Unlike Archie Bell and the Drells, this tighten-up is about The Federal Reserve tightening-up its monetary policy.

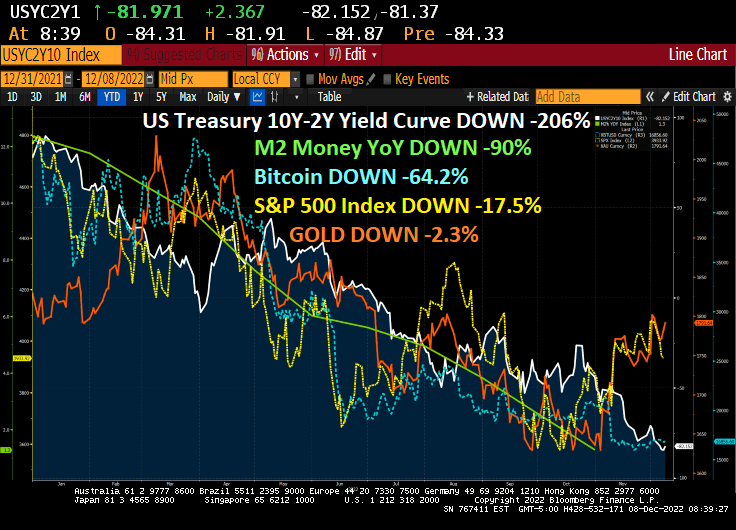

On December 31, 2021, the US Treasury yield curve (10Y-2Y) stood at +77.4 basis points, generally a good omen.

Then markets woke up. And not in a woke way.

As The Fed tightens to tamp down on inflation in 2022, we are seeing a pattern. The US Treasury 10Y=2Y yield curve has sunk to -82 basis points, a -206% decline.

In addition to the inversion of the US Treasury yield curve we have witnessed M2 Money growth declining -90%, the S&P 50) index down -17.5%, Bitcoin down -64.2% and gold down only -2.3%.

But we now have to worry about Project Cedar, a seemingly innocent project to replace the US Dollar. A new digital currency would allow Washington DC to monitor your purchases and behavior. And perhaps create a Social Credit Score like in China measuring how well you conform to Biden’s notion of a utopian, green society.

And the US yield curve has been inverted for 109 straight days.

The Fed has signaled the terminal rate will likely be around 5% — we think an upper bound of 5% — reached in early 2023. To get there, the central bank will likely raise rates by 50 basis points at its December 2022 meeting, followed by two more 25-bp hikes in 2023. We then see it holding at 5% throughout the year. Markets have priced in a similar amount of tightening.

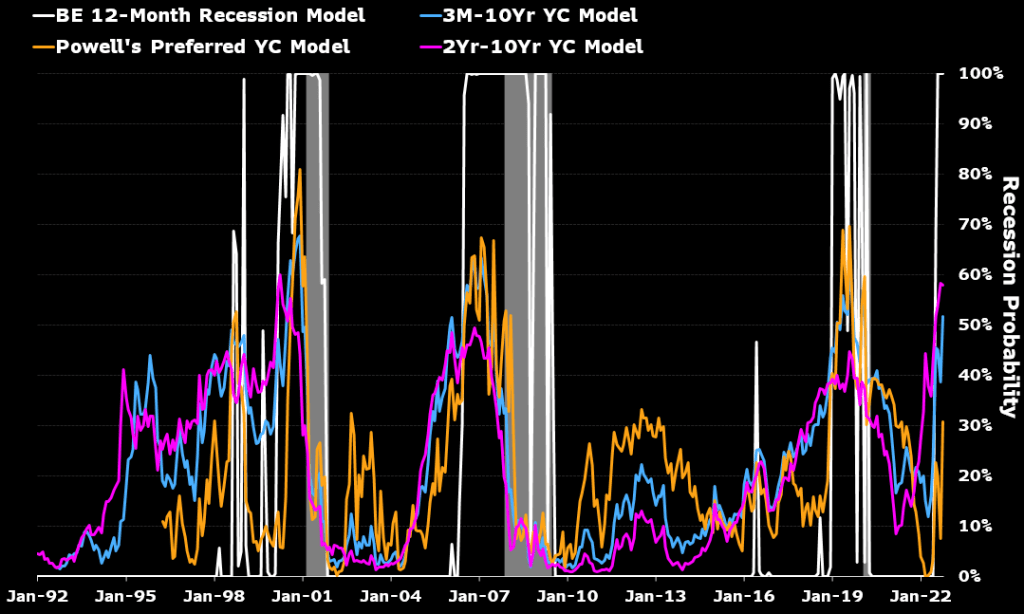

Controlling inflation comes at a cost to growth. Yield curves have inverted. A Bloomberg Economics model shows a 100% probability of recession starting by August 2023. Take that — like all model forecasts — with a grain of salt. But the basic view that aggressive Fed tightening will very likely tip the economy into a downturn is correct.

While various measures of impending US recession show a good chance of a 2023 recession, Powell’s preferred measure of the yield curve shows only a 30% chance.

What Might the Recession Look Like?

We project a 0.9% GDP contraction in 2H 2023, driven by an investment downturn as firms pare inventories amid a downshift in consumption. Residential investment will also contract with real interest rates likely to rise steadily throughout 2023 as nominal rates stay high and inflation moderates.

An Inventory-Led Downturn

Resilient consumption should help put a floor under demand.

Households have enough of a cash buffer — extra savings built up over the course of the pandemic, rising COLAs for Social Security recipients, ongoing state and local government stimulus and solid 2022 wage income growth — to sustain consumption during the recession. Our base case is for real spending to grow at a quarterly annualized pace of about 0.5% in 2023, with strength concentrated in services.

By one measure, households may still have $1.3 trillion in the coffers, based on flows within the personal income report through September. At the current rate of drawdown, that’s enough to last around 15 months, or through the end of 2023. Funds may dry up faster as job losses mount and the unemployed fall back on their savings.

$1.3 Trillion Extra Savings to Keep Spending Positive

The labor market remained exceptionally tight into the end of 2022. We expect it to soften significantly next year, with the unemployment rate rising to 4.5% by the end of 2023. The pace of hiring will slow markedly as support from catch-up hiring dissipates and the effects of restrictive monetary policy settle in. We estimate only 20%-30% of total employment is still in sectors experiencing labor shortages, implying demand for labor is falling fast.

Avoiding a Hard Landing Depends on Inflation, Fed

Extreme circumstances — the pandemic, Russia’s invasion of Ukraine — have made a recession more likely than not. Extreme circumstances can change, and so can policy makers’ response Whether the US can stick a soft landing depends substantially on how external conditions develop and how the Fed responds.

Not our base case, but we can envision a scenario in which the central bank opts to ease rates in 2023, boosting the chances of a soft landing.

One way that could happen is inflation falling faster than expected. Currently, our baseline is for headline CPI to drop to 3.5% and the core to 3.8% by the end of 2023. The most important assumption there is that energy prices remain flat next year from 2022.

In an alternative scenario, inflation fall faster as China maintains Covid controls and growth stumbles. A Bloomberg Economics model attributes the recent fall in oil prices entirely to a drop in demand — mainly from China. If China’s growth falls off the cliff, perhaps amid a sharp rise in Covid cases and resumed lockdowns, commodity prices could tumble sharply.

A warm winter in Europe and the US could also keep energy prices in check. Lower demand from Europe for US liquefied natural gas would help stem the increase in domestic electricity prices.

In that scenario, US energy prices could fall 20% in 2023 and headline inflation may drop to 2% by the end of the year. Lower gasoline prices would work to soften inflation expectations, easing pressure on the Fed to hold rates at higher level. A rate cut could then come in 2H 2023, raising the possibility of a soft landing.

Scenarios of CPI Inflation in 2023

The risk cuts both ways. A quick and successful pivot to reopening in China could boost oil and other commodities prices. A colder winter in Europe and the US would generate upward pressure for electricity and utility prices. Assuming China is fully open by mid-2023 — the base case for our China team — energy prices could increase by 20% in the year. In that case, headline US CPI would hit a bottom of 3.9% in midyear before surging to 5.7% by year-end.

In that scenario, the terminal fed funds rate would most likely top 5%, possibly closing 2023 near the upper end of St. Louis President James Bullard’s estimated restrictive range of 5%-7%.

Bloomberg Economics US Forecast Table

Thanks to Yellen’s legacy of too low interest rates for too long, The Fed is playing catch-up by finally raising rates.

The start of a new week and the US Treasury 10-year yield is up 10 basis points, always a noteworthy change. And with it, the 30-year mortgage rate should climb.

Since Biden/Pelosi/Schumer are in a lame duck session with Republicans taking the House in January, let’s see if Republicans can halt the insanity in Washington DC.

Be that as it may, Fed Funds Futures are pointing at a 50 basis point rate hike at the December 14th FOMC meeting.

Seriously, how is The Federal Reserve going to cope with $204 TRILLION … and growing Federal debt AND unfunded liabilities?

We are truly living in Strange Days under Joe Biden. And with Elon Musk’s release of Twitter’s suppression of the Hunter Biden laptop scandal, they call Joe Biden the Sleaze.

As The Federal Reserve tries to crush Bidenflation, we are seeing Fed Remittances to the US Treasury soaring (white line). At the same time, we see the Biden Administration draining the Strategic Petroleum Reserve (orange dashed line). And as The Fed tightens, M2 Money growth crashes (green line).

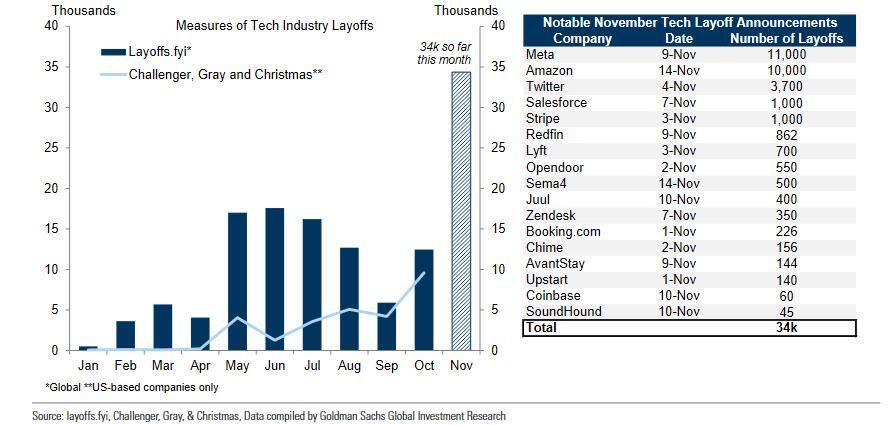

And with tech layoffs, I predict that 2023 job growth will be pretty bad.

As I have discussed before, I am a fan of ADP’s job reports and not a fan of the BLS NFP reports. As M2 Money growth slows, we can see declining ADP jobs added (yellow line), but BLS’s NFP report shows huge spikes.

Lastly, we have Sam Bankman-Fried and FTX. SBF should be in custody for being involved in one of the biggest fraud cases in history, but like Hunter Biden, is roaming free and trying to raise MORE funds. Why are these lapses in justice occuring with “10% for The Big Guy” Biden?

As The Federal Reserve continues its assault on inflation by raising their target rate, Blackstone Inc.’s $69 billion real estate fund for wealthy individuals said it will limit redemption requests, one of the most dramatic signs of a pullback at a top profit driver for the firm and a chilling indicator for the property industry.

Blackstone Real Estate Income Trust Inc. has been facing withdrawal requests exceeding its quarterly limit, a major test for the one of the private equity firm’s most ambitious efforts to reach individual investors. The news, in a letter Thursday, sent Blackstone stock falling as much as 10%, the biggest drop since March.

You can see the problem facing commercial real estate. Since December 31, 2021, NAREIT’s all-equity REIT index has fallen -23.6% while NAREIT’s mortgage REIT index has fallen -28.6%. It looks like Blackstone’s Real Estate Income Trust has a decline coming.

If I look at NCREIF’s commercial property index, we can see that The Fed helped boost CRE values. But what will happen if and when The Fed actually shrinks its balance sheet.

I call The Fed’s attempts at cooling inflation “Fed Dead Redemption” since it resulted in redemptions from real estate funds.

Yes, The US Treasury 10Y-2Y yield curve remains inverted, for the 104th straight day. And Bankrate’s 30-year mortgage rate has dropped -57 basis points since November 3, 2022.

This comes after a gruesome Pending Home Sales and mortgage applications reports today.

The Federal Reserve continues to remove the monetary punch bowl despite the global yield curve inverting and The Fed fighting Bidenflation.

On the mortgage front, mortgage applications decreased 0.8 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending November 25, 2022. This week’s results include an adjustment for the observance of the Thanksgiving holiday.

The Refinance Index decreased 13 percent from the previous week and was 86 percent lower than the same week one year ago. The unadjusted Purchase Index decreased 31 percent compared with the previous week and was 41 percent lower than the same week one year ago.

On the housing front, US pending home sales fell for a fifth month in October as demand continued to sag under the weight of high mortgage rates.

The National Association of Realtors index of contract signings to purchase previously owned homes decreased 4.6% last month, according to data released Wednesday. And fell -36.7% YoY.

All together now. Look at pending home sales YoY and mortgage purchase applications SA compared with M2 Money YoY.

The Covid outbreak of early 2020 begat a massive surge in monetary stimulus which has dissipated. Notice that home price growth is dissipating as well.

Also causing problems for housing is NEGATIVE REAL WAGE GROWTH. While the US is suffering from inflation and decling real wage growth, trading partner Germany has even a worse REAL WAGE GROWTH problem.

The hawkish drumbeat from central bankers is raising fears of a downturn, with global bonds joining US peers in signaling a recession, as a gauge measuring the worldwide yield curve inverted for the first time in at least two decades.

The US Treasury 10Y-2Y yield curve, on the other hand, has been inverted for 107 straight months.

And in Europe, 10-year sovereign yields are dropping like a paralyzed falcon.

The world and US yield curves are pointing to trouble. And drums along the Potomac (DC) and East River (NYC).

You must be logged in to post a comment.