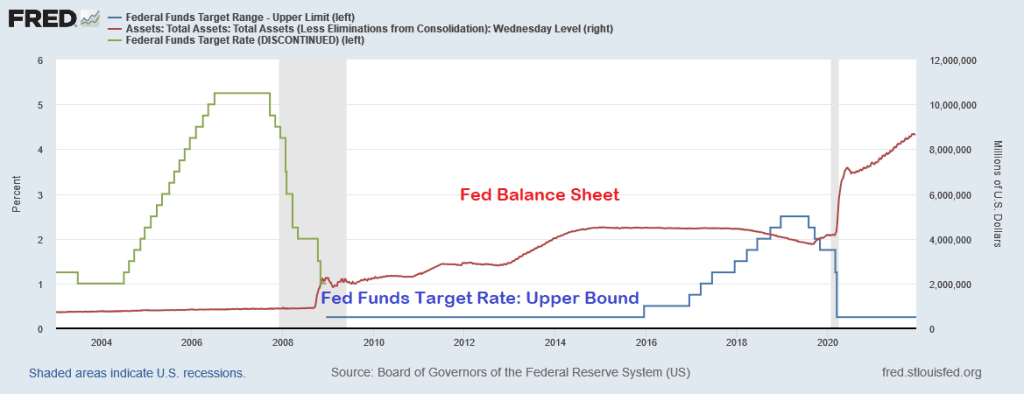

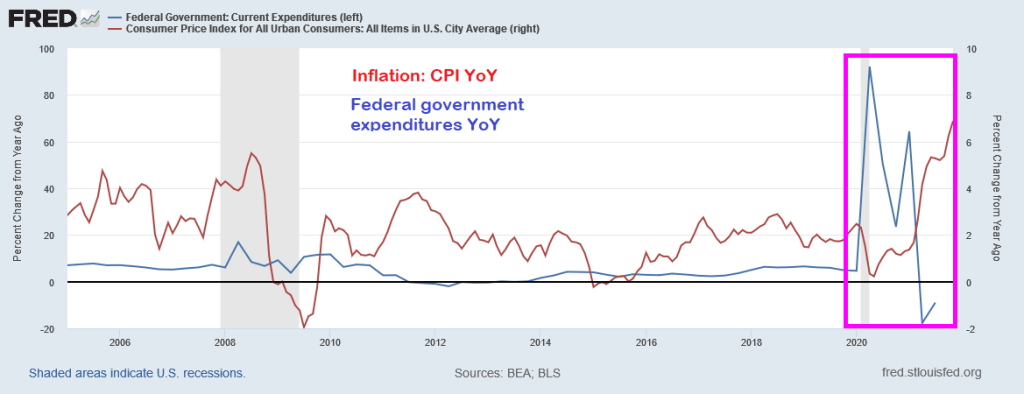

The Federal Reserve is only half of The Federal government “Stimulypto.” Starting in late 2008, The Fed crashed their target rate to 25 basis points and began their quantitative easing (QE) program where The Fed purchased Treasuries and Agency Mortgage-backed Securities (MBS) amongst other assets. Notice in the chart below that QE was adjusted, but never went away and The Fed’s target rate only was increased once before Trump’s election as President, then raised eight times then decreased five times. And no rate increases under Biden. So The Fed scorecard is Obama/Biden: 1 rate increase. Trump: 13 rate changes. And The Fed’s balance sheet has gone bananas since the COVID outbreak.

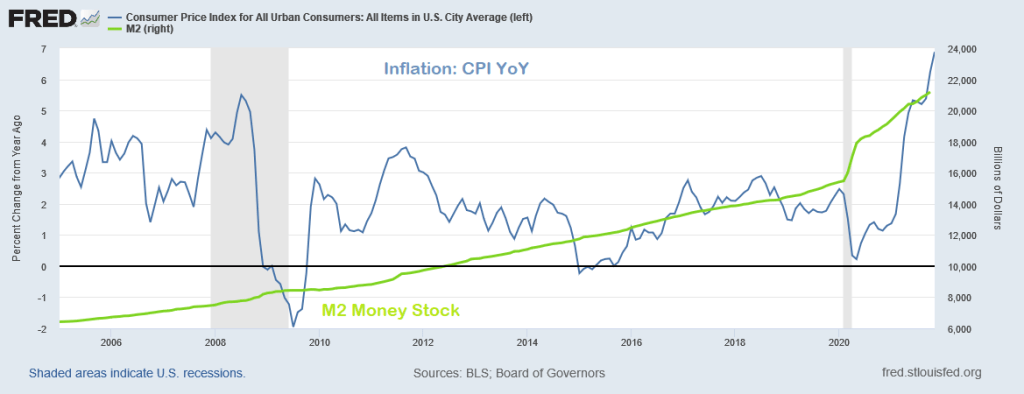

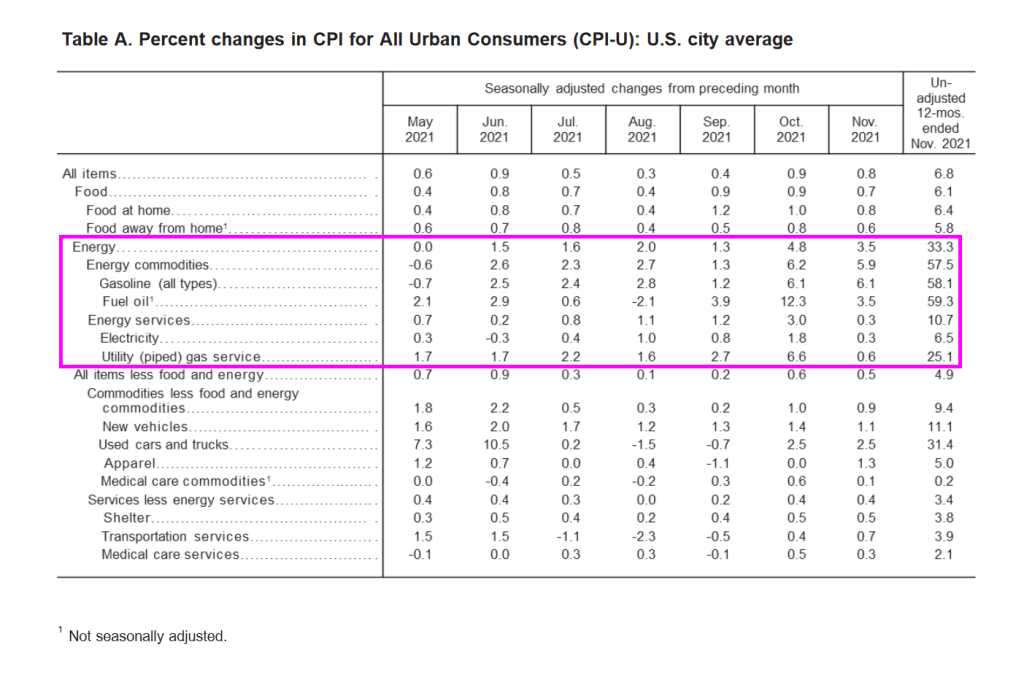

Inflation, as measured by the Consumer Price Index (CPI) didn’t really take-off until March 2021 as a result of STIMULYPTO (excessive monetary stimulus + Federal government spending).

Here is the Federal government spending surge that helped generate the highest inflation in a generation.

So while the op-ed author blames inflation solely on The Federal Reserve, The Fed was unable to achieve its inflation goal for much of the post-financial crisis period. It was the double whammy of Fed monetary stimulus + Federal government stimulus (spending) that pushed inflation to 6.8%.

Following Paul Harvey’s “The Rest of the Story,” I choose baseball player Whammy Douglas to represent the double whammy of Fed + Fed government stimulus to produce inflation. THAT is the rest of the story.

Throw in the Biden Administration’s war on fossil fuels (driving up energy costs by over 50%) and we have a TRIPLE WHAMMY!!

The WSJ op-ed author was focused only blaming The Fed. Sorry, it was a Double Whammy.

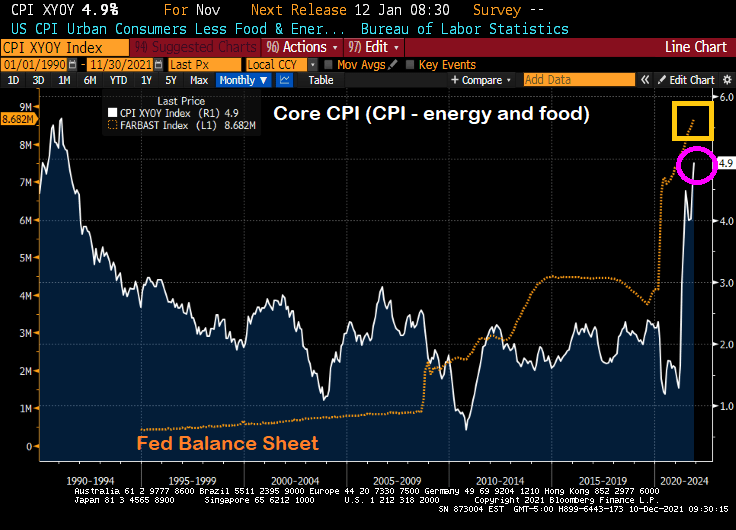

Inflation-adjusted return of Treasuries fell to lowest since the 1980s. For bond investors, this is their version of Kevin’s Famous Chili from The Office! Or The Fed’s Famous Chili!

(Bloomberg) — Treasury investors are losing more money than they have in four decades, once inflation is taken into account. And if markets are right, they’re unlikely to come out ahead for years.

The federal government’s debt has already lost about 2% outright over the past year as the Federal Reserve started removing pandemic-era stimulus from the economy and inched closer toward raising interest rates. But on top of that, the consumer price index has surged 6.8%, putting investors even deeper in the hole.

Taken together, that’s resulting in the worst real returns — or those adjusted for inflation — since the early 1980s, when then Fed Chair Paul Volcker was in the midst of fighting a wage-price spiral. What’s more, the dynamic isn’t expected to change: The bond market is projecting that 10-year Treasury yields will hold below the inflation rate for the next decade, meaning any investment income will be more than wiped out by the rising cost of living.

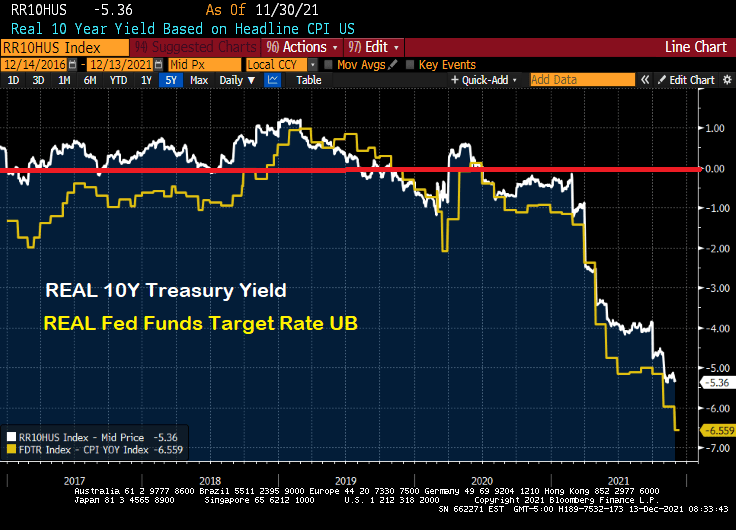

If we look at the REAL 10-year Treasury yield and REAL Fed Funds Target Rate, they are both negative.

Let’s see if Powell spills his famous chili on Wednesday at 2:00PM EST. The Fed keeps saying they are serious about controlling inflation, just like Kevin Malone.

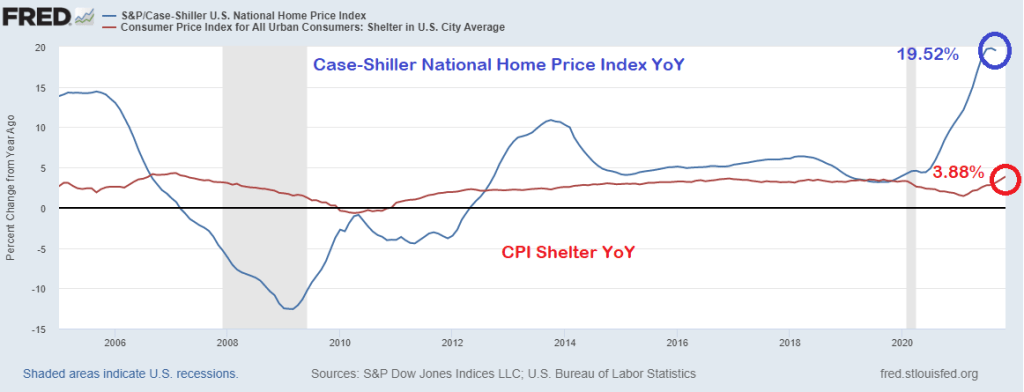

But that 6.9% YoY is very misleading because of the strange way the Bureau of Labor Statistics measures the largest asset in most households’ expenditures: housing.

The BLS measures inflation in housing using the Shelter measurement. Which was only 3.88% YoY. The problem is that the Case-Shiller National Home Price Index was 19.52% in its last reading. That is quite a discrepancy.

So, if we substitute the Case-Shiller National home price index for the CPI Shelter, we get an inflation rate of greater than 11%.

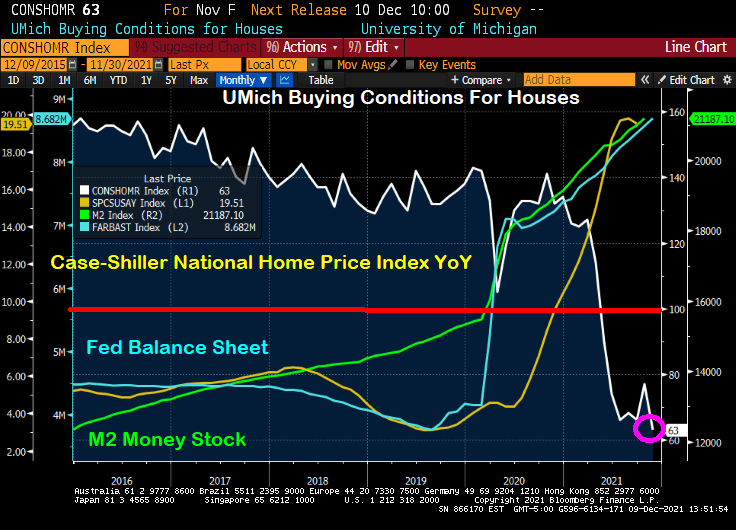

Just look at this chart of the University of Michigan Buying Conditions For Houses index. It was positive (meaning above 100) until shortly after COVID struck and The Federal Reserve rode to the rescue. National home price growth was already at 4.57% YoY in March 2020, then ballooned to 19.51% YoY at the last reading.

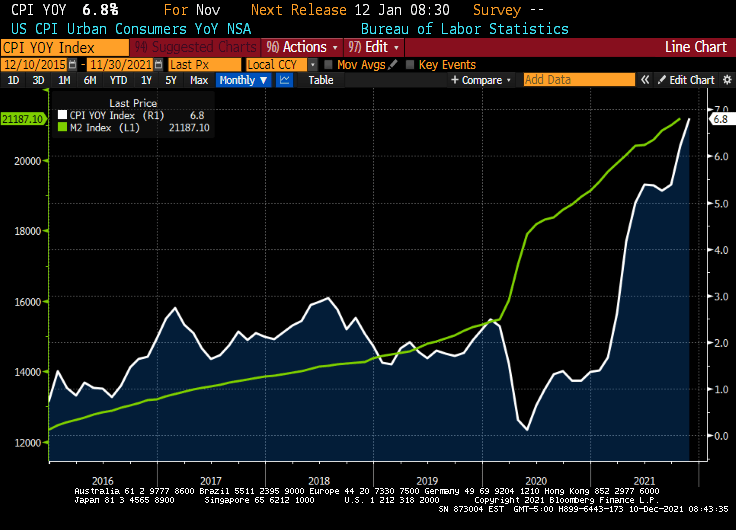

Here is the same chart with the broader M2 Money stock and The Fed’s Balance sheet. Same results, just not as dramatic as M1.

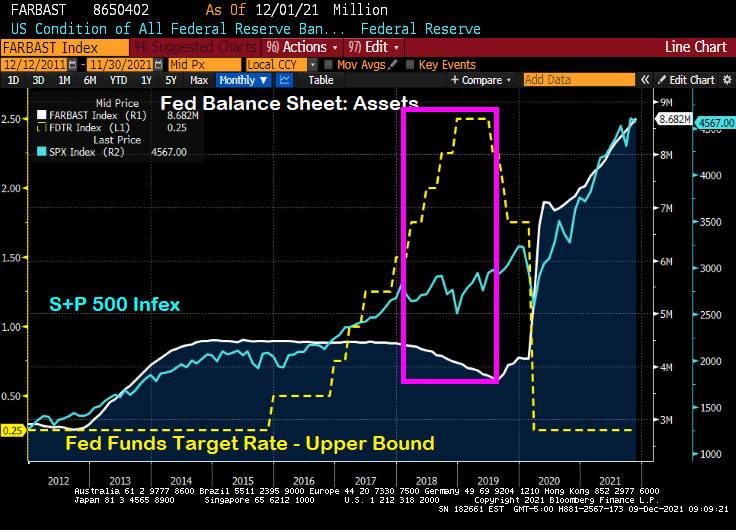

We will soon find out if The Federal Reserve will announce a rate hike or taper news. They are likely to confirm tapering, particularly if they believe that tapering won’t roil markets. After all, then Fed Chair Janet Yellen and the FOMC decided to let the Fed’s balance sheet taper (white line) while, at the same time, increasing the Fed’s target rate (yellow line). The S&P 500 index rose 9.5% over the taper/rate increase period of 12/29/2017 to 8/30/2019.

But since Stimulypto (2/28/2020 to 11/30/2021), the Fed’s balance sheet doubled+ from $4,158,637 to $8,681,771. And The Fed Funds Target Rate (UB) immediately fell from 1.75% in February 2020 to 0.25% in March 2020 … and has stayed there ever since. The S&P 500 index rose 54.6% over this Stimulypto period.

But The Fed’s upcoming decision on December 15, 2021 may be a Yellen-pivot (taper balance sheet, but raise The Fed Funds Target rate). But, then again, maybe not. The Fed is getting really bad about forward guidance and choose instead to surprise us. Hence, this is why an a-political rule is preferred (such as the Taylor Rule).

Unfortunately, the Taylor Rule infers a Fed Funds Target rate of 15.50% (using CPI YoY running at 6.20% YoY. If The Fed raises their target rate by 25-50 basis points at the December 15th meeting, color me surprised.

So, the Powell Pivot may just be the Yellen Pivot after all.

You must be logged in to post a comment.